DQ1.

to decide how to pay the liabilities, and they will have to settle their capital accounts, just

as they would if cash were involved.

Discussion Questions

Partnerships are indeed separate entities from the partners from an accounting standpoint,

CHAPTER 12—Solutions

ACCOUNTING FOR PARTNERSHIPS

12-1

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

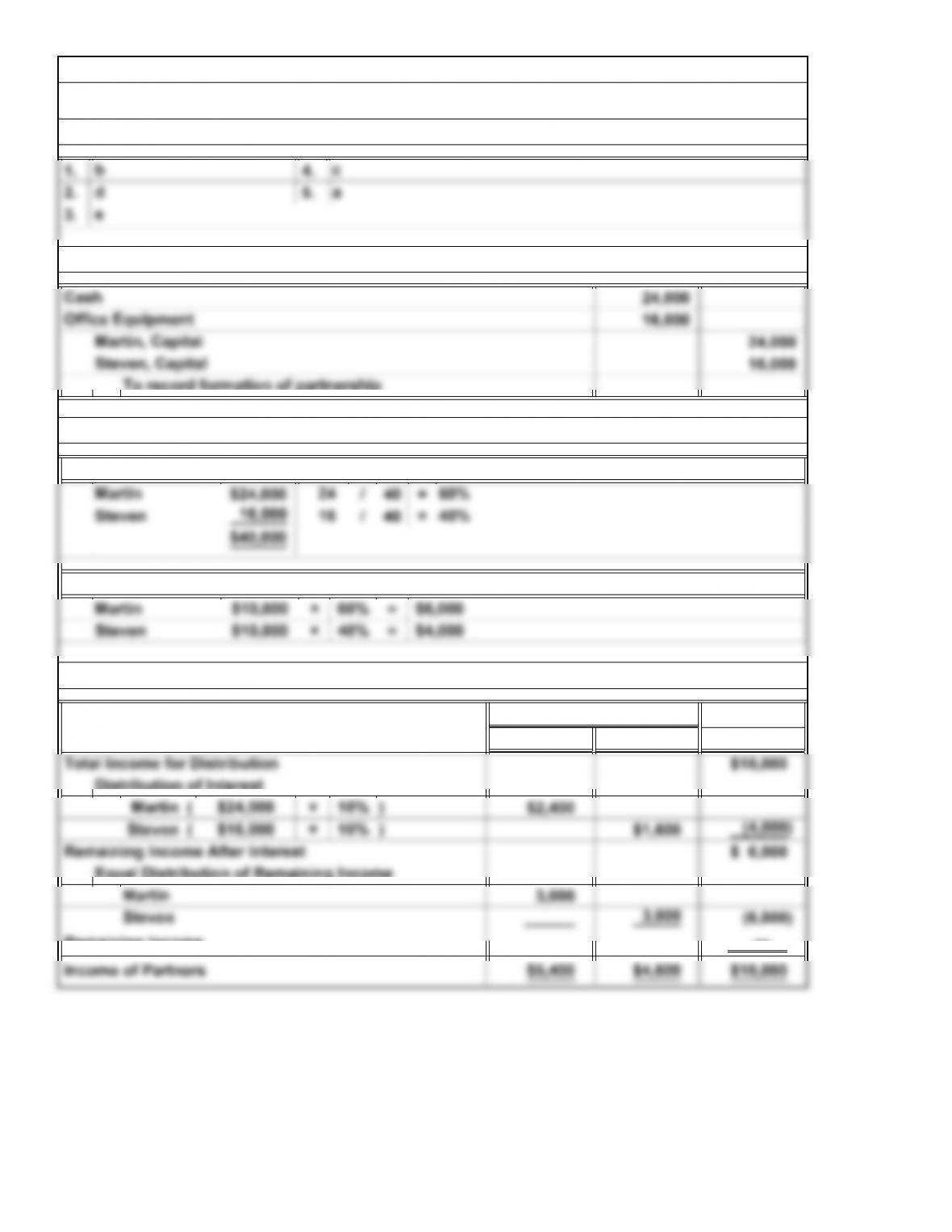

Martin Steven Distributed

—

SE4. Distribution of Partnership Income

Short Exercises

Income of Partner

SE1. Partnership Characteristics

SE2. Partnership Formation

Income

Remaining Income

12-2

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Martin Steven Distributed

—

10,000

10,000

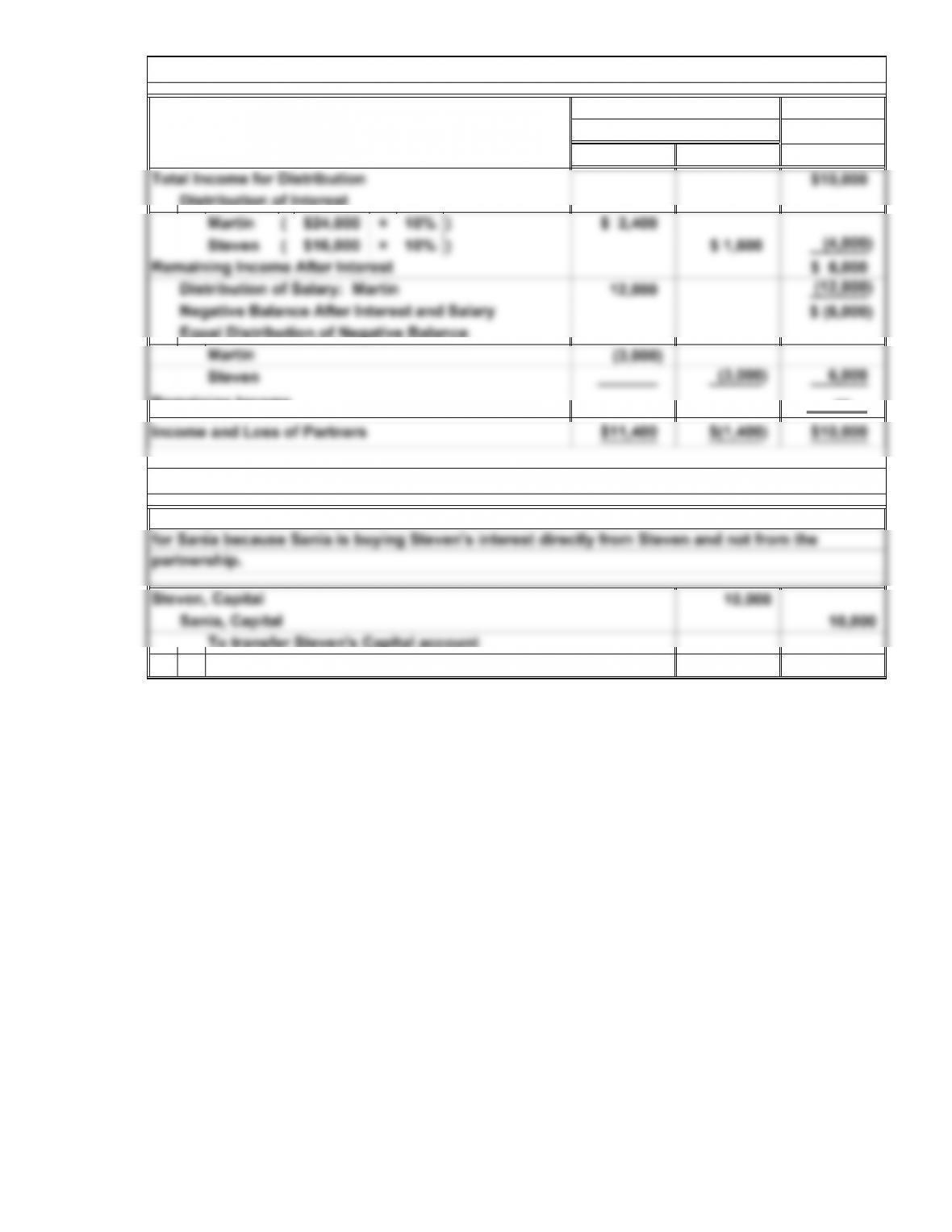

balance to Sania

Sania, Capital

To transfer Steven’s Capital account

Steven, Capital

of Partner Income

Income (Loss)

SE5. Distribution of Partnership Income

Remaining Income

12-3

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

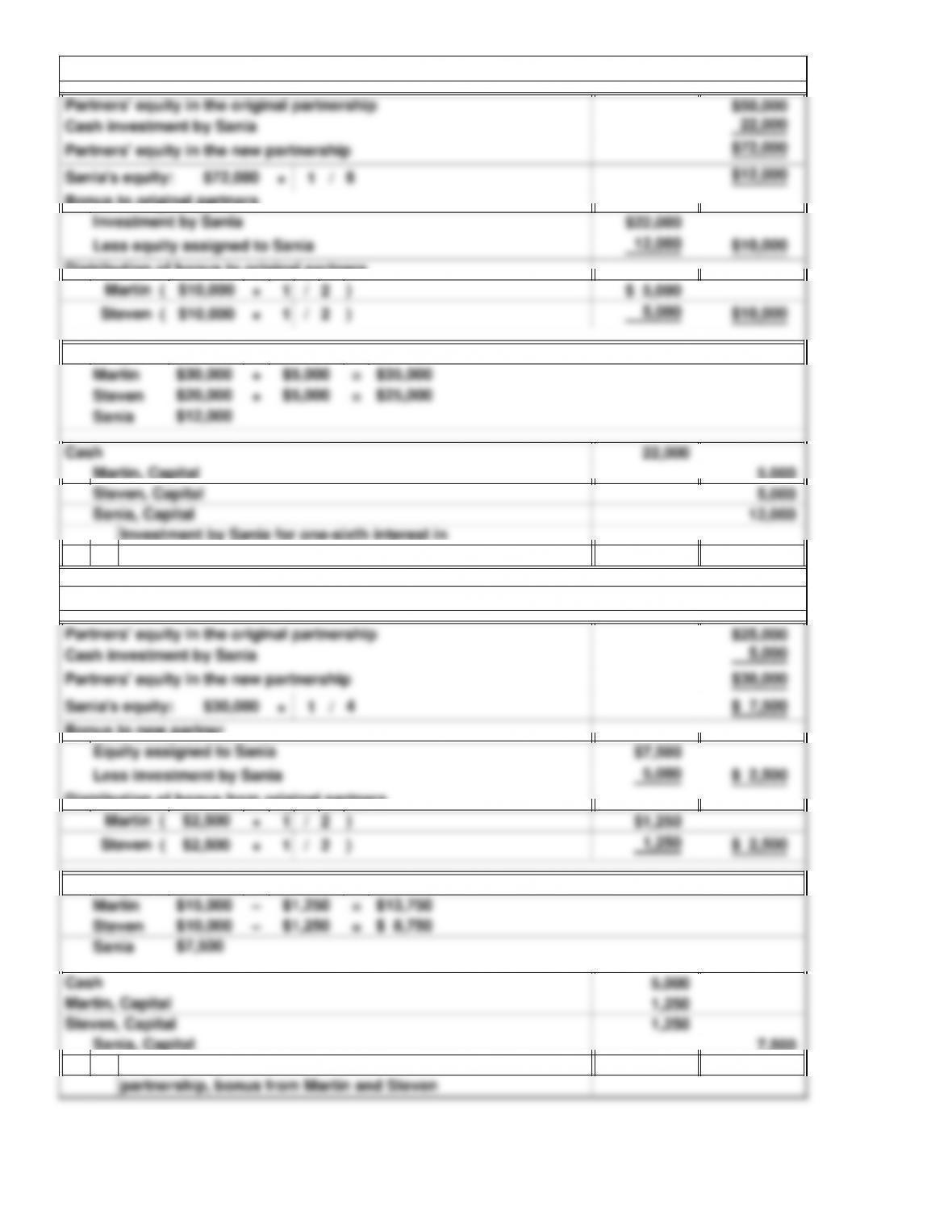

Sania

Steven – =

Sania

New Capital account balances:

$12,000

SE7. Admission of a New Partner

Investment by Sania for one-fourth interest in

Sania, Capital

partnership, bonus from Martin and Steven

$1,250 $ 8,750

$7,500

$10,000

New Capital account balances:

12-4

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Martin Steven

3.

SE11. Types of Partnerships

c

Distribution of Cash to Partners

SE9. Withdrawal of a Partner

12-5

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

3.

4.

5.

1.

2.

3.

4.

80,000

104,000

2,000

40,000

8,000

64,000

154,000

60,000

40,000

1,000

20,000

6,000

18,000

97,000

d

a

e

Exercises: Set A

E1A. Partnership Characteristics

a

b

a

b

b

c

E2A. Partnership Advantages and Disadvantages

E3A. Partnership Formation

Accounts Payable

Original investment by Hanna Hark

Accounts Payable

Allowance for Uncollectible Accounts

Jamie Rice, Capital

Supplies

Equipment

Original investment by Jamie Rice

Cash

Accounts Receivable

Supplies

Equipment

Allowance for Uncollectible Accounts

Hanna Hark, Capital

Cash

Accounts Receivable

12-6

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

—

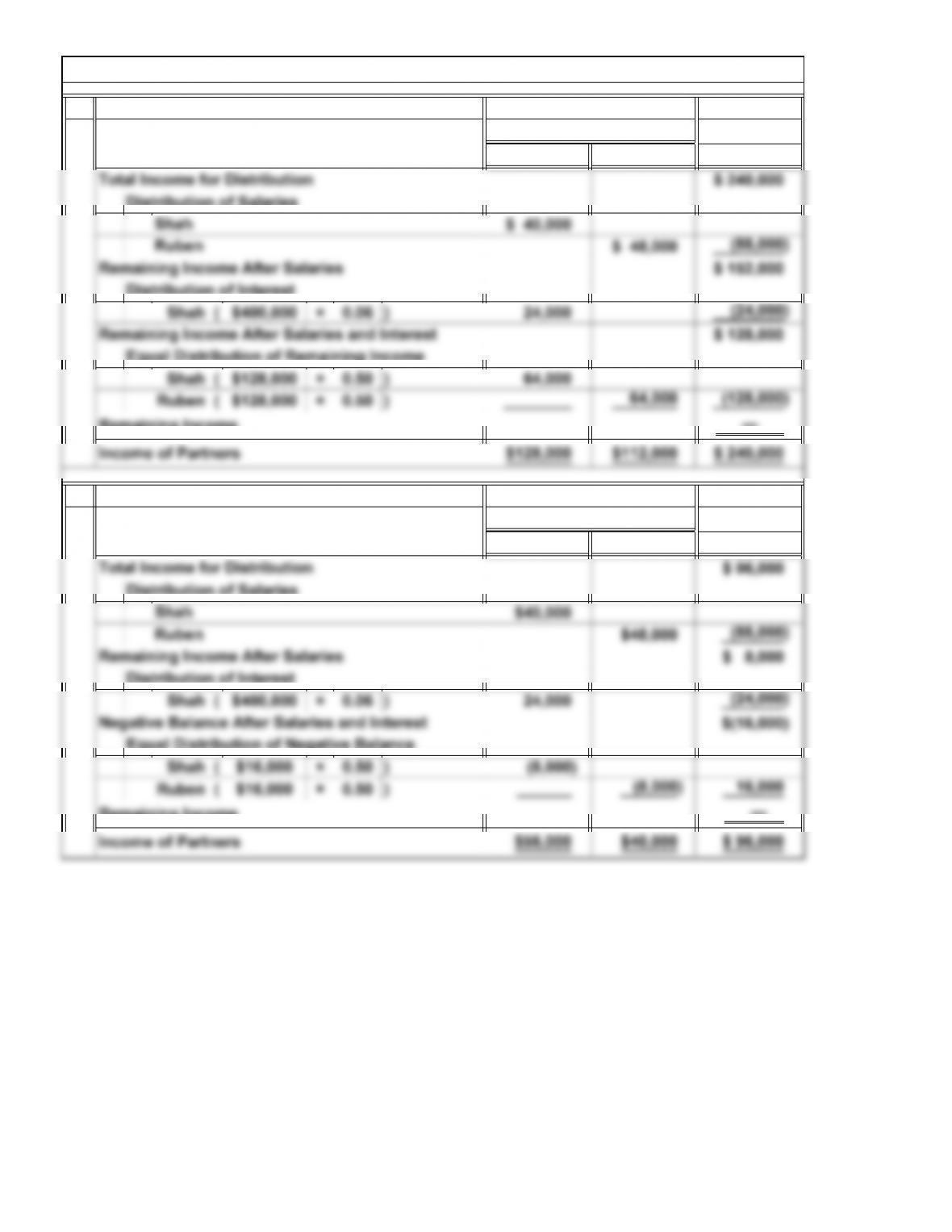

$100,000 $140,000 $ 240,000

to Ruben.

Computation: The partners agreed to share the income three-fifths to Shah and two-fifths

E4A. Distribution of Income

Computation: The partners share equally.

Note: Because the partnership agreement does not address the distribution of income and

losses, the law requires that income and losses be shared equally.

$240,000

Total net income

Income of Partners

Remaining Income

12-7

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

Shah Ruben Distributed

—

2.

Shah Ruben Distributed

—

Remaining Income

Income (Loss)

E5A. Distribution of Income or Losses: Salaries and Interest

Income

Computation:

Remaining Income

Income

of Partner

Computation: Income (Loss)

of Partner

12-8

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

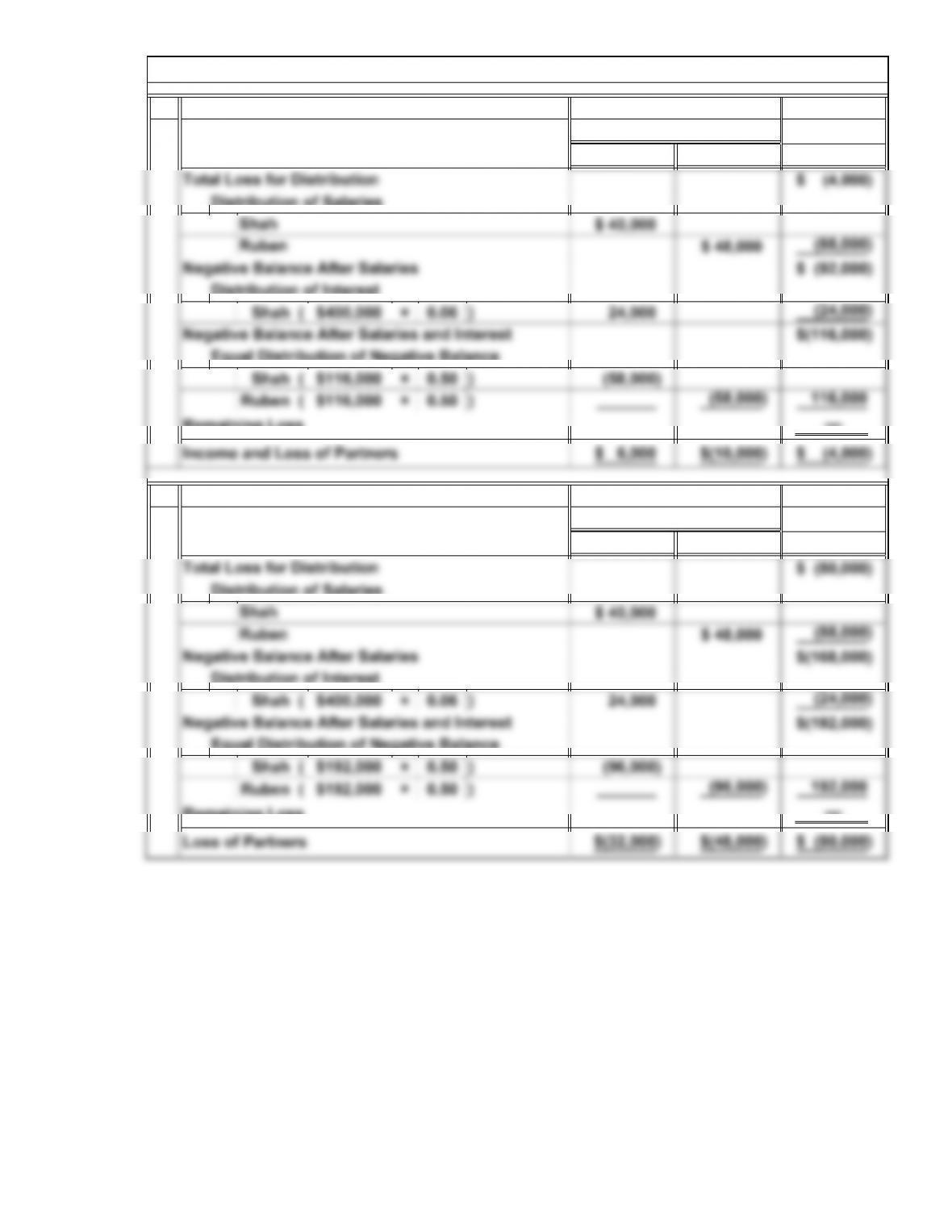

3.

Shah Ruben Distributed

—

4.

Shah Ruben Distributed

—

of Partner

Remaining Loss

E5A. Distribution of Income or Losses: Salaries and Interest (Concluded)

Computation:

Loss

Income (Loss)

Remaining Loss

Computation: Income (Loss)

of Partner

Loss

12-9

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Average

Date × = Total Capital

=

199,360

Ankit

Distribution of income computed:

Average capital balance ratios computed:

Months

UnchangedPartner

Capital

Balance

Average capital balances computed:

*Rounded

E6A. Distribution of Income: Average Capital Balance

$320,000 0.623

=×

12-10

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.