(continued) E 12-20A

Req. 2

Tullis’ cash flows look strong. Operations are the main source of cash.

The company is investing in new plant assets without having to borrow.

(5-10 min.) E 12-21A

Case A — A combination of operations and issuing stock generated

Case B — The sale of plant assets generated the cash needed to

(10-15 min.) E 12-22A

a. Cash proceeds of sale = Book value of asset sold, $38,000* +

Plant Assets, Net

Beginning balance

129,000

Depreciation expense

16,000

Purchases

47,000

Book value sold*

38,000

Ending balance

122,000

b. Cash dividend declared = $72,000*

Retained Earnings

Stock dividends

24,000

Beginning balance

67,000

Cash dividends*

72,000

Net income

132,000

Ending balance

103,000

(10-15 min.) E 12-23A

Cash flows from operating activities:

Receipts:

Collections from customers

($86,000 + $73,000) ………………………..

$ 159,000

Collection of dividend revenue …………..

12,000

Total cash receipts………………………..

171,000

Payments:

To suppliers ……………………………………..

$(61,000)

To employees……………………………………

(47,000)

For interest ……………………………………….

(8,000)

For income tax ………………………………….

(16,000)

Total cash payments ……………………..

(132,000)

Net cash provided by (used for)

operating activities …………………………...

$ 39,000

Operating cash flow is strong as shown by the net cash provided by

operating activities.

(5-10 min.) E 12-24A

Salary Payable — Report cash payments to employees as operating

cash flows.

(20-30 min.) E 12-25A

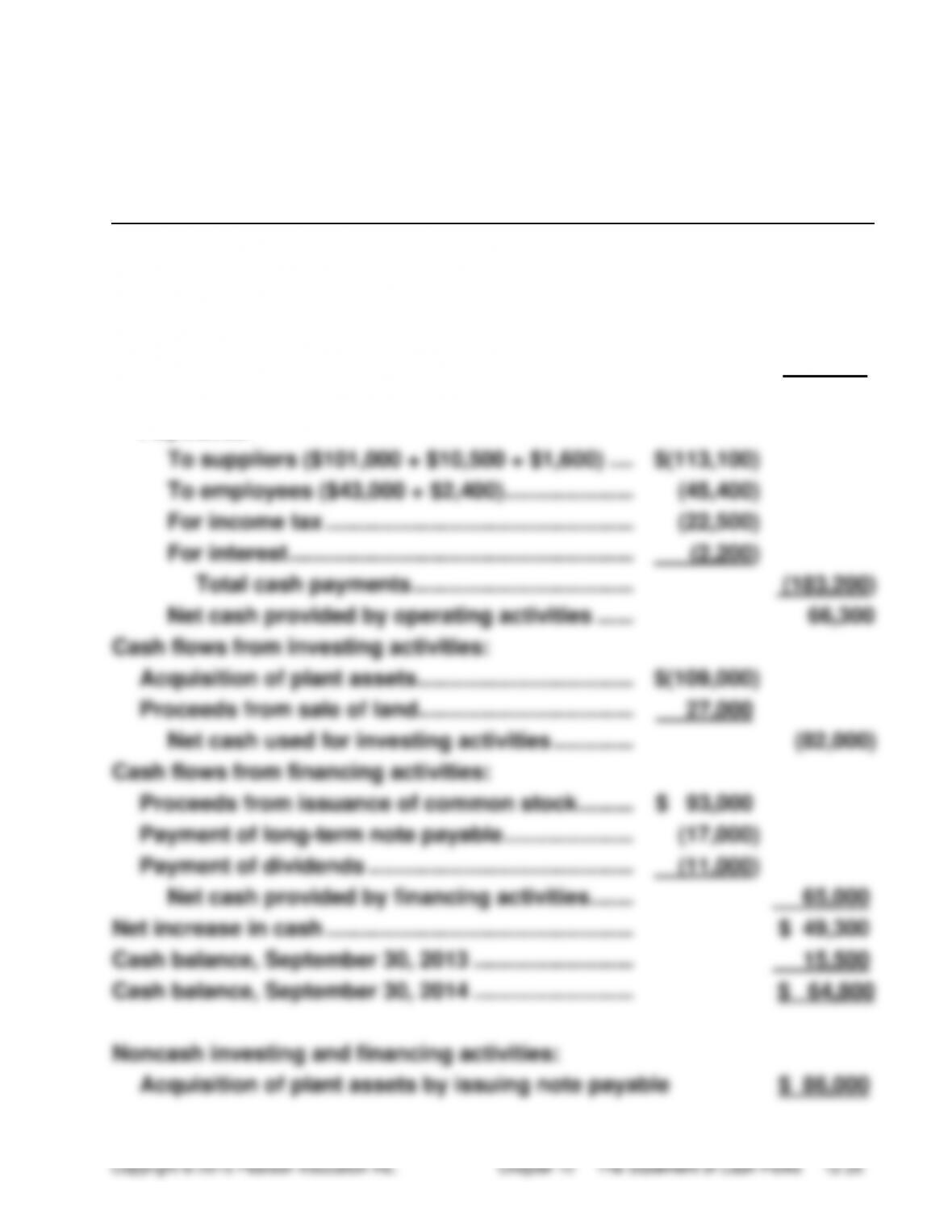

Req. 1

Office World, Inc.

Statement of Cash Flows

Year Ended September 30, 2014

Cash flows from operating activities:

Receipts:

Collections from customers

($255,000 − $15,000) ……………………………….

$ 240,000

Dividends received …………………………………….

9,500

Total cash receipts …………………………………

249,500

Payments:

To suppliers ($101,000 + $10,500 + $1,600) ….

$(113,100)

To employees ($43,000 + $2,400) …………………

(45,400)

For income tax …………………………………………..

(22,500)

For interest ………………………………………………..

(2,200)

Total cash payments …………………………..….

(183,200)

Net cash provided by operating activities ……

66,300

Cash flows from investing activities:

Acquisition of plant assets ……………………………..

$(109,000)

Proceeds from sale of land ……………………………..

27,000

Net cash used for investing activities ………….

(82,000)

Cash flows from financing activities:

Proceeds from issuance of common stock ………

$ 93,000

Payment of long-term note payable …………………

(17,000)

Payment of dividends …………………………………….

(11,000)

Net cash provided by financing activities …….

65,000

Net increase in cash …………………………………………..

$ 49,300

Cash balance, September 30, 2013 ……………………..

15,500

Cash balance, September 30, 2014 ……………………..

$ 64,800

Noncash investing and financing activities:

Acquisition of plant assets by issuing note payable

$ 86,000

(continued) E 12-25A

Req. 2

Office World’s cash flows look strong. Operations are the main source of

(10-15 min.) E 12-26A

$7,000 decrease in

a.

Cash collections

=

$139,000

+

Accounts Receivable

($42,000 − $35,000)

=

$146,000

Cash payments

for inventory

$3,000 increase in

$2,000 increase in

b.

=

$67,000

+

Inventory

−

Accounts Payable

($59,000 − $56,000)

($26,000 − $24,000)

=

$68,000

(10-15 min.) E 12-27B

O+

a.

Loss on sale of equipment

I+

k.

Sale of long-term

investment

O+

b.

Decrease in accounts

receivable

F+

l.

Issuance of common stock

for cash

NIF

c.

Acquisition of equipment

by issuance of note

O–

m.

Decrease in accrued

payable

liabilities

O+

d.

Increase in accounts

O+

n.

Amortization of intangible

payable

assets

F–

e.

Payment of cash

I–

o.

Acquisition of building by

dividend

cash payment

I–

f.

Purchase of long-term

F–

p.

Payment of long-term debt

investment

F+

q.

Issuance of long-term note

I+

g.

Cash sale of land

payable to borrow cash

O–

h.

Increase in prepaid

F–

r.

Purchase of treasury stock

expenses

O+

s.

Net income

O+

i.

Increase in salary payable

O+

j.

Depreciation of equipment

(5-10 min.) E 12-28B

a.

Investing

h.

Financing

b.

Investing

i.

Investing

c.

Operating

j.

Noncash investing and

Financing

d.

Operating

k.

Financing

e.

Operating

l.

Operating

f.

Financing

m.

Investing

g.

Financing

(10-15 min.) E 12-29B

Cash flows from operating activities:

Net income ………………………………………………..

$ 35,000

Adjustments to reconcile net income to

net cash used for operating activities:

Depreciation expense …………………………...

$ 7,000

Gain on sale of land ………………………………

(14,000)

Increase in current assets other

than cash ……………………………………………

(25,000)

Decrease in current liabilities…………………

(19,000)

(51,000)

Net cash provided by (used for) operating

activities …………………………………………………

$(16,000)

Operating cash flow is weak, as shown by the negative net cash flows

from operating activities. Normally, net cash provided by operations

is more than net income because of the depreciation add-back.

(15-20 min.) E 12-30B

Cash flows from operating activities:

Net income ………………………………………………

$ 21,000

Adjustments to reconcile net income to

net cash used for operating activities:

Depreciation expense …………………………

$ 6,000

Increase in accounts receivable …………..

(81,000)

Increase in inventory …………………………..

(47,000)

Increase in accounts payable ………………

61,500

Decrease in accrued liabilities …………….

(5,000)

(65,500)

Net cash used for operating activities ………….

$(44,500)

Chaplaine Fur Traders shows signs of trouble collecting receivables and

selling inventory. There is a large build-up in both Accounts Receivable

and Inventory. The large increase in Accounts Payable implies that the

company is having trouble paying their bills.

(20-30 min.) E 12-31B

Req. 1

Tyler Travel Products, Inc.

Statement of Cash Flows

Year Ended December 31, 2014

Cash flows from operating activities:

Net income ………………………………………………….

$109,400

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense …………………………….

$ 21,000

Decrease in accounts receivable …………….

16,000

Increase in inventory ……………………………..

(22,000)

Increase in prepaid expenses …………………

(1,200)

Increase in accounts payable …………………

1,500

Decrease in accrued liabilities ………………..

(12,000)

3,300

Net cash provided by operating activities …..

112,700

Cash flows from investing activities:

Acquisition of plant assets …………………………..

$(95,000)

Proceeds from sale of land …………………………..

14,000

Net cash used for investing activities …………

(81,000)

Cash flows from financing activities:

Proceeds from issuance of common stock ……

$ 50,000

Payment of long-term note payable ………………

(18,000)

Payment of dividends …………………………………..

(12,000)

Net cash provided by financing activities …..

20,000

Net increase in cash …………………………………………

$ 51,700

Cash balance, December 31, 2013 …………………….

33,500

Cash balance, December 31, 2014 …………………….

$ 85,200

Noncash investing and financing activities:

Acquisition of plant assets by issuing note payable

$ 55,000

(continued) E 12-31B

Req. 2

Tyler’s cash flows look strong. Operations are the main source of cash.

(5-10 min.) E 12-32B

Case A — A combination of operations and issuing stock generated

most of the cash for acquisition of plant assets. The company

also sold plant assets for cash.

(10-15 min.) E 12-33B

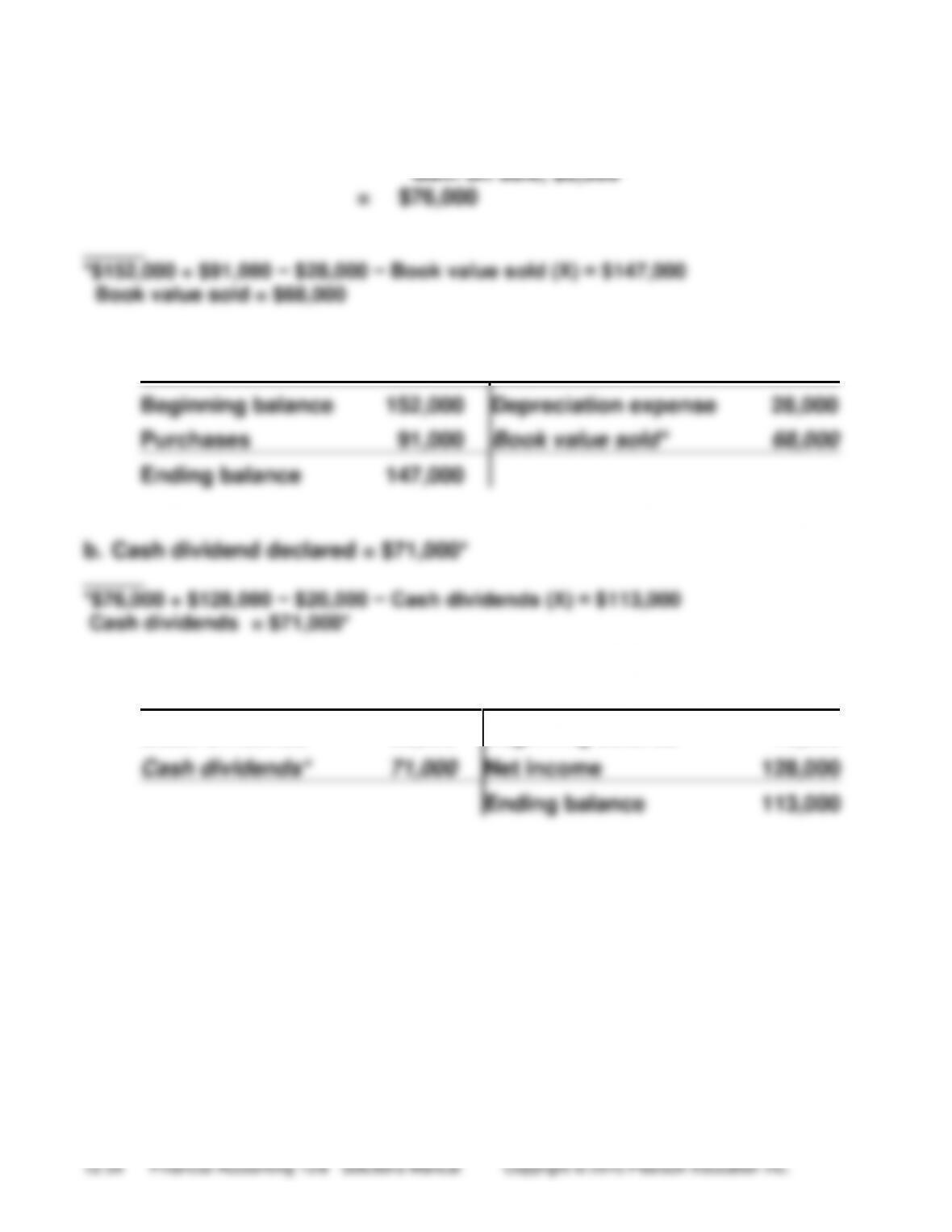

a. Cash proceeds of sale = Book value of asset sold, $68,000* +

Plant Assets, Net

Beginning balance

152,000

Depreciation expense

28,000

Purchases

91,000

Book value sold*

68,000

Ending balance

147,000

Retained Earnings

Stock dividends

20,000

Beginning balance

76,000

Cash dividends*

71,000

Net income

128,000

Ending balance

113,000

(10-15 min.) E 12-34B

Cash flows from operating activities:

Receipts:

Collections from customers

($119,000 + $51,000) ……………………….

$ 170,000

Collection of dividend revenue ……………

14,000

Total cash receipts…………………………

184,000

Payments:

To suppliers ………………………………………

$(63,000)

To employees…………………………………….

(44,000)

For interest ………………………………………..

(9,000)

For income tax …………………………………..

(20,000)

Total cash payments ………………………

(136,000)

Net cash provided by operating activities..

$ 48,000

(5-10 min.) E 12-35B

Salary Payable — Report cash payments to employees as operating

cash flows.

(20-30 min.) E 12-36B

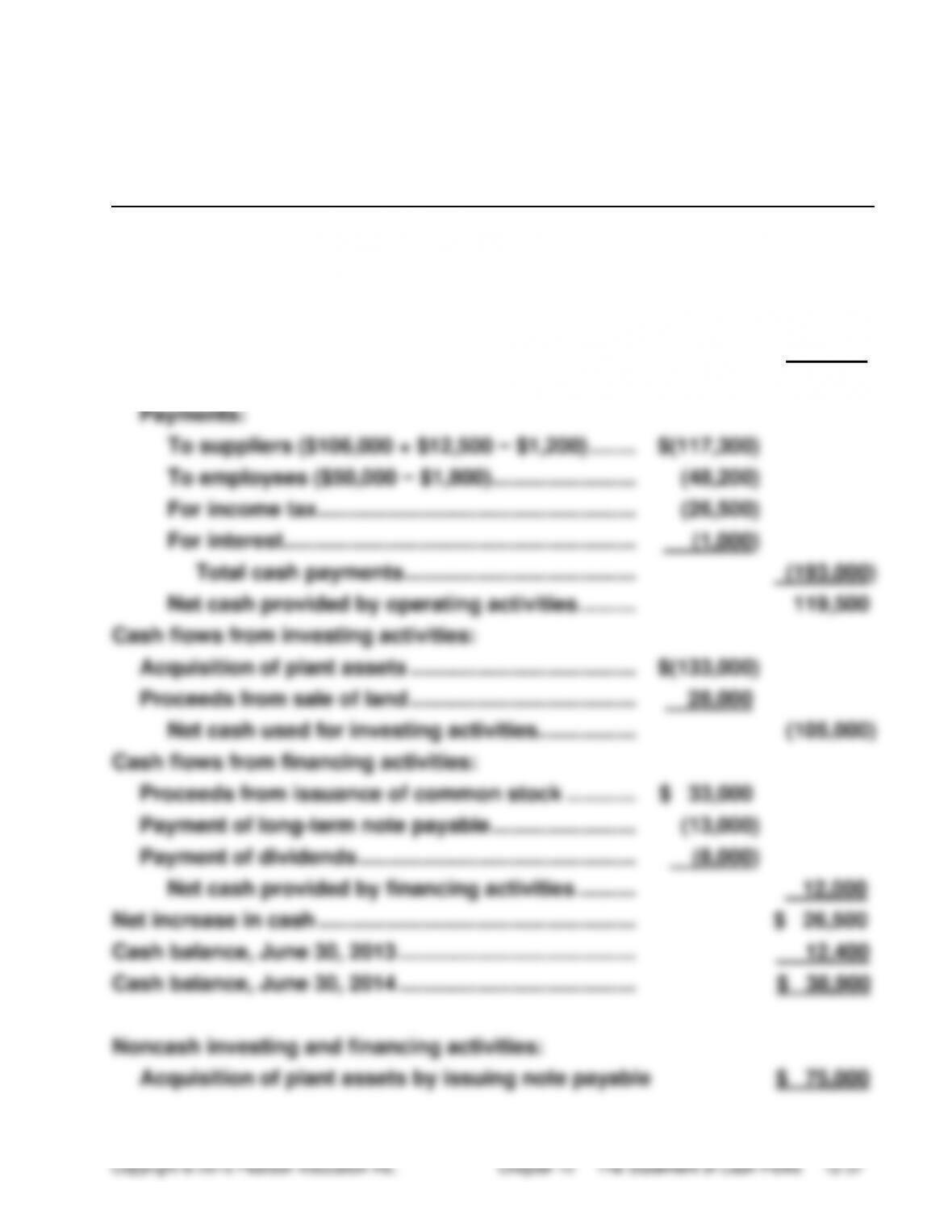

Req. 1

Quik Shop, Inc.

Statement of Cash Flows

Year Ended June 30, 2014

Cash flows from operating activities:

Receipts:

Collections from customers

($275,000 + $30,000) …………………………………..

$ 305,000

Dividends received ………………………………………..

7,500

Total cash receipts …………………………………….

312,500

Payments:

To suppliers ($106,000 + $12,500 − $1,200) ……..

$(117,300)

To employees ($50,000 − $1,800) …………………….

(48,200)

For income tax ……………………………………………….

(26,500)

For interest…………………………………………………….

(1,000)

Total cash payments ………………………………….

(193,000)

Net cash provided by operating activities ……….

119,500

Cash flows from investing activities:

Acquisition of plant assets …………………………………

$(133,000)

Proceeds from sale of land …………………………………

28,000

Net cash used for investing activities ……………..

(105,000)

Cash flows from financing activities:

Proceeds from issuance of common stock …………

$ 33,000

Payment of long-term note payable …………………….

(13,000)

Payment of dividends …………………………………………

(8,000)

Net cash provided by financing activities ……….

12,000

Net increase in cash …………………………..…………………..

$ 26,500

Cash balance, June 30, 2013 …………………………………..

12,400

Cash balance, June 30, 2014 …………………………………..

$ 38,900

Noncash investing and financing activities:

Acquisition of plant assets by issuing note payable

$ 75,000

(continued) E 12-36B

Req. 2

Quik Shop’s cash flows look strong. Operations are the main source of

(10-15 min.) E 12-37B

$6,000 increase in

a.

Cash collections

=

$141,000

−

Accounts Receivable

($53,000 − $47,000)

=

$135,000

Cash payments

for inventory

$4,000 decrease in

$3,000 increase in

b.

=

$76,000

−

Inventory

−

Accounts Payable

($39,000 − $35,000)

($32,000 − $29,000)

=

$69,000

Quiz

Q12–38

b

Q12–39

a

Q12–40

c

Q12-41

d

Q12-42

c

Q12-43

b

Q12-44

d

Q12-45

1. Receiving dividends – operating

2. Paying dividends – financing

Q12-46

b [Book value = $12,000 ($18,000 − $6,000); Gain =

$4,000; Proceeds = $16,000 ($12,000 + $4,000)]

Q12-47

a

Q12–48

c

Q12–49

a

Q12-50

d Net inc. − Gain + Depr. + A/R dec − Inv. inc − A/P dec + Acc Liab inc

($36,500 − $10,000 + $7,500 + $5,000 − $1,000 − $1,000 + $4,000)

Q12-51

b

Q12-52

a Cash from sale of equip., ($20,000 + $10,000) $30,000

Cash paid for purchase of equip. (55,500)

($67,000 − $20,000 − $7,500 + $X = $95,000)

Net cash used $25,500

Q12-53

d

Q12-54

a

Q12-55

c Cash flow from stock issuance ($24,000 – $12,000) $12,000

Cash dividends paid (26,500)

($66,000 + $36,500 − $X = $76,000)

Net cash used $14,500

Q12-56

b ($750,000 − $60,000 = $690,000)

Q12-57

c [$58,900 − ($5,000 − $2,600) = $56,500]