Present value of 40 periodic payments at 6% (from Table 2*):

*From Appendix B

E3A. Valuing Bonds Using Present Value

Choice A

14-8

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

a.

b.

c.

d.

e.

Present value of 20 periodic payments at 5%

Present value of 40 periodic payments at 6%

*From Appendix B

Present value of 40 periodic payments at 3%

E4A. Valuing Bonds Using Present Value

Present value of 20 periodic payments at 4%

Present value of 20 periodic payments at 3%

14-9

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Face value × 0.057 =

Face value =

Face value =

Face value of 30-year, 8% zero coupon bonds, compounded annually:

Present value of a single payment at the end of 30 periods at 8% (from Table 1*):

$877,192,982

$2,380,952,381 or about $2.38 billion

Present value of a single payment at the end of 50 periods at 10% (from Table 1*):

Face value of 50-year, 10% zero coupon bonds, compounded annually:

Present value of a single payment at the end of 30 periods at 10% (from Table 1*):

E5A. Zero Coupon Bonds

Face value of 30-year, 10% zero coupon bonds, compounded annually:

or about $877 million

$50,000,000

*From Appendix B

14-10

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. a.

b.

c.

2. a.

b.

c.

3. a.

b.

c.

Note: Part 2 and Part 3 are identical.

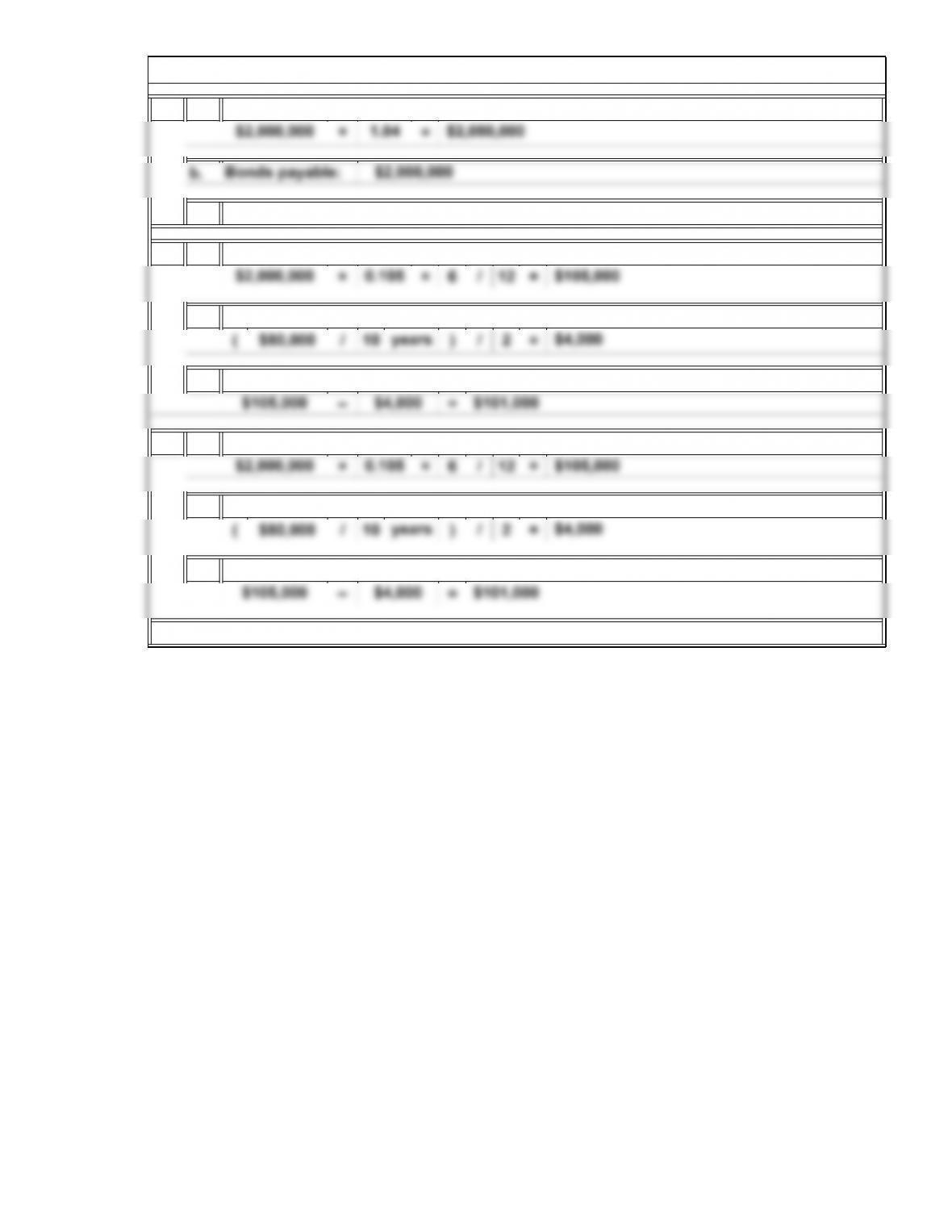

E6A. Straight-Line Method

Interest expense:

Amortization of bond premium:

Cash received:

Bonds payable:

$2,000,000

Cash paid in interest:

The difference of $80,000 is called unamortized bond premium.

Interest expense:

Amortization of bond premium:

Cash paid in interest:

14-11

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

/(5 ×2

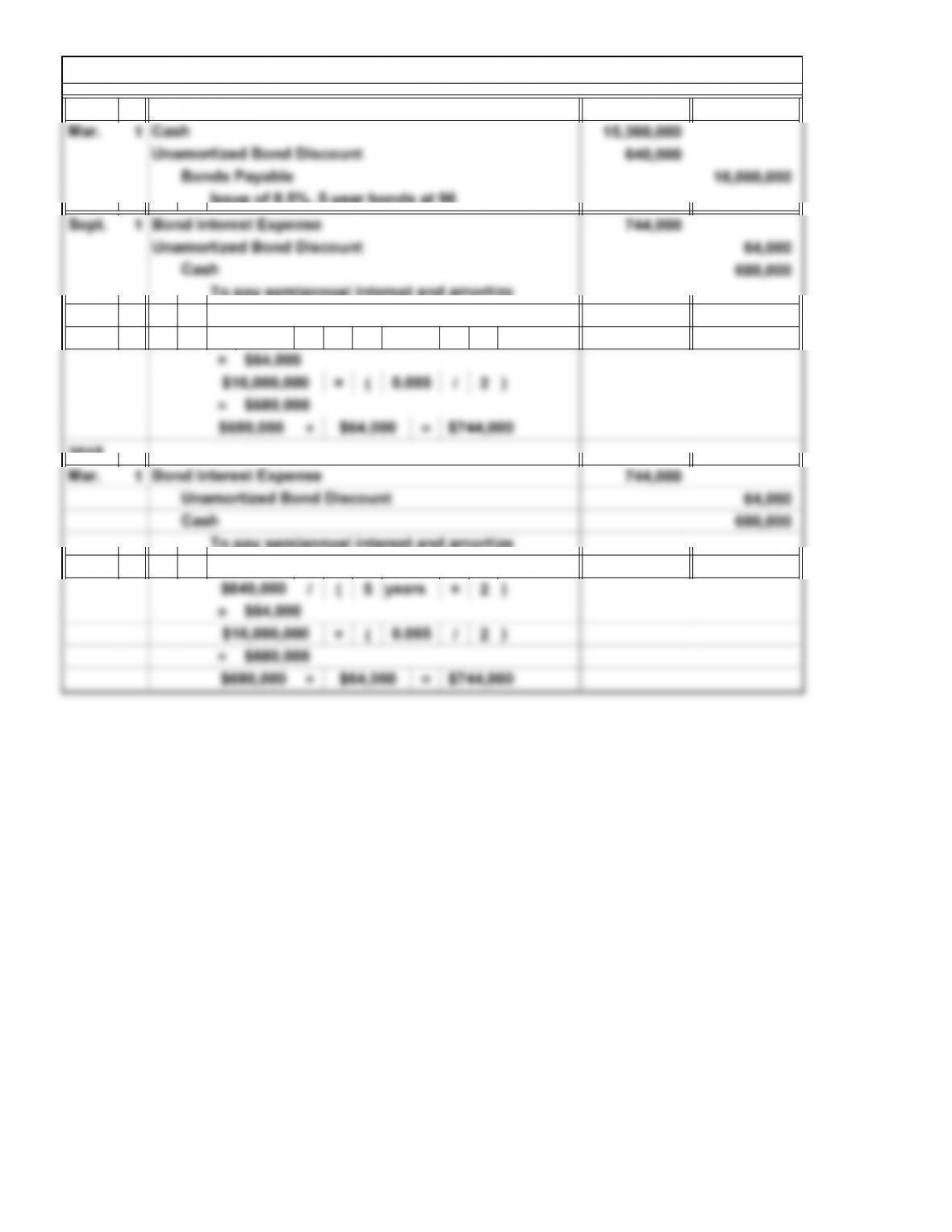

E7A. Straight-Line Method

2014

$640,000 years

To pay semiannual interest and amortize

the discount

)

14-12

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. a.

×=

b.

c.

2. a.

b.

( $250,000 × × 6 / 12 )

( $265,000 × × 6 / 12 )

c.

0.095

0.089

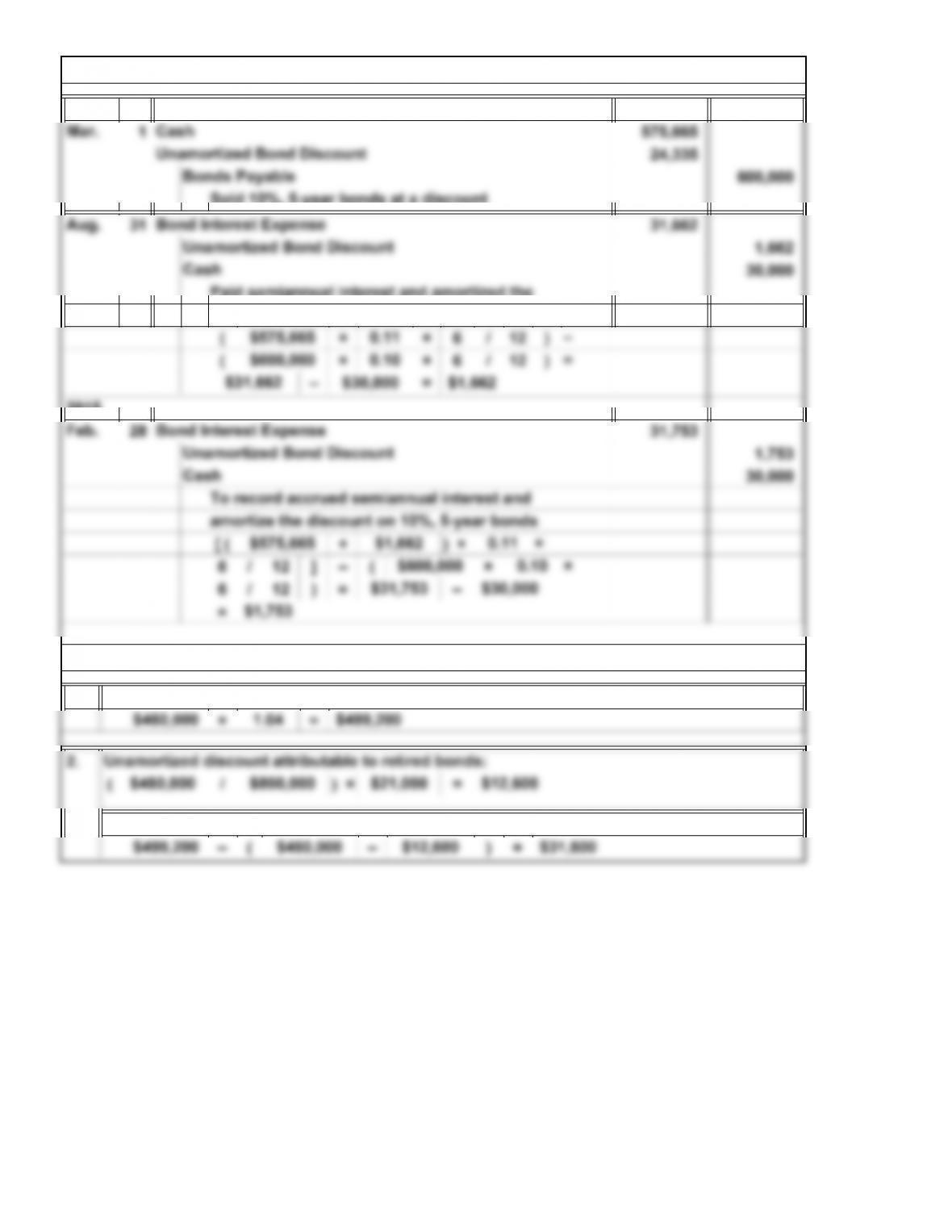

E8A. Effective Interest Method

$265,000

–

=

Cash received:

Bonds payable:

$250,000

$250,000 1.06

Amortization of bond premium:

Cash paid in interest:

Interest expense:

The difference of $15,000 is called unamortized bond premium.

14-13

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

=

1.

E9A. Effective Interest Method

2014

$1,753

E10A. Bond Retirement

Cash paid:

Loss:

14-14

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.