Archives

978-0133427530 Chapter 1 Part 1

Chapter 1 The Financial Statements Short Exercises (5 min.) S 1-1 Computed amounts in boxes Total Assets = Total Liabilities + Stockholders’ Equity a. $660,000 = $320,000 + $340,000 b. 135,000 = 57,000 + 78,000 c. 401,000 = 45,000 + […]

978-0133427530 Chapter 1 Part 2

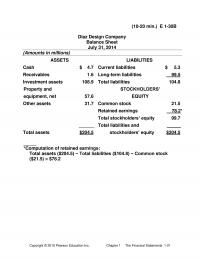

(10-20 min.) E 1-30B Diaz Design Company Balance Sheet July 31, 2014 (Amounts in millions) ASSETS LIABILITIES Cash $ 4.7 Current liabilities $ 5.3 Receivables 1.6 Long-term liabilities 99.5 Investment assets 108.9 Total liabilities 104.8 Property and equipment, net 57.6 […]

978-0133427530 Chapter 1 Part 3

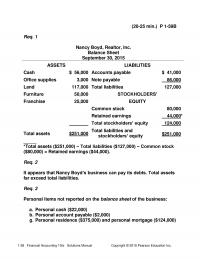

(20-25 min.) P 1-59B Req. 1 Nancy Boyd, Realtor, Inc. Balance Sheet September 30, 2015 ASSETS LIABILITIES Cash $ 56,000 Accounts payable $ 41,000 Office supplies 3,000 Note payable 86,000 Land 117,000 Total liabilities 127,000 Furniture 50,000 STOCKHOLDERS’ Franchise 25,000 […]

978-0133427530 Chapter 10 Part 1

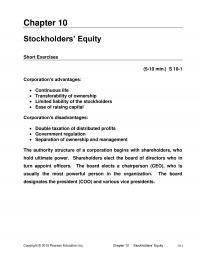

Chapter 10 Stockholders’ Equity Short Exercises (5–10 min.) S 10-1 Corporation’s advantages: • Continuous life • Transferability of ownership • Limited liability of the stockholders • Ease of raising capital Corporation’s disadvantages: • Double taxation of distributed profits • Government […]

978-0133427530 Chapter 10 Part 2

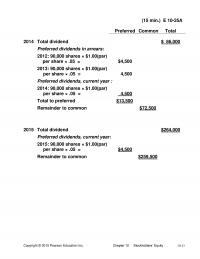

(15 min.) E 10-25A Preferred Common Total 2014 Total dividend $ 86,000 Preferred dividends in arrears: 2012: 90,000 shares × $1.00(par) per share × .05 = $4,500 2013: 90,000 shares × $1.00(par) per share × .05 = 4,500 Preferred dividends, […]

978-0133427530 Chapter 10 Part 3

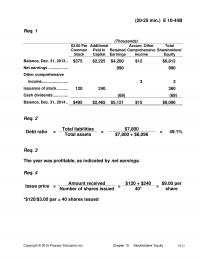

(20-25 min.) E 10-44B Req. 1 (Thousands) $3.00 Par Common Stock Additional Paid In Capital Retained Earnings Accum. Other Comprehensive Income Total Shareholders’ Equity Balance, Dec. 31, 2013 .. $375 $2,225 $4,200 $12 $6,812 Net earnings ……………… 990 990 Other […]

978-0133427530 Chapter 10 Part 4

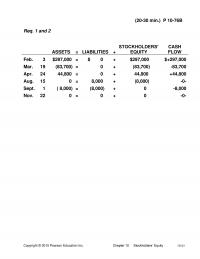

(20-30 min.) P 10-76B Req. 1 and 2 ASSETS = LIABILITIES + STOCKHOLDERS’ EQUITY CASH FLOW Feb. 3 $297,000 = $ 0 + $297,000 $+297,000 Mar. 19 (83,700) = 0 + (83,700) -83,700 Apr. 24 44,800 = 0 + 44,800 […]

978-0133427530 Chapter 10 Part 5

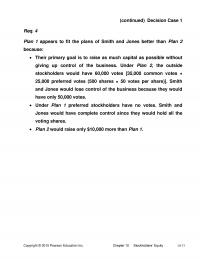

(continued) Decision Case 1 Req. 4 Plan 1 appears to fit the plans of Smith and Jones better than Plan 2 because: • Their primary goal is to raise as much capital as possible without giving up control of the […]

978-0133427530 Chapter 11 Part 1

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income 11-1 Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement & the Statement of Comprehensive Income Short Exercises (5-10 min.) S 11-1 There are several […]

978-0133427530 Chapter 11 Part 2

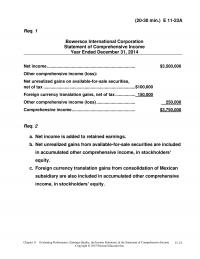

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income 11–21 (20-30 min.) E 11-23A Req. 1 Bowersox International Corporation Statement of Comprehensive Income Year Ended December 31, 2014 Net income ………………………………………………………………… $3,500,000 Other comprehensive […]

978-0133427530 Chapter 11 Part 3

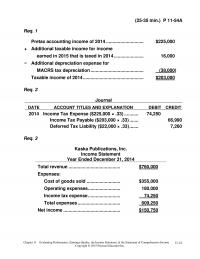

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income 11–41 (25-35 min.) P 11-54A Req. 1 Pretax accounting income of 2014 ……………………….. $225,000 + Additional taxable income for income earned in 2015 that is […]

978-0133427530 Chapter 11 Part 4

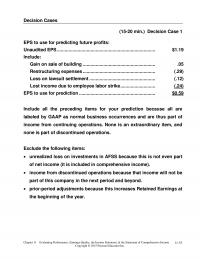

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income 11–53 Decision Cases (15-20 min.) Decision Case 1 EPS to use for predicting future profits: Unaudited EPS …………………………………………………………………. $1.19 Include: Gain on sale of building […]

978-0133427530 Chapter 12 Part 1

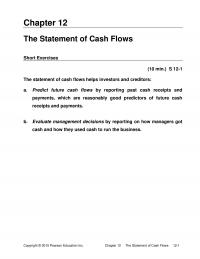

Chapter 12 The Statement of Cash Flows Short Exercises (10 min.) S 12-1 The statement of cash flows helps investors and creditors: a. Predict future cash flows by reporting past cash receipts and payments, which are reasonably good predictors of […]

978-0133427530 Chapter 12 Part 2

(continued) E 12-20A Req. 2 Tullis’ cash flows look strong. Operations are the main source of cash. The company is investing in new plant assets without having to borrow. It was able to issue stock and pay off a long-term […]

978-0133427530 Chapter 12 Part 3

Problems (40 min.) P 12-58A Req. 1 Fairfax Fine Automobiles, Inc. Income Statement Year Ended December 31, 2014 Sales revenue …………………………………………………………….. $497,000 Cost of goods sold [$136,000 + (3 × $45,000)] ………………. 271,000 Salary expense …………………………………………………………… 102,000 Depreciation expense ($150,000 […]

978-0133427530 Chapter 12 Part 4

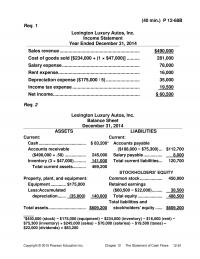

(40 min.) P 12-68B Req. 1 Lexington Luxury Autos, Inc. Income Statement Year Ended December 31, 2014 Sales revenue …………………………………………………….. $490,000 Cost of goods sold [$234,000 + (1 × $47,000)] ………. 281,000 Salary expense …………………………………………………… 78,000 Rent expense ……………………………………………………… 16,000 […]

978-0133427530 Chapter 12 Part 5

Challenge Exercises and Problem (20-30 min.) E 12-76 (All amounts in thousands) Decrease in Sales + Accounts Receivable a. Collections = $25,133 = $25,118 + ($612 − $597) Cost Increase in Increase in − Accounts b. Payments for of sales […]

978-0133427530 Chapter 13 Part 1

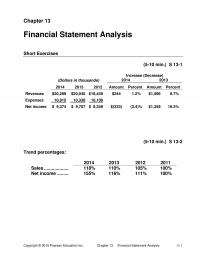

Chapter 13 Financial Statement Analysis Short Exercises (5-10 min.) S 13-1 Increase (Decrease) (Dollars in thousands) 2014 2013 2014 2013 2012 Amount Percent Amount Percent Revenues $20,289 $20,045 $18,449 $244 1.2% $1,596 8.7% Expenses 10,915 10,338 10,100 Net income $ […]

978-0133427530 Chapter 13 Part 2

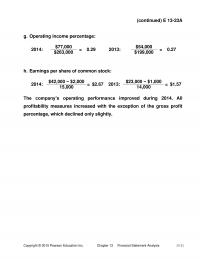

(continued) E 13-23A g. Operating income percentage: 2014: $77,000 = 0.29 2013: $54,000 = 0.27 $263,000 $199,000 h. Earnings per share of common stock: 2014: $42,000 − $2,000 = $2.67 2013: $23,000 − $1,000 = $1.57 15,000 14,000 The company’s […]

978-0133427530 Chapter 13 Part 3

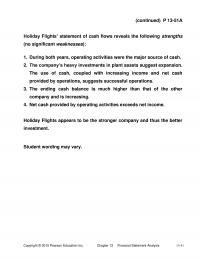

(continued) P 13-51A Holiday Flights’ statement of cash flows reveals the following strengths (no significant weaknesses): 1. During both years, operating activities were the major source of cash. 2. The company’s heavy investments in plant assets suggest expansion. The use […]

978-0133427530 Chapter 13 Part 4

Copyright © 2015 Pearson Education Inc. Chapter 13 Financial Statement Analysis 13–61 (20-30 min.) E 13-62 ORDER OF COMPUTATION Millions 5 Sales ($1,700 ÷ 0.25) ………………………………………… $6,800 6 Operating expenses ($6,800 − $1,700) ………………. 5,100 4 Operating income ……………………………………………. 1,700 […]

978-0133427530 Chapter 13 Part 4

(20-30 min.) E 13-62 ORDER OF COMPUTATION Millions 5 Sales ($1,700 ÷ 0.25) ………………………………………… $6,800 6 Operating expenses ($6,800 − $1,700) ………………. 5,100 4 Operating income ……………………………………………. 1,700 Given Interest expense ……………………………………………… 800 2 Pretax income [$540 ÷ (1 − […]

978-0133427530 Chapter 13 Part 5

(continued) Amazon.com 6. Evaluating stock as an investment Student opinions and answers based on the market price of the stock will vary. The following statistics will bolster their positions. Ratio Computation 2012 2011 Interpretation Price Market price $251* $173** earnings […]

978-0133427530 Chapter 2 Part 1

Chapter 2 Transaction Analysis Short Exercises (5 min.) S 2-1 Alexander’s payment was not an expense. Alexander acquired an asset, Equipment, because the computer is an economic resource of the business. (5 min.) S 2-2 a. $19,400 ($15,000 + $4,400 […]

978-0133427530 Chapter 2 Part 2

(10-15 min.) E 2-25B a. Increased assets (cash) b. Increased assets (land) c. Increased assets (supplies) d. No effect (a personal transaction) e. No effect on total assets. Increase in equipment offsets the decrease in cash. f. Increased assets (cash) […]

978-0133427530 Chapter 2 Part 3

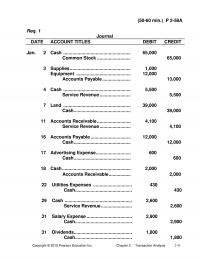

(50-60 min.) P 2-58A Req. 1 Journal DATE ACCOUNT TITLES DEBIT CREDIT Jan. 2 Cash ……………………………………………. 65,000 Common Stock …………………….. 65,000 3 Supplies ……………………………………….. 1,000 Equipment …………………………………… 12,000 Accounts Payable …………………. 13,000 4 Cash ……………………………………………. 5,500 Service Revenue …………………… 5,500 […]

978-0133427530 Chapter 2 Part 4

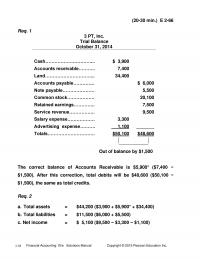

(20-30 min.) E 2-66 Req. 1 3 PT, Inc. Trial Balance October 31, 2014 Cash…………………………… $ 3,900 Accounts receivable……….. 7,400 Land…………………………… 34,400 Accounts payable………….. $ 6,000 Note payable………………… 5,500 Common stock……………… 20,100 Retained earnings………….. 7,500 Service revenue…………….. 9,500 Salary expense……………… […]

978-0133427530 Chapter 3 Part 1

Chapter 3 Accrual Accounting & Income Short Exercises (10 min.) S 3-1 Millions Sales revenue ……………………………………………………………. $825 Cost of goods sold ……………………………………………………. (255) All other expenses …………………………………………………….. (325) Net income ……………………………………………………………….. $245 Beginning cash …………………………………………………………. $ 75 Collections ($825 − […]

978-0133427530 Chapter 3 Part 2

(10-20 min.) E 3-25A Journal DATE ACCOUNT TITLES DEBIT CREDIT Closing Entries Dec. 31 Service Revenue ………………………………… 31,900 Other Revenue …………………………………… 400 Retained Earnings …………………………. 32,300 31 Retained Earnings ……………………………… 25,400 Cost of Services Sold ……………………. 14,300 Selling, General, and […]

978-0133427530 Chapter 3 Part 3

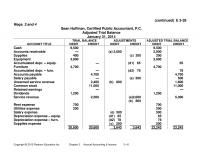

(continued) E 3-39 Reqs. 3 and 4 Sean Huffman, Certified Public Accountant, P.C. Adjusted Trial Balance January 31, 2014 TRIAL BALANCE ADJUSTMENTS ADJUSTED TRIAL BALANCE ACCOUNT TITLE DEBIT CREDIT DEBIT CREDIT DEBIT CREDIT Cash 9,500 9,500 Accounts receivable — (a) […]

978-0133427530 Chapter 3 Part 4

(45-60 min.) P 3-64A Req. 1 (All amounts in millions) Current ratio = Total current assets = $15.8 = 1.84 Total current liabilities $8.6 $13.9 Debt ratio = Total liabilities = $8.6 + $5.3 = 0.43 Total assets $32.1 Req. […]

978-0133427530 Chapter 3 Part 5

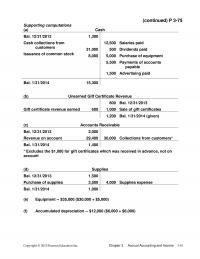

(continued) P 3-75 Supporting computations (a) Cash Bal. 12/31/2013 1,300 Cash collections from customers Issuance of common stock 31,000 8,000 12,500 500 5,000 Salaries paid Dividends paid Purchase of equipment 5,500 Payments of accounts payable 1,500 Advertising paid 1,500 Bal. […]

978-0133427530 Chapter 3 Part 6

(continued) Amazon.com, Inc. Req. 3 (amounts in millions) Journal DATE ACCOUNT TITLES DEBIT CREDIT a. Accrued Expenses and Other ………………….. 3,751 Cash ………………………………………………….. 3,751 b. Operating Expenses…………………………… 14,446 Cash ………………………………………………….. 8,762 Accrued Expenses and Other ……………… 5,684 The balance of […]

978-0133427530 Chapter 4 Part 1

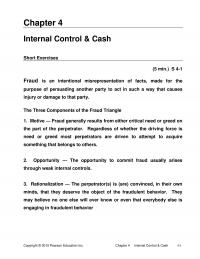

Chapter 4 Internal Control & Cash Short Exercises (5 min.) S 4-1 Fraud is an intentional misrepresentation of facts, made for the purpose of persuading another party to act in such a way that causes injury or damage to that […]

978-0133427530 Chapter 4 Part 2

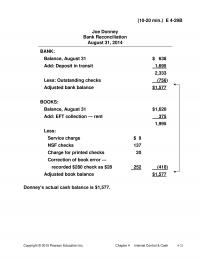

(10-20 min.) E 4-29B Joe Donney Bank Reconciliation August 31, 2014 BANK: Balance, August 31 $ 638 Add: Deposit in transit 1,695 2,333 Less: Outstanding checks (756) Adjusted bank balance $1,577 BOOKS: Balance, August 31 $1,620 Add: EFT collection — […]

978-0133427530 Chapter 4 Part 3

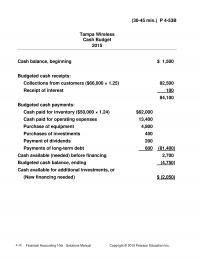

(30-45 min.) P 4-53B Tampa Wireless Cash Budget 2015 Cash balance, beginning $ 1,500 Budgeted cash receipts: Collections from customers ($66,000 × 1.25) 82,500 Receipt of interest 100 84,100 Budgeted cash payments: Cash paid for inventory ($50,000 × 1.24) $62,000 […]

978-0133427530 Chapter 5 Part 1

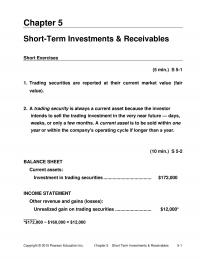

Chapter 5 Short-Term Investments & Receivables Short Exercises (5 min.) S 5-1 1. Trading securities are reported at their current market value (fair value). 2. A trading security is always a current asset because the investor intends to sell the […]

978-0133427530 Chapter 5 Part 2

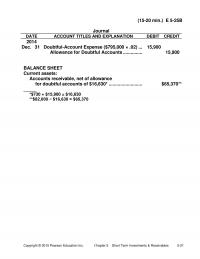

(15-20 min.) E 5-25B Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT 2014 Dec. 31 Doubtful-Account Expense ($795,000 × .02) … 15,900 Allowance for Doubtful Accounts …………… 15,900 BALANCE SHEET Current assets: Accounts receivable, net of allowance for doubtful accounts […]

978-0133427530 Chapter 5 Part 3

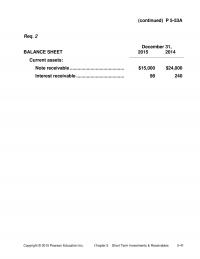

(continued) P 5-53A Req. 2 December 31, BALANCE SHEET 2015 2014 Current assets: Note receivable …………………………………… $15,000 $24,000 Interest receivable ………………………………. 98 240 Copyright © 2015 Pearson Education Inc. Chapter 5 Short Term Investments & Receivables 5-41 (15-25 min.) P […]

978-0133427530 Chapter 5 Part 4

(continued) P 5-61B Req. 2 The current ratio improved from 1.38 to 1.74. The quick (acid-test) ratio increased from 0.83 to 0.99. Days’ sales in receivables improved from 18 days to 17 days. All three ratio values improved during the […]

978-0133427530 Chapter 6 Part 1

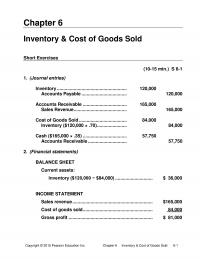

Chapter 6 Inventory & Cost of Goods Sold Short Exercises (10-15 min.) S 6-1 1. (Journal entries) Inventory ……………………………………………… 120,000 Accounts Payable …………………………….. 120,000 Accounts Receivable ……………………………. 165,000 Sales Revenue ………………………………….. 165,000 Cost of Goods Sold ………………………………. 84,000 Inventory ($120,000 […]

978-0133427530 Chapter 6 Part 2

(10-15 min.) E 6-26B Req. 1 Inventory Beg. bal. (6 units @ $170) 1,020 Purchases Aug. 15 (8 units @ $172) 1,376 Cost of goods sold 26 (14 units @ $180) 2,520 (17 units @ $?) ? Ending bal. (11 […]

978-0133427530 Chapter 6 Part 3

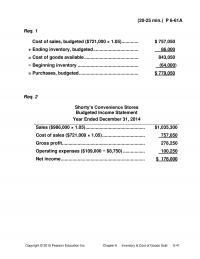

(20-25 min.) P 6-61A Req. 1 Cost of sales, budgeted ($721,000 × 1.05) …………. $ 757,050 + Ending inventory, budgeted …………………………….. 86,000 = Cost of goods available …………………………………… 843,050 − Beginning inventory ……………………………………….. (64,000) = Purchases, budgeted ………………………………………. $ 779,050 […]

978-0133427530 Chapter 6 Part 4

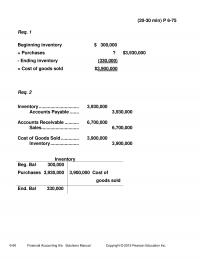

(20-30 min) P 6-75 Req. 1 Beginning inventory $ 300,000 + Purchases ? $3,930,000 – Ending inventory (330,000) = Cost of goods sold $3,900,000 Req. 2 Inventory …………………………. 3,930,000 Accounts Payable ……. 3,930,000 Accounts Receivable ……….. 6,700,000 Sales ……………………….. 6,700,000 […]

978-0133427530 Chapter 7 Part 1

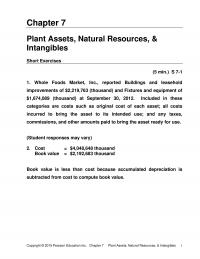

Chapter 7 Plant Assets, Natural Resources, & Intangibles Short Exercises (5 min.) S 7-1 1. Whole Foods Market, Inc., reported Buildings and leasehold improvements of $2,219,763 (thousand) and Fixtures and equipment of $1,674,089 (thousand) at September 30, 2012. Included in […]

978-0133427530 Chapter 7 Part 2

(5-10 min.) E 7-27A Req. 1 Net profit margin ratio for the years ended: January 31, 2013 January 31, 2012 Net earnings $ 2,010 = 4.12% $ 1,783 = 3.78% Net sales $48,815 $47,220 The net profit margin ratio improved […]

978-0133427530 Chapter 7 Part 3

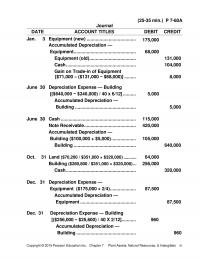

(25-35 min.) P 7-60A Journal DATE ACCOUNT TITLES DEBIT CREDIT Jan. 3 Equipment (new) ……………………………….. 175,000 Accumulated Depreciation — Equipment ………………………………………… 68,000 Equipment (old) ……………………………… 131,000 Cash ……………………………………………… 104,000 Gain on Trade-in of Equipment [$71,000 – ($131,000 − $68,000)] ……… […]

978-0133427530 Chapter 7 Part 4

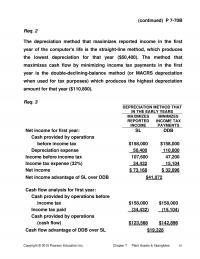

(continued) P 7-70B Req. 2 The depreciation method that maximizes reported income in the first year of the computer’s life is the straight-line method, which produces the lowest depreciation for that year ($50,400). The method that maximizes cash flow by […]

978-0133427530 Chapter 7 Part 5

(continued) Decision Case 1 Req. 1 *Cost of goods sold: Units Cost La Petite (FIFO): 10,000 × $4 = $ 40,000 5,000 × 5 = 25,000 7,000 × 6 = 42,000 3,000 × 7 = 21,000 25,000 $128,000 Burgers (LIFO): […]

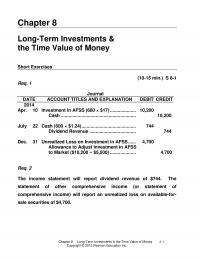

978-0133427530 Chapter 8 Part 1

Chapter 8 Long-Term Investments & the Time Value of Money Short Exercises (10-15 min.) S 8-1 Req. 1 Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT 2014 Apr. 10 Investment in AFSS (600 × $17) ……………….. 10,200 Cash …………………………………………………. 10,200 […]

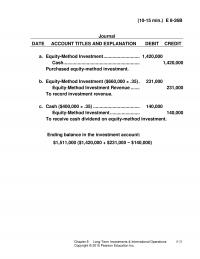

978-0133427530 Chapter 8 Part 2

Chapter 8 Long-Term Investments & International Operations 8-21 (10-15 min.) E 8-26B Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT a. Equity-Method Investment ………………………. 1,420,000 Cash ………………………………………………….. 1,420,000 Purchased equity-method investment. b. Equity-Method Investment ($660,000 × .35) . 231,000 Equity-Method […]

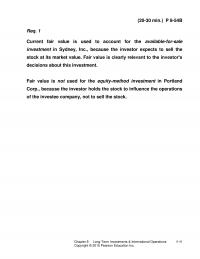

978-0133427530 Chapter 8 Part 3

Chapter 8 Long-Term Investments & International Operations 8-41 (20-30 min.) P 8-54B Req. 1 Current fair value is used to account for the available-for-sale investment in Sydney, Inc., because the investor expects to sell the stock at its market value. […]

978-0133427530 Chapter 8 Part 4

Chapter 8 Long-Term Investments and International Operations 53 (20-25 min.) P 8-63 Req. 1 Amount of Cash Flow 5% Factor from Table Present Value of Cash Flow $ 20,000 x .952 = $ 19,040 25,000 x .907 = 22,675 30,000 […]

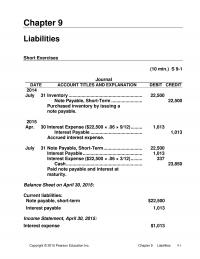

978-0133427530 Chapter 9 Part 1

Chapter 9 Liabilities Short Exercises (10 min.) S 9-1 Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT 2014 July 31 Inventory ………………………………………………… 22,500 Note Payable, Short-Term …………………… 22,500 Purchased inventory by issuing a note payable. 2015 Apr. 30 Interest Expense […]

978-0133427530 Chapter 9 Part 2

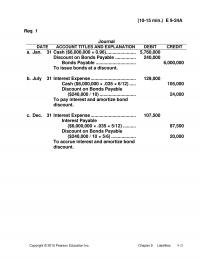

(10-15 min.) E 9-24A Req. 1 Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT a. Jan. 31 Cash ($6,000,000 × 0.96) ………………….. 5,760,000 Discount on Bonds Payable ……………. 240,000 Bonds Payable …………………………. 6,000,000 To issue bonds at a discount. b. […]

978-0133427530 Chapter 9 Part 3

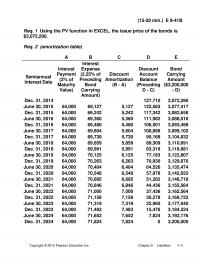

(15-20 min.) E 9-41B Req. 1 Using the PV function in EXCEL, the issue price of the bonds is $3,072,290. Req. 2 (amortization table) A B C D E Semiannual Interest Date Interest Payment (2% of Maturity Value) Interest Expense […]

978-0133427530 Chapter 9 Part 4

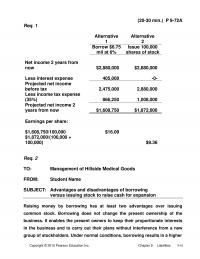

(20-30 min.) P 9-72A Req. 1 Alternative Alternative 1 2 Borrow $6.75 Issue 100,000 mil at 6% shares of stock Net income 2 years from now $2,880,000 $2,880,000 Less interest expense 405,000 -0- Projected net income before tax 2,475,000 2,880,000 […]

978-0133427530 Chapter 9 Part 5

(continued) P 9-82B Req. 5 Leverage ratio Total assets ($7,265,000) Total stockholders’ equity ($2,633,000) = 2.76 Debt ratio = Total liabilities ($4,632,000) = 0.64 Total assets ($7,265,000) The leverage ratio and debt ratio would increase. The company would be considered […]

978-0133427530 Chapter 9 Part 6

(continued) Ethical Issue 2 4. The FASB and IASB are working on a proposed new lease standard that removes the mechanical criteria for lease capitalization discussed in the chapter in favor of the more theoretically and substantively correct, but also […]

AC 111 Quiz

1) Fraud is a major problem in many businesses throughout the world. 2) The net of foreign-currency transaction gains and losses will appear on the income statement. Answer: TRUE 3) The process of determining the present value of a sum […]

AC 156

1) The total earned wages of an employee for the payroll period is the ________. The amount of earned wages the employee takes home is _________. A) gross pay; withholding amount B) gross pay; net pay C) net pay; gross […]

AC 184

1) Under the indirect method to prepare the statement of cash flows, a decrease in accounts payable is deducted from net income when calculating Net Cash Provided by Operating Activities. 2) Unrealized gains and losses on trading securities are reported […]

AC 647 Final

1) The market prices of bonds fluctuate inversely with market interest rates. 2) In order to effectively evaluate the days’ sales in receivables, it should be compared to the company’s credit terms. Answer: TRUE 3) A purchaser is willing to […]

AC 709 Final

1) Advantages of a corporation include: A) each stockholder can enter into agreements that legally bind all the stockholders B) the double taxation of distributed profits C) limited liability of the stockholders for the corporation’s debts D) each stockholder can […]

AC 801

1) The amount of cash received on the sale of the company’s stock in excess of par value is called retained earnings. 2) The straight-line amortization method keeps interest expense at the same dollar amount for every interest payment over […]

AC 810 Test 1

1) Items of comprehensive income, other than net income, do not enter into the determination of earnings per share. 2) Common stockholders receive dividends even if the total dividend is not large enough to pay the preferred stockholders first. Answer: […]

AC 887 Quiz 3

1) Which of the following is an accurate statement about book and tax depreciation methods? A) Straight-line depreciation is the most popular method for income-tax purposes B) The IRS has their own set of rules to compute depreciation for income […]

Acc 130 Test 1

1) The amount of prepaid insurance used up during a period of time is called Insurance Expense. 2) If the market interest rate is greater than the stated interest rate, the bonds will sell at a discount. Answer: TRUE 3) […]

Acc 149 1 A corporation acts under

1) A corporation acts under its own name and not the name of its stockholders. 2) The sum of the cash in the petty cash fund and the total of the paid vouchers should equal the opening balance in the […]

Acc 182 Test

1) On the stockholders’ equity section of the Balance Sheet, Common Stock is listed before Preferred Stock. 2) The Loss on Disposal of Equipment account is reported as Other Losses and Expenses on the income statement. Answer: TRUE 3) Expenses […]

Acc 271 Midterm 1

1) When bonds payable are converted into common stock, the carrying value of the bonds is transferred to paid-in capital. 2) A budget is a financial plan that helps coordinate business activities. Answer: TRUE 3) Accounting is moving in the […]

Acc 308

1) Accounts receivable is increased with a credit 2) Inventory is reported on the balance sheet at the selling price of the item. Answer: FALSE 3) In the statement of cash flows, purchases of fixed assets are considered to be […]

Acc 446 Test 1

1) An investor has a long-term available-for-sale stock investment. The investor receives a stock dividend on the stock investment. No journal entry is necessary for the stock dividend. 2) The adjusted trial balance lists only the balance sheet accounts and […]

ACC 510 Test

1) The maker of a note records interest expense. 2) Foreign-Currency Transaction Losses can be avoided if international transactions are settled in U.S. dollars instead of the foreign currency. Answer: TRUE 3) The principal of a note payable is the […]

Acc 663 Midterm 1

1) The word “payable” always signifies a liability. 2) In the units-of production method, a fixed amount of depreciation expense is assigned to each unit of output. Answer: TRUE 3) A note payable may require the borrower to accrue interest […]

ACC 708 Quiz

1) Accounts payable turnover is an important measure of liquidity for a retail business. 2) The choice of an inventory costing method does not impact a company’s balance sheet. Answer: FALSE 3) If a corporation pays taxes on its income, […]

ACC 851 Homework

1) On January 1, 2014, Bucket Company purchased as an investment a $1,000, 7% bond for $980. Bucket plans to hold the bond until the maturity date of January 1, 2024. The bond pays interest on January 1 and July […]

Accounting 194

1) In the statement of cash flows, more purchases of long-term assets than sales of long-term assets are considered a sign of a healthy company. 2) External auditors are responsible for maintaining the internal controls for each company they audit. […]

Accounting 256 Quiz 1

1) Accepting credit cards can increase revenue for a company, but the added revenue comes at a cost. 2) The indirect method of preparing the statement of cash flows provides the clearest picture of the cash inflows and cash outflows […]

Accounting 328 Midterm 2

1) A company has the following adjusted trial balance: What closing entries are needed? A) Debit Service Revenue for $33,000 and credit Retained Earnings for $33,000 B) Debit Rent Expense for $2,300 and credit Retained Earnings for $2,300 C) Credit […]

Accounting 366

1) Smart hiring practices and separation of duties is part of the control environment. 2) The income statement and the statement of cash flows often paint the same picture of the company. Answer: FALSE 3) If the stated interest rate […]

Accounting 465

1) Depreciation allocates the cost of land to expense over the useful life of the land. 2) A purchase discount decreases the cost of the inventory. Answer: TRUE 3) GAAP requires the use of accrual-basis accounting. Answer: TRUE 4) When […]

Accounting 766 Midterm

1) A compensating balance maintained for a loan increases the actual interest rate on a loan. 2) The Sarbanes-Oxley Act created the American Institute of Certified Public Accountants to oversee the audits of public companies. Answer: FALSE 3) Comprehensive income […]

ACCT 244 Test

1) Net cash provided by operating activities is $2.3 million. Planned capital expenditures are $2 million. Depreciation expense is $1 million per year. What is free cash flow? A) ($700,000) B) $300,000 C) $1,000,000 D) $1,300,000 2) An Investment in […]

Acct 272 Final

1) What is the proper order for the different categories of cash flows reported on the statement of cash flows? A) Financing activities, investing activities, and operating activities B) Operating activities, investing activities, and financing activities C) Operating activities, financing […]

ACCT 327 Midterm

1) The cost of installing lights in a company’s parking lot should be recorded as a cost of: A) land B) land improvements C) leasehold improvements D) leaseholds 2) The amount of owners’ equity attributable to each share of common […]

Acct 332 Final

1) The carrying amount of bonds at maturity should be equal to the face value of the bonds. 2) Since we live in a global economy, all countries have adopted the same accounting standards for business transactions. Answer: FALSE[/cpmembership] 3) […]

Acct 383 Final

1) Access to sensitive data files in a business should be protected by Trojan horses. 2) A receiving report informs a vendor of the amount of goods received by the purchaser. Answer: FALSE 3) Cash equivalents do NOT include highly […]

Acct 436 1 Accounting information

1) Accounting information is used by investors and lenders, but not by regulatory bodies. 2) When an investor owns 35% of the stock of another business, cash dividends received from the investee company are recorded by decreasing the Equity-Method Investment […]

ACCT 457 Test 2

1) An error in ending inventory creates errors for two accounting periods. 2) Trend analysis using income statement data is widely used for predicting the future. Answer: TRUE 3) Trend percentages are computed only for balance sheet items. Answer: FALSE […]

Acct 493 Midterm 2

1) Orlando Corporation incorporated on January 2, 2015. During 2015, Orlando had the following transactions: issued 30,000 shares of common stock at $25 per share. The par value per share is $1. purchased 5,000 shares of treasury stock at $28 […]

ACCT 661 Midterm 2

1) The shipping terms in the sales contract determine when ownership of goods changes hands between the buyer and the seller. 2) A 2-for-1 stock split will increase total stockholders’ equity. Answer: FALSE 3) Lease payments are paid by the […]

ACCT 669 Quiz 3

1) At the end of the period, the difference between the total credits and the total debits is the balance in the account 2) Under the equity method, the investor applies his percentage of ownership in recording his share of […]

Acct 733

1) The cost of land may include the cost of any back property taxes that the purchaser pays. 2) A company can sell common stock in exchange for assets other than cash. Answer: TRUE 3) The statement of cash flows […]

Acct 770 Quiz 1

1) What is the calculation to determine the number of outstanding shares of stock? A) number of treasury stock shares plus number of issued shares B) number of authorized shares minus number of issued shares C) number of issued shares […]

ACCT 824 Quiz 1

1) A gain or loss on the sale of a long-term investment using the equity method is calculated by taking the difference between the cash received and: A) fair value of the investment B) lower-of-cost-or-market value of the investment C) […]

ACT 238

1) Gary Kraen Company purchased equipment on May 1, 2014 for $100,000. The residual value is $10,000 and the estimated useful life is 10 years. What is the Depreciation Expense for the year ending December 31, 2015, if the company […]

ACT 330

1) The expense recognition principle recognizes expenses in the period they are paid. 2) Taxable income should always match pretax accounting income. Answer: FALSE 3) A current ratio below 1.0 is a sign of financial strength for a company. Answer: […]

MET MG 159

1) The Balance Sheet reports the Retained Earnings at the end of a fiscal year. Where does the amount of Retained Earnings as reported on the Balance Sheet come from? A) Trial Balance Worksheet B) Adjusted Trial Balance C) Unadjusted […]

MET MG 310 Quiz

1) Cash-basis accounting does NOT record: A) purchase of supplies with cash B) sale of common stock C) payment of note payable D) depreciation expense 2) When a company uses borrowed money to earn a higher profit than the cost […]

MET MG 394 Final

1) All employees should have a background check before being hired, and should be properly trained and supervised. 2) If a company declares and pays a dividend to its stockholders, both cash and expenses will decrease Answer: FALSE 3) The […]

MET MG 414

1) If an investor company owns 35% of the common stock of another business, income received from the investee company are generally recorded by the investor company by: A) decreasing the investor company’s Common Stock account B) increasing the value […]

MET MG 814

1) A company reports the following balances: What is reported on the statement of cash flows prepared with the indirect method for the year ended December 31, 2016? Assume there were no retirements of common stock during 2016. No dividends […]

SMG AC 188 Homework

1) The inventory turnover ratio should be the same for all types of industries. 2) Cost of Goods Sold is an operating expense on the income statement. Answer: FALSE 3) A corporation is not an entity that is separate from […]

SMG AC 390 Test 1

1) If a company has sales of $250 in 2015 and $225 in 2016, the percentage decrease from 2015 to 2016 is 10%. 2) If a corporation’s economic value added is negative, stockholders will probably be displeased with the company’s […]

SMG AC 457

1) An investor receives a stock dividend from a long-term available-for-sale investment. Which journal entry is required? A) a debit to Cash and a credit to Dividend Revenue B) a debit to Cash and a credit to Unrealized Gain on […]

SMG AC 598

1) The ratio that measures a company’s success in using its assets to earn income for the persons who finance the business is the: A) leverage B) rate of return on total assets C) debt ratio D) times-interest-earned ratio 2) […]

SMG AC 797 Test

1) A business purchased office supplies of $10,000 using a note The business would: A) debit Supplies for $10,000 and credit Accounts Payable for $10,000 B) debit Supplies for $10,000 and credit Notes Payable for $10,000 C) debit Note Receivable […]