Archives

Accounting Appendix F The Capital account balances would remain

1 12,000 8,000 12 ÷20= 8 ÷20= ×= ×= 0.60 0.40 $5,000 $5,000 Division of income: $2,000 40% 8,000 $20,000 Kim $3,000 Kim Bob Bob Kim Distributed $5,000 ( × ) $1,200 ( × ) $ 800 ( 2,000) $3,000 […]

Accounting Chapter 1 A major function of management is to provide

Chapter 01 – Uses of Accounting Information and the Financial Statements TRUE/FALSE 1. The processing stage of accounting is accomplished by the recording of data. 2. Two major goals of business are to achieve profitability and to achieve liquidity. ANS: […]

Accounting Chapter 1 Palm Textile Corporation had the following balance sheet

c. decrease by $16,000. d. increase by $42,000. 52. Palm Textile Corporation had the following balance sheet accounts and balances: Accounts Payable $12,000 Common Stock ? Accounts Receivable 2,000 Equipment $14,000 Building ? Land 14,000 Cash 6,000 Retained Earnings 4,000 […]

Accounting Chapter 1 Salaries Wages And Other Costs Associated With

2. User Insight: Form of business discussed Chapter 1, P 4. (Continued) 20 © 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part. The corporation […]

Accounting Chapter 1 Income Statement For the Year Ended December

1. 4. 2. 5. 3. b c b a a 1. 4. 2. 5. 3. 6. a c b c a c 1. 2. 3. Assets Liabilities $120,000 $ 72,000 $100,000 Stockholders’ Equity = = = 1. + + = […]

Accounting Chapter 10 Feb Bond Interest Expense Unamortized Bond Discount

a. ×= b. c. Depreciation Expense—Capital Lease Building 14,322 Accumulated Depreciation—Capital Lease Building 14,322 ÷12 = years $171,864 $14,322 Recorded depreciation on leased building for first year d. 15,468 8,532 24,000 ×= 14,700 9,300 24,000 ( – ) × 0.09 […]

Accounting Chapter 10 Income Taxes Expense Appears The Income Statement

1. a. b. c. d. e. f. g. 6 5 3 2 1 Reduction in Debt $200 ** 201 ** 203 ÷12 = 149,599 149,3963 2 1 149,800$1,000 0.006667 Rounded * 997 999 ** 8% 1,200 $1,200 1,200 Unpaid Balance […]

Accounting Chapter 10 The Accounting Year Ends December 31 Prepare

b. A long-term debt secured by real property. c. Bonds that are issued in the name of the bondholder. d. The method of bond amortization that uses a constant interest rate each period to amortize the bond premium or discount. […]

Accounting Chapter 10 The debt to equity ratio is expressed as a percent

Chapter 10 – Long-Term Liabilities TRUE/FALSE 1. Financial leverage is also known as trading on the debt. 2. The debt to equity ratio is a measure of financial leverage. ANS: T PTS: 1 DIF: Easy OBJ: 1 NAT: AACSB Analytic […]

Accounting Chapter 10 This Feature Gives Management Flexibility Managing Its

5. User Insight: Strategy of calling bonds when stock price has risen Chapter 10, P 7. (Continued) rather than accepting the call price. Since the price of the company’s stock has The company can improve its debt to equity ratio […]

Accounting Chapter 10 When bonds have been issued at a premium

d. Interest expense remains constant in amount for each interest period. 49. When the effective interest method of amortization is used for a bond premium, the amount of interest expense for an interest period is calculated by multiplying the a. […]

Accounting Chapter 11 can be paid on common stock until all

2. Use the following information to obtain the ratios requested below. Where necessary, carry answers to one decimal place. Dividends per share: $.76 Market price per share: $40 Net income: $64,000 Stockholders’ equity, beginning of year: $500,000 Stockholders’ equity, end […]

Accounting Chapter 11 Return Equity Return Assets Debt Equity Current

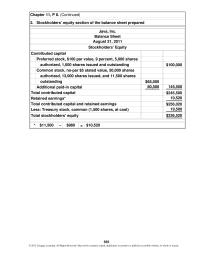

$100,000 *–= $11,500 $980 $10,520 Chapter 11, P 8. (Continued) Contributed capital Preferred stock, $100 par value, 9 percent, 5,000 shares Stockholders’ equity section of the balance sheet prepared Total stockholders’ equity 2. Stockholders’ Equity Java, Inc. Balance Sheet August […]

Accounting Chapter 11 The dividends yield is measured in terms of

Chapter 11 – Stockholders’ Equity TRUE/FALSE 1. The price/earnings (P/E) ratio is a common measure of management’s performance. 2. The dividends yield is measured in terms of “times.” ANS: F PTS: 1 DIF: Easy OBJ: 1 NAT: AACSB Analytic | […]

Accounting Chapter 11 The total amounts payable to preferred stockholders

53. Chambers Corporation had the following shares of stock outstanding on December 31, 2013: Common stock, $100 par value, 100,000 shares outstanding Preferred stock, 8 percent, $200 par value, cumulative, 10,000 shares outstanding Dividends were in arrears for 2011 and […]

Accounting Chapter 11 Total start-up and organization costs

1. 4. 2. 5. 3. 6. Disadvantage Advantage Disadvantage Advantage 28,000 28,000 28,000 28,000 Payment of dividends 6/1 6/15 outstanding × $0.20 per share Dividends Payable No entry necessary on record date Cash $40,000 24,000 $64,000 ($64,000) ($24,000) 24,000 16,000 […]

Accounting Chapter 11 User Insight Investors Return Discussed Stas Corporations

( 400 × ) + Chapter 11, E 19. $2,400 Preferred Stock Book Value per Share =$105 400 Shares * 538 © 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible […]

Accounting Chapter 11 where necessary, carry answers to one decimal

112. Winston Corporation has retained earnings of $400,000. It has 5,000 shares of 6 percent, $200 par value preferred stock outstanding that is callable at 102. The preferred stock is cumulative, and one year of dividends is in arrears. It […]

Accounting Chapter 12 A yield of less than 1 signals potential problems

1. b 4. (+) ÷2 ––+ $20,000 = Free Cash Flow = $90,000= $20,000 Net Cash Flows from Operating Activities – Dividends – $60,000 $10,000 Purchases of Plant Assets + Sales of Plant Assets 22.8% Net Cash Flows from Operating […]

Accounting Chapter 12 Cash equivalents include money market accounts

Chapter 12 – The Statement of Cash Flows TRUE/FALSE 1. The statement of cash flows discloses the effect on cash of the purchase and sale of long-term investments and not of short-term investments. 2. It is unethical, and considered a […]

Accounting Chapter 12 Ebit da Earnings Before Interest Taxes Depreciation And

3,000 ( 47,500) ( 2,500) ( 50,500) ($26,500) ($29,000) 37,500 8,500 $60,000 ( 45,000) ( 10,000) 15,000 Repayment of mortgage Cash flows from financing activities Purchase of investments Issue of bonds Repayment of notes payable Issue of notes payable Cash […]

Accounting Chapter 12 Laguna’s Corporation sold investments for

MSC: ACBSP-APC-24-Statement of Cash Flows 54. Assume the indirect method is used to compute net cash flows from operating activities. For this item extracted from the financial statements—Interest Income (assume that cash received is equal to amount reported)—indicate the effect […]

Accounting Chapter 12 Malzone Enterprises is preparing a statement of cash

11. A company sells equipment with a carrying value of $10,000 for $7,000. Where, and for what amounts, would this transaction appear on a statement of cash flows using the indirect method? ANS: First, the loss on sale of $3,000 […]

Accounting Chapter 13 Information from prior years could be used to

+$0 + $0 ++ ++ + + ++ + + $552,800 = 2.8 Times $1,520,400 $629,800 $54,400 e. Payables turnover Chapter 13, P 5. (Continued) Ratio Name Roma Lima 6. Company with More Favorable Ratio $6,142,000 $14,834,000 $80,000 $203,400 + […]

Accounting Chapter 13 It is in the best interests of a company to

Chapter 13 – Financial Performance Measurement TRUE/FALSE 1. It is in the best interests of a company to base executive compensation on a single performance measure. 2. Per the Sarbanes-Oxley Act of 2002, a compensation committee, comprised of a public […]

Accounting Chapter 13 She has asked her administrative assistant

16. The following information pertains to Bailey Corporation: Profit margin for 2013 10.0% Total assets, 12/31/12 $430,000 Total assets, 12/31/13 $470,000 Net income, 2013 $ 30,000 Calculate the return on assets for 2013. Round your answer to two decimal places. […]

Accounting Chapter 13 The division that was sold was operating at a profit

that in its restructuring, the company sold off profitable operations rather than im- Chapter 13, C 2. (Continued) 2. User Insight: Restructuring plan assessed Dash Corporation’s operations have not improved, although the contrary might be inferred from the year’s change […]

Accounting Chapter 13 The Following Selected Amounts Were Extracted

Accrued expenses and other current liabilities 836 696 Income taxes payable 107 224 Total current liabilities $2,838 $2,491 Long-term debt $1,230 $1,222 Deferred income taxes 362 333 Other liabilities 243 229 Total liabilities $4,673 $4,275 Common stock $ 30 $ […]

Accounting Chapter 13 The length of the operating cycle equals the days’

a. Return on equity b. Return on assets c. Asset turnover d. Quick ratio 57. Free cash flow is measured in terms of a. a percentage. b. dollars. c. days. d. times. ANS: B PTS: 1 DIF: Easy OBJ: 4 […]

Accounting Chapter 13 Unless Two Successive Base Years Have Exactly

1. 1. 2. 3. 4. 5. d b c a 1. 2. 3. 4. 5. 6. 7. c b; increase in percentage is more conservative. c b; 10-year useful life is more conservative. a; accelerated method is more conservative. c […]

Accounting Chapter 13 an investor in Matthews Company obtains more

*–* Mayer Company. However, in other respects, Mayer Company is more acceptable. obtains more underlying earnings per dollar invested compared to an investor in dividends yield for Mayer Company (10.0 percent) is better than that for Matthews For example, even […]

Accounting Chapter 14 A non influential and noncontrolling investment

Chapter 14 – Investments TRUE/FALSE 1. Gains and losses on the sale of investments appear as adjustments within the financing activities section of the statement of cash flows. 2. Another term for short-term investments is marketable securities. ANS: T PTS: […]

Accounting Chapter 14 Allowance Adjust Short term Investments Market Unrealized Gain

Chapter 14, P 3. (Continued) 2. User Insight: Goodwill accounts discussed The Goodwill account would indicate that Arrak Company paid more than fair value for Bivak Company. On the balance sheet, goodwill appears as an asset. 697 © 2012 Cengage […]

Accounting Chapter 14 Market account appears on the balance sheet

2011 Dec. 31 85,000 2012 Mar. 23 95,000 5,000 100,000 2011 Dec. 31 70,000 70,000 $640,000 – $570,000 = $70,000 to market Unrealized Gain on Long-Term Investments To record increase in investment portfolio Short-Term Investments less than cost To record […]

Accounting Chapter 14 Received a cash dividend from Upshur Corporation

c. Dividend Income 900 Cash 900 d. Cash 900 Investment in Upshur Corporation 900 36. Use this information to answer the following question. These facts concern the long-term stock investments of Webster Corporation: June 1, 2012 Paid cash for the […]

Accounting Chapter 14 Tally Corporation the Market Value The Tally Corporation

Investment in Coll Company 130,000 — Plant and equipment 240,000 135,000 Total assets 430,000 165,000 Liabilities 180,000 35,000 Common stock 150,000 90,000 Retained earnings 100,000 40,000 Total liabilities and stockholders’ equity 430,000 165,000 16. Ming Company purchased 100 percent of […]

Accounting Chapter 2 Continued Ledger Accounts Set Amounts From

2 14,400 14,400 Issued 14,400 shares of $1 par value common stock 5,800 Purchased shed to store bicycles for cash 8 800 800 Paid for shed installation 9 10 150 150 Paid for cleanup 13 1,940 1,940 Recorded rentals made […]

Accounting Chapter 2 Others May Insist That The Action Fell

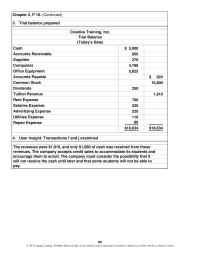

$ 5,000 850 270 4,799 5,825 $18,634 $18,634 encourage them to enroll. The company must consider the possibility that it pay. will not receive the cash until later and that some students will not be able to The revenues were […]

Accounting Chapter 2 Purchase requisitions are recognized in the accounting

Chapter 02 – Analyzing Business Transactions TRUE/FALSE 1. When a company receives a product previously ordered, a recordable transaction has occurred. 2. When a business pays a new employee for the first time, a recordable transaction has occurred. ANS: T […]

Accounting Chapter 2 Solutions Analyzing Business Transactions Jan

10 1. 5. 2. 6. 3. 7. 4. 8. Revenue None (Stockholders’ Equity) Liability Asset Asset Asset 1. 5. 2. 6. 3. 7. 4. 8. Debit Debit Debit Credit Credit Debit Chapter 2, SE 1. Jan. Do not recognize because […]

Accounting Chapter 2 The answer given here assumes the perpetual inventory

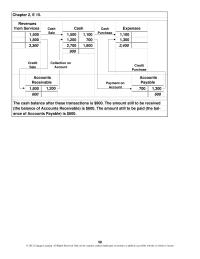

1,500 1,500 1,100 1,100 1,800 1,200 700 1,300 3,300 2,700 1,800 2,400 900 Revenues from Services Cash Expenses Chapter 2, E 15. Cash Sale Cash Purchase 58 © 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, […]

Accounting Chapter 2 Which of the following errors will not cause the debit

62. Which of the following errors will not cause the debit and credit columns of the trial balance to be unequal? a. A debit entry was recorded in the wrong account. b. A debit was entered in an account as […]

Accounting Chapter 2 Why is the Dividends account increased by a debit

PROBLEM 1. Explain why the dollar amount of total stockholders’ equity probably will not equal the dollar amount that would remain if all the assets were sold and all the liabilities were then settled. ANS: The valuation of assets on […]

Accounting Chapter 3 Accounting periods of greater than a year are

Chapter 03 – Measuring Business Income TRUE/FALSE 1. Accounting periods of greater than a year are called interim periods. 2. If a company is not expected to survive, it is considered a going concern. ANS: F PTS: 1 DIF: Easy […]

Accounting Chapter 3 Adjusting Entries Recorded The General Journal General

$ 13,786 2,780 11,000 19,387 15,000 60,865 33,630 1,750 8,200 894 720 600 2,780 $111,412 $111,412 Rent Expense Office Supplies Expense Depreciation Expense—Office Equipment Income Taxes Expense Interest Expense Utilities Expense Salaries Expense 141 Retained Earnings Dividends Income Taxes Payable […]

Accounting Chapter 3 All Current Assets Except Cash Can

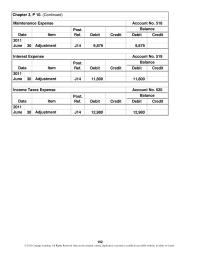

Ref. Debit Credit Debit Credit 30 J14 9,879 9,879 Ref. Debit Credit Debit Credit 30 J14 12,980 12,980 2011 Post. June Adjustment Date Item Balance Balance Chapter 3, P 10. (Continued) Post. Income Taxes Expense Account No. 520 Interest Expense […]

Accounting Chapter 3 Dividends Their Balances And Transferring Them Retained

Supplement to CHAPTER 3 CLOSING ENTRIES AND THE WORK SHEET Answers to Review Questions 1. No, the work sheet cannot be used as a substitute for the financial statements. It is a tool used in preparing financial statements. Work sheets […]

Accounting Chapter 3 Homework Accumulated Depreciation—Repair Equipment

Page 6 Post. Ref. Debit Credit 30 314 467 312 467 Date June General Journal Chapter 3S, P 2. (Continued) Description 2011 Income Summary Retained Earnings 178 © 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, […]

Accounting Chapter 3 Inc Income Statement For The Month Ended

1. 31 800 800 + – = $800 Dec. 31 920 920 + – = $920 Mar. 31 100 100 To record depreciation for the month Supplies Expense $380 To record supplies used during the year Accumulated Depreciation—Office Equipment $980 […]

Accounting Chapter 3 Payroll For The Five day Workweek Paid Friday

8. Prepare year-end adjusting entries for each of the following situations. a. The Office Supplies account showed a beginning debit balance of $600 and purchases of $1,000. The ending debit balance was $400. b. Depreciation on buildings is estimated to […]

Accounting Chapter 3 Use this information pertaining to the Essex

Cash $ 400 Accounts Receivable 1,000 Prepaid Insurance 100 Supplies 300 Office Equipment 800 Accumulated Depreciation–Office Equipment $ 400 Accounts Payable 600 Common Stock 1,200 Service Revenue Earned 1,000 Salaries Expense 200 Rent Expense 400 ______ $3,200 $3,200 If the […]

Accounting Chapter 3 What are the three things that must be done

KEY: Cash flow and current assets MSC: ACBSP-APC-09-Financial Statements 128. Unearned Revenue was $600 at the end of February and $750 at the end of March. Service Revenue was $4,200 for the month of March. How much cash was received […]

Accounting Chapter 3 Depreciation Expense Office Equipment Interest Expense

Bal. 660 (b) 305 Bal. 4,620 Bal. 355 (c) 263 Bal. 1,033 Bal. 2,970 Bal. 5,500 (f) 902 Bal. 1,485 Bal. 583 (d) 285 (e) 165 (h) 2,100 Bal. 6,000 Bal. 7,001 Bal. 11,000 Accounts Payable Income Taxes Payable Notes […]

Accounting Chapter 4 However The Return Assets Ratio More Comprehensive

1. 1. 2. 3. 4. 5. Cost-benefit Conservatism Materiality Consistency 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. Current liability Investment Current asset Current liability Not on the balance sheet Current asset Stockholders’ equity Intangible asset Chapter 4, […]

Accounting Chapter 4 Net Income Net Sales C Cash Flow

2011 2010 $262,966 100.0% $237,632 100.0% 117,474 44.7% 85,925 36.2% $145,492 55.3% $151,707 63.8% $ 33,213 12.6% $ 55,314 23.3% * $ 900 0.3% * $ 425 0.2% 1,800 0.7% * 850 0.4% $ 900 0.3% $ 425 0.2% * […]

Accounting Chapter 4 Only investors have an interest in a company’s

55. Use this information to answer the following question. Ramsey Company Income Statement For the Year Ended December 31, 2013 Revenues Net sales $200,000 Dividend income 17,500 Total revenues $217,500 Costs and expenses Costs of goods sold $ 58,000 Selling […]

Accounting Chapter 4 Profitability means having enough cash on hand to pay

Chapter 04 – Financial Reporting and Analysis TRUE/FALSE 1. Only investors have an interest in a company’s ability to generate favorable cash flows. 2. Investors and creditors use financial statements to evaluate a company’s ability to pay dividends and interest. […]

Accounting Chapter 4 The Higher Negative Profit Margin Supervalu Makes

1,840 $253,900 24,800 $ 11,700 $20,600 14,200 6,400 18,100 2,000 $298,800 Delivery equipment Trademark Total property, plant, and equipment Property, plant, and equipment Land Intangible assets Less accumulated depreciation Deposit for future advertising Total assets Investments Building, not in use […]

Accounting Chapter 4 Which of the following is expressed in terms

Current assets Current liabilities Investments Long-term liabilities Property, plant, and equipment Stockholders’ equity Intangible assets Not on balance sheet For each account name below, write the name of the category above to which it belongs. a. Accumulated Depreciation b. Revenues […]

Accounting Chapter 5 Centralization The Records Would Mean That

Chapter 5, P 8. (Continued) Second, the components of gross margin and operating expenses can be ex- When possible, an analysis would also include comparing the ratios above for Robert’s Shop, Inc., to prior years and to other companies of […]

Accounting Chapter 5 Compute the dollar amount of the items indicated

7. Given the following information, prepare in good form the cost of goods sold section of an income statement for 2013. Freight-In $ 16,000 Merchandise Inventory, December 31, 2012 60,000 Merchandise Inventory, December 31, 2013 64,000 Purchases 152,000 Purchases Returns […]

Accounting Chapter 5 Continued Against The Records Maintained The

17 500 500 18 100 100 18 60 60 24 1,600 1,600 $1,900 – $300 = $1,600 25 950 950 $1,050 – $100 = $950 Accounts Receivable Received payment on account from Tina Land s Cash Merchandise Inventory account Company […]

Accounting Chapter 5 Following is a classification scheme for

Chapter 05 – The Operating Cycle and Merchandising Operations TRUE/FALSE 1. Businesses can be classified as service companies, wholesalers, or retailers. 2. Profitability means having enough cash on hand to pay bills when they become due. ANS: F PTS: 1 […]

Accounting Chapter 5 Gross Margin Operating Expenses Selling Expenses General

1. = $ 5,000 + + + = $14,000 =– = $14,000 – = $7,500 Working Capital Current Assets $6,500 $14,000 = $6,500 Current Liabilities Current Liabilities Current Ratio Current Assets 2.15== 40 25 (33) 32 Less creditors’ payment terms […]

Accounting Chapter 5 Prepare journal entries without explanations for

6. Scuilli Corporation purchased $5,000 worth of merchandise, terms n/30, from the Zupcic Corporation on June 4. The cost of the merchandise to Zupcic was $3,600. On June 10, Scuilli returned $700 worth of goods to Zupcic for full credit. […]

Accounting Chapter 5 The amount of goods available for sale during

a. decrease to Sales. b. increase to Sales. c. decrease to Sales Returns and Allowances. d. increase to Sales Returns and Allowances. 36. Under the perpetual inventory system, the entry to record a purchase return would include a credit to […]

Accounting Chapter 6 A retail company has goods available for sale

44. Use this information to answer the following question. July 1 Inventory 15 units @ $8.00 8 Purchase 60 units @ $8.80 17 Purchase 30 units @ $8.40 25 Purchase 45 units @ $9.60 Total sales 100 units A periodic […]

Accounting Chapter 6 The cost of goods sold figures range from

( + ) ÷ 2 Times = $2,200,000 $560,000 365 = Days’ Inventory on Hand = 4.2 Times $2,200,000 $520,000 $480,000 = = Number of Days in a Year Inventory Turnover Days 86.9 =4.2 Days (+ 2 = $1,440,000 Days’ […]

Accounting Chapter 6 The higher the value assigned to ending inventory

Chapter 06 – Inventories TRUE/FALSE 1. Supply-chain management works well in a just–in-time operating environment. 2. The higher the value assigned to ending inventory, the lower the gross margin. ANS: F PTS: 1 DIF: Easy OBJ: 1 NAT: AACSB Analytic […]

Accounting Chapter 6 This Possible Because The Amount The Overstatement

1. Unit Units Price* Amount 50 $204.00 $10,200 60 $214.67 $12,880 Unit Units Price Amount May 2 100 $216 $21,600 May 14 50 224 11,200 May 22 60 234 14,040 210 46,840 270 221.19 $59,720 200 70 221.19 15,483 $44,237 […]

Accounting Chapter 6 An inventory management system in which goods

14. How does the perpetual inventory system differ from the periodic inventory system in the determination of cost of goods sold? ANS: Under the perpetual system, cost of goods sold is accumulated as sales are made. Under the periodic system, […]

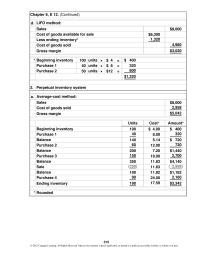

Accounting Chapter 6 Goods available for sale Ratio of cost

d. $8,000 $6,300 a. $8,000 2,958 $5,042 Units Cost* Amount* 100 $ 4.00 $ 400 40 8.00 320 140 5.14 $ 720 60 12.00 720 200 7.20 $1,440 150 18.00 2,700 350 11.83 $4,140 (250) 11.83 ( 2,958) 100 11.82 […]

Accounting Chapter 7 April Reported Accrued Interest Income April Date

Amount $25,873 $4,196 350 $4,546 Amount of adjustment Debit balance in allowance account length of history used when analyzing accounts receivable, credit policy, current economy, regional layoffs, and seasonal factors. uncollectible in each category. These percentages are multiplied by the […]

Accounting Chapter 7 The Entry that Would Made Record The Dishonor

57. The general ledger account for Accounts Receivable shows a debit balance of $50,000. Allowance for Uncollectible Accounts has a credit balance of $3,000. Net sales for the year were $500,000. In the past, 3 percent of sales have proved […]

Accounting Chapter 7 The Fee Will Higher Than The Factoring

Chapter 07 – Cash and Receivables TRUE/FALSE 1. Under discounting, a company sells its receivables in batches at a discount. 2. Purchasing receivables with recourse is riskier than purchasing them without recourse. ANS: F PTS: 1 DIF: Easy OBJ: 1 […]

Accounting Chapter 7 The Following Information Pertains The Bank Transactions

17. Determine the interest on the following notes payable: Round answers to two decimal places. a. $3,000 at 10 percent for 60 days b. $600 at 16 percent for 4 months c. $5,000 at 12 percent for 45 days d. […]

Accounting Chapter 7 To record estimated uncollectible accounts expense

1. ( + ) ÷ 2 Days Times b. = $90,000 $70,000 $720,000 $80,000 9.0= $720,000 Times = Days in a Year =365 = 40.6 9.0 Days’ Sales Uncollected Receivable Turnover = Days a. Receivable Turnover c (also could be […]

Accounting Chapter 8 Amount Service Revenue Determined Service Revenue For

= == ( + ) ÷ 2 = 8.0 $65,000 Cost of Goods Sold +/– Change in Merchandise Inventory $25,000 =$35,000 Payables Turnover $240,000 = $40,000 – = Average Accounts Payable $30,000 Times $25,000 $230,000 $10,000+ Chapter 8, SE 1. […]

Accounting Chapter 8 Each widget carries a warranty that provides for j

4. Anson’s Auto Parts had cash sales of $10,000 for the month of April. Sales are subject to a 6 1/2 percent sales tax and an 8 percent excise tax. In the journal provided, prepare a compound entry without explanation […]

Accounting Chapter 8 If 5 percent typically need to be replaced

d. credit to Payroll Taxes and Benefits Expense for $64. 41. Use this information to answer the following question. Baker Company has the following information for the pay period of January 1-15. Payment occurs on January 20. Gross payroll $16,000 […]

Accounting Chapter 8 If an accrued liability for salaries is not

Chapter 08 – Current Liabilities and Fair Value Accounting TRUE/FALSE 1. Working capital equals current assets minus current liabilities. 2. Payables turnover is measured in number of days. ANS: F PTS: 1 DIF: Easy OBJ: 1 NAT: AACSB Analytic | […]

Accounting Chapter 8 Most Students Will Acknowledge That The Estimated

$18,000.00 952.00 $39,436.20 necessary. In addition, Gundy may have to pay penalties and interest to the state or federal government because of the failure to remit the taxes payable on a timely basis. Inquiries should be made of the proper […]

Accounting Chapter 9 Cash was ex-pended as an investing activity when the

Carrying Value a. ÷ 4 $70,000 2,400 12,000 3,600 12,000 4,800 12,000 1,200 12,000 50,000 × 80,000 2 3 18,000 10,000 80,000 × 4 × 8,000 32,000 80,000 24,000 c. × 50% $45,000 × 50% 22,500 × 50% 11,250 –$10,000 […]

Accounting Chapter 9 For Movable Assets Use The Straightline Method

14. On November 1, 2011, Rob’s Auto Repair purchased diagnostic equipment for $18,000. The equipment had an estimated residual value of $3,000 and a five-year life and was sold on May 1, 2013. Assuming that the company depreciates the asset […]

Accounting Chapter 9 If cash received for the asset equals its carrying

1. 4. =+ This amount of free cash flow is the amount of cash that Sun Corporation has avail- able for other purposes, such as expansion or investment, after it deducts the funds it has committed to continue operations at […]

Accounting Chapter 9 Land held for speculative purposes should be classified

Chapter 09 – Long Term Assets TRUE/FALSE 1. Asset impairment occurs when the fair value of a long-term asset falls below its carrying value. 2. Fair value is the amount for which an asset could be bought or sold in […]

Accounting Chapter 9 Overton Corporation purchased a truck for

12. Overton Corporation purchased a truck for $80,000. The company expected the truck to last four years or 100,000 miles, with an estimated residual value of $8,000 at the end of that time. During the second year, the truck was […]

Accounting Chapter 9 what is the asset’s carrying value after three

b. down as one goes from left to right. c. down and then up as one goes from left to right. d. up and down in a zig-zag as one goes from left to right. 49. Accelerated depreciation assumes all […]

Accounting Supplement F Both Us Gaap And Ifrs Recognize Accrual

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part. INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS): AN OVERVIEW—Solutions Discussion Questions 1. Convergence is a process through […]

Accounting Supplement F Summary Wages Expense Rent Expense Supplies

Account Name Trial Balance Adjustments Adjusted Income Statement Balance Sheet Trial Balance Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit Cash 120 Accounts Receivable 80 Prepaid Insurance 48 Supplies 40 Equipment 160 Accumulated Depreciation–Equipment 24 Accounts Payable 48 […]

Accounting Supplement F When the Income Statement columns of the work

Chapter 03 – Supplement – Closing Entries and the Work Sheet TRUE/FALSE 1. The first step to preparing closing journal entries is to close the credit balance on the income statement to the Retained Earnings account. 2. The final step […]