Chapter 8 Long-Term Investments & International Operations

8-21

(10-15 min.) E 8-26B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

a.

Equity-Method Investment ……………………….

1,420,000

Cash …………………………………………………..

1,420,000

Purchased equity-method investment.

b.

Equity-Method Investment ($660,000 × .35) .

231,000

Equity-Method Investment Revenue …….

231,000

To record investment revenue.

c.

Cash ($400,000 × .35) ………………………………

140,000

Equity-Method Investment …………………..

140,000

To receive cash dividend on equity-method investment.

(10-15 min.) E 8-27B

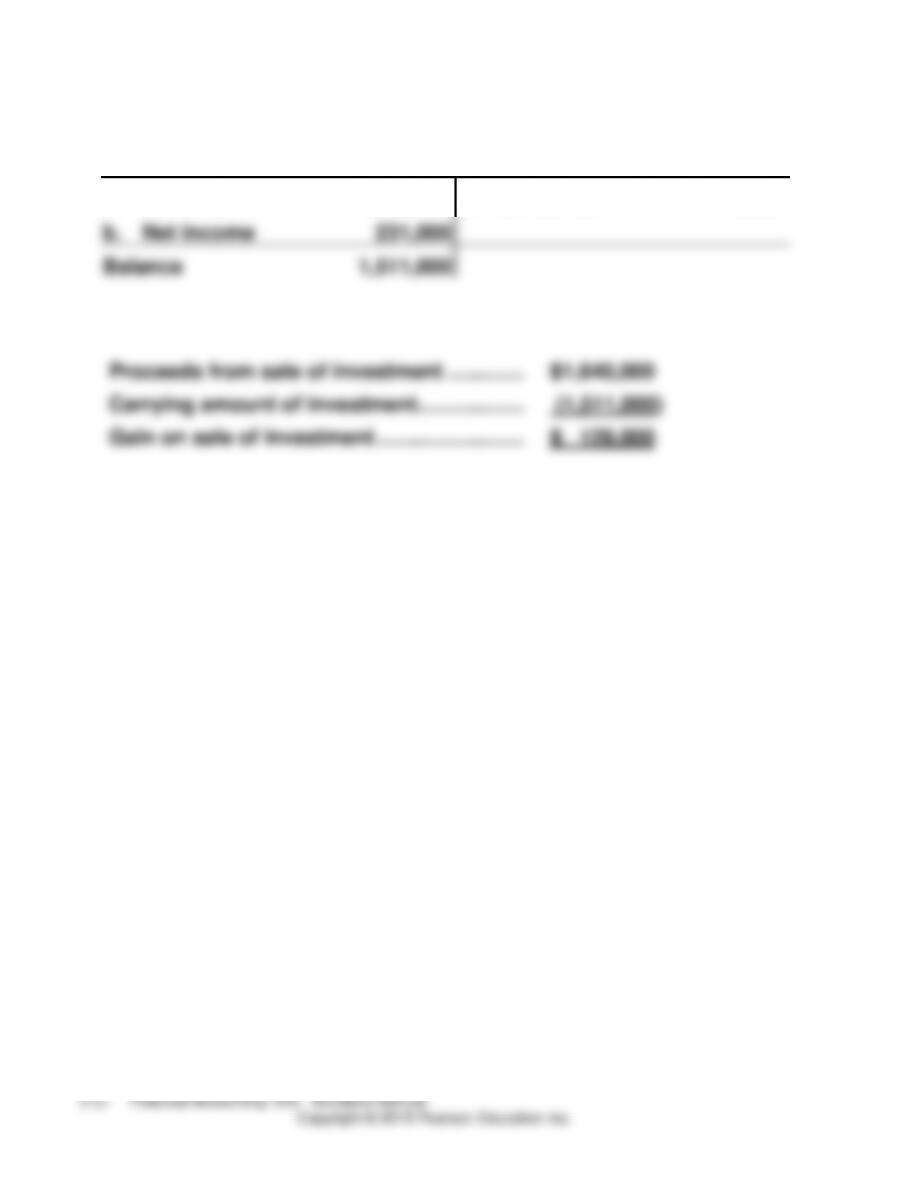

Equity-Method Investment

a.

Purchase

1,420,000

c.

Dividends

140,000

b.

Net income

231,000

Balance

1,511,000

Chapter 8 Long-Term Investments & International Operations

8-23

(15-20 min.) E 8-28B

Req. 1

The equity method is appropriate for a 45% investment in another

company’s common stock. Equity method is used for 20-50%

investments.

Req. 2

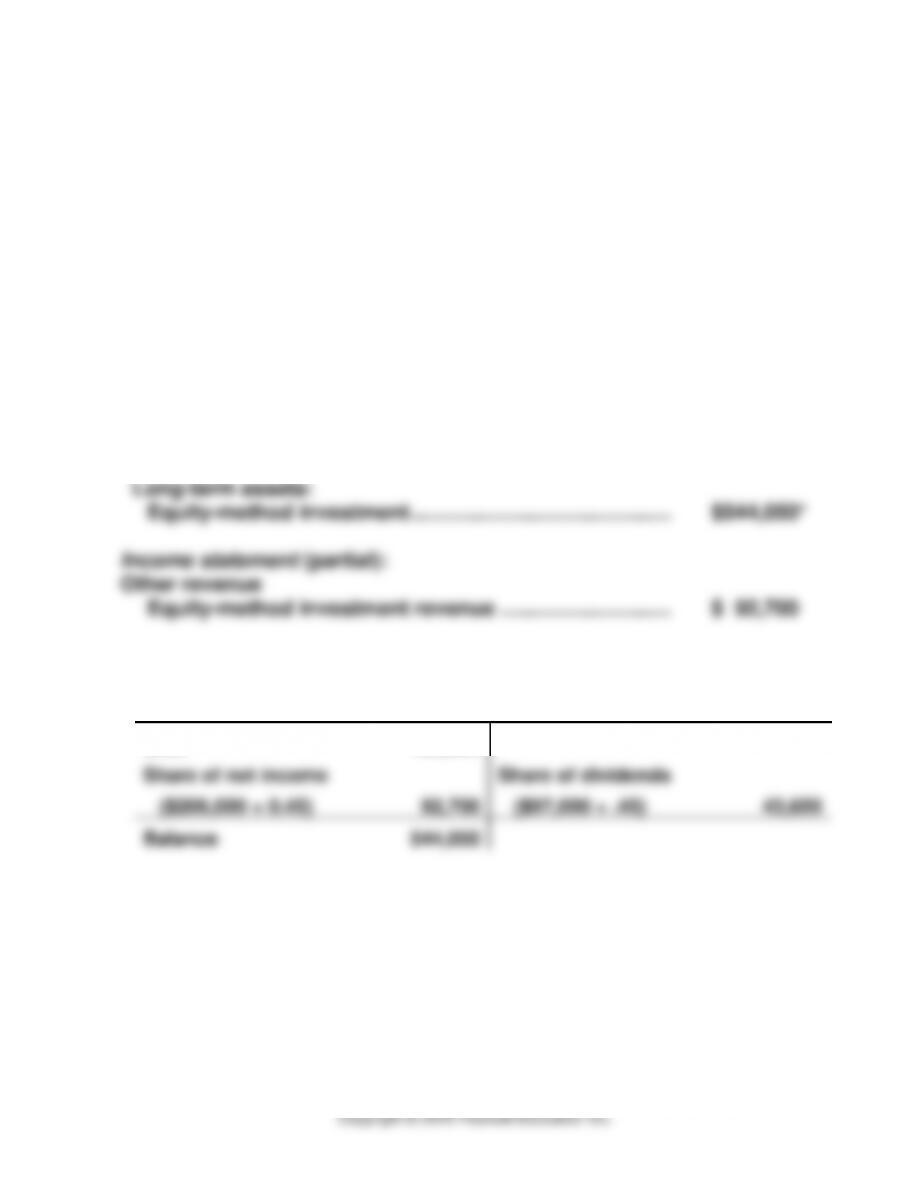

Balance sheet (partial):

ASSETS

Long-term assets:

Equity-method investment ……………………………………..

$544,050*

Income statement (partial):

Other revenue

Equity-method investment revenue ………………………..

$ 92,700

_____

*Explanation:

Equity-Method Investment

Cost

495,000

Share of net income

Share of dividends

($206,000 × 0.45)

92,700

($97,000 × .45)

43,650

Balance

544,050

(20-25 min.) E 8-29B

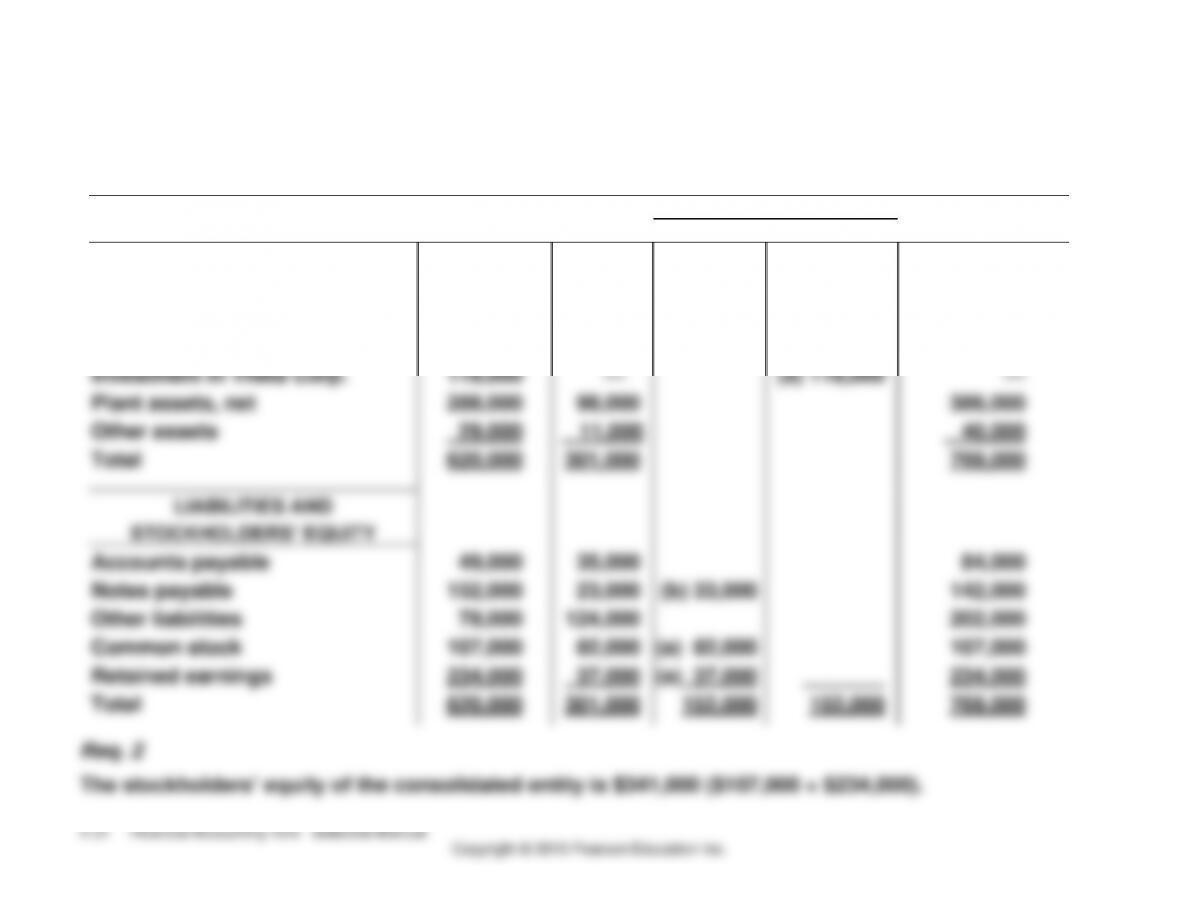

Req. 1 (consolidation work sheet and balance sheet)

Theta

ELIMINATION

CONSOLIDATED

ASSETS

Zeta, Inc.

Corp.

DEBIT

CREDIT

BALANCE SHEET

Cash

48,000

18,000

66,000

Accounts receivable, net

82,000

58,000

140,000

Note receivable from Zeta

—

33,000

(b) 33,000

—

Inventory

54,000

83,000

137,000

Investment in Theta Corp.

119,000

—

(a) 119,000

—

Plant assets, net

288,000

98,000

386,000

Other assets

29,000

11,000

40,000

Total

620,000

301,000

769,000

LIABILITIES AND

STOCKHOLDERS’ EQUITY

Accounts payable

49,000

35,000

84,000

Notes payable

152,000

23,000

(b) 33,000

142,000

Other liabilities

78,000

124,000

202,000

Common stock

107,000

82,000

(a) 82,000

107,000

Retained earnings

234,000

37,000

(a) 37,000

_______

234,000

Total

620,000

301,000

152,000

152,000

769,000

Req. 2

The stockholders’ equity of the consolidated entity is $341,000 ($107,000 + $234,000).

Chapter 8 Long-Term Investments & International Operations

8-25

(15-20 min.) E 8-30B

Req. 1

Rentex should use the amortized-cost method.

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Sept.

30

Held-to-Maturity Investment in Bonds

($80,000 × .96) ……………………………………….

76,800

Cash …………………………………………………

76,800

To purchase bond investment.

Dec.

31

Interest Receivable

($80,000 × .07 × 3/12) ………………………………

1,400

Interest Revenue ……………………………….

1,400

To accrue interest revenue.

31

Held-to-Maturity Investment in Bonds

[($80,000 − $76,800) / 60 mo. × 3 mo.] ………

160

Interest Revenue …………………………..…..

160

To amortize discount on bond investment.

Req. 3

Balance sheet (partial)

ASSETS

Current:

Interest receivable …………………………………………………

$ 1,400

Long-term:

Held-to-maturity investment in bonds

($76,800 + $160) …………………………………………………….

$76,960

(10-20 min.) E 8-31B

$20,922.22 EXCEL formula =PV(1.5%,10,-400,-20000,0)

(10-15 min.) E 8-32B

Spanish Subsidiary:

EUROS

EXCHANGE

RATE

DOLLARS

Assets

400,000

$1.34

$536,000

Liabilities

300,000

1.34

$402,000

Stockholders’ equity:

Common stock

45,000

1.02

45,900

Retained earnings

55,000

1.17

64,350

Accumulated other

comprehensive income:

Foreign-currency

translation adjustment

23,750

400,000

$536,000

Chapter 8 Long-Term Investments & International Operations

8-27

(15-20 min.) E 8-33B

Creative Cupcakes

Statement of Cash Flows (partial)

Fiscal Year 2014

Millions

Cash flows from investing activities:

Capital expenditures ………………………………………………

$ (8.5)

Sale of property, plant, and equipment …………………….

5.8

Sale of other businesses ………………………………………..

1.9

Purchase of long-term investments …………………………

(12.1)

Sale of investments …………………………..……………………

4.3

Net cash (used) in investing activities …………………..

$ (8.6)

Based on Creative Cupcake’s investing activities, it appears that the

(20-25 min.) E 8-34B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Cash ………………………………………………………

2,508,000

Notes Receivable ……………………………….

2,508,000

Short-Term Investments ………………………….

3,031,000

Cash …………………………………………………

3,031,000

Cash ………………………………………………………

419,000

Accumulated Depreciation ………………………

3,681,000

Equipment …………………………………………

4,100,000

Cash ………………………………………………………

421,000

Investments ………………………………………

410,000

Gain on Sale of Investments ……………….

11,000

Property and Equipment ………………………….

326,800

Cash …………………………………………………

326,800

Chapter 8 Long-Term Investments & International Operations

8-29

Quiz

Q8-35

c [(800 × $71) + (100 × $11) + (300 × $24) = $65,100]

Q8–36

d [(800 x $1.90) + (100 x $1.30) + (300 x $1.10) = $1,980]

Q8–37

Cash (800 × $67) …………………………………

53,600

Investment in AFSS (800 × $56) ………..

44,800

Gain on Sale of Investment in AFSS ….

8,800

Q8–38

b

Q8–39

a

Q8–40

b

Q8–41

a ($120,000 × .09) = $10,800

Q8–42

c [($120,000 × .09) − ($124,800 − $120,000) / 5 = $9,840]

Q8–43

d ($5,000 x .677)

Q8–44

b

Q8–45

c =PV(4%,8,-150,-5000,0)

Q8–46

a

Problems

(20-30 min.) P 8-47A

Req. 1

Current fair value is used to account for the available-for-sale

investment in Detroit, Inc., because the investor expects to sell the

(continued) P 8-47A

Req. 2

Balance sheet:

ASSETS

Total current assets …………………………..……………………….

$ XXX

Long-term assets:

Equity-method investment ………………………………………..

551,250*

Investment in AFSS ………………………………………………….

31,600

Property, plant, and equipment, net …………………………….

XXX

STOCKHOLDERS’ EQUITY

Common stock …………………………..………………………………

$ XXX

Retained earnings ………………………………………………………

XXX

Accumulated other comprehensive income:

Unrealized (loss) on investment in AFSS

[$31,600 − (800 × $41.75)] …………………………………………

(1,800)

Income statement:

Income from operations ……………………………………………..

$ XXX

Other revenue:

Equity-method investment revenue ($475,000 × .35) ….

166,250

Dividend revenue (800 × $.39) …………………………………..

312

Net income ………………………………………………………………..

XXX

Statement of other comprehensive income:

Unrealized (loss) on investment in AFSS …………………..

$ (1,800)

Balance

551,250

Chapter 8 Long-Term Investments & International Operations

8-33

(45-60 min.) P 8-48A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Mar.

16

Investment in AFSS (2,700 × $12.00) ……………

32,400

Cash ………………………………………………..

32,400

Purchased investment.

May

21

Cash (2,700 × $0.80) ………………………………..

2,160

Dividend Revenue …………………………….

2,160

Received cash dividend.

Aug.

17

Cash ………………………………………………………

65,000

Equity-Method Investment …………………

65,000

Received cash dividend on equity-method

investment.

Dec.

31

Equity-Method Investment

($612,000 × .30) ……………………………………….

183,600

Equity-Method Investment Revenue …..

183,600

To record investment revenue.

31

Allowance to Adjust Investment in AFSS

to Market ($39,000 − $32,400) …………………..

6,600

Unrealized Gain on Investment in AFSS

6,600

Adjusted investment to market value.

(continued) P 8-48A

Req. 2

Equity-Method Investment

Jan.

1

Balance

581,000

Aug.

17

Dividends

65,000

Dec.

31

Net income

183,600

Dec.

31

Balance

699,600

Req. 3

(20-30 min.) P 8-49A

Req. 1

(35-45 min.) P 8-50A

Req. 1

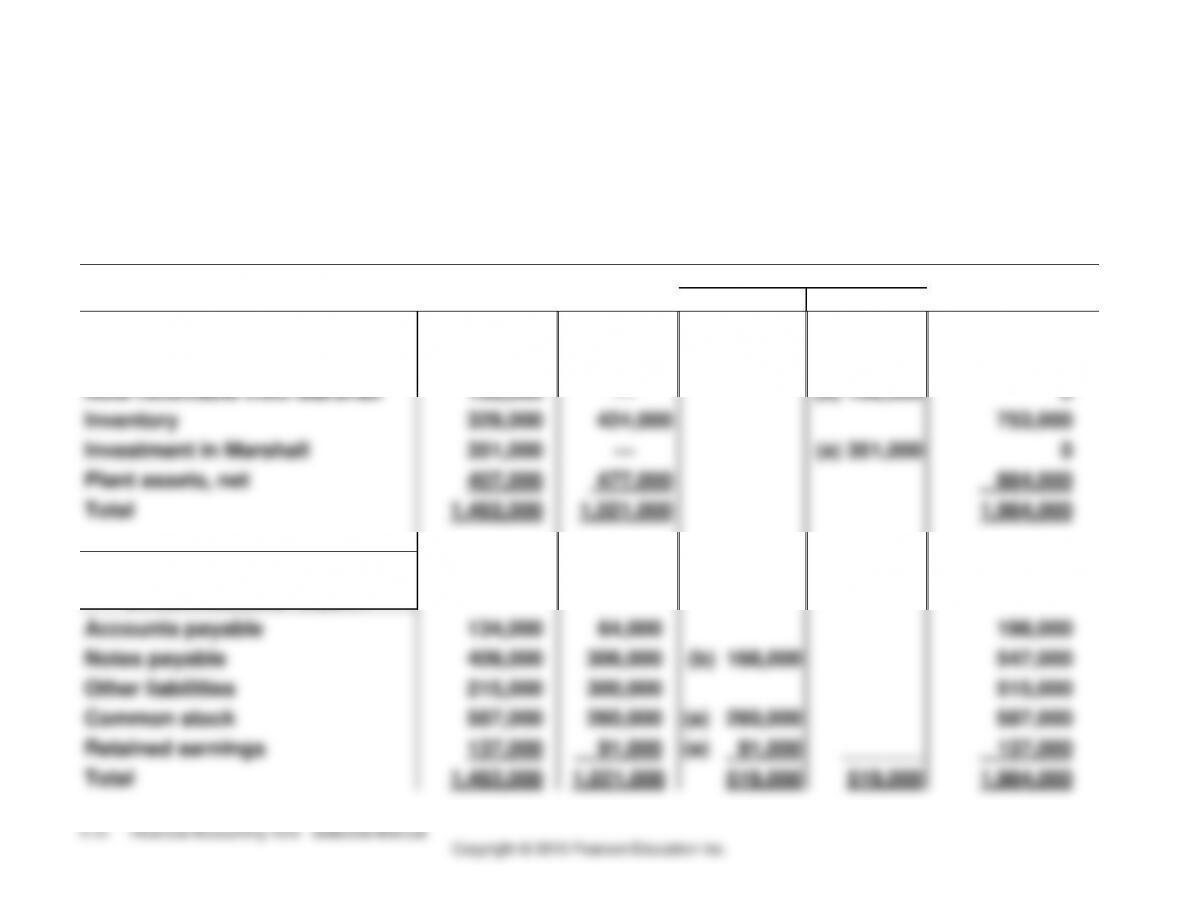

Jackson Corp.

Consolidation Work Sheet

September 30, 2014

ELIMINATIONS

CONSOLIDATED

ASSETS

JACKSON

MARSHALL

DEBIT

CREDIT

AMOUNTS

Cash

48,000

32,000

80,000

Accounts receivable, net

179,000

88,000

267,000

Note receivable from Marshall

168,000

—

(b) 168,000

0

Inventory

329,000

424,000

753,000

Investment in Marshall

351,000

—

(a) 351,000

0

Plant assets, net

407,000

477,000

884,000

Total

1,482,000

1,021,000

1,984,000

LIABILITIES AND

STOCKHOLDERS’ EQUITY

Accounts payable

134,000

64,000

198,000

Notes payable

409,000

306,000

(b) 168,000

547,000

Other liabilities

215,000

300,000

515,000

Common stock

587,000

260,000

(a) 260,000

587,000

Retained earnings

137,000

91,000

(a) 91,000

_______

137,000

Total

1,482,000

1,021,000

519,000

519,000

1,984,000

Chapter 8 Long-Term Investments & International Operations

8-37

(45-60 min.) P 8-51A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Jan.

1

Held-to–Maturity Investment in Bonds

($2,500,000 × 1.16) ………………………………..

2,900,000

Cash ……………………………………………….

2,900,000

To purchase bond investment.

July

1

Cash ($2,500,000 × .06 × 6/12) ……………….

75,000

Interest Revenue ……………………………..

75,000

To receive semiannual interest.

1

Interest Revenue ………………………………….

50,000

Held-to-Maturity Investment in Bonds

[($2,900,000 − $2,500,000) / 48*] x 6 ……

50,000

To amortize premium on bond

investment.

Req. 2

Oct.

31

Interest Receivable

($2,500,000 × .06 × 4/12) …………………………

50,000

Interest Revenue ………………………………

50,000

To accrue interest revenue.

31

Interest Revenue …………………………………..

33,333

Held-to-Maturity Investment in Bonds

[($2,900,000 − $2,500,000) / 48*] x 4 …….

33,333

To amortize premium on bond investment.

(continued) P 8-51A

Req. 3

Balance sheet at October 31, 2014:

Current assets:

Interest receivable ……………………………………………

$ 50,000

Long-term assets:

Held-to-maturity investment in bonds

($2,900,000 − $50,000 − $33,333) ………………………..

2,816,667

Income statement for the year ended October 31, 2014:

Other revenues:

Interest revenue ($75,000 − $50,000 + $50,000 − $33,333) ……..

$41,667

Chapter 8 Long-Term Investments & International Operations

8-39

(20-25 min.) P 8-52A

Req. 1

Investment Opportunity A

Year

Cash

Flow

x

Factor

=

PV of

Cash Flow

1

$14,000

x

.893

=

$12,502

2

8,000

X

.797

=

6,376

3

5,000

X

.712

=

3,560

$27,000

$22,438

Investment Opportunity B

(20-25 min.) P 8-53A

Req. 1

This situation will generate a positive translation adjustment, which is

YEN

EXCHANGE

RATE

DOLLARS

Assets

515,000,000

$.0107

$5,510,500

Liabilities

145,000,000

.0107

$1,551,500

Stockholders’ equity:

Common stock

18,000,000

.0092

165,600

Retained earnings

352,000,000

.0095

3,344,000

Accumulated other

comprehensive income:

Foreign-currency

translation adjustment

449,400

515,000,000

$5,510,500

The foreign currency translation adjustment is reported in accumulated

other comprehensive income in stockholders’ equity on the balance sheet