Ref. Debit Credit Debit Credit

30 J3 5,500 5,500

30 J3 3,576 1,924

Ref. Debit Credit Debit Credit

15 J1 1,600 1,600

30 J2 3,900 5,500

Ref. Debit Credit Debit Credit

1 J1 1,700 1,700

Ref. Debit Credit Debit Credit

8 J1 240 240

2014

June

Advertising Expense Account No. 512

Post.

Date Item

Balance

P10. The Complete Accounting Cycle Without a Work Sheet: Two Months (second month optional)

(Continued)

2014

June

Store Rent Expense

Post.

Date Item

Balance

Account No. 511

Date Item

2014

June

Repair Revenue Account No. 411

Post.

Balance

Date Item

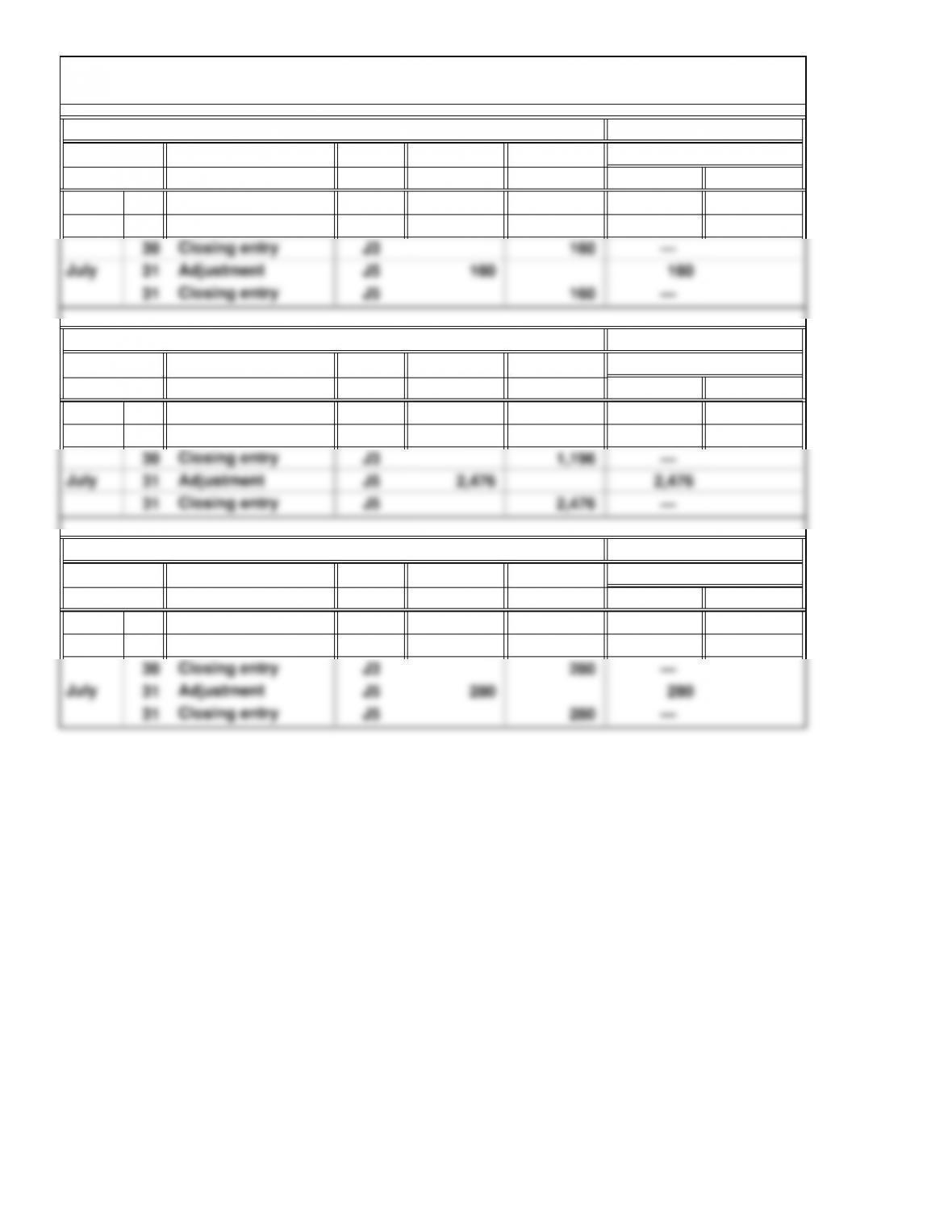

June Closing entry

Closing entry

Income Summary Account No. 314

Post. Balance

2014

4-57

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Ref. Debit Credit Debit Credit

30 J2 160 160

Ref. Debit Credit Debit Credit

30 J2 1,196 1,196

Ref. Debit Credit Debit Credit

30 J2 280 280

P10. The Complete Accounting Cycle Without a Work Sheet: Two Months (second month optional)

(Continued)

Balance

Date Item

2014

June Adjustment

Post.

2014

Depreciation Expense—Repair Equipment Account No. 515

June Adjustment

Date Item Post.

Repair Supplies Expense Account No. 514

Balance

2014

June Adjustment

Balance

Date Item Post.

Insurance Expense Account No. 513

4-58

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

10.

17,324

1,600

Lutz Repair Service

Cash

P10. The Complete Accounting Cycle Without a Work Sheet: Two Months (second month optional)

(Continued)

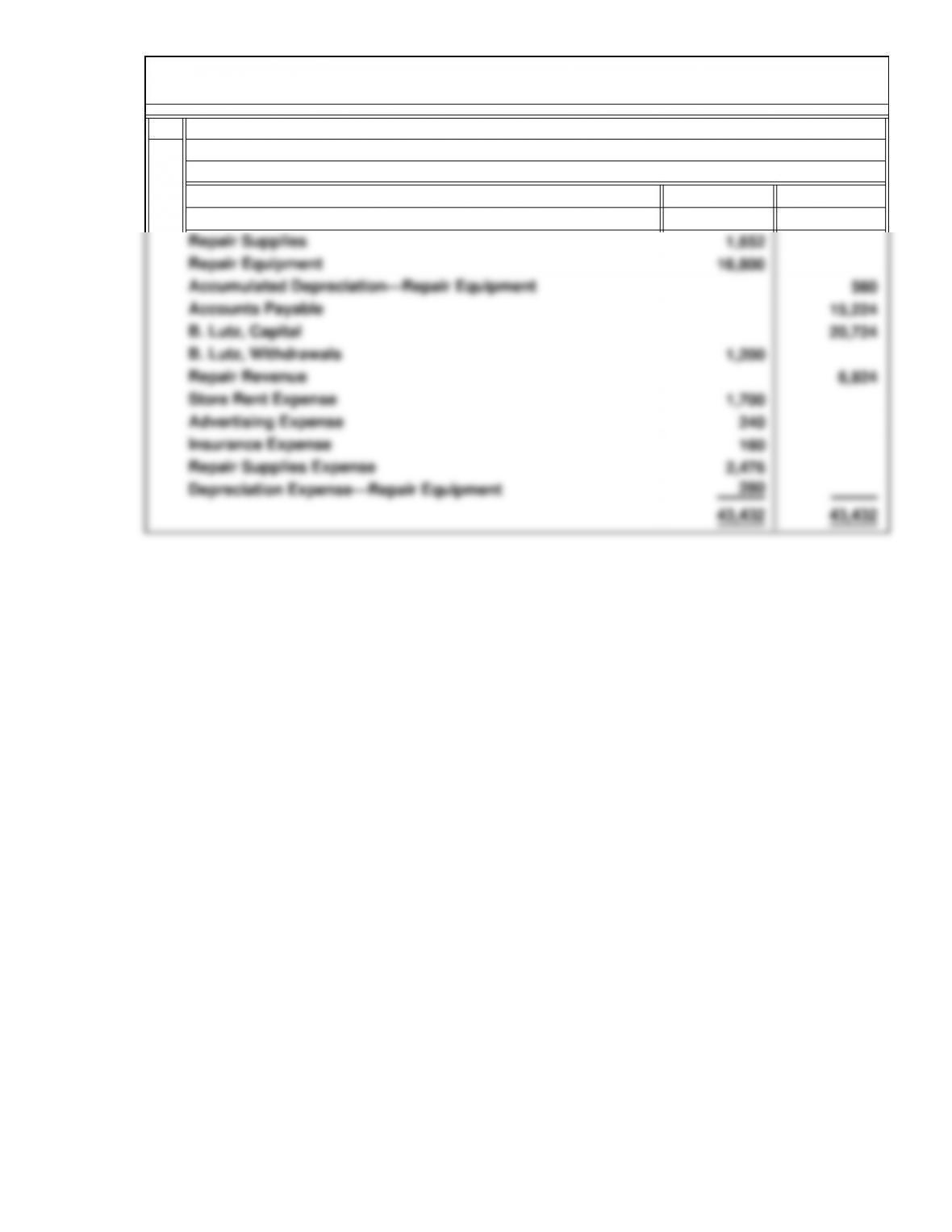

Adjusted Trial Balance

July 31, 2014

Prepaid Insurance

4-59

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

$6,924

$20,724

2,068

Lutz Repair Service

Revenue

Repair revenue

P10. The Complete Accounting Cycle Without a Work Sheet: Two Months (second month optional)

(Continued)

Expenses

For the Month Ended July 31, 2014

B. Lutz, capital, June 30, 2014

Net income

Income Statement

For the Month Ended July 31, 2014

Lutz Repair Service

Statement of Owner’s Equity

4-60

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

$17,324

1,600

13.

17,324

1,600

P10. The Complete Accounting Cycle Without a Work Sheet: Two Months (second month optional)

(Concluded)

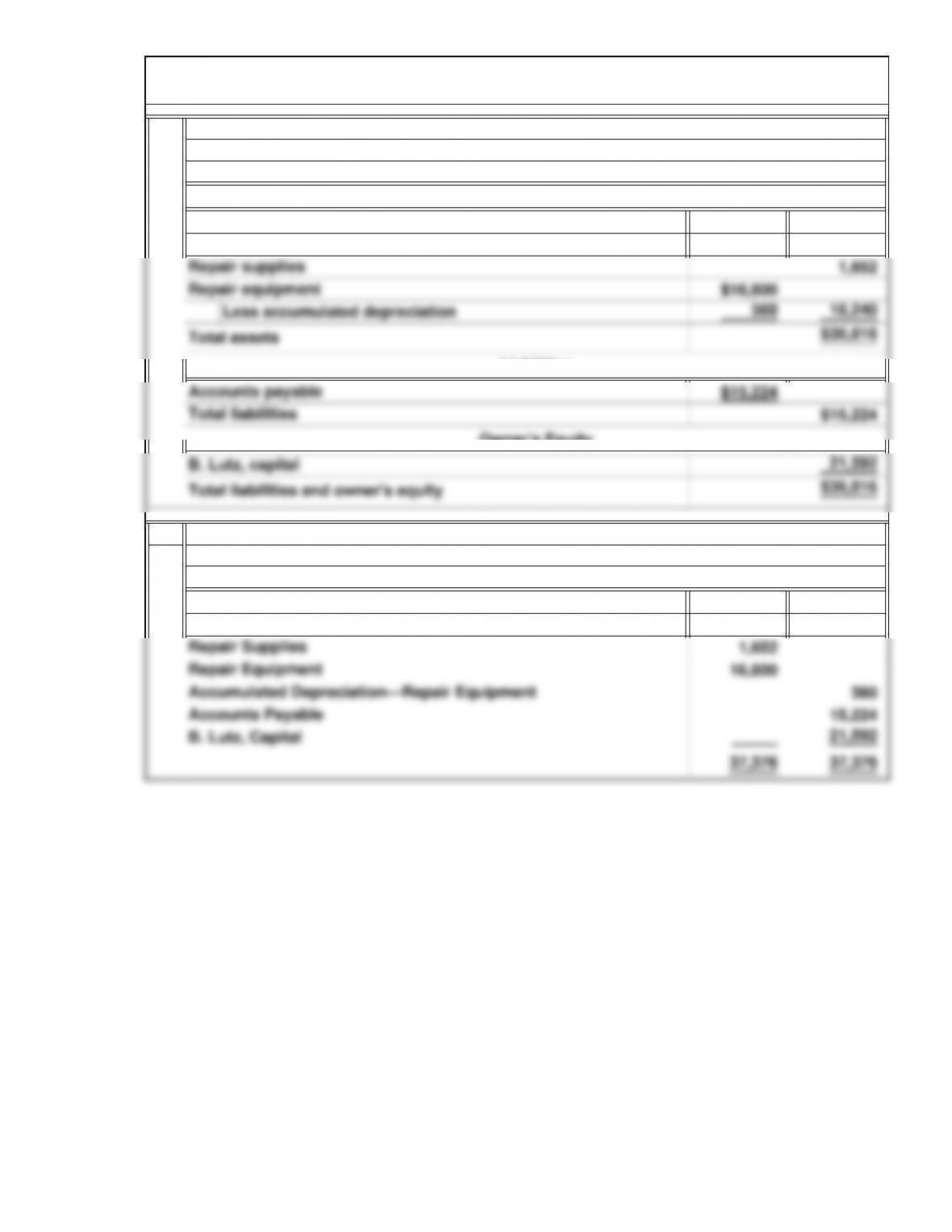

Lutz Repair Service

Post-Closing Trial Balance

July 31, 2014

Cash

Prepaid Insurance

Assets

Cash

Prepaid insurance

Lutz Repair Service

Balance Sheet

July 31, 2014

4-61

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

interest income is accrued at the end of the next period or received as the loans mature

is automatically offset by what has been accrued previously, leaving a balance that repre-

sents the correct interest income for the period.

crued to date. Third, the use of reversing entries is very helpful because they simplify the

process of tracking the interest accrued to date. Each month the amount of the accrual is

reversed, becoming a negative amount in the Interest Income account. Thus, whatever

This case offers rich material for discussion. First, students are usually eager to discuss

the type of business, the nature of loans, and the method of financing sales. Second,

many students will suggest the development of a computer program in which each loan

is entered along with its duration, amount, and interest rate. The program would auto-

matically compute the accrued interest each month and keep track of the amount ac-

the effort and cost of doing so, but the cost is usually more than offset by the valuable

information the financial statements provide management, investors, and creditors, such

C3. Conceptual Understanding: Accounting Efficiency

C2. Conceptual Understanding: Purpose of Closing Entries

as National Bank of New Orleans in this case.

reversing entries must be recorded in the general journal and posted to the ledger ac-

counts. A disadvantage of preparing financial statements more often than once a year is

When financial statements are prepared, it is usually necessary to prepare adjusting

entries and use a work sheet or computer to prepare the financial statements. In addition,

Cases

C1. Conceptual Understanding: Interim Financial Statements

Closing entries prepare the accounts for the next accounting period by clearing the rev-

4-62

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

The notes to consolidated financial statements in the annual report present quarterly fi-

nancial data, so the company prepares interim financial statements at least every three

months. This means the company must go through the end-of-period procedures of pre-

paring adjusting entries, closing entries, and financial statements at least four times per

year. Although such interim procedures are usually not as extensive as the year-end pro-

cedures, they must still be done with care to produce financial statements that reflect

generally accepted accounting principles.

close the books and do other year-end procedures just as the company was making its

final frantic push for sales.

CVS ends its fiscal year on December 31 in 2011. There are several advantages to choos-

ing this date for the end of the fiscal year. First, inventory levels are low, which makes

counting the inventory less costly. Second, it coordinates well with the business’s natural

error by introducing another error. The consequences to the individual and the company

C4. Ethical Dilemma: Ethics and Time Pressure

Although an accountant facing a deadline may find it frustrating and potentially embar-

rassing to admit that the trial balance will not balance, it is unethical to compound one

that the final statements will be delivered later. Although the bank’s loan officers may not

be happy with this situation, at least they would know that the company is being honest.

C5. Annual Report Case: Fiscal Year, Closing Process, and Interim Reports

4-63

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

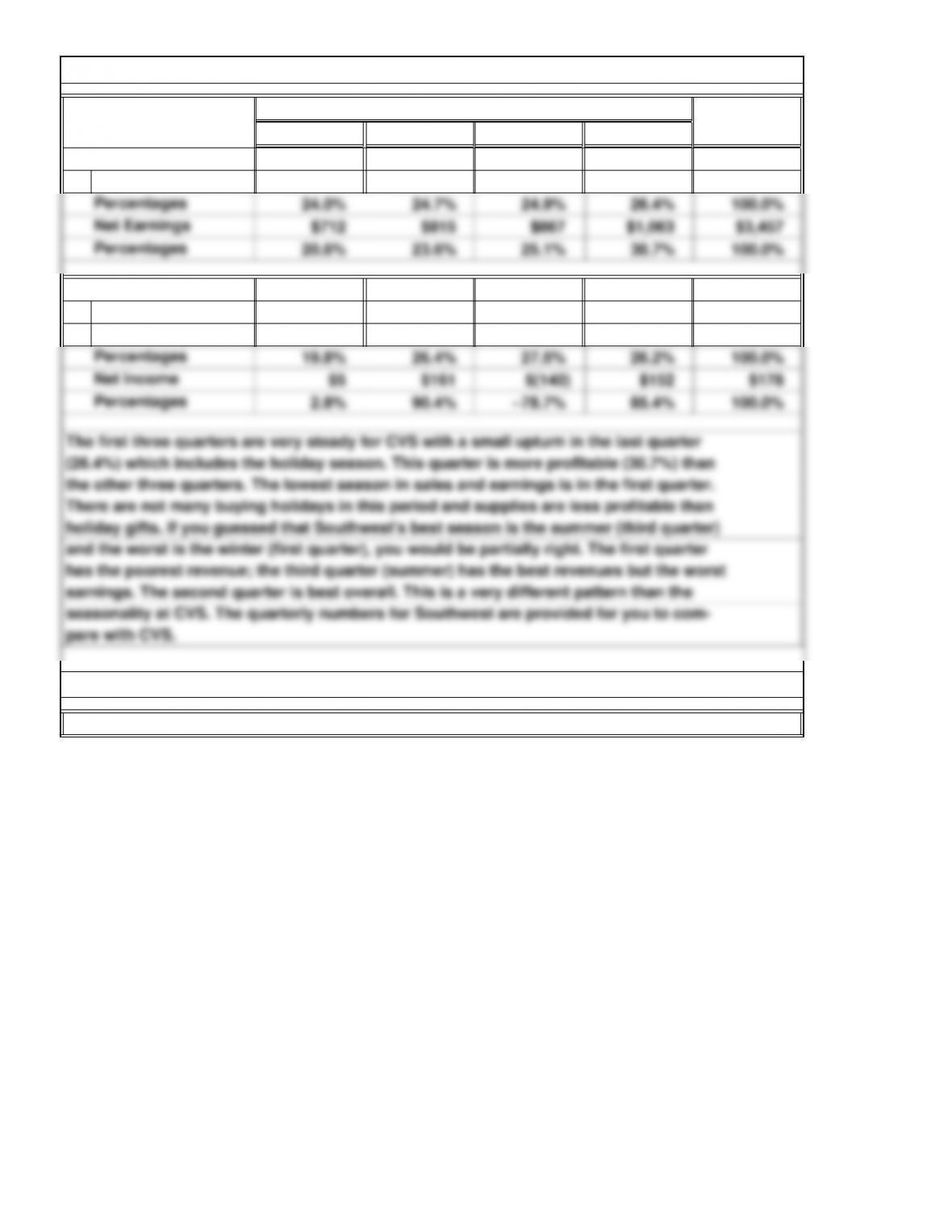

1st 2nd 3rd 4th

Net Revenues $25,695 $26,414 $26,674 $28,317 $107,100

Operating

Revenues $3,103 $4,136 $4,311 $4,108 $15,658

C7. Continuing Case: Annual Report Project

C6. Comparison Analysis: Interim Financial Reporting and Seasonality

Southwest—2011

Total

Quarter

Note to Instructor: Answers will vary depending on the company selected by the students.

(in millions)

CVS—2011

4-64

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.