Net Cash Flows from Operating Activities

E9A. Cash-Generating Efficiency Ratios and Free Cash Flow

$390,000

=Net Income

Cash Flow Yield

15-9

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Operating Investing Financing Noncash

Activity Activity Activity Transaction Increase Decrease No Effect

Problems

P1. Classification of Cash Flow Transactions

Cash Flow Classification Effect on Cash Flows

*Cash equivalent

Transaction

15-10

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

2013: $(76,944) ‒$39,946 ‒$66,224 =

2014: $368,454 ‒$45,848 ‒$32,290 =

3.

4.

term bank notes. The entire strategy of diversification was not well thought out. The

company’s regular sales probably declined due to its traditional customers resent-

ing the competition from one of their suppliers. The company had no experience

running a retail business.

$290,316

dividends and buying treasury stock when it is using so much cash.

In 2014, in addition to depreciation, the company decreased its accounts receivable

P2. Interpreting and Analyzing the Statement of Cash Flows

The company immediately began to lose money after the acquisition and had to

close outlets to reduce inventory and receivables to raise cash to pay off the short-

pense on the income statement.

had to obtain funds externally. In 2014, free cash flow was large but came mostly

from the downsizing of failed outlets and expansion of accounts payable, as ex-

plained in 1 above. The total cost of the acquisition consists of cash of $402,000

and a bond issue of $100,000. (See significant noncash investing and financing

$(183,114)

In 2013, the company did not have sufficient free cash flow for expansion and thus

term debt. In addition, it is questionable whether the company should be paying

The most significant financing activity by far was the increase in short-term bank

financing. The company also paid dividends, purchased treasury stock, and re-

duced long-term debt. It is not a good idea to finance expansion mostly using short-

and inventory in its retail division due to the closed outlets, which is evident from

the loss on closure of retail outlets. In addition, the company increased its payables

to suppliers. The latter may be a sign of financial difficulties.

Using the “law of large numbers,” the primary reasons for the difference between

net income and cash flows from operating activities in 2013 are increases in inven-

tory, accounts receivable, and depreciation. The first two are the result of building

up inventories and receivables in the retail division. Depreciation is a noncash ex-

Free Cash Flow

15-11

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

For the Year Ended December 31, 2014

P3. Statement of Cash Flows: Indirect Method

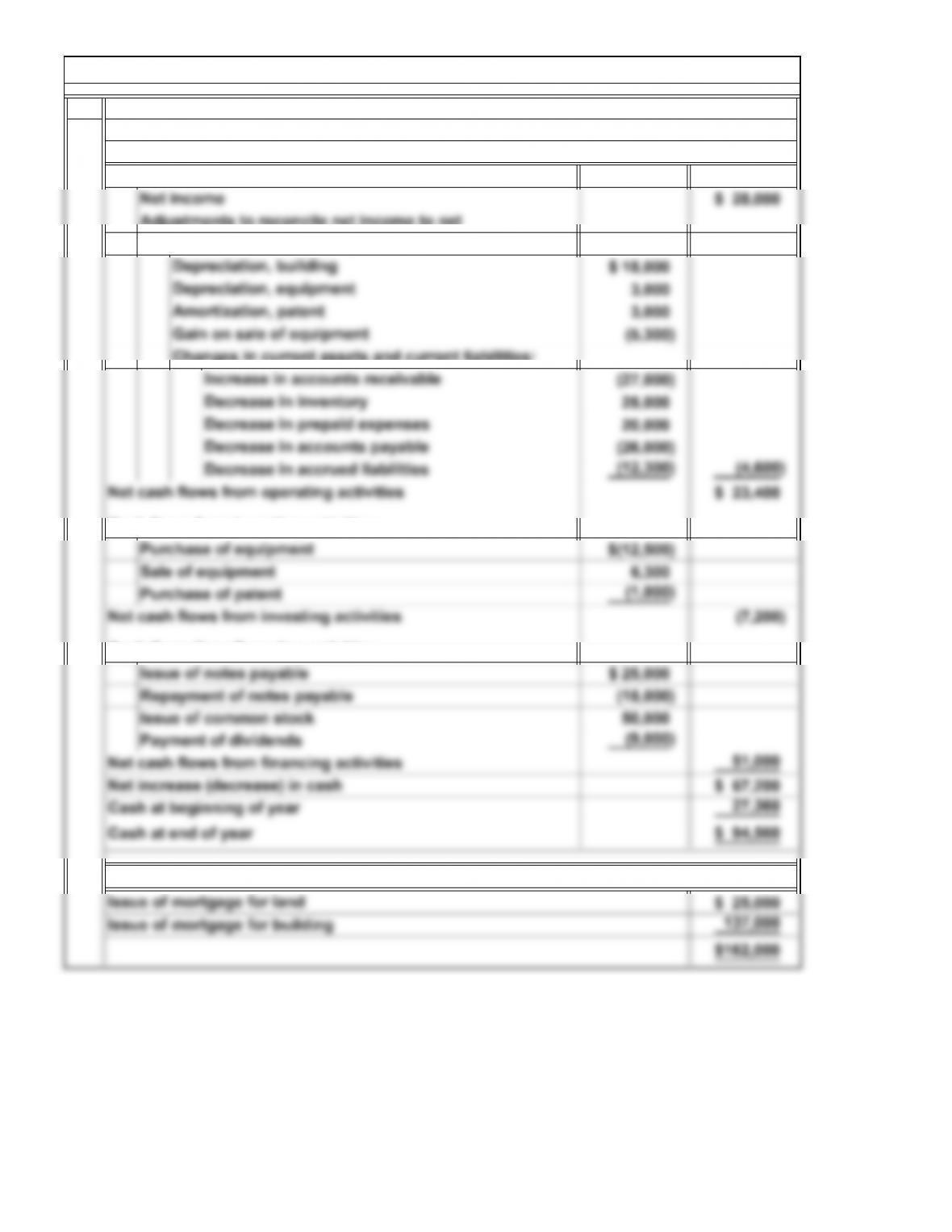

Statement of Cash Flows

Chaplin Arts, Inc.

Cash flows from operating activities:

15-12

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2.

3.

=

Net Income

P3. Statement of Cash Flows: Indirect Method (Concluded)

relatively small. Next year’s statement of cash flows will reveal what management

$51,000. Chaplin Arts has increased its cash balance through these financing activities

*Rounded

Free Cash Flow

Although net income of $28,000 generated only $23,400 of cash flows from operating

activities, and $7,200 was used by investing activities, Chaplin Arts managed to in-

by borrowing from the bank and issuing common stock. Its investing activities were

Net Cash Flows from Operating Activities – Dividends –

crease cash by $67,200. Net cash flows (or increases) from financing activities were

did with the cash.

$23,400

$28,000

Cash Flow Yield =

Net Cash Flows from Operating Activities

15-13

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

P4. Statement of Cash Flows: Indirect Method

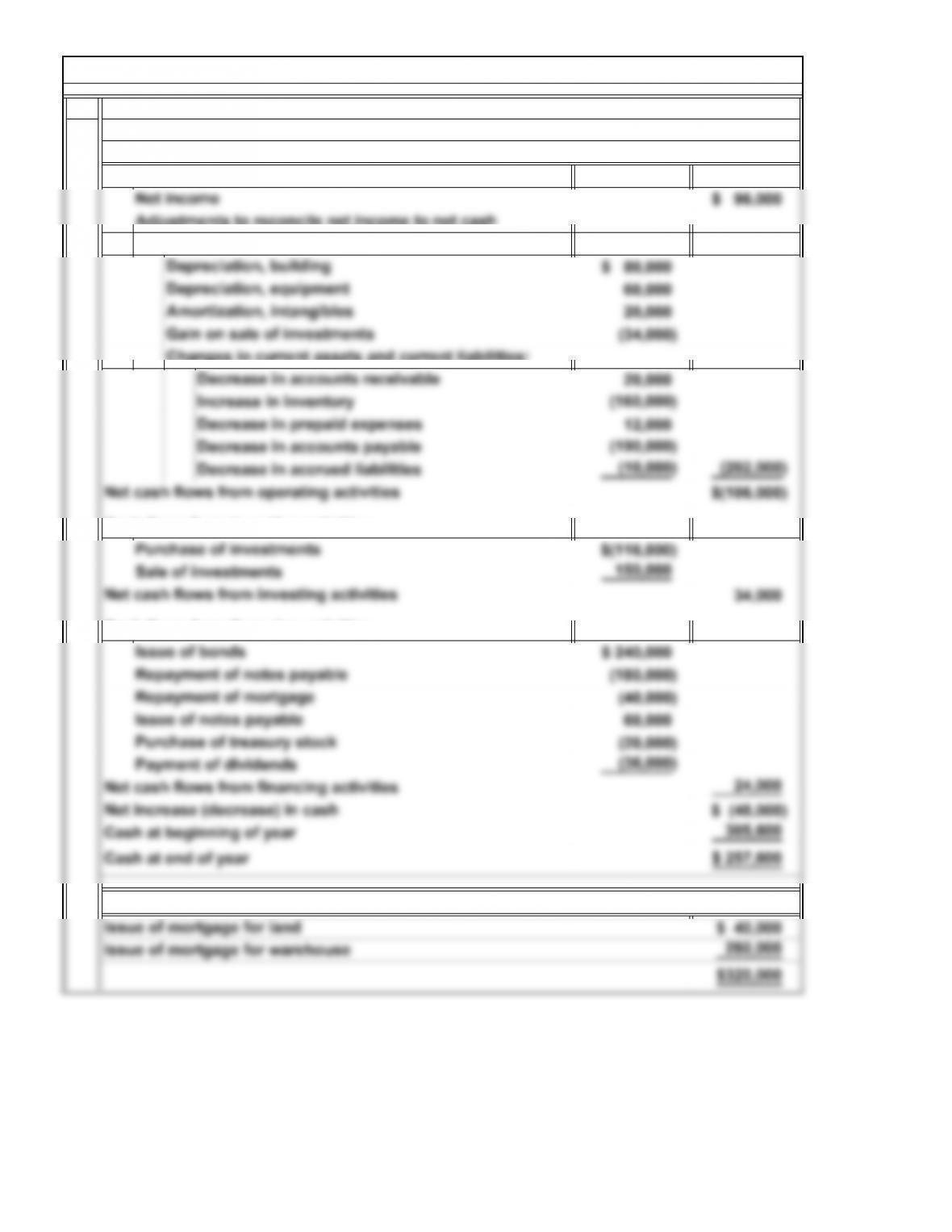

Ben Tools, Inc.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities:

15-14

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

P4. Statement of Cash Flows: Indirect Method (Concluded)

on increasing cash flows from operating activities and, secondarily, on a positive

free cash flow.

enough to more than offset the increase in cash through investing and financing

15-15

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

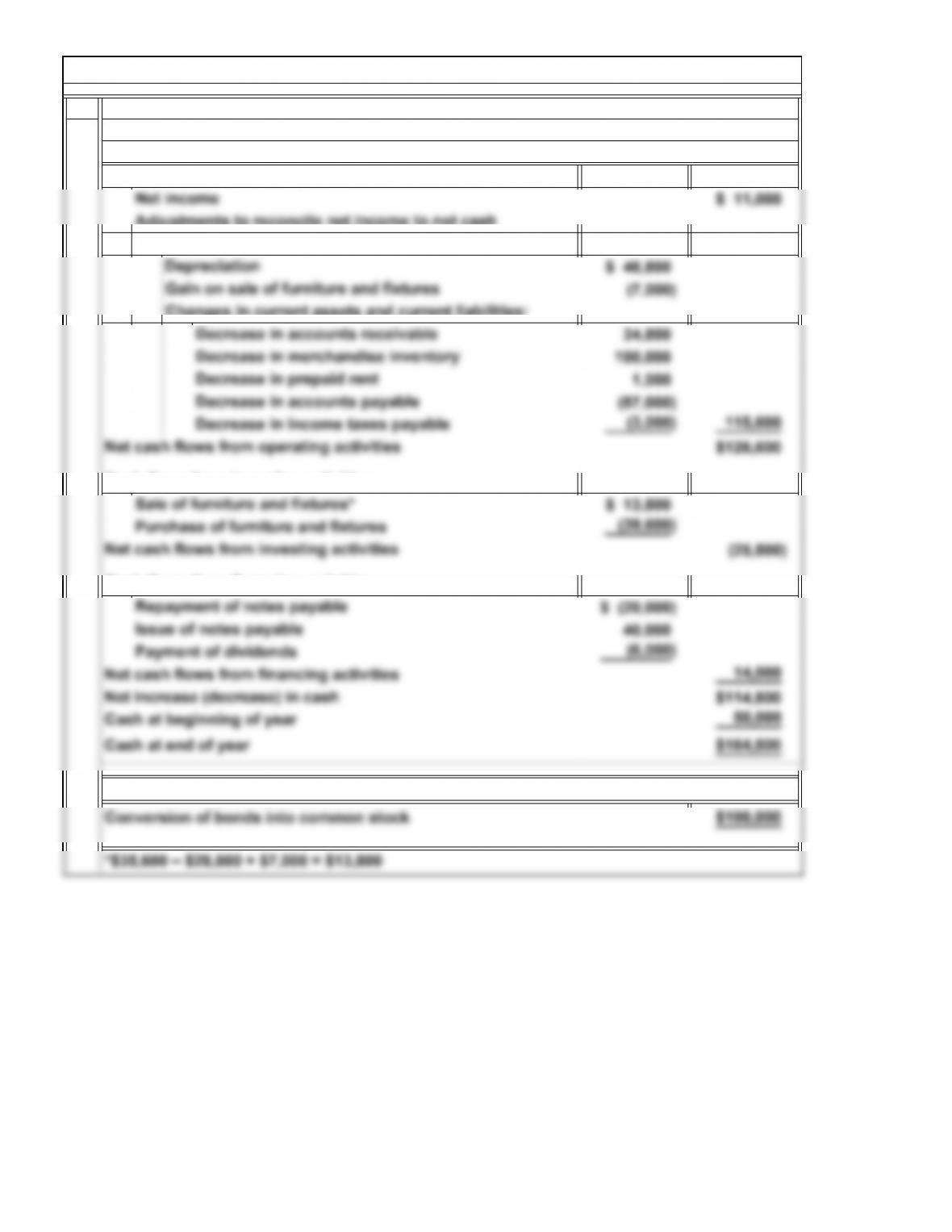

Yong Company

P5. Statement of Cash Flows: Indirect Method

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities:

15-16

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

3.

=

11.5

2014

P5. Statement of Cash Flows: Indirect Method (Concluded)

outflows from investing activities ($25,800) were relatively unimportant factors.

payable ($57,000). Net cash inflows from financing activities ($14,000) and net cash

expense ($46,800). These cash flows were partially offset by the decrease in accounts

times*

Net Cash Flows from Operating Activities – Dividends –

=

=

Purchases of Plant Assets + Sales of Plant Assets

Free Cash Flow

Net Cash Flows from Operating Activities

Net Income

$126,600

Cash Flow Yield =