Chapter 12

The Statement of Cash Flows

Short Exercises

(10 min.) S 12-1

The statement of cash flows helps investors and creditors:

a. Predict future cash flows by reporting past cash receipts and

(10-15 min.) S 12-2

DATE: _______________

TO: Managers of Kobe Inc.

FROM: Student Name

SUBJECT: Purposes of the statement of cash flows

The statement of cash flows is designed to help predict the future cash

flows of a business. The statement of cash flows measures past cash

flows, which are a reasonably good predictor of future cash flows. Net

(5-10 min) S 12-3

Three things that could cause operating cash flows to be positive (under

the indirect method) are:

1. Increase in net income

(15-30 min.) S 12-4

DATE: _______________

TO: Managers of Bayside Inns

FROM: Student Name

SUBJECT: Assessment of 2014 and Outlook for the Future

2014 was not a good year. Most of the increase in net income resulted

from the gain on the insurance proceeds from fire damage to a building,

which means that normal operations were not very profitable. This is

confirmed by the increase in receivables, which hints that collections

are lagging.

(continued) S 12-4

Financing activities provided a net cash inflow, which is normal.

(5-10 min.) S 12-5

Cash flows from operating activities:

Net income …………………………………………………………………

$76,000

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense ……………………………………………..

12,000

Loss on sale of land ………………………………………………..

3,100

Increase in accounts receivable, inventory,

and prepaid expenses ($59,000 − $56,000) ……………

(3,000)

Increase in current liabilities ($45,000 − $41,000) ………

4,000

Net cash provided by operating activities …………………….

$92,100

(10 min.) S 12-6

O−

a.

Decrease in accrued

O+

h.

Increase in accounts

liabilities

payable

O+

b.

Net income

O+

i.

Decrease in accounts

O+

c.

Decrease in prepaid

receivable

expense

O−

j.

Gain on sale of

N

d.

Collection of cash

building

from customers

O+

k.

Loss on sale of land

I

e.

Purchase of

O+

l.

Depreciation expense

equipment

O−

m.

Increase in inventory

N

f.

Retained earnings

F

n.

Issuance of common

F

g.

Payment of dividends

stock

(10 min.) S 12-7

Adams Corporation

Statement of Cash Flows (partial)

Year ended June 30, 2014

Cash flows from operating activities:

Net income …………………………………………………..

$102,000*

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense ……………………………….

$12,000

Increase in current assets other than

cash ……………………………………………………

(63,000)

Increase in current liabilities …………………….

20,100

(30,900)

Net cash provided by operating activities ………

$71,100

_____

*$376,000 − $198,000 − $64,000 − $12,000 = $102,000

(15 min.) S 12-8

Adams Corporation

Statement of Cash Flows

Year ended June 30, 2014

Cash flows from operating activities:

Net income ………………………………………………….

$ 102,000*

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense ………………………………

$12,000

Increase in current assets other than

cash ……………………………………………………

(63,000)

Increase in current liabilities …………………….

20,100

(30,900)

Net cash provided by operating activities ……..

71,100

Cash flows from investing activities:

Purchase of equipment ………………………………..

$(37,000)

Proceeds from sale of land …………………………..

28,000

Net cash used for investing activities ……………

(9,000)

Cash flows from financing activities:

Proceeds from issuance of common stock ……

$ 24,000

Payment of note payable ………………………………

(37,000)

Payment of dividends …………………………………..

(6,400)

Purchase of treasury stock …………………………..

(8,000)

Net cash used for financing activities ……………

(27,400)

Net increase in cash …………………………………………

$ 34,700

_____

*$376,000 − $198,000 − $64,000 − $12,000 = $102,000

(10 min) S 12-9

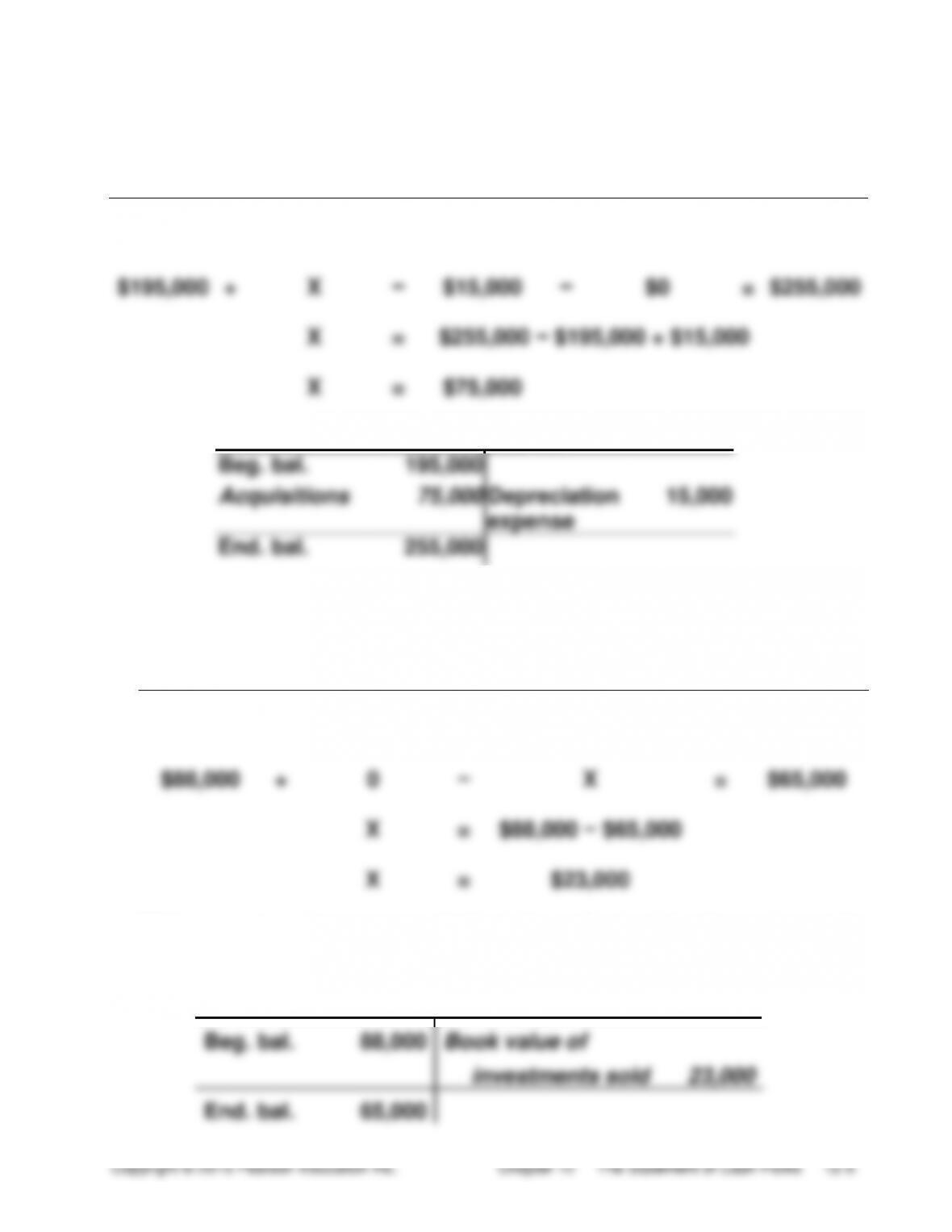

a. Acquisitions of plant assets = $75,000, as follows:

Plant Assets, net

Beg.

+

Acquisitions

−

Depreciation

−

Book value of

=

End.

bal.

assets sold

bal.

$195,000

+

X

−

$15,000

−

$0

=

$255,000

X

=

$255,000 − $195,000 + $15,000

X

=

$75,000

Plant Assets, net

Beg. bal.

195,000

Acquisitions

75,000

Depreciation

expense

15,000

End. bal.

255,000

b. Proceeds from the sale of long-term investments = $23,000, as

follows:

Long-term investments

Beg. bal.

+

Purchases

−

Book value of

=

End. bal.

investments sold

$88,000

+

0

−

X

=

$65,000

X

=

$88,000 − $65,000

X

=

$23,000

With no gain or loss, proceeds from the sale must be the same as the

book value of the investments sold, $23,000.

Long-Term Investments

Beg. bal.

88,000

Book value of

investments sold

23,000

End. bal.

65,000

(15 min.) S 12–10

a. New borrowing on long-term notes payable = $9,000 ($75,000 −

$66,000)

c. Payment (and declaration) of dividends = $151,000, as follows:

Beginning

Net

income

Dividend

declarations

Ending

Retained

+

−

=

Retained

Earnings

Earnings

$297,000

+

$163,000

−

X

=

$309,000

X

=

$297,000 + $163,000 − $309,000

X

=

$151,000

Retained Earnings

Beg. bal.

297,000

Dividends declared

(paid)

151,000

Net income

163,000

End. bal.

309,000

(15 min.) S 12-11

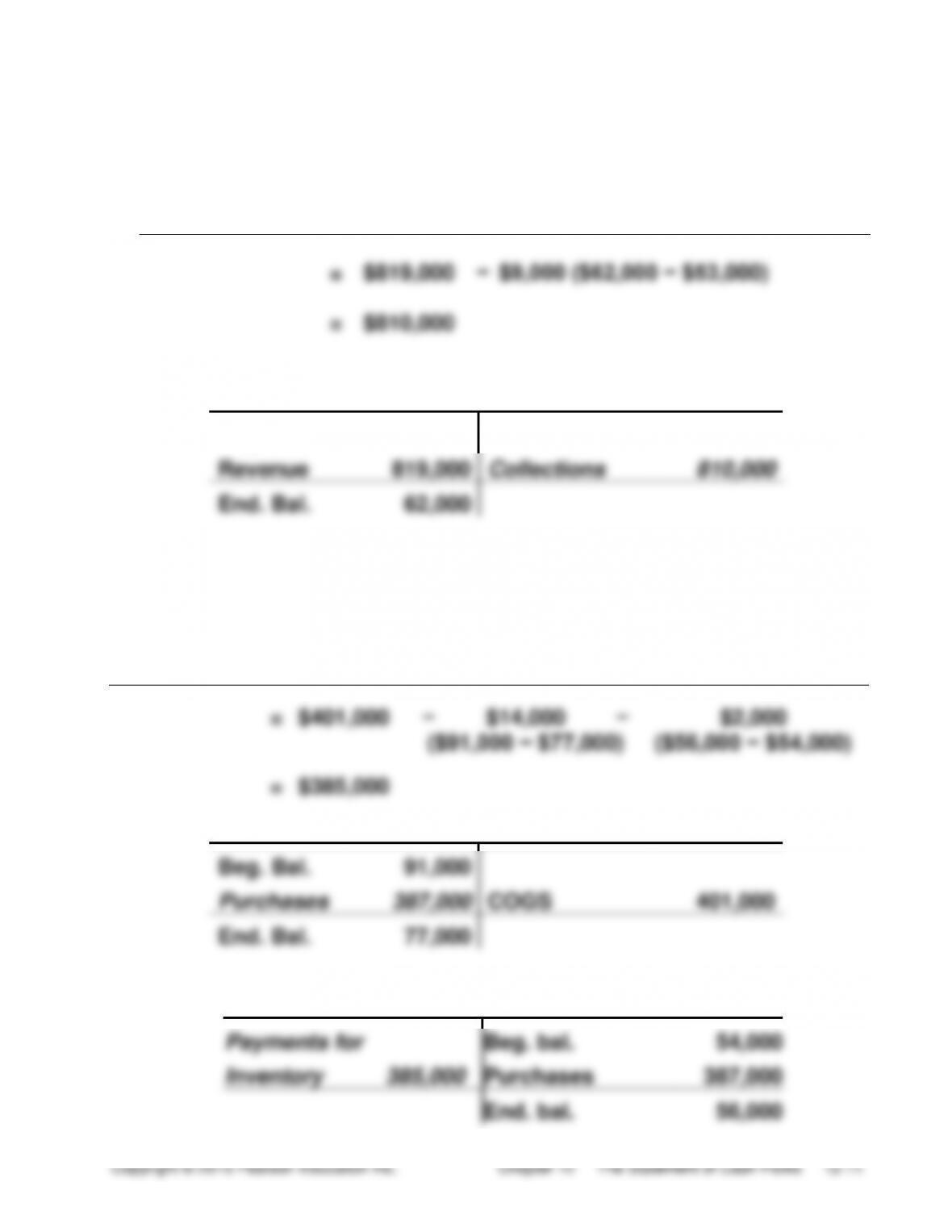

a. Collections from customers = $810,000, as follows:

Collections

=

Service

−

Increase in Accounts Receivable

from customers

Revenue

=

$819,000

−

$9,000 ($62,000 − $53,000)

=

$810,000

Accounts Receivable

Beg. Bal.

53,000

Revenue

819,000

Collections

810,000

End. Bal.

62,000

b. Payments for inventory = $385,000, as follows:

Payments for

inventory

Decrease in

Inventory

Increase in

Accounts Payable

=

COGS

−

−

=

$401,000

−

$14,000

−

$2,000

($91,000 − $77,000)

($56,000 − $54,000)

=

$385,000

Inventory

Beg. Bal.

91,000

Purchases

387,000

COGS

401,000

End. Bal.

77,000

Accounts Payable

Payments for

Beg. bal.

54,000

Inventory

385,000

Purchases

387,000

End. bal.

56,000

(10-15 min.) S 12-12

a. Payments to employees = $56,000, as follows:

Payments to

=

Salary

−

Increase in

employees

Expense

Salary Payable

=

$60,000

−

$4,000

($26,000 − $22,000)

=

$56,000

Salary Payable

Payments to

Beg. bal.

22,000

Employees

56,000

Salary expense

60,000

End. bal.

26,000

b. Payments for other expenses = $184,000, as follows:

Payments

of other

expenses

Other

Expenses

Increase in

Decrease in

=

+

Prepaid

+

Accrued

Expenses

Liabilities

=

$180,000

+

$1,000

+

$3,000

($17,000 − $16,000) ($16,000 − $13,000)

=

$184,000

(15 min.) S 12–13

McCracken Horse Farms, Inc.

Statement of Cash Flows

Year 2014

Cash flows from operating activities:

Collections from customers ………………………

$ 640,000

Payments to suppliers and employees……….

(465,000)

Net cash provided by operating activities …..

$175,000

Cash flows from investing activities:

Purchase of equipment ……………………………..

$(119,000)

Net cash used for investing activities…………

(119,000)

Cash flows from financing activities:

Issued note payable to borrow money ……….

$ 25,000

Payment of dividends ……………………………….

(37,000)

Net cash used for financing activities ………..

(12,000)

Net increase in cash ……………………………………..

$ 44,000

Cash balance, beginning ……………………………….

58,000

Cash balance, ending …………………………..……….

$102,000

(5 min.) S 12-14

Phoenix Golf Club, Inc.

Statement of Cash Flows (partial)

Year ended September 30, 2014

Cash flows from operating activities:

Collections from customers …………………………...

$ 263,000

Payments to suppliers ……………………………………

(124,000)

Payments to employees …………………………………

(78,000)

Payment of income tax …………………………………..

(19,000)

Net cash provided by operating activities ……….

$42,000

(15 min.) S 12-15

Phoenix Golf Club, Inc.

Statement of Cash Flows

Year ended September 30, 2014

Cash flows from operating activities:

Collections from customers …………………………...

$ 263,000

Payments to suppliers ……………………………………

(124,000)

Payments to employees …………………………………

(78,000)

Payment of income tax …………………………………..

(19,000)

Net cash provided by operating activities ………..

$42,000

Cash flows from investing activities:

Purchase of equipment …………………………………..

$(29,000)

Proceeds from sale of land ……………………………..

46,000

Net cash provided by investing activities ………..

17,000

Cash flows from financing activities:

Proceeds from issuance of common stock ………

$ 30,000

Payment of note payable ………………………………..

(36,000)

Payment of dividends …………………………………….

(12,000)

Purchase of treasury stock …………………………….

(5,400)

Net cash used for financing activities ……………..

(23,400)

Net increase in cash …………………………………………..

$35,600

Exercises

(10-15 min.) E 12-16A

I–

a.

Purchase of long-term

F–

k.

Payment of long-term debt

investment

O+

l.

Increase in salary payable

F+

b.

Issuance of long-term note

payable to borrow cash

I+

m.

Cash sale of land

O–

c.

Increase in prepaid

I+

n.

Sale of long-term

expenses

investment

O–

d.

Decrease in accrued

I–

o.

Acquisition of building by

liabilities

cash payment

O+

e.

Loss on the sale of

O+

p.

Net income

equipment

F+

q.

Issuance of common stock

O+

f.

Decrease in accounts

for cash

receivable

F–

r.

Payment of cash dividend

O+

g.

Depreciation of equipment

NIF

s.

Acquisition of equipment

O+

h.

Increase in accounts

by issuance of note

payable

payable

O+

i.

Amortization of intangible

assets

F–

j.

Purchase of treasury stock

(5-10 min.) E 12-17A

a.

Financing

h.

Investing

b.

Financing

i.

Financing

c.

Investing

j.

Financing

d.

Operating

k.

Operating

e.

Operating

l.

Operating

f.

Investing

m.

Noncash investing and

financing

g.

Investing

(10-15 min.) E 12-18A

Cash flows from operating activities:

Net income ……………………………………………….

$19,000

Adjustments to reconcile net income to

net cash used for operating activities:

Depreciation expense ………………………….

$ 7,000

Gain on sale of land …………………………….

(8,000)

Increase in current assets other

than cash ………………………………………….

(29,000)

Increase in current liabilities ………………..

6,000

(24,000)

Net cash used for operating activities ………..

$ (5,000)

Operating cash flow is weak, as shown by the negative net cash flows

(15-20 min.) E 12-19A

Cash flows from operating activities:

Net income ……………………………………………………

$17,000

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense ……………………………..

$ 17,000

Increase in accounts receivable ……………….

(3,000)

Increase in inventory ………………………………

(1,500)

Increase in accounts payable …………………..

62,000

Decrease in accrued liabilities …………………

(4,000)

70,500

Net cash provided (used) by operating

activities …………………………..…………………………...

$87,500

Lane Fur Traders does not have trouble collecting receivables or selling

(20-30 min.) E 12-20A

Req. 1

Tullis Travel Products, Inc.

Statement of Cash Flows

Year Ended December 31, 2014

Cash flows from operating activities:

Net income …………………………………………………..

$ 38,300

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense ………………………………

$ 28,000

Decrease in accounts receivable ………………

19,000

Increase in inventory ……………………………….

(10,000)

Increase in prepaid expenses …………………..

(500)

Increase in accounts payable ……………………

12,900

Increase in accrued liabilities ……………………

9,000

58,400

Net cash provided by operating activities ….

96,700

Cash flows from investing activities:

Acquisition of plant assets …………………………...

$(65,000)

Proceeds from sale of land …………………………...

17,000

Net cash used for investing activities………..

(48,000)

Cash flows from financing activities:

Proceeds from issuance of common stock …….

$ 46,000

Payment of long-term note payable ………………..

(17,000)

Payment of dividends ……………………………………

(8,000)

Net cash provided by financing activities ….

21,000

Net increase in cash …………………………………………

$ 69,700

Cash balance, December 31, 2013 …………………….

48,600

Cash balance, December 31, 2014 …………………….

$118,300

Noncash investing and financing activities:

Acquisition of plant assets by issuing note payable

$ 30,000