Archives

978-1111823450 Chapter 1 Solution Manual Part 1

Title: 1.1 terms and concepts discussed in the chapter. Students may wish to consult the glossary at the end of the book in addition to the definitions and discussions in the chapter. Title: 1.2 QA_Ori: Setting Goals and Strategies: Although […]

978-1111823450 Chapter 1 Solution Manual Part 2

QA_Edit: Title: 1.24 millions of US$) QA_Edit: Title: 1.25 QA_Ori: (Veldt, a South African firm; retained earnings relations) Title: 1.23 QA_Ori: (GrandRider, an automotive manufacturer; income statement relations.) (amounts in millions of pounds sterling) QA_Ori: (AutoCo, an automotive manufacturer; income […]

978-1111823450 Chapter 1 Solution Manual Part 3

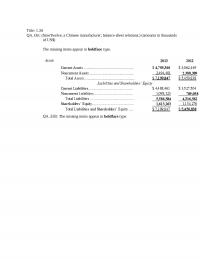

Title: 1.34 QA_Ori: (SinoTwelve, a Chinese manufacturer; balance sheet relations.) (amounts in thousands of US$) The missing items appear in boldface type. QA_Edit: The missing items appear in boldface type. Title: 1.35 QA_Ori: (EastonHome, a consumer products manufacturer; income statement […]

978-1111823450 Chapter 1 Solution Manual Part 4

Title: 1.40 QA_Ori: (Block’s Tax and Bookkeeping Services; cash versus accrual accounting.) (amounts in US$) a. Income for July 2013: QA_Edit: (Block’s Tax and Bookkeeping Services; cash versus accrual accounting.) (amounts in US$) a. Income for July 2013: (1) Cash […]

978-1111823450 Chapter 10 Solution Manual Part 1

CHAPTER 10 LONG-LIVED TANGIBLE AND INTANGIBLE ASSE T S Questions, Exercises, and Problems: Answers and S ol u tio ns 10.1 See the text or the glossary at the end of the book. 10.2 The central concept underlying GAAP for […]

978-1111823450 Chapter 10 Solution Manual Part 2

10.27 (Wilcox Corporation; working backward to derive proceeds fr om disposition of plant assets.) (amounts in US$) 10.28 (Journal entries to correct accounting errors.) (amounts in US$) 10.29 (Moon Macrosystems; recording transactions involving tangible and intangible assets.) (amounts in US$) […]

978-1111823450 Chapter 11 Solution Manual Part 1

CHAPTER 11 NOTES, BONDS, AND L EASES Questions, Exercises, and Problems: Answers and S ol u tio ns 11.1 See the text or the glossary at the end of the book. 11.2 Generally, accountants initially record assets at acquisition cost […]

978-1111823450 Chapter 11 Solution Manual Part 2

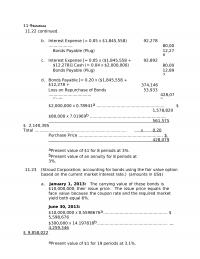

……………………………………. 2 d. Bonds Payable [= 0.20 X ($1,845,558 + $12,278 + 374,146 $12,892)]…………………………………………….. Loss on Repurchase of Bonds ……………………………. Cash……………………………………………………. 53,933 428, 07 9 $2,000,000 X 0 . 78941a ……………………………………………… $ 1,578,820 $80,000 X 7.01969b ………………………………………………….. 56 1 , […]

978-1111823450 Chapter 11 Solution Manual Part 3

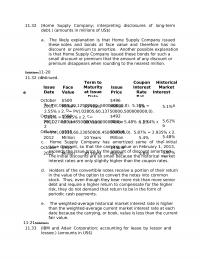

b Oc tob er 2012 $550 Million 10 Years $545.6 Million 5.4% 5.48 % c Oc tob er 2012 $450 Million 30 Years $445.6 Million 5.8% 5.87 % d 11.32 (Home Supply Company; interpreting disclosures of long-term debt.) (amounts in […]

978-1111823450 Chapter 12 Solution Manual Part 1

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. 40 Solutions12–22 i. 2013 Pension Expe ns e ……………………………………………….. 253 394 Assets = Liabilities + Shareholders’ Equity (Class.) […]

978-1111823450 Chapter 12 Solution Manual Part 2

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. 12.23 (Fleet Sneaks; preparing journal entries for income tax expense.) (amounts in millions of US$) a. 2011 Income […]

978-1111823450 Chapter 12 Solution Manual Part 3

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. CHAPTER 12 LIABILITIES: OFF-BALANCE-SHEET F I N A N CI NG , RETIREMENT BENEFITS, AND INCOME T A […]

978-1111823450 Chapter 13 Solution Manual Part 1

CHAPTER 13 MARKETABLE SECURITIES AND D ERIVA T IVES Questions, Exercises, and Problems: Answers and S ol u tio ns 13.1 See the text or the glossary at the end of the book. 13.2 a. Debt securities that a firm […]

978-1111823450 Chapter 13 Solution Manual Part 2

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. liability for the full purchase price. The commitment is an executory contract. It recognizes the commitment only to […]

978-1111823450 Chapter 13 Solution Manual Part 3

13.31 continued. December 31, 1 13.28 (Delmar; accounting for forward commodity price contract as a cash flow hedge.) (amounts in US$) a. Delmar does not make an entry on October 31, 2013, because the forward commodity contract is a mutually […]

978-1111823450 Chapter 14 Solution Manual Part 1

CHAPTER 14 INTERCORPORATE INVESTMENTS IN COMMON STOCK Questions, Exercises, and Problems: Answers and S ol u tio ns 14.1 See the text or the glossary at the end of the book. 14.2 Control is present when one entity has the […]

978-1111823450 Chapter 14 Solution Manual Part 2

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. Solutions14-12 (8) Amortization Expense………………………………………. 4,000 Investment in Stock of Vogel Company…………… 4,000 Assets = Liabilities + Shareholders’ Equity […]

978-1111823450 Chapter 14 Solution Manual Part 3

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. Solutions14-20 14.29 b. continued. Sales Revenue …………….. $ 400,000 $ 125,000 $ 525,000 Equity in Earnings of Valley […]

978-1111823450 Chapter 15 Solution Manual Part 1

CHAPTER 15 SHAREHOLDERS’ EQUITY: CAPITAL C ONT RIB UT I ON S AND D IS T RIB UT I ON S Questions, Exercises, and Problems: Answers and S ol u tio ns 15.1 See the text or the glossary at […]

978-1111823450 Chapter 15 Solution Manual Part 2

Solutions15-12 Cash…………………………………………………………………… 46,180,000 Convertible Preferred S t ock …………………………….. 43,450, 000 Additional Paid-In Capital (Stock Warrants)……. 2,730, 000 Assets = Liabilities + Shareholders’ Equity (Class.) +46,180,000 +43,450,000 ContriCap +2,730,000 ContriCap To record issuance of convertible preferred stock with stock warrants. […]

978-1111823450 Chapter 15 Solution Manual Part 3

15-19Solutions 15.27 e. continued. Assets = Liabilities + Shareholders’ Equity (Class.) +10,000 +4,000 IncSt RE –6,000 (4b) Securities Available for Sale ……………………… 2,000 Unrealized Gain on Securities Available for Sale (Accumulated Other Comprehensive Income) ……………………… 2,0 00 Assets = […]

978-1111823450 Chapter 16 Solution Manual Part 1

CHAPTER 16 STATEMENT OF CASH FLOWS: ANOTHER LOO K Problems and Cases: Answers and S ol u tio ns 16.1 (Effects of transactions on statement of cash flows.) (amounts in US$) a. The journal entry to record this transaction is: […]

978-1111823450 Chapter 16 Solution Manual Part 2

16-11Solutions 16.4 continued. (13) Property, Plant, and Eq ui pm en t ………………………. 875.7 Solutions16-12 Cash (Investing—Acquisition of Property, Plant, and Equipment)…………………………….. 875.7 (14) Investments in Securities ……………………………….. 44.5 Cash (Investing—Acquisition of Su b si d i a ri e […]

978-1111823450 Chapter 16 Solution Manual Part 3

16.17 (Cypress Corporation; interpreting the statement of cash flows.) a. Although net income increased between 2011 and 2013, the b. The principal factors causing cash flow from operations to increase in 2013 is an increase in net income. Inventories decreased […]

978-1111823450 Chapter 16 Solution Manual Part 4

© 2013 Cengage Lea rning. All rights reserved. No distribution allowed without express authorization. 16.11 continued. c. During 2013, cash flow from operations exceeded net income Net I nc ome ……………………………………………… $ 101$ 324 Depreciation Expe ns e ………………………………. 560 […]

978-1111823450 Chapter 16 Solution Manual Part 5

Work Sales ……………………………… $364,212 Gain on Sale of Ma r ketable Equity Securities ……………. 3,600 $(37,50 0) (3,60 = Accounts Receivable Increase Gain Produces No Operating Cash Roth’s Share of Earnings Retained by P e r iod 326,71 2 Receipts […]

978-1111823450 Chapter 17 Solution Manual Part 1

1. (Identifying accounting p rinci p l e s. ) a. FIFO cost flow assumption. b. Allowance method. assumption. f. Effective interest method. g. Cash flow hedge. h. Market value method. i. Percentage-of-completion method. j. Allowance method. k. Fair value […]

978-1111823450 Chapter 17 Solution Manual Part 2

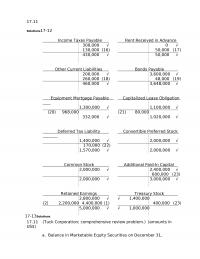

17.11 continued. Solutions17-12 I n c o m e T a x es P ay a b l e R e n t R e c e i v ed i n A d v a n c e O […]

978-1111823450 Chapter 2 Solution Manual Part 1

Title: 2.1 QA_Ori: See the text or the glossary at the end of the book. QA_Edit: See the text or the glossary at the end of the book. Title: 2.2 QA_Ori: Accounting is governed by the balance sheet equation, which […]

978-1111823450 Chapter 2 Solution Manual Part 2

Assets = Liabilities + Shareholder s’ Equity (Class.) +600 –600 (9) The placing of an order does not give rise to a journal entry because it represents QA_Edit: (Winkle Grocery Store; journal entries for various transactions.) (amounts in US$) Assets […]

978-1111823450 Chapter 2 Solution Manual Part 3

balance sheet.) (amounts in thousands of Mexican pesos [$]) a. T-accounts. Title: 2.15 QA_Ori: (Regaldo Department Store; recording transactions in T-accounts and preparing a QA_Edit: a. T-accounts. (Regaldo Department Store; recording transactions in T-accounts and preparing a balance sheet.) (amounts […]

978-1111823450 Chapter 3 Solution Manual Part 1

3-1 © 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. Solution s CHAPTER 3 THE BASICS OF RECORD KEEPING A ND FINANCIAL STATEMENT PREPARATION: INCOME S T […]

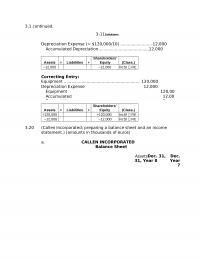

978-1111823450 Chapter 3 Solution Manual Part 2

3.1 continued. 3-11Solutions Depreciation Expense (= $120,000/10) ……………………. 12,000 Accumulated Depreciation………………………………….12,000 Assets = Liabilities + Shareholders’ Equity (Class.) –12,000 –12,000 IncSt RE Correcting Entry: Equipment …………………………………………………… ……… 120,000 Depreciation Expe ns e ……………………………………………. 12,000 Equipment Expense…………………………………………… 120,00 0 Accumulated […]

978-1111823450 Chapter 3 Solution Manual Part 3

3.23 continued. b. PATTERSON CORPORATION 3-21Solutions Income Stat e m en t For the Month of February, Year 13 Sales Revenue………………………………………………………… $ 1 , 50 0 , 00 0 Expenses: Cost of Goods S o l d ………………………………………………. $ 950,000 […]

978-1111823450 Chapter 3 Solution Manual Part 4

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. 3-31Solutions 3.27 (Regaldo Department Stores; analysis of transactions and preparation of income statement and balance sheet.) (amounts in […]

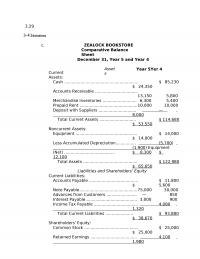

978-1111823450 Chapter 3 Solution Manual Part 5

3.29 continued. 3-41Solutions c. ZEALOCK BOOKSTORE Comparative Balance Sheet December 31, Year 5 and Year 4 Current Assets: Asset s Year 5Yer 4 Cash ………………………………………………….. $ 85,230 $ 24,350 Accounts Receivable ……………………………. 13,150 5,800 Merchandise Inventories ……………………… 6,300 5,400 Prepaid […]

978-1111823450 Chapter 3 Solution Manual Part 6

3.36 continued. (Prima Company; working backward to the balance sheet at the beginning of the period.) (amounts in US$) A T-account method for deriving the solution appears below and on the following page. The end-of-year balance appears at the bottom […]

978-1111823450 Chapter 4 Solution Manual Part 1

accounting reports as currently prepared is to present fairly the results of operations and the financial condition of the firm. Both U.S. GAAP and IFRS require reporting that results in a more conservative measurement of earnings. 4.3 One justification relates […]

978-1111823450 Chapter 4 Solution Manual Part 2

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. 4-11Solutions 4.22 (Nestlé S.A.; asset recognition and measurement.) a. Both U.S. GAAP and IFRS would recognize Investment in […]

978-1111823450 Chapter 4 Solution Manual Part 3

4.31 continued. 4-23Solutions Current Liabilities: Liabilities and Shareholders’ Equity © 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. Trade Payables ………………………………………………………… SEK 17,427 Borrowings, Current …………………………………………………. 5,896 […]

978-1111823450 Chapter 5 Solution Manual Part 1

1. QA_Ori: See the text or the glossary at the end of the book. 2. QA_Ori: Revenues measure the inflow of net assets from operating activities, and 3. QA_Ori: Cost is the economic sacrifice made to acquire goods or services. […]

978-1111823450 Chapter 5 Solution Manual Part 2

23. QA_Ori: (PharmaCare; discontinued operations.) (amounts in millions of euros) a. In Year 7, 51% [= €2,410/(€2,410 + €2,306)] of PharmaCare’s income came b. In Year 7, less than 0.2% (= €84/€51,378) of PharmaCare’s total assets were associated with discontinued […]

978-1111823450 Chapter 6 Solution Manual Part 1

2. Q A _ O r i : One can criticize a single income statement using a cash basis of accounting from two standpoints: (1) it provides a poor measure of operating performance each period because of the inaccurate matching […]

978-1111823450 Chapter 6 Solution Manual Part 2

c. I n ve n t or y …………………………………………………………. 7,500 Accounts Payable…………………………………………… 7,500 Change in Cash 6.31 (Effect of various transactions on statement of cash flows.) (amounts in US$) Note to instructors: We use this question for in-class discussion. We […]

978-1111823450 Chapter 6 Solution Manual Part 3

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. 6.35 a. continued. Accumulated Depreciation- B u il d i n g s a n d M a […]

978-1111823450 Chapter 6 Solution Manual Part 4

6-35Solutions 6.39 (Quintana Company; working backward through the statement of cash flows.) (amounts in thousands of US$) QUINTANA C O MPA NY Condensed Balance S hee t January 1, 2013 (amounts in thousands of U S $) Current Assets: Assets […]

978-1111823450 Chapter 7 Solution Manual Part 1

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. increases in the cost of theft or product obsolescence which the firm could not pass on to the […]

978-1111823450 Chapter 7 Solution Manual Part 2

7.1 continued. 2011 $ 1,571 $ 2,015.0a78.0% 2012 1,668 2,306.0b72.3% 2013 1,879 2,598.5c72.3% a0.5($2,031 + $1,999) = $2,015.0. b0.5($1,999 + $2,613) = $2,306.0. c0.5($2,613 + $2,584) = $2,598.5. 6.27 2012 14,955 2,322.5b 6.44 2013 16,326 2,439.0c 6.69 $2,191.0. b0.5($2,262 + […]

978-1111823450 Chapter 7 Solution Manual Part 3

7.26 b. continued. b. Rate on Assets (ROA) Bullseye’s ROA increased between the fiscal years ended January 31, Profit Margin The changes in the profit margin result primarily from changes in the selling and administrative Total Assets Turnover The total […]

978-1111823450 Chapter 7 Solution Manual Part 4

7.30 continued. 7.27 a. continued. b. The current and quick ratios vary considerably between fiscal 2012 and fiscal 2013, but neither company appears risky by these measures. Limito pays its suppliers more c. Limito has higher levels of debt than […]

978-1111823450 Chapter 8 Solution Manual Part 1

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. CHAPTER 8 REVENUE RECOGNITION, RECEIVABLES, A ND ADVANCES FROM C U S TO MERS Questions, Exercises, and Problems: […]

978-1111823450 Chapter 8 Solution Manual Part 2

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. 8-11Solutions (amounts in millions of pounds sterling) a. Journal entry to recognize revenues and expenses: Accounts Receivable, Gross……………………………….. […]

978-1111823450 Chapter 8 Solution Manual Part 3

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. Assets = Liabilities + 8.28 continued. Assets = Liabilities + Shareholders’ Equity (Class.) +72,000,000 –72,000,000 8.29 (Reconstructing events […]

978-1111823450 Chapter 8 Solution Manual Part 4

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. refundable room reservation. Assets = Liabilities + Shareholders’ Equity (Class.) e. February 2, 2013: Journal entry to record […]

978-1111823450 Chapter 8 Solution Manual Part 5

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. Assets = Liabilities + Shareholders’ Equity (Class.) Solutions8-42 8.47 (Areva Group: income recognition for a nuclear generator manufacturer.) […]

978-1111823450 Chapter 8 Solution Manual Part 6

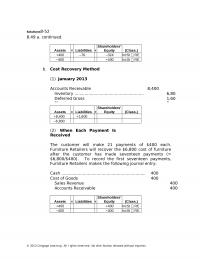

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. +400 –76 –324 IncSt RE –400 +400 IncSt RE b. Cost Recovery Method (1) January 2013 […]

978-1111823450 Chapter 9 Solution Manual Part 1

during which it receives services. All assets promise future economic benefits, so all assets are prepayments. 9.3 The underlying principle is that acquisition cost includes all costs required to prepare an asset for its intended use. Assets provide future services. […]

978-1111823450 Chapter 9 Solution Manual Part 2

210,00 0 Wages and Salaries Payable…………………………. 490,00 0 Amounts payable to and for employees. Wage and Salary Expense ………………………………… 114,800 Taxes P ayab l e ……………………………………………… 70,00 0 Payable to Profit Sharing Fund …………………….. 28,00 0 Vacation Liability ……………………………………….. 16,80 […]

978-1111823450 Chapter 9 Solution Manual Part 3

© 2013 Cengage Learning. All r ights reserved. No d is t r ibution allowed without express a u t hor ization. 9.42 (Good Luck Brands; lower-of-cost-or-market valuation; U.S. GAAP ve rsus IFRS.) (amounts in millions of US$) a. No […]

978-1111823450 Solutions to Foreign Currency Translation Solution Manual Part 1

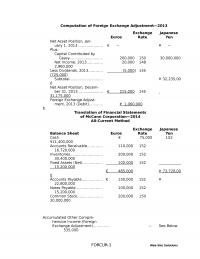

uary 1, 2013…………………. € — ¥ — Plus: Capital Contributed by Casey……………………….. 200,000 150 30,000,000 Net Income, 2013………….. 20,000 148 2,960,000 Less Dividends, 2013………… (5 ,000) 145 (725,000) Subtotal……………………….. ¥ 32,235,00 0 Net Asset Position, Decem- ber 31, 2013…………………. € […]

978-1111823450 Solutions to Foreign Currency Translation Solution Manual Part 2

ongoing basis. The only conversion required is the remission of dividends or other distributions to the parent company. The base for such distributions is total shareholders’ equity (or net assets). Exchange rate changes affect the amount of funds the foreign […]

978-1111823450 Solutions to Further Issues in Income Taxes Solution Manual

FURTHER ISSUES IN ACCOUNTING FOR INCOME TAXES Problems: Solutions DEFTAX 1.(Kleen Cleaners; measuring income tax expense.) 2012 Income Tax Expense (Plug)…………………………………… 236 2013 Income Tax Expense (Plug)…………………………………… 264 Deferred Tax Liability [= .40(€400 – €550)]……………… 60 Deferred Tax Asset [= […]

Chapter 1 1 Which The Following Not Business Activity

Chapter 1: Introduction to Business Activities and Overview of Financial Statements and the Reporting Process Key 1. The activities of a business include establishing goals and strategies, obtaining financing, making investments and conducting operations. 2. Goals are the end results […]

Chapter 1 2 Use The Abbreviations Below Classify The

107. Education Power is a charitable organization that promotes educational opportunities for inner city children and adults. Describe how the four common key activities would differ for this organization as opposed to a for-profit business entity. Setting Goals and Strategies: […]

Chapter 1 3 The FASB is an agency of the federal government

Liabilities and Shareholders’ Equity Current liabilities Accounts payable $ 5,219 $ 7,873 Salaries payable 481 594 Income taxes payable 414 580 Other current liabilities 185 1,115 Total current liabilities 6,299 10,162 Noncurrent liabilities Bonds payable, due Year 20 10,313 4,602 […]

Chapter 10 1 Firms With Tangible Long term Assets And

Chapter 10: Long-Lived Tangible and Intangible Assets Key 1. With the exception of internally developed software costs, U.S. GAAP requires that the firm expense both research and development expenditures as incurred. 2. Market-to-book-value ratios tend to be large for firms […]

Chapter 10 2 Calculating Depreciation And Amortization For Tangible

98. In calculating depreciation and amortization for tangible assets, physical factors that limit service lives include all of the following except: 99. In calculating depreciation and amortization for tangible assets, functional factors that limit service lives include: A. ordinary wear […]

Chapter 10 3 Impairment Loss All Intangibles That Not

157. An impairment loss on all intangibles that do not require amortization, except goodwill, arises when 158. An impairment loss on a trademark arises when A. the book value of the trademark exceeds the undiscounted cash flows. B. the book […]

Chapter 10 4 accumulate in the Work-in-Process Inventory account

MEASUREMENT OF DEPRECIATION AND AMORTIZATION Calculating depreciation or amortization of long-lived assets requires management to 1. Measure the depreciable or amortizable basis of the asset. 2. Estimate its service (useful) life. 3. Decide the pattern of expiration of asset cost […]

Chapter 11 1 Firms That Need Cash For Long term

Chapter 11: Notes, Bonds, and Leases Key 1. Firms typically finance long-term assets, particularly property, plant, and equipment, with long-term borrowing or funds provided directly or indirectly by shareholders. 2. The more long-term debt in a firm’s capital structure, the […]

Chapter 11 2 Us Gaap Specifies Criteria For Capital

102. U.S. GAAP specifies criteria for a capital lease. Which of the following is not one of the criteria? 103. U.S. GAAP specifies criteria for a capital lease. Which of the following is not one of the criteria? A. The […]

Chapter 11 3 Part Briefly Explain Bond Contract And

125. Part 1: Briefly explain a bond contract and its relationship to cash flows. Part 2: Define the following terminology with respect to bonds: a. Face Value b. Principal c. Maturity Value d. Market Value e. Coupon Interest Rate f. […]

Chapter 12 1 Managers Frequently Cite Which The Following

Chapter 12: Liabilities: Off-Balance Sheet Financing, Retirement Benefits, and Income Taxes Key 1. Many off-balance-sheet financings fall into one of two categories that accounting typically does not recognize as liabilities: executory contracts and contingent obligations. 2. U.S. GAAP and IFRS […]

Chapter 12 2 Its First Year Operations Lear Company

92. In its first year of operations, Lear Company reported financial statement income (prior to income tax expense) of $100,000. In the same year, Lear Company reported $80,000 of taxable income, the difference being due to temporary differences. Assuming the […]

Chapter 12 3 Baltimore Corporation Purchases New Machine For

110. Baltimore Corporation purchases a new machine for $50,000 on January 1, 2008. The machine has a four-year estimated service life and an estimated salvage value of zero. After paying the cost of running and maintaining the machine, the firm […]

Chapter 13 1 marketable securities must be readily convertible into

Chapter 13: Marketable Securities and Derivatives Key 1. The future value of held-to-maturity debt securities reflects the economic opportunity cost of continuing to hold the securities. 2. Acquisition and disposition of trading securities are usually financing activities. FALSE 3. U.S. […]

Chapter 13 2 which of the following is/are elements of a derivative

77. U.S. GAAP classifies securities that are neither debt securities held to maturity or trading securities as 78. A financial instrument that obtains its value from some other financial item is known as a(n) A. clone. B. mutual fund. C. […]

Chapter 13 3 Cummings Industries Places Firm Order For

129. Cummings Industries places a firm order for the equipment on June 30, 2013. It simultaneously signs a forward currency contract for £20,000. The forward rate on June 30, 2013, for settlement on June 30, 2014, is $1.64 per £1. […]

Chapter 14 1 The Combined Market Value Trading Securities

Chapter 14: Intercorporate Investments in Common Stock Key 1. The accounting for investments in common stock depends on (1) the expected holding period, and (2) the purpose of the investment, as determined by both the percentage held and management intent. […]

Chapter 14 2 Consolidated Financial Statements Are Typically Prepared

75. Consolidated financial statements are typically prepared when one company has 76. Marley Company had the following portfolio of securities at the end of its first year of operations: Year-End Security Classification Cost Market Value A Trading $18,000 $23,000 B […]

Chapter 14 3 Parent Computer Corporation Acquired Significant Influence

91. Parent Computer Corporation acquired significant influence over Child Computer Company on January 2 by purchasing 20 percent of its outstanding stock for $100 million. Parent attributes the entire excess of cost over book value acquired to a patent, which […]

Chapter 15 1 Lakeside Company Has Not Declared Nor

Chapter 15: Shareholders’ Equity: Capital Contributions and Distributions Key 1. Shareholders’ equity is a residual interest. It represents the shareholders’ claim on the assets of a firm after the firm satisfies all higher-priority claims. 2. All corporations must issue preferred […]

Chapter 15 2 the major segments of the statement of retained earnings

99. A stock split that is accomplished by a change in par value that is not proportional to the new number of shares or if the firm does not change the par value, the firm 100. Which of the following […]

Chapter 15 3 Prepare Journal Entries For The Following

170. Based on the following summary of shareholders’ equity accounts, answer the following questions. No dividends were paid during the Year 1 and Year 2. December 31, Year 1 December 31, Year 2 Common stock, $5 par value $1,000,000 $1,250,000 […]

Chapter 15 4 For Example The Board Directors Might Think

188. Discuss the various laws and contracts that govern the rights and obligations of a shareholder. 189. Discuss callable preferred shares from the issuer’s point-of-view. Call Provisions Callable preferred shares provide the issuer with the right (that is, the option)—but […]

Chapter 16 1 Choose The Combination Below That Best

Chapter 16: Statement of Cash Flows: Another Look Key 1. Most, but not all, firms report cash flows from operations using the indirect method. 2. Revenues from sales of goods or services to customers during a period equal cash received […]

Chapter 16 2 Avoid Understating The Amount Cash Flow

89. The effect of patent amortization on cash flow is conceptually identical to that of 90. To avoid understating the amount of cash flow from operations, the accountant A. subtracts the loss from net income. B. adds back the loss […]

Chapter 16 3 Other Comprehensive income These Changes Have Effect Any

Suppleme ntal Informati on For Fiscal Year Ended May 31, Year 4 (a) Land costing $11,000 was sold for $14.500, resulting in a $3,500 gain. (b) During the year, a fire completely destroyed a building with an original cost of […]

Chapter 17 1 Recent Changes The Financial Reporting Environment

Chapter 17: Synthesis and Extensions Key 1. The current FASB’s financial reporting objectives identify current and potential investors and creditors as the principal users of financial reports. 2. Authoritative guidance classifies gains and losses from the remeasurement of certain assets […]

Chapter 17 2 Firms Must Designate Each Derivative Hedging

99. Firms account for leases using either the operating lease method or the capital (finance) lease method. Which of the following is not true? 100. Firms account for leases using either the operating lease method or the capital (finance) lease […]

Chapter 17 3 set forth qualitative characteristics of financial reporting

169. The FASB and the IASB are reconsidering the role of uncertainty, or probability, in the definition, recognition, and measurement of liabilities. Existing recognition criteria include a probable future sacrifice of resources; one issue involves the minimum probability level to […]

Chapter 17 4 Explain The Accounting For Income Taxes

215. Discuss the definition, recognition, and measurement of liabilities. Liability The FASB’s conceptual framework defines a liability as a probable future sacrifice of economic resources arising from present obligations of a particular entity to transfer assets or provide services to […]

Chapter 17 5 The Denominator Roa Firmwide Level The Average

232. Explain the accounting for marketable securities. MARKETABLE SECURITIES Firms sometimes acquire bonds or capital stock of other entities for their expected returns (through interest, dividends, and price appreciation) without any intent to exert influence or control over the other […]

Chapter 2 1 Maintain The Balance Sheet Equality Necessary

Chapter 2: The Basics of Record Keeping and Financial Statement Preparation: Balance Sheet Key 1. The T-account looks like the letter T, with a horizontal line bisected by a vertical line. Increases in shareholders’ equity appear on the right side, […]

Chapter 2 2 European Countries Terminology Financial Statements Sometimes

89. Supplies and More, a firm specializing in building materials, engaged in the following four transactions during 2014: (1) purchased and received inventory costing $18,600 million, of which $12,000 million was on account with the rest paid in cash; (2) […]

Chapter 3 1 Record The Purchase Equipment That Fully

Chapter 3: The Basics of Record Keeping and Financial Statement Preparation: Income Statement Key 1. The last step in the accounting record-keeping process is preparing the balance sheet from amounts in the balance sheet accounts. 2. Current accounting practice takes […]

Chapter 3 2 The Intermingling Performance One Period With

106. The intermingling of performance of one period with that of preceding or succeeding periods is characteristic of which basis of accounting? Cash basis Accrual basis 107. The net income for a period and the financial position at the end […]

Chapter 3 3 Assume That Firm Uses The Accrual

120. Entries for the following items were either omitted or recorded incorrectly in preparing the financial statements for Year 3. Indicate the amount and nature [understatement (U), overstatement (O), no effect (N)] of the effect of the omission on total […]

Chapter 4 1 What Probable Future Economic Benefit That

Chapter 4: Balance Sheet: Presenting and Analyzing Resources and Financing Key 1. Accounting does not normally recognize mutually unexecuted contracts as assets or liabilities. 2. Acquisition cost includes all costs required to prepare an asset for its intended use. TRUE […]

Chapter 4 2 For Each The Following Items Indicate

100. For each of the following items, indicate whether the item meets all of the criteria in the definition of a liability [Yes or No]. If so, how does the firm value it? If not, why not? a.. Bonds payable. […]

Chapter 5 1 The Firm Recognizes Expense When The

Chapter 5: Income Statement: Reporting Results of Operating Activities Key 1. Revenues measure the inflow of net assets from operating activities. 2. Expenses provide future benefits, and assets measure the consumption of those benefits. FALSE 3. Expenditures on advertising and […]

Chapter 5 2 which of the following is/are not a component of

89. Comprehensive income as defined by the FASB 90. All of the following is/are components of comprehensive income except A. foreign currency translation adjustment. B. unrealized gains and losses on trading securities. C. deferred gains and losses on derivative financial […]

Chapter 6 1 Many Countries Around The World Require

Chapter 6: Statement of Cash Flows Key 1. A profitable firm can never run out of cash. 2. Using the accrual basis of accounting to measure net income creates the need for a separate financial statement that reports the impact […]

Chapter 6 2 While The Indirect Method Prevalent The

97. While the indirect method is prevalent in the construction of cash flow statements in the U.S., why might a firm choose to construct its cash flow statement using the direct method? 98. U.S. GAAP A. permits firms to report […]

Chapter 6 3 Different Points Their Existence Companies Will

130. Below is an Income Statement and a Statement of Cash Flows for Morgan Corporation for Year 8. Morgan Corporation Income Statement For the Year Ended December 31, Year 8 Sales Revenue $11,400 Gain on Sale of Equipment 60 Interest […]

Chapter 7 1 Practical Matter Most Firms Report Segment

Chapter 7: Introduction to Financial Statement Analysis Key 1. Financial statement ratios alone provide direct indicators of good or poor management. 2. The return from investing in the shares of common stock has two components: cash dividends and the change […]

Chapter 7 2 Selected Data From Carson Corporations Financial

99. Selected data from Carson Corporation’s financial statements for the year ended December 31, Year 2 are as follows. Current ratio 1.4 Quick ratio 0.86 Current liabilities $450,000 Accounts receivable turnover 6.0 Merchandise inventory turnover 4.0 Rate of return on […]

Chapter 7 3 The Financial Statements The Poston Company

140. Use the following comparative balance sheet to compute ratios as requested. Buff Company COMPARATIVE BALANCE SHEET As of December 31, Year 1 and Year 2 Assets Year 2 Year 1 Current assets Cash $10,000 $ 5,000 Accounts receivable 6,000 […]

Chapter 7 4 Describe The Relationship Between Return Assets

153. Describe the relationship between return on assets and return on common shareholders’ equity. RELATION BETWEEN RETURN ON ASSETS AND RETURN ON COMMON SHAREHOLDERS’ EQUITY For profitable firms, it is common for ROCE to exceed ROA. ROA measures the profitability […]

Chapter 8 1 The Firm Has Received Promise Payment

Chapter 8: Revenue Recognition, Receivables, and Advances from Customers Key 1. If the firm has received a promise of payment but cannot measure this promise with reasonable reliability, and U.S. GAAP would permit revenue to be recognized, but IFRS would […]

Chapter 8 2 Recognizing Revenue Before The Seller Collects

75. Recognizing revenue before the seller collects cash requires estimating the amount of uncollectible accounts with reasonable accuracy. Both U.S. GAAP and IFRS require the 76. Allowance for Uncollectibles contra account appears among the _____ on a firm’s balance sheet […]

Chapter 8 3 Prepare Entries Record The Following Transactions

126. Prepare entries to record the following transactions using the direct write-off method for uncollectibles. a. The firm assumes that approximately 1% of total sales on account will prove uncollectible. Sales for Year 1 are $1,000,000. All sales are on […]

Chapter 9 1 Many Firms Provide Similar Types Airline

Chapter 9: Working Capital Key 1. The current–noncurrent distinction refers to whether a firm will convert an asset to cash, or consume it, or sell it within one operating cycle and whether a firm will pay or otherwise settle a […]

Chapter 9 2 Which The Following Not Generally Accepted

99. Winner Company Winner Company’s beginning and ending inventories for the fiscal year ended September 30, Year 5, are October 1, Year 4 September 30, Year 5 Raw materials $15,000 $22,000 Work-in-process 40,000 35,000 Finished goods 8,000 12,000 Production data […]

Chapter 9 3 Terrace Inc Uses The Periodic Lifo

149. The following data relates to Rose Industries during Year 8. January 1, Year 8 December 31, Year 8 Raw Materials Inventory $ 47,570 $ 58,640 Work-in-Process Inventory 128,910 117,390 Finished Goods Inventory 36,250 47,220 It incurred factory costs for […]

Chapter 9 4 Describe The Similarities And Differences Between

163. Discuss inventory accounting concepts and issues. INVENTORY Inventory refers to goods and other items that a firm owns and holds for sale or for further processing as part of its operations. Inventory is also called “stock” in some countries; […]