(continued) P 7-70B

Req. 2

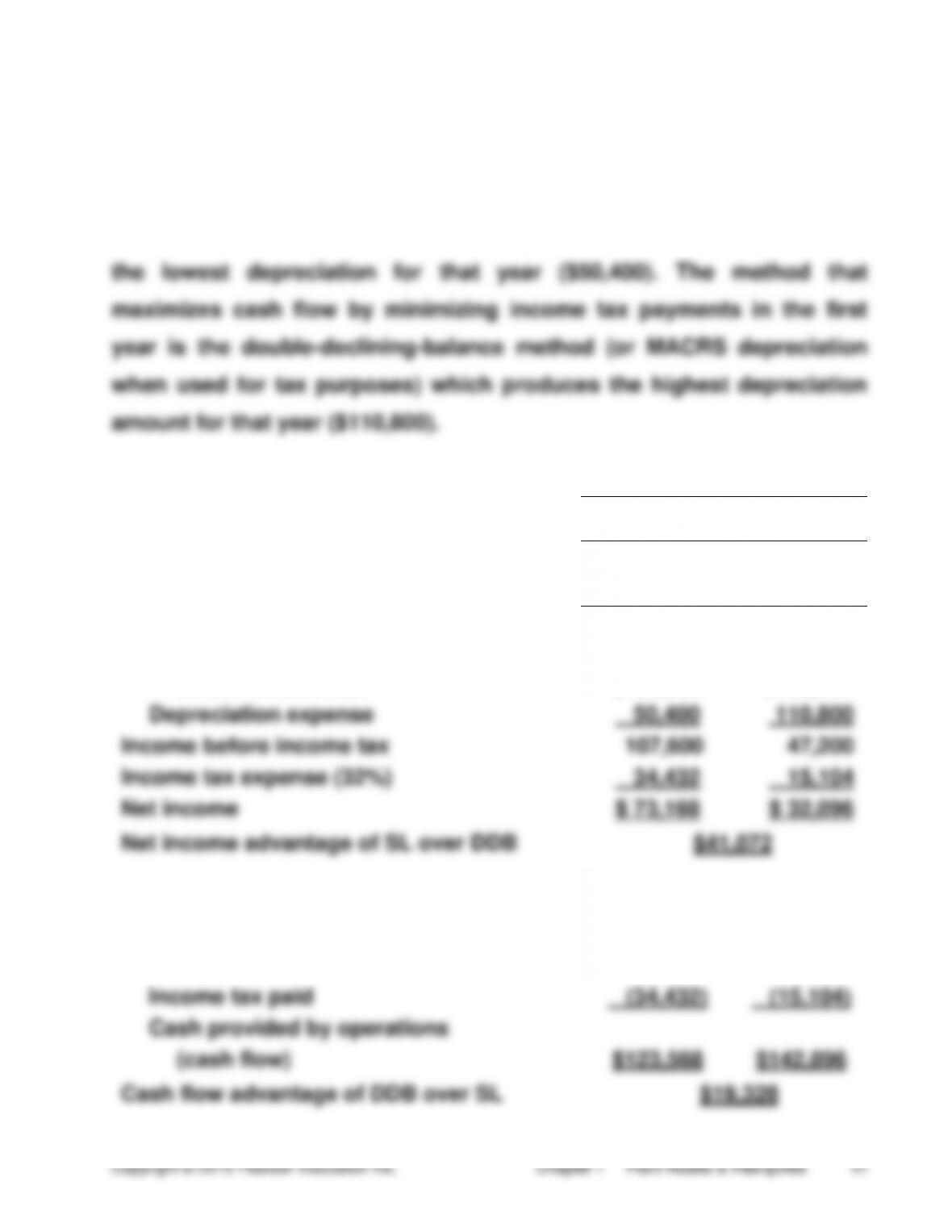

The depreciation method that maximizes reported income in the first

year of the computer’s life is the straight-line method, which produces

Req. 3

DEPRECIATION METHOD THAT

IN THE EARLY YEARS

MAXIMIZES

REPORTED

INCOME

MINIMIZES

INCOME TAX

PAYMENTS

Net income for first year:

SL

DDB

Cash provided by operations

before income tax

$158,000

$158,000

Depreciation expense

50,400

110,800

Income before income tax

107,600

47,200

Income tax expense (32%)

34,432

15,104

Net income

$ 73,168

$ 32,096

Net income advantage of SL over DDB $41,072

Cash flow analysis for first year:

Cash provided by operations before

income tax

$158,000

$158,000

Income tax paid

(34,432)

(15,104)

Cash provided by operations

(cash flow)

$123,568

$142,896

Cash flow advantage of DDB over SL $19,328

(20-25 min.) P 7-71B

Req. 1

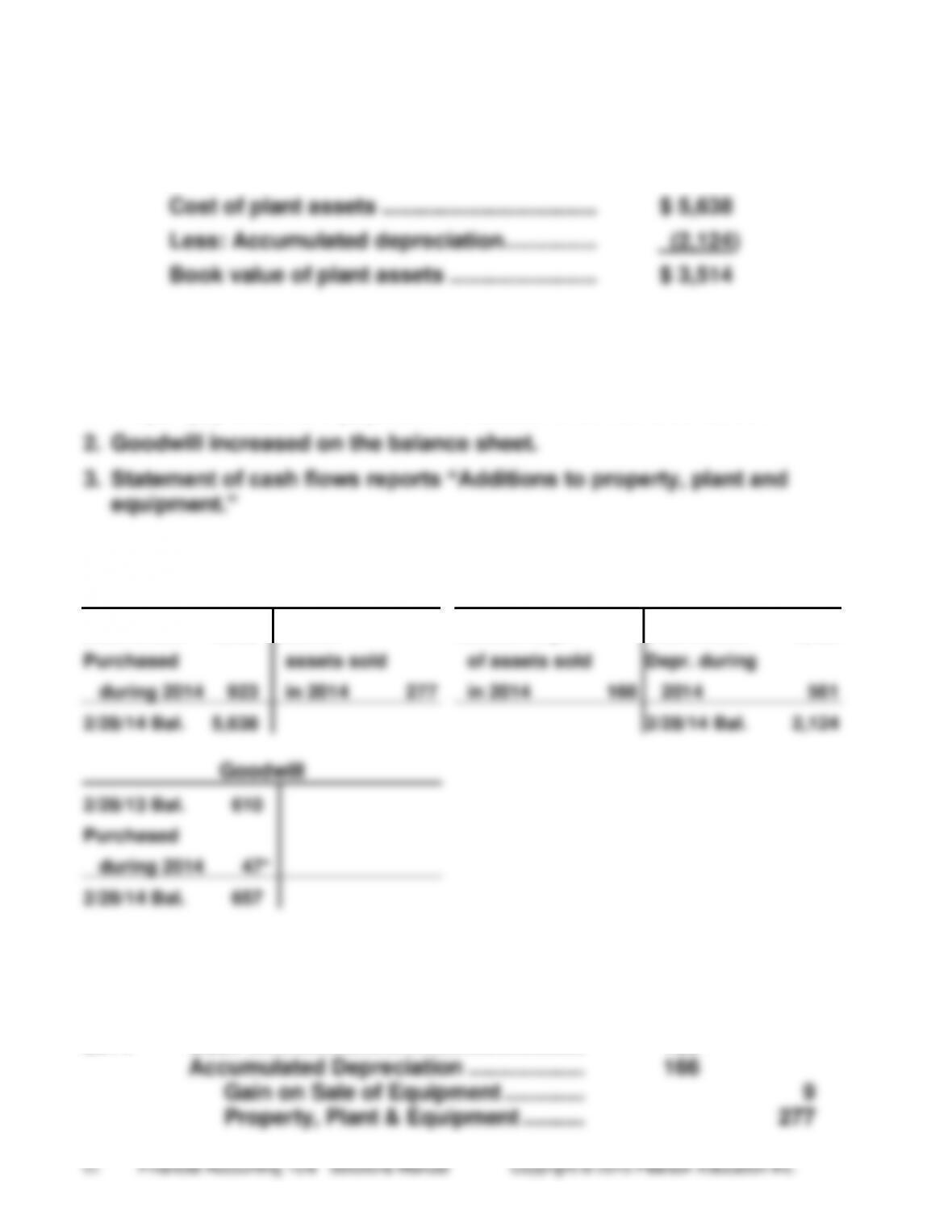

Millions

Cost of plant assets ……………………………..

$ 5,638

Less: Accumulated depreciation ……………

(2,124)

Book value of plant assets ……………………

$ 3,514

Req. 2

Evidences of the purchase of plant assets and goodwill:

1. Property, plant, and equipment increased on the balance sheet.

Req. 3

Property, Plant, and Equipment

Accumulated Depreciation

2/28/13 Bal.

4,992

Cost of

Accum. depr.

2/28/13 Bal.

1,729

Purchased

assets sold

of assets sold

Depr. during

during 2014

923

in 2014

277

in 2014

166

2014

561

2/28/14 Bal.

5,638

2/28/14 Bal.

2,124

2/28/13 Bal.

610

Purchased

during 2014

47*

2/28/14 Bal.

657

(20-30 min.) P 7-72B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Iron Ore ……………………………………………..

2,750,000

Cash……………………………………………..

2,750,000

Iron Ore ……………………………………………..

67,000

Cash……………………………………………..

67,000

Iron Ore …………………………………………….

78,500

Cash……………………………………………..

78,500

Iron Ore …………………………………………….

38,550

Note Payable …………………………………

38,550

Iron Ore Inventory ………………………………

580,125*

Iron Ore ………………………………………..

580,125

Accounts Receivable (38,000 × $37) …….

1,406,000

Sales Revenue ………………………………

1,406,000

Cost of Iron Ore Sold (38,000 x $13.65) ..

518,700

Iron Ore Inventory………………………….

518,700

Operating Expenses …………………………..

412,000

Cash……………………………………………..

412,000

Income Tax Expense (see Req. 2)………..

166,355

Income Tax Payable ………………………

166,355

*$2,750,000 + $67,000 + $78,500 + $38,550 = $2,934,050;

$2,934,050 / 215,000 = $13.65 x 42,500 = $580,125

(continued) P 7-72B

Req. 2

Central Atlantic Energy Company

Income Statement — Iron Ore Mine Project

Year 1

Sales revenue ………………………………………

$1,406,000

Cost of iron ore sold …………………………….

$518,700

Operating expenses ……………………………..

412,000

930,700

Income before tax ………………………………..

475,300

Income tax expense (35%) ……………………

166,355

Net income ………………………………………….

$ 308,945

The Iron Ore Mine project was very profitable. Net income of $308,945 on

sales of $1,406,000 (22%) is outstanding.

Req. 3

Iron ore inventory ($580,125 – $518,700)..

$ 61,425

Iron ore ($2,934,050 – $580,125) ……………

2,353,925

Accounts receivable …………………………….

1,406,000

Income tax payable ………………………………

166,355

Note payable ……………………………………….

38,550

(30-40 min.) P 7-73B

Req. 1

To determine the gain or loss on the sale of a plant asset, compare the

cash received to the asset’s book value, as follows:

Billions

Cash received from sale of asset ………………………….

$ 0.7

Book value of asset sold:

Cost ……………………………………………………………….

$ 1.1

Less: Accumulated depreciation ……………………..

(0.8)

( 0.3)

Gain (Loss) on sale ……………………………………………..

$ 0.4

Req. 2

Balance sheet at December 31, 2014:

Property, plant, and equipment ($4.2 + $1.8 − $1.1) …………..

$ 4.9

Less: Accumulated depreciation ($2.7 + $1.6 − $0.8) …………

(3.5)

Property, plant, and equipment, net (book value) ………………

$ 1.4

Req. 3

Statement of cash flows for 2014:

Cash flows from operating activities:

Net income ($26.2 − $22.0) …………………………………………..

$4.2

Reconciliation of net income to

net cash provided by operations:

Depreciation ………………………………………………………

1.6

Cash flows from investing activities:

Purchases of property, plant, and equipment …………………….

$(1.8)

Sales of property, plant, and equipment …………………………...

0.7

(20-30 min.) P 7-74B

Req. 1

Feb. 2, 2013 Jan. 28, 2012

Net income

$ 986

$ 1,167

÷ Net revenue

÷ $19,279

÷ $18,804

= Net profit

margin ratio

= 5.11%

= 6.21%

Req. 2

Feb. 2, 2013 Jan. 28, 2012

Sales (net revenue)

$19,279

$18,804

÷ Average total assets

÷ $14,027

÷ $13,856

= Asset turnover

= 1.37

= 1.36

Req. 3

Feb. 2, 2013 Jan. 28, 2012

Net income

$ 986

$ 1,167

÷ Average total assets

÷ $14,027

÷ $13,856

= Return on assets

7.03%

8.42%

Req. 4

All of the following contributed to the decrease in ROA during the most

recent year:

(20-30 min.) P 7-75B

Req. 1

(Amounts in millions)

Property & Equipment

Accumulated Depreciation

12/31/13 Bal.

32,009

X =

Cost of

Accum. depr.

= X

12/31/13 Bal.

22,065

Purchased

assets sold

of assets sold

Depr. during

during 2014

3,518

in 2014

in 2014

2014

2,149

12/31/14 Bal.

34,075

12/31/14 Bal.

23,312

X = $1,452, cost of P & Eq. sold

X = $902, accumulated depreciation on

P & Eq. sold

Req. 2

Cost

$1,452

– Acc. Depr.

–902

= Book value of assets sold

$ 550

Book value

= Loss on sale

(continued) P 7-75B

Req. 3

Cash ………………………………………………………………………………

71

Accumulated Depreciation – Prop. & Equipment ……………….

902

Loss on the Sale of Prop. & Equipment …………………………….

479

Property & Equipment …………………………………………………

1,452

Assets decrease, liabilities unaffected, and stockholders’ equity

decreases; revenues unaffected, expenses (losses) increase, and net

income decreases.

The total book value of $550 ($1,452 − $902) is $479 more than the sales

price of $71. This is the same calculation as in Req. 2.

Req. 4

Property & Equipment, net

12/31/13 Bal.

9,944

550

Book value, assets sold

Purchases

3,518

2,149

Depreciation

12/31/14 Bal.

10,763

Challenge Exercises and Problem

(15-20 min.) E 7-76

Millions

Net income under straight-line depreciation ………….

$64

Difference in depreciation for 2015 (year 2 of 8):

Straight line depreciation, as reported ………………

$30

DDB depreciation for year 2 (see below) ……………

45

Increase in depreciation expense ……………………..

15

Decrease in net income ………………………………………..

(15)

Net income Kerusi can expect for 2015

if the company uses DDB depreciation ……………..

$49

DDB depreciation by year:

Millions

Year

1

$240 × 2/8 ……………………………………………………

$60

2

($240 − $60) × 2/8 …………………………………………

45

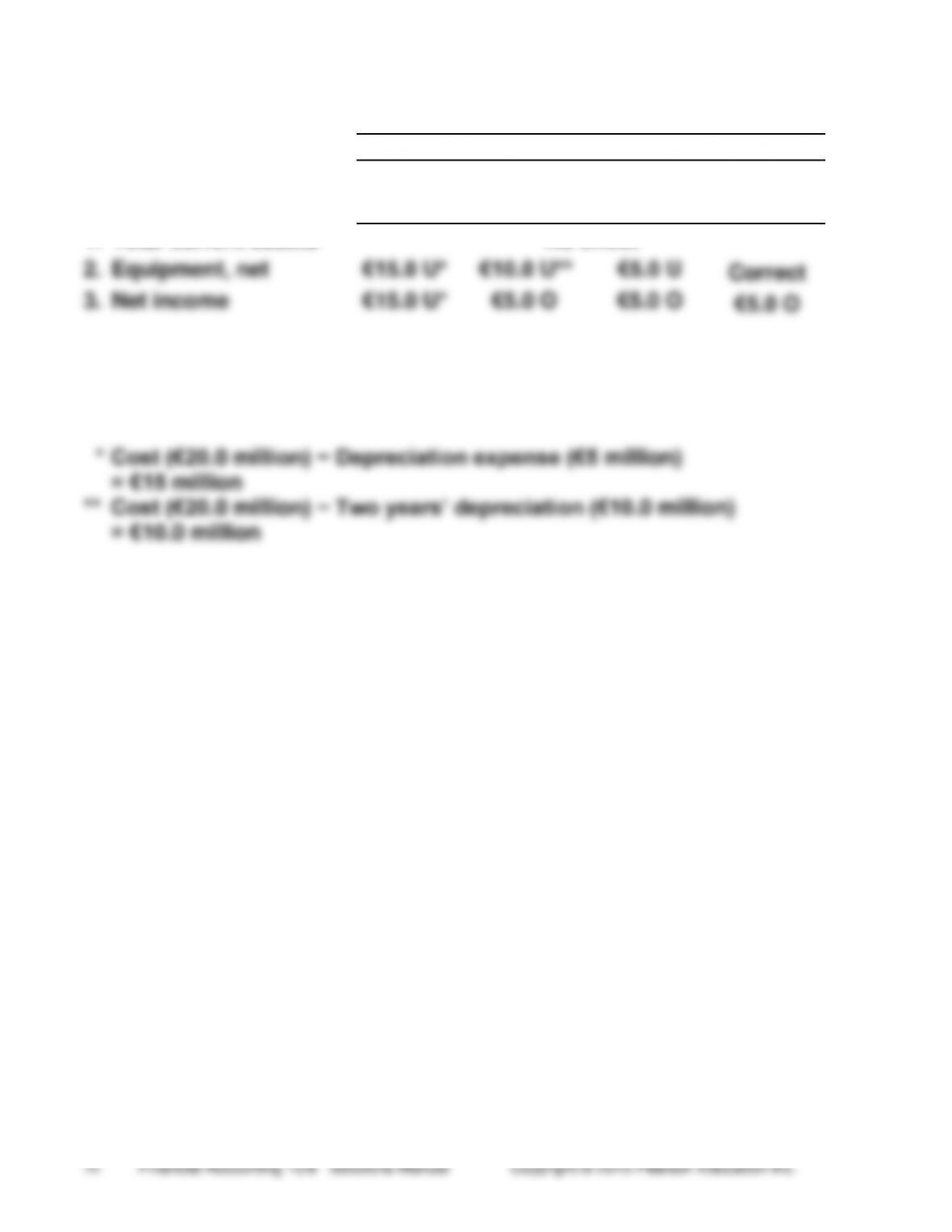

(15-25 min.) E 7-77

Year

1

2

3

4

Millions of Euros (€)

1.

Total current assets

No effect

2.

Equipment, net

€15.0 U*

€10.0 U**

€5.0 U

Correct

3.

Net income

€15.0 U*

€5.0 O

€5.0 O

€5.0 O

_____

U = Understated

O = Overstated

(20-30 min.) P 7-78

(All amounts in millions)

Req.1

Property and Equipment

Bal 5/31/2011 (BS) 33,686

Capital expenditures (SCF) 4,007

134 Impairment (note)

1,395 Original cost of plant and

equipment sold (plug)

Bal.5/31/2012 (BS) 36,164

Accumulated Depreciation

Acc. Depr. on assets sold 1,327

(plug)

18,143 Bal. 5/31/2011 (BS)

2,100 Depr. exp.(note)

18,916 Bal 5/31/2012 (BS)

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Property and Equipment …………………..

4,007

Cash ……………………………………………

4,007

Depreciation Expense ………………………

2,100

Accumulated Depreciation ……………

2,100

Loss on Impairment of Prop & Equip …

134

Property and Equipment ………………

134

Cash (SCF) ………………………………………

74

Accumulated Depreciation ………………..

1,327

Gain on Sale of Prop & Equip …….

6

Property and Equipment ……………

1,395

Decision Cases

(30-45 min.) Decision Case 1

Req. 1

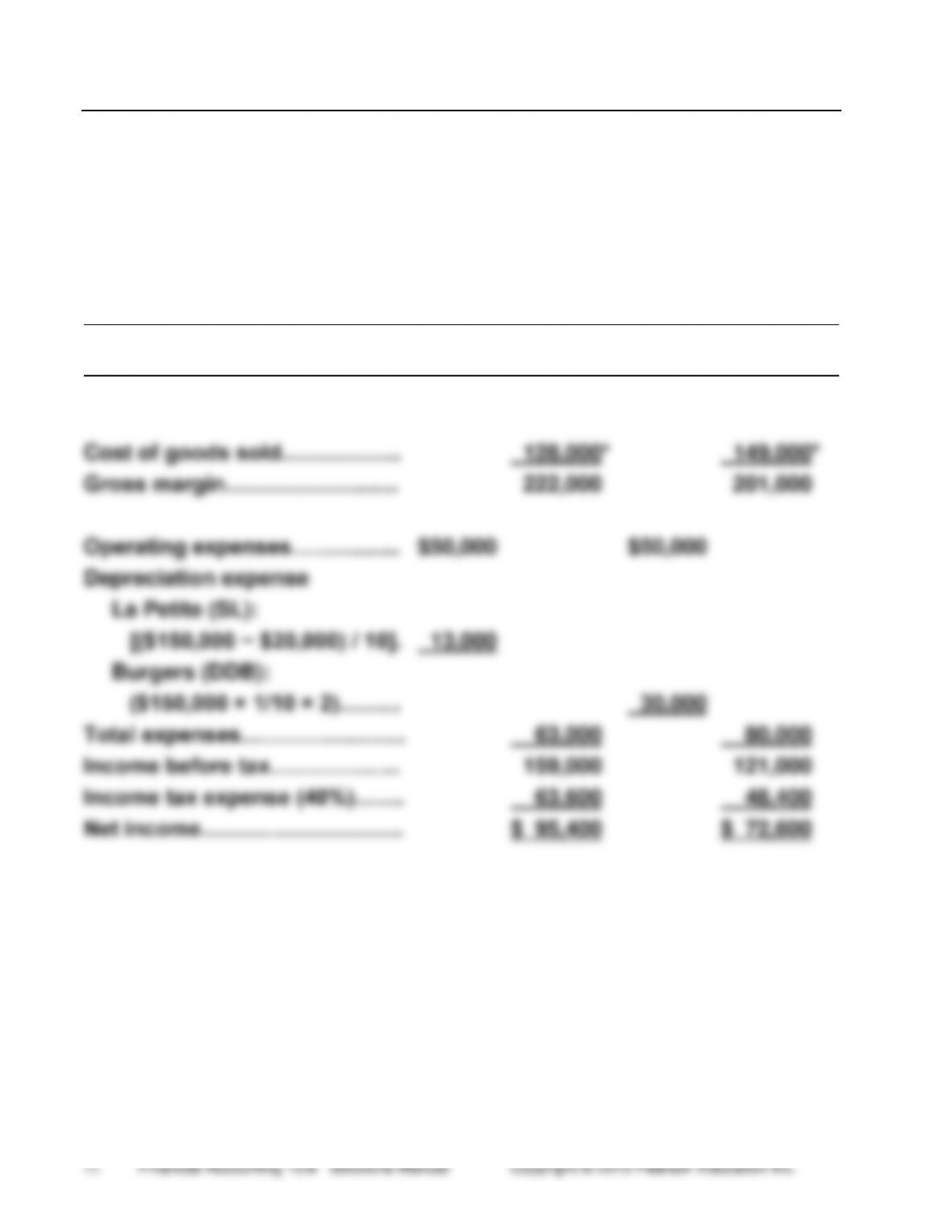

La Petite France Bakery and Burgers Ahoy!

Income Statements

For the Year Ended December 31

ACCOUNT TITLE

La Petite France

(FIFO and SL)

Burgers Ahoy!

(LIFO and DDB)

Sales revenue……………………

$350,000

$350,000

Cost of goods sold……………..

128,000*

149,000*

Gross margin………………….…

222,000

201,000

Operating expenses………….…

$50,000

$50,000

Depreciation expense

La Petite (SL):

[($150,000 − $20,000) / 10].

13,000

Burgers (DDB):

($150,000 × 1/10 × 2)……...

30,000

Total expenses…………………..

63,000

80,000

Income before tax…………….…

159,000

121,000

Income tax expense (40%)…….

63,600

48,400

Net income……………………….

$ 95,400

$ 72,600