Archives: Solution Manual

978-0134475585 Chapter 9 Solution 6

SOLUTION (60 min.) Variable and absorption costing and breakeven points 1. 2017 Variable-Costing Based Operating Income Statement Revenues (1,300 boards ´ $800 per board) Variable costs: Beginning inventory (240 boards ´ $375 per board) $ 90,000 Variable manufacturing costs (1,200 […]

978-0134475585 Chapter 9 Solution 5

SOLUTION (25 min.) Cost allocation, downward demand spiral. SOLUTION EXHIBIT 9-45 2017 Master Budget (1) Practical Capacity (2) 2018 Master Budget (3) Budgeted fixed cost per meal Budgeted fixed costs ¸ Denominator level ($1,533,000 1,050,000; $1,533,000 1,460,000; ¸ ¸ $1,533,000 […]

978-0134475585 Chapter 9 Solution 4

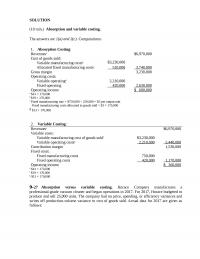

SOLUTION (10 min.) Absorption and variable costing. The answers are 1(a) and 2(c). Computations: 1. Absorption Costing: Revenuesa Cost of goods sold: $6,970,000 Operating costs: Variable operatingd Fixed operating Operating income 2,210,000 420 ,000 2 ,630,000 $ 600 ,000 a […]

978-0134475585 Chapter 9 Solution 3

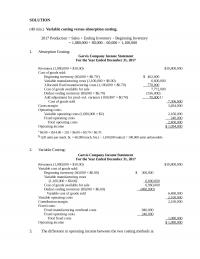

SOLUTION (40 min.) Variable costing versus absorption costing. 2017 Production = Sales + Ending Inventory – Beginning Inventory 1. Absorption Costing: Garvis Company Income Statement For the Year Ended December 31, 2017 Revenues (1,080,000 × $10.00) $10,800,000 Cost of goods […]

978-0134475585 Chapter 9 Solution 2

SOLUTION (20 min.) Throughput costing (continuation of Exercise 9-21). 1. April 2017 May 2017 Direct material cost of goods sold Beginning inventory Direct materials in goods manufacturedb $ 0 3 ,350,000 $1,005,000 2 ,680,000 Cost of goods available for sale […]

978-0134475585 Chapter 9 Solution 1

CHAPTER 9 INVENTORY COSTING AND CAPACITY ANALYSIS 9-1 Differences in operating income between variable costing and absorption costing are due solely to accounting for fixed costs. Do you agree? Explain. 9-2 Why is the term direct costing a misnomer? The […]

978-0134475585 Chapter 8 Solution 7

SOLUTION EXHIBIT 8-36 Variable Manufacturing Overhead Actual Costs Incurred (1) Actual Input Qty. × Budgeted Rate (2) Flexible Budget: Budgeted Input Qty. Allowed for Actual Output × Budgeted Rate (3) Allocated: Budgeted Input Qty. Allowed for Actual Output × Budgeted […]

978-0134475585 Chapter 8 Solution 6

SOLUTION (3040 min.) Straightforward coverage of manufacturing overhead, standard-costing system. 1. Solution Exhibit 8-28 shows the computations. Summary details are: Actual Flexible Budget Output units 66,500 66,500 Allocation base (machine-hours) 75,700 79,800a Allocation base per output unit 1.14b1.2 An overview […]

978-0134475585 Chapter 8 Solution 5

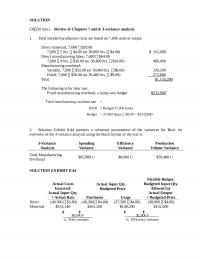

SOLUTION (3050 min.) Review of Chapters 7 and 8, 3-variance analysis. 1. Total standard production costs are based on 7,600 units of output. Direct materials, 7,600 $20.00 Direct manufacturing labor, 7,600 $64.00 7,600 4 hrs. $16.00 […]

978-0134475585 Chapter 8 Solution 4

SOLUTION (20 min.) Overhead variances, service setting. 1. and 2. Variable and Fixed Technology Overhead Variance Analysis for Carlyle Capital Company for the first quarter of 2017 Actual Costs Incurred Actual Input Qty. Budgeted Rate Flexible Budget: Budgeted Input […]

978-0134475585 Chapter 8 Solution 3

SOLUTION (20 min.) Activity-based costing, batch-level variance analysis 1. Static budget number of crates = Budgeted pairs shipped / Budgeted pairs per crate 2. Flexible budget number of crates = Actual pairs shipped / Budgeted pairs per crate = 180,000/15 […]

978-0134475585 Chapter 8 Solution 2

SOLUTION (30 min.) Fixed manufacturing overhead variance analysis (continuation of 8-23). 1. Budgeted standard direct manufacturing labor used = 0.02 per baguette Budgeted output = 3,100,000 baguettes Budgeted standard direct manufacturing labor-hours Budgeted fixed manufacturing overhead costs = 62,000 × […]

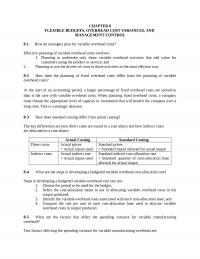

Chapter 8 How Do Managers Plan For Variable Overhead Costs

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 How do managers plan for variable overhead costs? Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities that add value for 8-2 […]

978-0134475585 Chapter 7 Solution 7

SOLUTION (30 min.) Direct-cost and selling price variances. 1. Computing unit selling prices and unit costs of inputs: Actual selling price = $3,626,700 ÷ 462,000 2., 3., and 4. The actual and budgeted unit costs are: Actual Budgeted Direct materials […]

978-0134475585 Chapter 7 Solution 6

SOLUTION (20–30 min.) Direct materials and manufacturing labor variances, solving unknowns. All given items are designated by an asterisk. Actual Costs Incurred (Actual Input Qty. × Actual Price) Actual Input Qty. × Budgeted Price Flexible Budget (Budgeted Input Qty. Allowed […]

978-0134475585 Chapter 7 Solution 5

SOLUTION (60 min.) Comprehensive variance analysis review Actual Results Units sold (90% × 700,000) 630,000 Selling price per unit $8.20 Direct materials purchased and used: Direct materials per unit $3.90 Total direct materials cost (630,000 × $3.90) $2,457,000 Direct manufacturing […]

978-0134475585 Chapter 7 Solution 4

SOLUTION (45 min.) Static and flexible budgets, service sector. 1. Static Budget Revenue (8,200 × 0.8% × $145,000) $9,512,000 Variable costs: Professional labor (8 × $45 × 8,200) 2,952,000 2. Actual results for third quarter 2017: Revenue (10,250 × 0.8% […]

978-0134475585 Chapter 7 Solution 3

SOLUTION (30 min.) Price and efficiency variances, journal entries. 1. Direct materials and direct manufacturing labor are analyzed in turn: Actual Costs Incurred (Actual Input Qty. × Actual Price) Actual Input Qty. × Budgeted Price Flexible Budget (Budgeted Input Qty. […]

978-0134475585 Chapter 7 Solution 2

SOLUTION (25–30 min.) Flexible-budget preparation and analysis. 1. Variance Analysis for Bank Management Printers for September 2017 Level 1 Analysis Actual Results (1) Static-Budget Variances (2) = (1) – (3) Static Budget (3) Units sold 12 ,000 3 ,000 U […]

978-0134475585 Chapter 7 Solution 1

CHAPTER 7 FLEXIBLE BUDGETS, DIRECT-COST VARIANCES, AND MANAGEMENT CONTROL 7-1 What is the relationship between management by exception and variance analysis? Management by exception is the practice of concentrating on areas not operating as expected and 7-2 What are two […]

978-0134475585 Chapter 6 Solution 8

SOLUTION (60 min.) Comprehensive budgeting problem; activity-based costing, operating and financial budgets. 1a. Revenues Budget For the Month of June, 2018 Units Selling Price Total Revenues Regular 2,000 $120 $240,000 b. Production Budget For the Month of June, 2018 Product […]

Chapter 6 Tyva Makes A Very Popular Undyed

11. Nonmanufacturing Costs Budget For the Year Ending December 31, 2018 Variable Fixed Total Marketing $21,150 $90,000 $111,150 12. Budgeted Income Statement For the Year Ending December 31, 2018 Revenue $528,000 Cost of goods sold 396,240 Gross margin 131,760 Operating […]

978-0134475585 Chapter 6 Solution 6

4. Schedule 4: Direct Manufacturing Labor Budget for January 2018 Labor Category Cost Driver Units DML Hours per Driver Unit Total Hours Wage Rate Total 5. Schedule 5: Manufacturing Overhead Budget for January 2018 At Budgeted Level of 13,000 Direct […]

978-0134475585 Chapter 6 Solution 5

SOLUTION (15 min.) Responsibility of purchasing agent. The cost of the biscuits is usually the responsibility of the purchasing agent, and usually controllable by the Central Warehouse. However, in this scenario, Betty the cook has taken the Paula should not […]

978-0134475585 Chapter 6 Solution 4

SOLUTION (40 min.) Budget schedules for a manufacturer. 1a. Revenues Budget Broncos Blankets Rams Blankets Total b. Production Budget in Units Broncos Blankets Rams Blankets Budgeted unit sales 140 195 Add budgeted ending fin. goods inventory 24 29 Total requirements […]

978-0134475585 Chapter 6 Solution 3

SOLUTION (20–30 min.) Kaizen approach to activity-based budgeting (continuation of 6-30). 1. Budgeted Cost-Driver Rates Activity Cost Hierarchy January February March Ordering Batch-level $45.00 $44.82000a $44.64072b The March 2018 rates can be used to compute the total budgeted cost for […]

978-0134475585 Chapter 6 Solution 2

SOLUTION (30 min.) Revenues and production budget. 1. Selling Price Units Sold Total Revenues 12-ounce bottles $0.30 6,000,000a$1,800,000 2. Budgeted unit sales (12-ounce bottles) 6,000,000 Add target ending finished goods inventory 660,000 Total requirements 6,660,000 Deduct beginning finished goods inventory […]

978-0134475585 Chapter 6 Solution 1

CHAPTER 6 MASTER BUDGET AND RESPONSIBILITY ACCOUNTING 6-1 What are the four elements of the budgeting cycle? The budgeting cycle includes the following elements: a. Planning the performance of the company as a whole as well as planning the 6-2 […]

978-0134475585 Chapter 5 Solution 6

SOLUTION (50 min.) ABC, implementation, ethics. 1. Plum Electronics should not emphasize the Maximum model and should not phase out the Mammoth model. Under activity-based costing, the Maximum model has an operating income percentage of less than 3%, while the […]

978-0134475585 Chapter 5 Solution 5

SOLUTION (40 min.) ABC, health care. 1a. Medical supplies rate = years-patient ofnumber Total costs supplies Medical = $242,000 110 = space offeet square ofamount Total costs maint. clinic andRent = $138,600 21,000 = $6.60 per square foot = years-patient […]

978-0134475585 Chapter 5 Solution 4

SOLUTION (50 min.) Activity-based costing. 1. Overhead allocation using a simple job-costing system, where overhead is allocated based on machine hours: Job 220 Job 330 Overhead allocateda$588.60 $1,373.40 a $19.62 per machine-hour × 30 hours; 70 hours 2. Overhead allocation […]

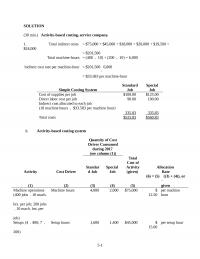

978-0134475585 Chapter 5 Solution 3

SOLUTION (30 min.) Activity-based costing, service company. 1. Total indirect costs = $75,000 + $45,000 + $18,000 + $20,000 + $19,500 + $24,000 Simple Costing System Standard Job Special Job Cost of supplies per job $100.00 $125.00 Direct labor cost […]

978-0134475585 Chapter 5 Solution 2

SOLUTION (20 min.) Plantwide, department, and ABC indirect cost rates. 1. Actual plantwide variable MOH rate based on machine hours, $280,000 ¸ 5,000 $56 per machine hour Southern Motors Caesar Motors Jupiter Auto Total Variable manufacturing overhead, allocated based on […]

978-0134475585 Chapter 5 Solution 1

CHAPTER 5 ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT 5-1 What is broad averaging, and what consequences can it have on costs? Broad averaging (or “peanut-butter costing”) describes a costing approach that uses broad 5-2 Why should managers worry about product overcosting […]

978-0134475585 Chapter 4 Solution 7

1/1/201 7 25,00 0 630,00 0 1/1/201 7 280,00 0 2,900,00 0 1/1/201 7 320,00 0 2,930,00 0 650,00 0 Dir. Man.Lbr 880,00 0 2,900,00 0 12/31/201 7 45,00 0 Dir. Matls. 630,00 0 12/31/201 7 290,00 0 OH Alloc. […]

978-0134475585 Chapter 4 Solution 6

Work in process inventory 12/31/2017 SOLUTION (35 min.) General ledger relationships, under- and overallocation. The solution assumes all materials used are direct materials. A summary of the T-accounts for Southwick Company before adjusting for under- or overallocation of overhead follows: […]

978-0134475585 Chapter 4 Solution 5

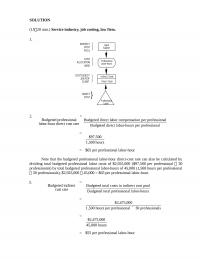

SOLUTION (1520 min.) Service industry, job costing, law firm. 1. Profession al La bor-Hou rs Lega l Support COST OBJECT: JOB FOR CLIENT INDIRECT COST POOL COST ALLOCATION BASE } DIRECT COST Ind irect Costs Direct Costs […]

978-0134475585 Chapter 4 Solution 4

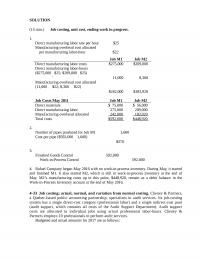

SOLUTION (15 min.) Job costing, unit cost, ending work in progress. 1. Direct manufacturing labor rate per hour $25 Manufacturing overhead cost allocated per manufacturing labor-hour $22 Job M1 Job M2 ¸ ¸ 11,000 8,360 Manufacturing overhead cost allocated (11,000 […]

978-0134475585 Chapter 4 Solution 3

SOLUTION (10–15 min.) Accounting for manufacturing overhead. 1. Budgeted manufacturing overhead rate = $4,140,000 180,000 labor-hours = $23 per direct labor-hour 2. Work-in-Process Control 4,347,000 3. $4,337,000– $4,347,000 = $10,000 overallocated, an insignificant amount of difference compared to manufacturing overhead […]

978-0134475585 Chapter 4 Solution 2

SOLUTION (20 -30 min.) Job costing, normal and actual costing. 1. Budgeted indirect- cost rate = Budgeted indirect costs (assembly support) Budgeted direct labor-hours = $8,800,000 220,000 hours = $40 per direct labor-hour Actual indirect- cost rate = Actual indirect […]

978-0134475585 Chapter 4 Solution 1

CHAPTER 4 JOB COSTING 4-1 Define cost pool, cost tracing, cost allocation, and cost-allocation base. Cost pool––a grouping of individual indirect cost items. 4-2 How does a job-costing system differ from a process-costing system? In a job-costing system, costs are […]

978-0134475585 Chapter 3 Solution 7

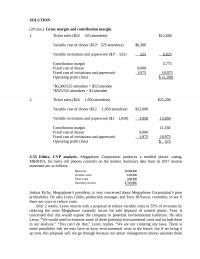

SOLUTION (20 min.) Gross margin and contribution margin. 1. Ticket sales ($24 ´ 525 attendees) $12,600 2. Ticket sales ($24 ´ 1,050 attendees) $25,200 Variable cost of dinner ($12 ´ 1,050 attendees) $12,600 Variable invitations and paperwork ($1 ´ 1,050) […]

978-0134475585 Chapter 3 Solution 6

SOLUTION (20-30 min.) CVP, alternative cost structures. 1. Variable cost per unit = $10 Contribution margin per unit = Selling price –Variable cost per unit Fixed Costs: Manager’s salary ($72,000 × 0.5) ÷12 $3,000 per month Rent 1,000 per month […]

978-0134475585 Chapter 3 Solution 5

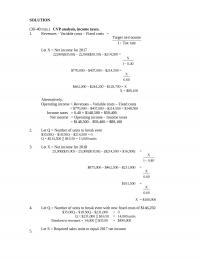

SOLUTION (30–40 min.) CVP analysis, income taxes. 1. Revenues – Variable costs – Fixed costs = rateTax 1 incomenet Target Alternatively, Operating income = Revenues – Variable costs – Fixed costs = $770,000 – $407,000 – $214,500 = $148,500 […]

978-0134475585 Chapter 3 Solution 4

SOLUTION (15 min.) Contribution margin, decision making. 1. Revenues $600,000 Deduct variable costs: 2. Contribution margin percentage = $198,000 $600,000 = 33% 3. Incremental revenue (25% × $600,000) = $150,000 Incremental contribution margin (33% × $150,000) $49,500 Incremental fixed costs […]

978-0134475585 Chapter 3 Solution 3

SOLUTION (15 min.) CVP analysis, international cost structure differences. Variable Variable Sales Price Annual Manufacturing Marketing and Contribution Operating Income to Retail Fixed Cost per Distribution Cost Margin Breakeven Breakeven for Budgeted Sales Country Outlets Costs Rug per Rug Per […]

978-0134475585 Chapter 3 Solution 2

SOLUTION (20 min.) CVP exercises. Revenues Variable Costs Contribution Margin Fixed Costs Budgeted Operating Income Orig. $11,000,000G$7,500,000G$3,500,000 $3,000,000G$500,000 1. 11,000,000 7,150,000 3,850,000a3,000,000 850,000 2. 11,000,000 7,850,000 3,150,000b3,000,000 150,000 9. Alternative 1, a 10% increase in contribution margin holding revenues constant, […]

978-0134475585 Chapter 3 Solution 1

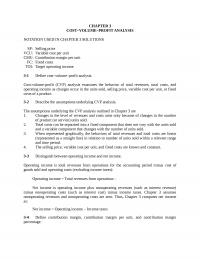

CHAPTER 3 COST–VOLUME–PROFIT ANALYSIS NOTATION USED IN CHAPTER 3 SOLUTIONS SP: Selling price VCU: Variable cost per unit CMU: Contribution margin per unit FC: Fixed costs TOI: Target operating income 3-1 Define cost–volume–profit analysis. Cost-volume-profit (CVP) analysis examines the behavior […]

978-0134475585 Chapter 2 Solution 5

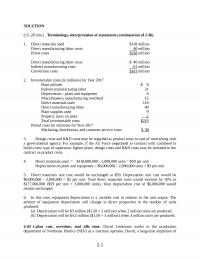

SOLUTION (15–20 min.) Terminology, interpretation of statements (continuation of 2-36). 1. Direct materials used $118 million 2. Inventoriable costs (in millions) for Year 2017 Plant utilities $ 8 Indirect manufacturing labor 21 Depreciation—plant and equipment 6 Miscellaneous manufacturing overhead 15 […]

978-0134475585 Chapter 2 Solution 4

SOLUTION (20 min.) Flow of Inventoriable Costs. (All numbers below are in millions). 1. Direct materials inventory 10/1/2017 $ 105 Direct materials used (385) Direct materials inventory 10/31/2017 $ 85 2. Total manufacturing overhead costs $ 450 Subtract: Variable manufacturing […]