Ending merchandise inventory for LIFO will be the same dollar amount under a

periodic inventory system as under a perpetual inventory system.

Mineral deposits are subject to a process called depletion.

Trading securities are valued on the balance sheet at market value.

It is possible for horizontal analysis to indicate an increase in revenues from one year to

another and a decrease in net income.

The effective interest method produces a constant dollar amount of bond interest

expense to be reported each interest period.

A debit to Accumulated Depreciation will increase the carrying value of an asset.

The heading for a balance sheet might include the line “For the Month Ended

December 31, 20–.”

The adjusting entries involving Rent Receivable and Salaries Payable could be

reversed.

Dividends in arrears on cumulative preferred stock are not paid until after dividends are

paid on common stock.

The double-entry system is possible because all business transactions have at least two

equal and opposite aspects.

Net income can be used to assess a company’s progress in meeting the goal of

profitability.

A trial balance is normally prepared at the end of each business day.

Purchase requests and purchase orders are economic events, and as such they affect a

company’s financial position, and are recognized in the accounting records.

Following a lenient credit-granting policy will probably result in fewer defaults by

customers.

If the partnership agreement does not describe the method of income and loss

distribution, the partners must share income and losses equally.

The quality of earnings refers to the substance of earnings and their sustainability into

future periods.

The book value of one share of callable preferred stock is equal to the call value of the

preferred share minus any dividends in arrears.

If a partnership agreement does not specify how income and losses are to be distributed,

the partners share them equally.

Asset turnover measures how efficiently assets are used to produce revenues.

The interest coverage ratio and the debt to equity ratio are measures of profitability.

Driveways and parking lots are properly included in the Land account because they are

not subject to depreciation.

The present value of a bond is always less than the face value of the bond.

A discounted note represents a contingent liability to the original holder.

Treasury stock usually is recorded at cost when purchased.

An advantage of the partnership form of business is that the life of the partnership is

limited.

When salary and interest allocations exceed net income, a net loss has occurred.

In computing book value per share of common stock, common stock distributable is

included in the divisor.

A retail operation would not have to take a physical inventory if it uses a perpetual

inventory system.

The primary purpose of an expense is to generate revenue.

When earnings from the investment exceed the interest payments on an investment,

negative financial leverage has occurred.

When the dividends yield is relatively low, investors must expect some of their return to

come from increases in the price of the shares.

If liquidation of a partnership results in a negative balance in a partner’s account, the

partner must pay into the partnership the amount of the negative balance.

The market interest rate is the rate that an issuer of bonds actually will have to bear and

that an investor (purchaser) actually will earn over the bond’s life.

The par value of stock is an arbitrary amount assigned to each share of stock.

The choice of accounting methods does not affect cash flows except for possible

differences in income taxes.

Creditors’ equities is another term for liabilities.

If a company uses LIFO for tax purposes, it need not use LIFO for financial reporting

purposes.

When bonds are purchased between interest dates, the buyer must pay (in addition to

the bonds’ cost) the amount of interest that has accrued since the last interest payment

date.

The lower the current ratio, the more likely the company will be able to meet its

liabilities.

a. Indicate on the blanks below the effect (I = increase, D = decrease, NE = no effect) of

the entry to record the declaration of a common stock dividend on each of the items

listed.

b. Indicate on the blanks below the effect (I = increase, D = decrease, NE = no effect) of

the entry to record the distribution of a (previously declared and recorded) common

stock dividend on each of the items listed.

For each of the following oversights, state whether total assets will be understated,

overstated, or not affected.

______ a.Failure to record revenue earned but not yet received

______ b.Failure to record expired rent

______ c.Failure to record accrued interest in the bank

______ d.Failure to record depreciation

______ e.Failure to record accrued wages

______ f.Failure to convert unearned revenue to earned revenue

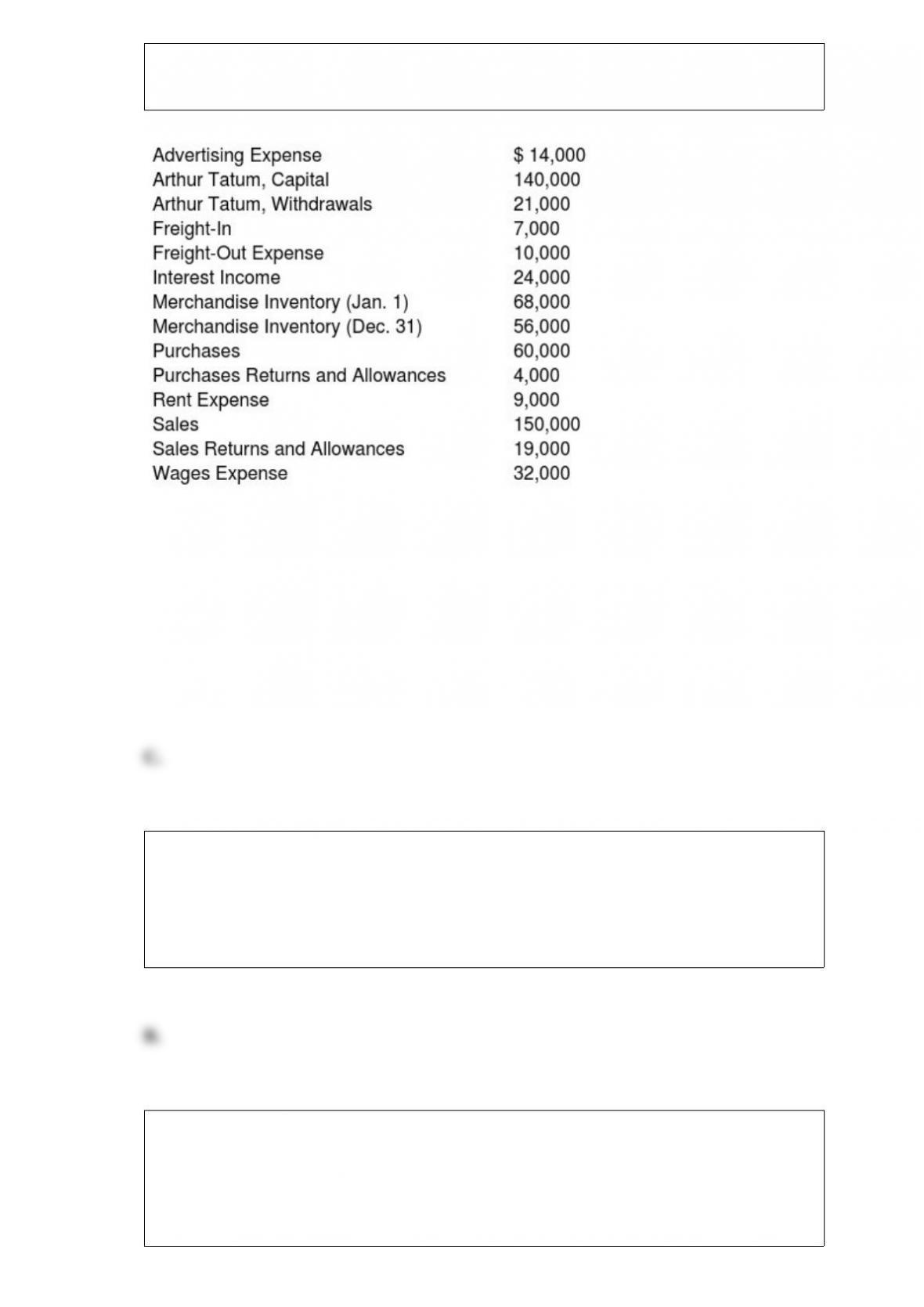

Use this information to answer the following question.

The selected accounts and balances for Keystone Market appear as follows:

Cost of goods available for sale would appear on the income statement as

A. $124,000.

B. $71,000.

C. $131,000.

D. $61,000.

Free cash flow is

A. a financial ratio.

B. an important measure of a company’s ability to finance long-term assets.

C. what remains after deducting dividends declared from net income.

D. an important measure of a company’s ability to invest in short-term assets.

Goodwill would appear in which balance sheet section?

A. Investments

B. Property, plant, and equipment

C. Current assets

D. Intangible assets

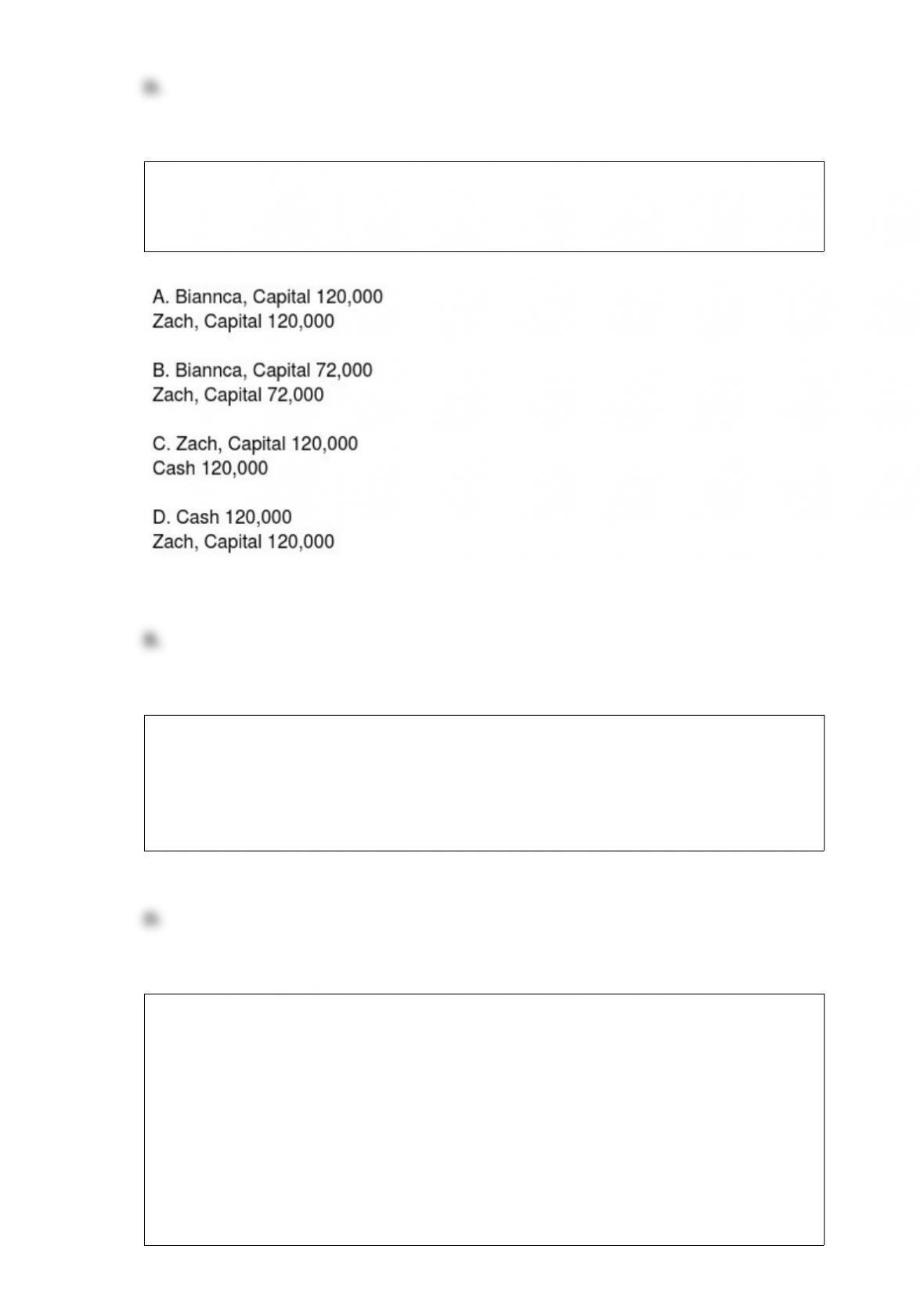

Zach has bought Biannca’s interest in the A&B Partnership for a $120,000 direct

payment to Biannca. Zach and Biannca’s capital balances before the sale were $48,000

and $72,000, respectively. The entry to record the purchase of interest in partnership is:

Which of the following bank reconciliation items would not result in a journal entry?

A. Service charge

B. NSF check of a customer

C. Collection of a note by the bank

D. Deposits in transit

On June 3, Addison Company purchased merchandise worth $1,600 on credit, terms

2/10, n/30. The account was paid on June 10. What is the required journal entry to

record the payment under the periodic inventory system?

A. Accounts Payable 1,568

Purchases Discounts 32

Cash 1,600

B. Accounts Payable 1,600

Purchases Discounts 32

Cash 1,568

C. Cash 1,568

Purchases Discounts 32

Accounts Payable 1,600

D. Cash 1,600

Applying the lower-of-cost-or-market rule follows which of the following accounting

conventions?

A. Full disclosure

B. Matching

C. Materiality

D. Conservatism

Assuming that the current ratio was 1.6 times and the quick ratio was 1.4 times before

this transaction, the entry to record the payment of a previously declared and recorded

cash dividend will

A. increase the current ratio and the quick ratio.

B. decrease the current ratio and the quick ratio.

C. increase the current ratio but have no effect on the quick ratio.

D. have no effect on the current ratio or the quick ratio.

Which of the following is not classified properly as property, plant, and equipment?

A. Land improvements, such as parking lots and fences

B. Natural resources

C. Land used in ordinary business operations

D. A truck held for resale by an automobile dealership

Total partners’ equity will not change when a withdrawing partner

A. withdraws assets equal to his or her capital balance

B. withdraws assets amounting to less than his or her capital balance

C. sells his or her interest to a new or remaining partner

D. withdraws assets amounting to greater than his or her capital balance

Legal capital is a descriptive phrase for

A. stockholders’ equity.

B. residual equity.

C. market value.

D. par value.

A revenue expenditure results in a

A. debit to an expense account.

B. credit to an expense account.

C. debit to an asset account.

D. credit to an asset account.

An NSF check should appear in which section of the bank reconciliation?

A. Deductions from the balance per books

B. Deductions from the balance per bank

C. Additions to the balance per books

D. Additions to the balance per bank

An amount would not appear opposite the Withdrawals account in which of the

following work sheet columns?

A. Trial Balance

B. Income Statement

C. Balance Sheet

D. Adjusted Trial Balance

Gomez Company purchases a piece of equipment on Jan. 2, 2014, for $30,000. The

equipment has an estimated life of eight years or 50,000 units of production and an

estimated residual value of $3,000. Lester uses a calendar fiscal year. The entry to

record the amount of depreciation for 2014, using the straight-line method, is

A. debit to Depreciation Expense, 3,750; credit to Cash, 3,750

B. debit to Depreciation Expense, 3,375; credit to Accumulated Depreciation, 3,375

C. debit to Depreciation Expense, 2,500; credit to Accumulated Depreciation, 2,500

D. debit to Accumulated Depreciation, 2,250; credit to Cash, 2,250

In a trend analysis, an index number of 139 for 20×5 sales indicates that

A. sales for 20×5 were 139 percent higher than sales for the same company in the base

year.

B. sales for 20×5 for this company were 139 percent of the sales figure of another

company being used in the comparison.

C. sales for 20×5 were 139 percent of the sales for the same company in the base year.

D. actual sales for 20×5 exceeded budgeted sales for 20×5 by 39 percent.

Using the following information and the trial balance accounts and balances in the work

sheet provided, complete the work sheet.

a. Expired insurance totals $260.

b. Of the unearned revenue, all has been earned by the balance sheet date.

c. Estimated depreciation of equipment is $120.

d. Accrued wages equal $400.

e. Unused supplies on hand are $90.

A general rule in choosing among alternative investments is the greater the risk taken,

the

A. greater the return required.

B. lower the potential expected.

C. greater the price of the investment.

D. lower the profits expected.

If Year 1 equals $2,800, Year 2 equals $3,108, and Year 3 equals $3,668, the index

number to be assigned for Year 3 in trend analysis, assuming that Year 1 is the base

year, is

A. 100.

B. 141.

C. 131.

D. 136.

If creditors’ payment terms are 60 days, financing period is 20 days, and it takes 30

days to collect the amount from customers. What time does it take to sell the inventory?

A. 60 days.

B. 20 days.

C. 30 days.

D. 50 days.

An American company makes a credit sale of goods to a company in London for 20,000

British pounds. On the date of sale, the exchange rate was $1.60 per pound. However,

on the date payment was received, the exchange rate had risen to $1.70 per pound. As a

result, the American company would record

A. an exchange gain of $2,000.

B. an exchange loss of $200.

C. an exchange loss of $2,000.

D. no exchange gain or loss.

Cost of goods sold equals $250,000, and average inventory equals $100,000. Days’

inventory on hand equals

A. 91.3 days.

B. 146.0 days.

C. 821.9 days.

D. 912.5 days.

Plum Corporation issues $400,000 of 7 percent, five-year bonds on January 1, 20×5,

and sells them on the same date for their face value. The bond indenture states that

interest is to be paid on January 1 and July 1 of each year. The entry to record the

issuance includes

A. a credit to Cash.

B. a credit to Bonds Payable.

C. a credit to Interest Expense.

D. All of these choices.

The return on assets and the asset turnover ratios are used to analyze

A. leverage.

B. long-term solvency.

C. profitability.

D. liquidity.

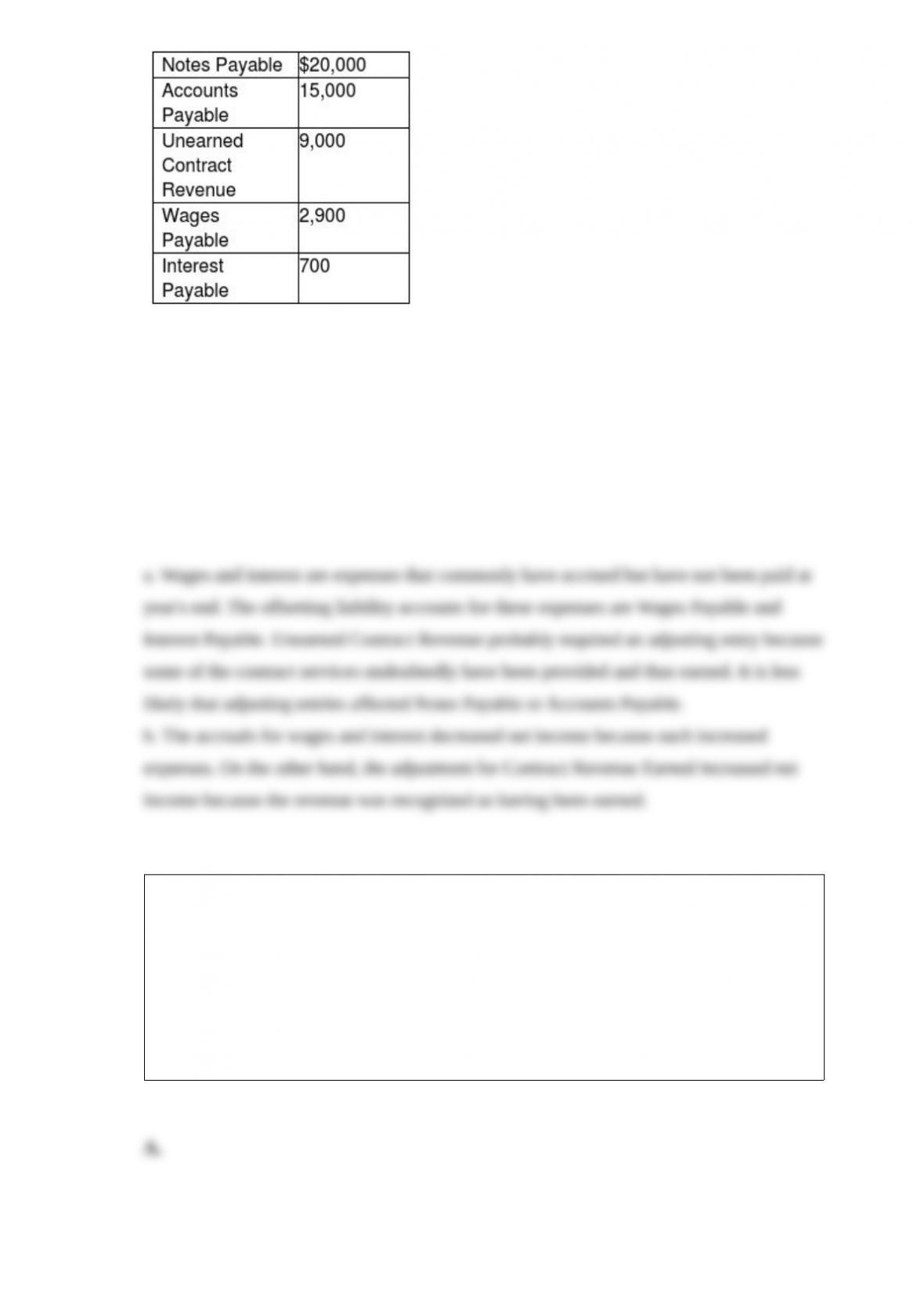

Quality Heating Company has the following liabilities at year end:

a. Which of these accounts probably was/were created at the end of the fiscal year as a

result of an accrual? Which probably was/were adjusted at year end? Explain your answer.

b. Which adjustments probably reduced net income? Which probably increased net

income? Explain your answers.

Assume the direct method is used to compute net cash flows from operating activities.

For this item extracted from the financial statements—Decrease in Accrued Liabilities

—indicate the effect on cash payments for operating expenses by choosing one of the

following:

A. Add to operating expenses to arrive at cash payments for operating expenses.

B. Subtract from operating expenses to arrive at cash payments for operating expenses.

C. Not used to adjust operating expenses to arrive ay cash payments for operating

expenses.

A merchandiser will earn an operating income of exactly $0 when

A. gross margin equals operating expenses.

B. net sales equals cost of goods sold.

C. cost of goods sold equals gross margin.

D. operating expenses equal net sales

Which of the following categories of investments can be both debt and equity

securities?

A. Available-for-sale securities

B. Trading securities

C. Held-to-maturity securities

D. Both available-for-sale and trading securities

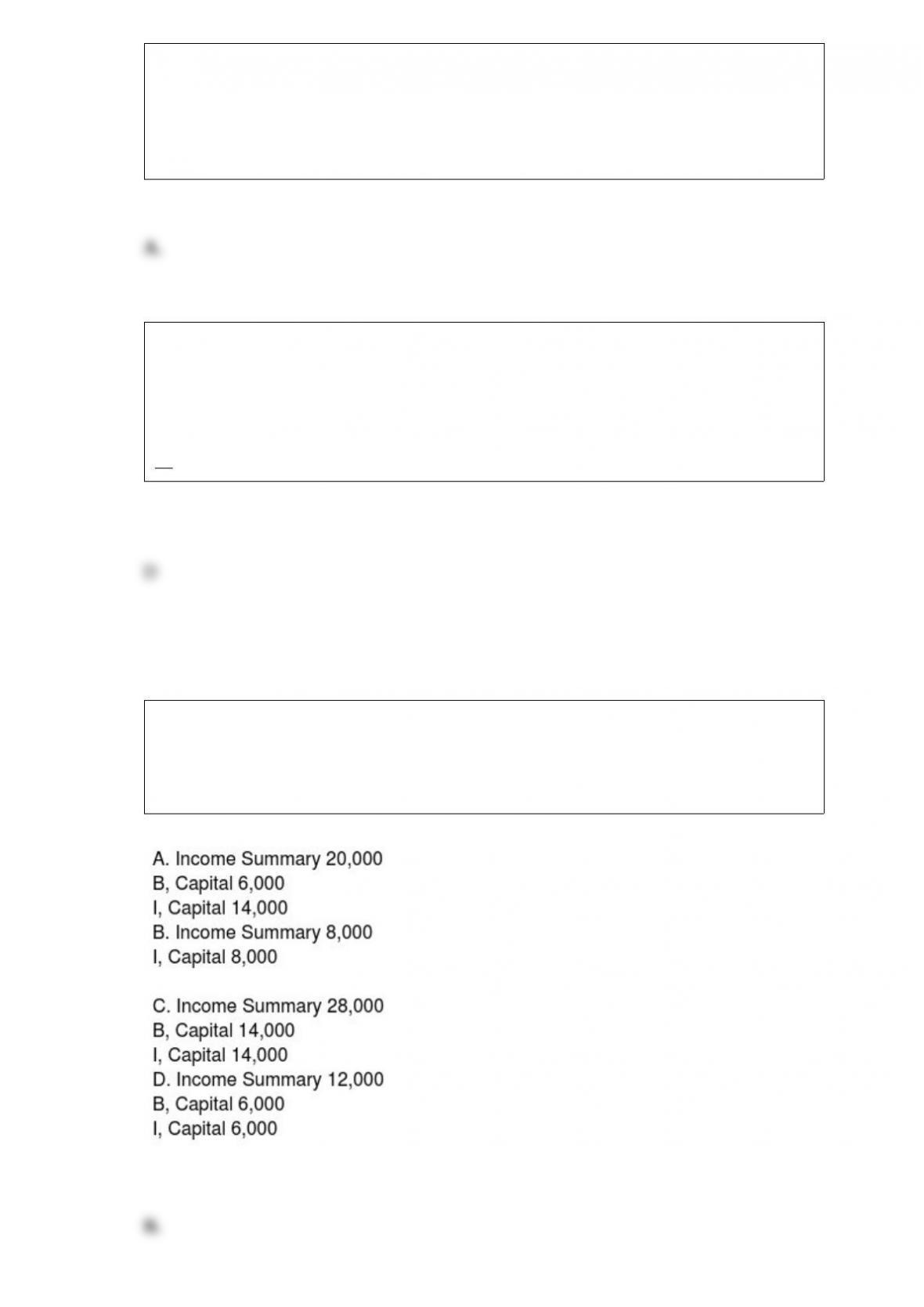

Partners K and R receive an interest allowance of $20,000 and $30,000, respectively,

and divide the remaining profits and losses in a 3:1 ratio. If the company sustained a net

loss of $22,000 during the year, the entry to close the income or loss into their capital

accounts is:

Which costing method will produce different results under perpetual and periodic

systems?

A. Specific identification

B. Average-cost

C. FIFO

D. Both FIFO and specific identification

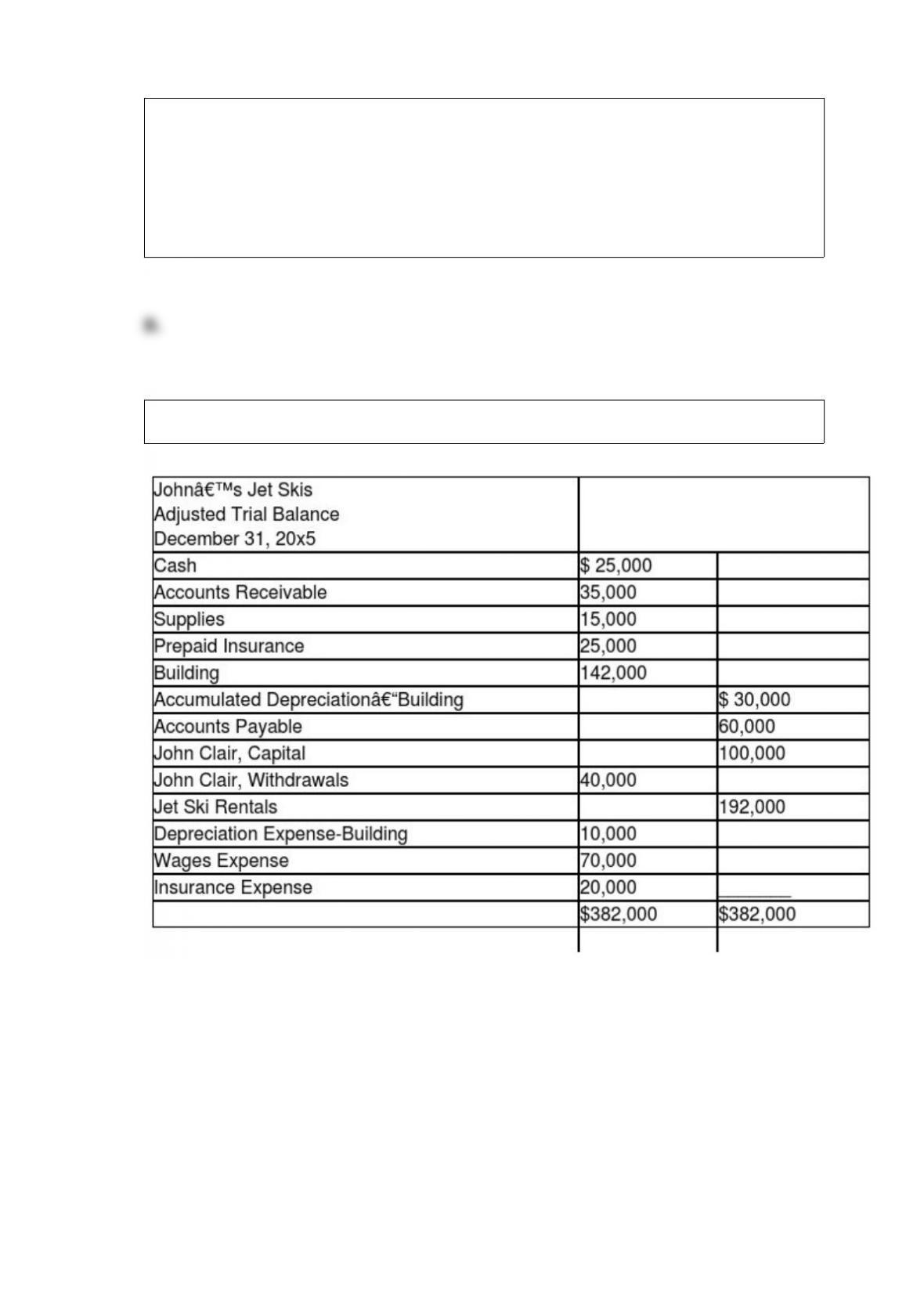

Use the following adjusted trial balance to answer the question below.

The entry to close Income Summary is

A. Income Summary 92,000

John Clair, Capital 92,000

B. John Clair, Withdrawal 142,000

Income Summary 142,000

C. John Clair, Capital 182,000

Income Summary 182,000

D. John Clair, Capital 92,000