Archives: Solution Manual

978-0134475585 Chapter 18 Solution 3

2. The cost per equivalent unit of beginning inventory and of work done in the current period differ substantially: Beginning Inventory Work Done in Current Period Direct Materials Conversion Costs Cost per equivalent unit (weighted-average) $204*$82* Cost per equivalent unit […]

978-0134475585 Chapter 18 Solution 2

SOLUTION (2025 min.) Physical units, inspection at various stages of completion Inspection Inspection Inspection at 20% at 45% at 100% Work in process, beginning (25%)* Started during March 2,500 30 ,000 2,500 30 ,000 2,500 30 ,000 *Degree of completion […]

978-0134475585 Chapter 18 Solution 1

CHAPTER 18 SPOILAGE, REWORK, AND SCRAP 18-1 Why is there an unmistakable trend in manufacturing to improve quality? 18-2 Distinguish among spoilage, rework, and scrap. Spoilage—units of production that do not meet the standards required by customers for good units […]

978-0134475585 Chapter 17 Solution 5

SOLUTION EXHIBIT 17-29B Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign Costs to the Units Completed and Units in Ending Work-in-Process Inventory; Weighted-Average Method of Process Costing for ZanyBrainy Corporation for October 2017. […]

978-0134475585 Chapter 17 Solution 4

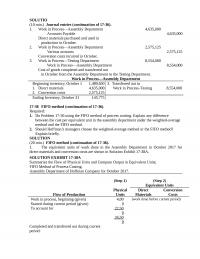

SOLUTION EXHIBIT 17-44B Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign Costs to the Units Completed and Units in Ending Work-in-Process Inventory; FIFO Method of Process Costing, Stitching Department of Spelling Sports for […]

978-0134475585 Chapter 17 Solution 3

SOLUTION (20 min.) Operation costing. 1. Calculate the conversion cost rates for each department: Relax Refresh Total Budgeted Conversion Cost Cost Driver Budgeted Quantity of Cost Driver Conversion Cost Rate Mixing $11,760 Direct labor-hours 1,200 $9.80 per labor-hour Blending 20,160 […]

978-0134475585 Chapter 17 Solution 2

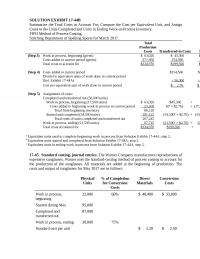

SOLUTIO (10 min.) Journal entries (continuation of 17-36). 1. Work in Process––Assembly Department 4,635,000 Accounts Payable 4,635,000 Work in Process––Assembly Department Beginning inventory, October 1 1,489,650 1. Direct materials 4,635,000 2. Conversion costs 2,575,125 3. Transferred out to Work in […]

978-0134475585 Chapter 17 Solution 1

CHAPTER 17 PROCESS COSTING 17-1 Give three examples of industries that use process-costing systems. Industries using process costing in their manufacturing area include chemical processing, oil 17-2 In process costing, why are costs often divided into two main classifications? Process […]

978-0134475585 Chapter 16 Solution 5

SOLUTION EXHIBIT 16-23 (all numbers are in thousands) 16-24 Alternative joint-cost-allocation methods, further-process decision. The Tempura Spirits Company produces two products—methanol (wood alcohol) and turpentine—by a joint process. Joint costs amount to $124,000 per batch of output. Each batch totals […]

978-0134475585 Chapter 16 Solution 4

SOLUTION(40 min.) Joint-cost allocation, process further or sell. 1. a. Physical-measure method Red Rock White Rock Gravel Total .20; .30; .50 × $190,000 b. Sales Value at Split off method Red Rock White Rock Gravel Total Sales Value of total […]

978-0134475585 Chapter 16 Solution 3

SOLUTION (25 min.) Methods of joint-cost allocation, ending inventory. 1. Net realizable value of human product: Net realizable value of veterinarian product: 500 gallons × ($450 – $20) = $215,000 Joint costs: $50,000 + $155,000 = $205,000 Joint costs charged […]

978-0134475585 Chapter 16 Solution 2

SOLUTION (30 min.) Joint-cost allocation, sales value, physical measure, NRV methods. 1a. PANEL A: Allocation of Joint Costs using Sales Value at Splitoff Method Special B/ Beef Ramen Special S/ Shrimp Ramen Total Sales value of total production at splitoff […]

978-0134475585 Chapter 16 Solution 1

CHAPTER 16 COST ALLOCATION: JOINT PRODUCTS AND BYPRODUCTS 16-1 Give two examples of industries in which joint costs are found. For each example, what are the individual products at the splitoff point? Exhibit 16-1 presents many examples of joint products […]

978-0134475585 Chapter 15 Solution 6

SOLUTION (20 min.) Support-department cost allocations: direct, step-down, and reciprocal methods. 1 a. Allocate the total Support Department costs to the operating departments under the Direct Allocation Method: Eastern Department Western Department Departmental Overhead Costs $650,000 $ 920,000 From: Information […]

978-0134475585 Chapter 15 Solution 5

SOLUTION (20-25 mins.) Stand-alone revenue allocation 1. Allocation using individual selling price per unit. Computer Hardware Component Individual Selling Price per Unit Percentage of Total Price Allocation % × $1,500 2. Allocation using cost per unit Computer Hardware Component Cost […]

978-0134475585 Chapter 15 Solution 4

SOLUTION (20 min.) Fixed cost allocation. 1. i) Allocation using actual usage. Department (1) Actual Usage (2) Percentage of Total Usage (3) = (2) ÷ 130,000 Allocation (4) = (3) × $2,000,000a expense related to building. ii) Allocation using planned […]

978-0134475585 Chapter 15 Solution 3

SOLUTION (50 min.) Support-department cost allocation, reciprocal method (continuation of 15-19). 1a. Support Departments Operating Departments AS I S Govt. Corp. Reciprocal Method Computation AS = $600,000 + 0.10 IS IS =$2,400,000 + 0.25AS IS = $2,400,000 + 0.25 ($600,000 […]

978-0134475585 Chapter 15 Solution 2

SOLUTION (20 min.) Revenue allocation, bundled products. 1a. Under the stand-alone revenue-allocation method based on selling price, Smarty will be allocated 40% of all revenues, or $36 of the bundled selling price, and Sublime will be allocated 60% of all […]

978-0134475585 Chapter 15 Solution 1

CHAPTER 15 ALLOCATION OF SUPPORT-DEPARTMENT COSTS, COMMON COSTS, AND REVENUES 15-1 Distinguish between the single-rate and the dual-rate methods. The single-rate (cost-allocation) method makes no distinction between fixed costs and variable 15-2 Describe how the dual-rate method is useful to […]

978-0134475585 Chapter 14 Solution 4

SOLUTION (20 min.)Market-share and market-size variances (continuation of 14-27). In some editions of the text, the last sentence before “Required” reads “However, actual total sales volume in the western region was 1.5 million cartons.” The word “western” should be replaced […]

978-0134475585 Chapter 14 Solution 3

SOLUTION (25 min.) Cost allocation to divisions. Percentages for various allocation bases (old and new): Pulp Paper Fibers Total (1) Division margin percentages $6,000,000; $14,600,000; $19,400,000 ¸ ¸ 30.0 15.0 55.0 100.0 (3) Share of floor space 106,400; 70,680; 202,920 […]

978-0134475585 Chapter 14 Solution 2

Customer-Level Operating Income $126,45 0 $81,225 $1,050 $(15,300) $(25,050) -$60,00 0 -$30,00 0 $ 0 $30,00 0 $60,00 0 $90,00 0 $120,00 0 $150,00 0 Customers Custo mer-Le vel Opera ting Incom e Grainger Avery Okie Duran Wizard SOLUTION (20−30 […]

978-0134475585 Chapter 14 Solution 1

CHAPTER 14 COST ALLOCATION, CUSTOMER-PROFITABILITY ANALYSIS, AND SALES-VARIANCE ANALYSIS 14-1 “I’m going to focus on the customers of my business and leave cost-allocation issues to my accountant.” Do you agree with this comment by a division president? Explain. Disagree. Cost […]

978-0134475585 Chapter 13 Solution 5

SOLUTION (25 min.) Cost-plus, target return on investment pricing. ´ 2. Revenues* $4,800,000 Variable costs [($3.00 + $2.00) 400,000 cases ´ 2,000,000 Contribution margin 2,800,000 Fixed costs ($400,000 + $700,000 + $500,000) 1,600,000 Operating income (from requirement 1) $1,200,000 * […]

978-0134475585 Chapter 13 Solution 4

SOLUTION (20 mins.) Anti-trust laws and pricing. 1. The company is not practicing price discrimination because all customers are being offered the same prices. The offer is simply restricting the times and locations that the promotion is available but not […]

978-0134475585 Chapter 13 Solution 3

SOLUTION (25 min.) Considerations other than cost in pricing decisions. 1. Guest nights on weeknights: 18 weeknights × 100 rooms × 70% = 1,260 Guest nights on weekend nights: Total costs for June: Depreciation $ 25,000 Administrative costs 40,000 Fixed […]

978-0134475585 Chapter 13 Solution 2

SOLUTION (20 min.) Target costs, effect of product-design changes on product costs. 1. and 2. Manufacturing costs of HJ6 in 2016 and 2017 are as follows: 2016 2017 Per Unit Per Unit Total (2) = Total (4) = (1) (1) […]

978-0134475585 Chapter 13 Solution 1

CHAPTER 13 PRICING DECISIONS AND COST MANAGEMENT 13-1 What are the three major influences on pricing decisions? The three major influences on pricing decisions are 13-2 “Relevant costs for pricing decisions are full costs of the product.” Do you agree? […]

978-0134475585 Chapter 12 Solution 6

SOLUTION EXHIBIT 12-33B Strategy Map for Scott Company In the learning and growth perspective, Scott measures the percentage of employees trained in quality management and the percentage of manufacturing processes with real-time feedback. These objectives improve manufacturing processes, which has […]

978-0134475585 Chapter 12 Solution 5

SOLUTION EXHIBIT 12-42A Strategy Map for WrightAir On the business side of the balanced scorecard, WrightAir measures the motivation of ground crew (learning and growth perspective) that helps to reduce turnaround time of the planes on the ground (internal business […]

978-0134475585 Chapter 12 Solution 4

SOLUTION(30 min.) Balanced scorecard. 1. The market for color laser printers is competitive. Vic’s strategy is to produce and sell high-quality laser printers at a low cost. The key to achieving higher quality is reducing defects The scorecard correctly measures […]

978-0134475585 Chapter 12 Solution 3

SOLUTION (20 min.) Analysis of growth, price-recovery, and productivity components (continuation of 12-25 and 12-26). Effect of the industry-market-size factor on operating income Of the 10-unit increase in sales from 200 to 210 units, 3% or 6 (3% 200) […]

978-0134475585 Chapter 12 Solution 2

SOLUTION (25–30 min.) Strategic analysis of operating income (continuation of 12-21). 1. Operating Income Statement 2016 2017 Revenues ($30 ´ 200,000; $31 ´ 225,000) $6,000,000 $6,975,000 2. The Growth Component Revenue effect of growth = Actual units of Actual units […]

978-0134475585 Chapter 12 Solution 1

CHAPTER 12 STRATEGY, BALANCED SCORECARD, AND STRATEGIC PROFITABILITY ANALYSIS 12-1 Define strategy. 12-2 Describe the five key forces to consider when analyzing an industry. The five key forces to consider in industry analysis are: (1) competitors, (2) potential entrants into […]

978-0134475585 Chapter 11 Solution 8

SOLUTION (20–25 min.) Relevant costs, contribution margin, product emphasis. 1. Cola Lemonade Punch Natural Orange Juice 2. The argument fails to recognize that shelf space is the constraining factor. There are only 12 feet of front shelf space to be […]

978-0134475585 Chapter 11 Solution 7

SOLUTION (20 min.) Choosing customers. If Newbury accepts the additional business from Kimberly, it would take an additional 800 machine-hours. If Newbury accepts all of Kimberly’s and Wallace’s business for February, it Wallace Kimberly Corporation Corporation Contribution margin per machine-hour […]

978-0134475585 Chapter 11 Solution 6

SOLUTION (30 min.) Special order, activity-based costing. 1. Direct materials cost per unit ($600,000 10,000 units) = $60 per unit Reward One’s opera&ng income under the alterna&ves of accep&ng/rejec&ng the special order are: Without One-Time Only Special Order 10,000 […]

978-0134475585 Chapter 11 Solution 5

SOLUTION (15-20 min.) Short-run pricing, capacity constraints. 1. Per pair of shorts: Fabric (3 yards ´ $12 per yard) If Fashion Fabrics can get all the fabric it needs and has sufficient production capacity, then the minimum price it should […]

978-0134475585 Chapter 11 Solution 4

SOLUTION (30 min.) Make versus buy, activity-based costing, opportunity costs. 1. Relevant costs under buy alternative: Relevant costs under make alternative: Direct materials $320,000 Direct manufacturing labor 160,000 Variable manufacturing overhead 80,000 Inspection, setup, materials handling 8,000 Machine rent 12 […]

978-0134475585 Chapter 11 Solution 3

SOLUTION (25 min.) Closing down divisions. 1. and 2. Division A Division B Sales $504,000 $948,000 Variable costs of goods sold ($440,000 ´ 0.90; $930,000 ´ 0.80) Division A Division B Fixed costs of goods sold ($440,000 ´ 0.10; $930,000 […]

978-0134475585 Chapter 11 Solution 2

SOLUTION (25 min.) Dropping a customer, activity-based costing, ethics. 1. CRS would not benefit from dropping Donnelly’s Pizza because it would lose $43,680 in revenues and save $43,344 in costs resulting in a $336 decrease in operating income. Difference: Incremental […]

978-0134475585 Chapter 11 Solution 1

CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION 11-1 Outline the five-step sequence in a decision process. The five steps in the decision process outlined in Exhibit 11-1 of the text are 1. Identify the problem and uncertainties. 11-2 Define relevant […]

978-0134475585 Chapter 10 Solution 7

SOLUTION (30 min.) Multiple regression (continuation of 10-42). 1. Solution Exhibit 10-43 presents the regression output for medical supplies costs using both number of procedures and number of patient-hours as independent variables (cost drivers). SOLUTION EXHIBIT 10-43 Regression Output for […]

978-0134475585 Chapter 10 Solution 6

SOLUTION (30–40 min.) Cost estimation, cumulative average-time learning curve. 1. Cost to produce the 2nd through the 7th troop deployment boats: ´ $1,194,000 Direct manufacturing labor (DML), 61,8521 $42 ´ 2,597,784 Variable manufacturing overhead, 61,852 $26 ´ 1,608,152 Other manufacturing […]

978-0134475585 Chapter 10 Solution 5

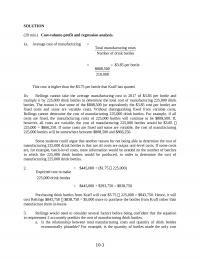

SOLUTION (20 min.) Cost-volume-profit and regression analysis. 1a. Average cost of manufacturing = Total manufacturing costs Number of drink bottles = $808,500 210,000 = $3.85 per bottle This cost is higher than the $3.75 per bottle that Kraff has quoted. […]

978-0134475585 Chapter 10 Solution 4

SOLUTION (15-20min.) Interpreting regression results, matching time periods. 1. Here is the regression data for monthly operating costs as a function of the total freight miles travelled by Sprit vehicles: SUMMARY OUTPUT Regression Statistics ANOVA df SS MS F Significance […]

978-0134475585 Chapter 10 Solution 3

SOLUTION (30min.) High-low method and regression analysis. 1. See Solution Exhibit 10-36. SOLUTION EXHIBIT 10-36 250 300 350 400 450 500 $22,000 $23,000 $24,000 $25,000 $26,000 $27,000 $28,000 $29,000 Number of Weekly Orders Weekly Total Costs 2. Number of Orders […]

978-0134475585 Chapter 10 Solution 2

.SOLUTION (20 min.) Various cost-behavior patterns. 1. K 2. B 3. G 10-24 Matching graphs with descriptions of cost and revenue behavior. (D. Green, adapted) Given here are a number of graphs. Required: The horizontal axis of each graph represents […]

978-0134475585 Chapter 10 Solution 1

CHAPTER 10 DETERMINING HOW COSTS BEHAVE 10-1 What two assumptions are frequently made when estimating a cost function? The two assumptions are 1. Variations in the level of a single activity (the cost driver) explain the variations in the 2. […]

978-0134475585 Chapter 9 Solution 7

SOLUTION (30–35 min.) Comparison of variable costing and absorption costing. 1. Since production volume variance is unfavorable, the budgeted fixed manufacturing overhead must be larger than the fixed manufacturing overhead allocated. = – 2. The problem provides the beginning and […]