Archives: Solution Manual

978-0078025556 Appendix E Solution Manual Part 1

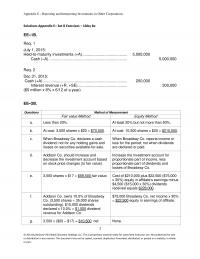

Appendix E Reporting and Interpreting Investments in Other Corporations ANSWERS TO QUESTIONS 1. A short-term investment is one that meets the two tests of (1) ready marketability and (2) management intention to convert it to cash in the short run. […]

978-0078025556 Appendix E Lecture Note Part 2

Appendix E – Reporting and Interpreting Investments in Other Corporations App E – 14 2. When a company acquires another, and both companies continue their separate legal existence, consolidated financial statements must be presented a. The parent company is the […]

978-0078025556 Appendix E Lecture Note Part 1

Appendix E – Reporting and Interpreting Investments in Other Corporations App E – 1 APPENDIX E REPORTING AND INTERPRETING INVESTMENTS IN OTHER CORPORATIONS Learning Objectives and Related Assignment Materials Learning Objectives Mini- Exercises Exercises Problems Alternate Problems Cases and Projects […]

978-0078025556 Appendix E Exercise Solution

Appendix E – Reporting and Interpreting Investments in Other Corporations © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not […]

978-0078025556 Appendix E Excel

Student Name: Class: Date Account Debit Credit 200,000 «- Correct! 200,000 40,000 «- Correct! 40,000 120,000 «- Correct! 120,000 ` 60,000 «- Correct! 60,000 200,000 «- Correct! 200,000 40,000 «- Correct! 40,000 120,000 «- Correct! 120,000 60,000 «- Correct! 60,000 […]

978-0078025532 Chapter 9 Solution Manual Part 6

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-74 9-49 (continued-4) 5. Calculation and interpretation of degree of operating leverage (DOL) under each decision alternative at Q = 400,000 units and at Q = 600,000 units. DOL, at any […]

978-0078025532 Chapter 9 Solution Manual Part 5

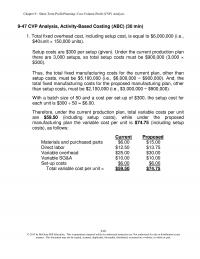

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-61 9-47 CVP Analysis, Activity-Based Costing (ABC) (30 min) 1. Total fixed overhead cost, including setup cost, is equal to $6,000,000 (i.e., $40/unit × 150,000 units). Setup costs are $300 per […]

978-0078025532 Chapter 9 Solution Manual Part 4

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-46 9-43 CVP Analysis; Commissions; Ethics (50 min) 1. Breakeven dollars (dollars in thousands), Y: Y = total fixed costs ÷ contribution margin ratio Y = ($6,120 + $1,890) ÷ (1 […]

978-0078025532 Chapter 9 Solution Manual Part 3

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-31 9-38 Profit Planning: Multiple Products (50-60 min) 1. Break-even in units: weighted-average contribution margin approach a. Overall breakeven point = F ÷ weighted-average contribution margin/unit Weighted-average unit contribution per unit […]

978-0078025532 Chapter 9 Solution Manual Part 2

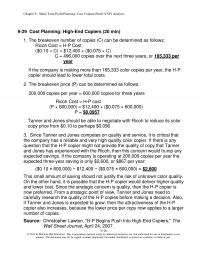

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-16 9-29 Cost Planning: High-End Copiers (20 min) 1. The breakeven number of copies (C) can be determined as follows: Ricoh Cost = H-P Cost ($0.10 × C) = $12,400 + […]

978-0078025532 Chapter 9 Solution Manual

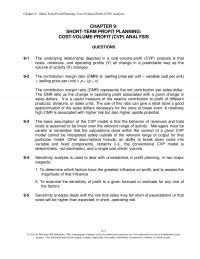

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-1 CHAPTER 9: SHORT-TERM PROFIT PLANNING: COST-VOLUME-PROFIT (CVP) ANALYSIS QUESTIONS 9-1 The underlying relationship depicted in a cost-volume-profit (CVP) analysis is that costs, revenues, and operating profits (Y) all change in […]

978-0078025532 Chapter 9 Lecture Note Part 2

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9–12 Case 9-5: Sensitivity Analysis: Regression Analysis 1. The regression analysis to identify the stores that seem to be operating at below their potential, based on relationships for all the stores […]

978-0078025532 Chapter 9 Lecture Note

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9–1 Chapter 9 Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis Teaching Notes for Cases Case 9-1: CVP Analysis; Strategy This problem can perhaps be visualized most easily by first constructing a table […]

978-0078025532 Chapter 8 Solution Manual Part 5

8-56 8-54 (continued –1) 2. The limitations of this regression are somewhat unique since the independent variables (except for average pay) and the dependent variable are rankings (ordinal numbers rather than real numbers). Thus, the issue of nonlinearity arises, but […]

978-0078025532 Chapter 8 Solution Manual Part 4

8-46 8-49 (continued -3) 2. If Lexon is involved in global production of its products, then expenses incurred from returns must be analyzed by production facility, as these costs are likely to differ among production facilities due to different equipment […]

978-0078025532 Chapter 8 Solution Manual Part 3

Chapter 8 – Cost Estimation 8-31 8-42 (continued – 3) 3. The Gilmore company is likely to have a number of sustainability issues in its business. As a company that renovates older homes, it must frequently deal with hazardous materials […]

978-0078025532 Chapter 8 Solution Manual Part 2

8-16 8-35 Cost Estimation: High-Low method (15 min) 1. Model to fit: Maintenance Expense = a + (b x M) (where M = machine hours) The highest and lowest points are months 6 and 10, respectively. Note that the point […]

978-0078025532 Chapter 8 Solution Manual

Chapter 8 – Cost Estimation 8-1 CHAPTER 8: COST ESTIMATION QUESTIONS 8-1 Cost estimation is the process of developing a well-defined relationship between a cost object and its cost driver for the purpose of predicting the cost. The cost predictions […]

978-0078025532 Chapter 8 Lecture Note Part 2

Chapter 8 – Cost Estimation 8-11 Case 8-5 Predicting the Effect of Poverty on High School Graduation Rate High School graduation rates are a key measure of economic development and potential for economic growth. The data below show the graduation […]

978-0078025532 Chapter 8 Lecture Note

Chapter 8 – Cost Estimation 8-1 Chapter 8 Cost Estimation Teaching Notes for Cases 8-1. High-Low Method and Regression Analysis 1, 2. The spreadsheet below shows the analysis of the Brenham Hospital data using both regression and high-low methods. Before […]

978-0078025532 Chapter 7 Solution Manual Part 5

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-58 7-45 (continued –2) Net Realizable Value Method M10 M15 M18 Total Units Sold 150,000 125,000 125,000 400,000 Price (after addt’l processing) 20$ 10$ 15$ Separable Processing cost 550,000$ 125,000$ […]

978-0078025532 Chapter 7 Solution Manual Part 4

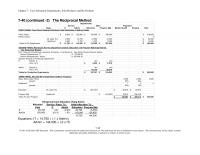

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-46 7-40 (continued -2) The Reciprocal Method Base IT Admin Education Program Mgt Mental Health Housing Total FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs Direct […]

978-0078025532 Chapter 7 Solution Manual Part 3

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-31 7-35 (continued –3) Sourcing Operations Asssembly Finishing Total DEPARTMENTAL ALLOCATION BASES Information Systems Hours 25,000 45,000 70,000 140,000 percent 17.8571% 32.1429% 50.00% 100% Facilities; square feet (000) 10,000 50,000 […]

978-0078025532 Chapter 7 Solution Manual Part 2

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-16 7-28 (continued -1) Premium Dept. Advertising Dept Sales Dept Allocation of Actuarial Dept $80,000 x .8 = $64,000 $80,000 x .1 = $8,000 $80,000 x .1 = $8,000 Allocation […]

978-0078025532 Chapter 7 Solution Manual

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-1 CHAPTER 7: COST ALLOCATION: DEPARTMENTS, JOINT PRODUCTS, AND BY-PRODUCTS QUESTIONS 7-1 The four objectives in the strategic role of cost allocation are to achieve effective cost management through methods […]

978-0078025532 Chapter 7 Lecture Note

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-1 Chapter 7 Cost Allocation: Departments, Joint Products, and By-Products Teaching Notes for Cases 7-1. Revenue Allocation; Utility Industry; Strategy This case concerns the process used in the state of […]

978-0078025532 Chapter 6 Solution Manual Part 4

Chapter 6 – Process Costing 6-40 Problem 6-50 (continued –2) Ted is apparently correct about the under-costing of ending working process. The activity-based method, which separates the batch-related costs from the other conversion costs, shows $104,329 ending work in process, […]

978-0078025532 Chapter 6 Solution Manual Part 3

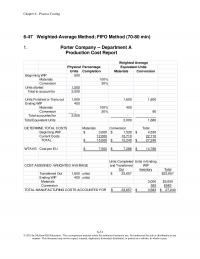

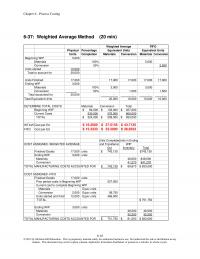

Chapter 6 – Process Costing 6-31 6-47 Weighted-Average Method; FIFO Method (70-80 min) 1. Porter Company — Department A Production Cost Report Physical Percentage Units Completion Materials Conversion Beginning WIP 500 Materials 100% Conversion 30% Units started 1,500 Total to […]

978-0078025532 Chapter 6 Solution Manual Part 2

Chapter 6 – Process Costing 6-16 6-37: Weighted Average Method (20 min) Physical Percentage Units Completion Materials Conversion Materials Conversion Beginning WIP 5,000 Materials 100% 5,000 Conversion 50% 2,500 Units started 15,000 Total to account for 20,000 Units FinIshed 17,000 […]

978-0078025532 Chapter 6 Solution Manual

Chapter 6 – Process Costing 6-1 CHAPTER 6: PROCESS COSTING QUESTIONS 6-1 A company that should use a process costing system typically has homogenous products, which pass through a series of similar processes or departments. These firms usually engage in […]

978-0078025532 Chapter 5 Solution Manual Part 4

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-42 5-47 (continued –1) 2. The additional business with AS would leave very little unused capacity(less than 3%) as shown below: Total Calls Answered Avg. No. of Minutes/ Call Total Time […]

978-0078025532 Chapter 5 Solution Manual Part 3

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-31 5-42 (continued-1) Calculation for general administration allocated to branches: Total direct labor dollar: $382,413 + $317,086 + $317,188 = $1,016,687 Allocation of general administration based on direct labor dollar: Proportion […]

978-0078025532 Chapter 5 Solution Manual Part 2

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-16 5-35 Customer Profitability Analysis (25 minutes) 1. Jerry Inc. Kate Co. Customer Unit Level Costs: Sales return(40×$5;175×$5) $200 $875 Customer Batch Level Costs: Order processing (5×$300; 30×$300) $1,500 $9,000 Sales […]

978-0078025532 Chapter 5 Lecture Note Part 3

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-29 Comparison Incrrease Total Total Batch Batch Total Total Batch Batch Total Total Batch Batch (Drop) in Cost Cost Total Gross Cost Cost Total Gross Cost Cost Total Gross Gross Product […]

978-0078025532 Chapter 5 Lecture Note Part 2

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-16 In practice, TOC accounting is similar to variable costing, and like variable costing, “Emphasis is placed on short-run differential or incremental costs rather than on long-run full costs” (Usry & […]

978-0078025532 Chapter 5 Lecture Note

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-1 Chapter 5 Activity-Based Costing and Customer Profitability Analysis Teaching Notes for Cases 5-1 Blue Ridge Manufacturing (Activity-Based Costing for Marketing Channels) Case Description: Blue Ridge Manufacturing produces and sells towels […]

978-0078025532 Chapter 4 Solution Manual Part 4

Chapter 4 – Job Costing 4-42 4-49 (continued –5) 2. Go to the Insert tab on the ribbon, and select the PivotTable button. You can choose Pivot Table or Pivot Chart; choose Pivot Table. 3. Once you have selected PivotTable […]

978-0078025532 Chapter 4 Solution Manual Part 3

Chapter 4 – Job Costing 4-31 h. Selling& Administrative Expense 2,400 Accumulated Depreciation 2,400 4-46 (Continued –1) i. Advertising Expense 5,500 Cash 5,500 j. Factory Overhead 13,500 Cash 13,500 k. Selling & Administrative Expense 13,250 Cash 13,250 l. Applied Overhead […]

978-0078025532 Chapter 4 Solution Manual Part 2

Chapter 4 – Job Costing 4-16 4-37 Application of Overhead (15 min) 1. Budgeted total overhead $360,125 Budgeted direct labor hours 33,500 Overhead rate $10.75 =$360,125/33,500 Job Direct Materials Gallons of Paint Direct Labor Hours Direct Labor Cost Applied Overhead […]

978-0078025532 Chapter 4 Solution Manual Part 1

Chapter 4 – Job Costing 4-1 CHAPTER 4: JOB COSTING QUESTIONS 4-1 The strategic role of costing is to provide accurate cost information that is need for product pricing, profitability analysis of products and customers, evaluation of managers, and refinement […]

978-0078025532 Chapter 4 Lecture Note

Chapter 4 – Job Costing 4-1 Chapter 4 Job Costing Teaching Notes For Cases 4-1. Constructo Inc. (Under or Overapplied Overhead) This case has the learning objectives of: (1) explaining when it is appropriate for a company to use a […]

978-0078025532 Chapter 3 Solution Manual Part 3

Chapter 3 – Basic Cost Management Concepts 3-26 3-51 Classification of Costs (15 Min) Parts 1 and 2 Fixed(F) or Product (P) Variable (V) Period (PD) 1.Technicians F P 2.Parts V P 3.Purchase of oil and tires V P 4.Supplies […]

978-0078025532 Chapter 3 Solution Manual Part 2

Chapter 3 – Basic Cost Management Concepts 3-16 3-42 (continued –1) 3. The growth of the company globally means that the company will be more exposed to the effects of foreign currency fluctuations. For example, a falling dollar relative to […]

978-0078025532 Chapter 3 Solution Manual Part 1

Chapter 3 – Basic Cost Management Concepts 3-1 CHAPTER 3: BASIC COST MANAGEMENT CONCEPTS QUESTIONS 3-1 Cost assignment refers to the general case of assigning costs to cost pools or cost objects. When there is a direct and traceable link […]

978-0078025532 Chapter 3 Lecture Note

Chapter 3 – Basic Cost Management Concepts 3-1 Chapter 3 Basic Cost Management Concepts Teaching Notes for Cases 3-1. Strategy; Critical Success Factors, Cost Objects, and Performance Measures Increasingly, students in accounting and business courses are expected to actively engage […]

978-0078025532 Chapter 20 Solution Manual Part 4

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20–43 20-45 (continued -1) Liquidity looks OK overall, except for the recent buildup in inventory. The current ratio has fallen below the bank restriction years ago, but has been safely […]

978-0078025532 Chapter 20 Solution Manual Part 3

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20–31 20–39 (continued -1) 2. [Operating Income – (.06 x Invested Assets)] x .10 = Bonus Amount The total bonuses for each division and in total are determined as follows: […]

978-0078025532 Chapter 20 Solution Manual Part 2

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20–16 20-28 Compensation and Trust (15 min) This question is intended primarily for class discussion or for a short written project. The answers are likely to vary. I would have […]

978-0078025532 Chapter 20 Solution Manual

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20-1 CHAPTER 20: MANAGEMENT COMPENSATION, BUSINESS ANALYSIS, AND BUSINESS VALUATION QUESTIONS 20-1 The key objective of the firm is to develop management compensation plans that support the firm’s strategic objectives: […]

978-0078025532 Chapter 20 Lecture Note Part 3

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20–31 experience and commitment of its employees (an environment fostered by this long relationship) as one of its sustaining competitive advantages (Salter and Dayley 2000). If John Deere used (or […]