Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–41

(25-35 min.) P 11-54A

Req. 1

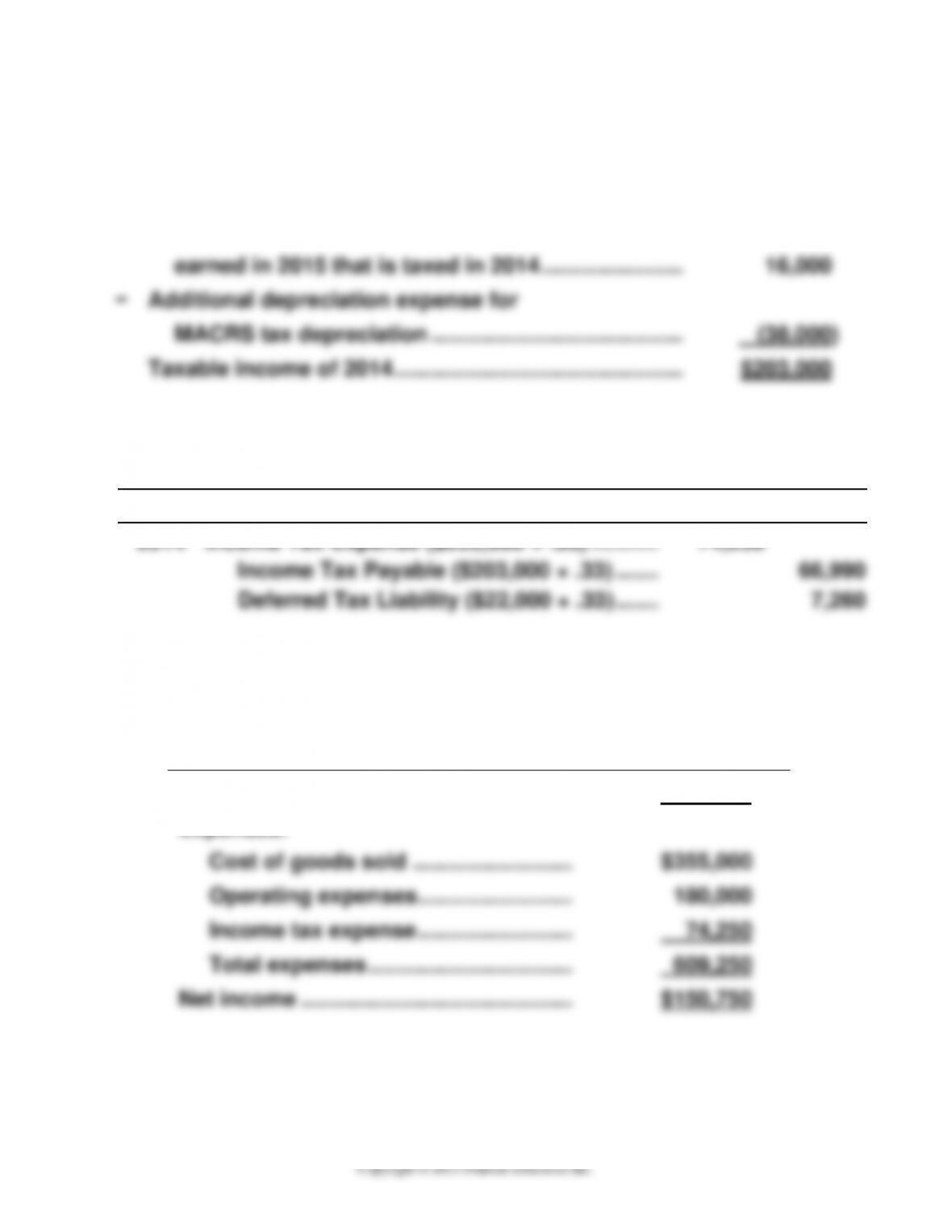

Pretax accounting income of 2014 ………………………..

$225,000

+

Additional taxable income for income

earned in 2015 that is taxed in 2014 …………………..

16,000

−

Additional depreciation expense for

MACRS tax depreciation …………………………………..

(38,000)

Taxable income of 2014 ………………………………………..

$203,000

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Income Tax Expense ($225,000 × .33) ………..

74,250

Income Tax Payable ($203,000 × .33) …….

66,990

Deferred Tax Liability ($22,000 × .33) …….

7,260

Req. 3

Kaska Publications, Inc.

Income Statement

Year Ended December 31, 2014

Total revenue ………………………………….

$760,000

Expenses:

Cost of goods sold ……………………..

$355,000

Operating expenses …………………….

180,000

Income tax expense …………………….

74,250

Total expenses …………………………...

609,250

Net income ……………………………………..

$150,750

(20-30 min.) P 11-55B

Req. 1

Midler Cosmetics, Inc.

Income Statement

Year Ended December 31, 2014

Revenues:

Sales revenue ………………………………………………….

$628,000

Dividend revenue …………………………………………….

16,000

Gain on lawsuit settlement ……………………………….

10,400

Total revenues …………………………..…………………

654,400

Expenses and losses:

Cost of goods sold ………………………………………….

$314,200

Selling expenses ……………………………………………..

93,000

General expenses ……………………………………………

81,000

Interest expense ……………………………………………..

25,000

Loss on sale of plant assets …………………………....

15,000

Income tax expense …………………………………………

35,950

Total expenses and losses …………………………...

564,150

Income from continuing operations ……………………..

90,250

Income from discontinued operations,

$20,000, less income tax, $6,100 ………………………

13,900

Income before extraordinary item …………………………

104,150

Extraordinary loss, $14,000,

less income tax savings of $4,300 …………………….

(9,700)

Net income ……………………………………………………….…

$ 94,450

.

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–43

(continued) P 11-55B

Req. 1 (continued)

Earnings per share:

Income from continuing operations

[($90,250 – $1,800* / 31,000**] ……………………………………….

$2.85

Income from discontinued operations ($13,900 / 31,000)……

.45

Income before extraordinary item

[($104,150 − $1,800) / 31,000] ………………………………………..

3.30

Extraordinary loss ($9,700 / 31,000) ………………………………….

(.31)

Net income [($94,450 − $1,800) / 31,000] …………………………..

$2.99

_____

Computations:

*Preferred dividends: $30,000 x 6% = $1,800

**Common shares outstanding: 31,000 (36,000 issued − 5,000 treasury)

Req. 2

The company hoped to earn income from continuing operations equal

(10-15 min.) P 11-56B

Midler Cosmetics, Inc

Statement of Retained Earnings

Year Ended December 31, 2014

Retained earnings balance, December 31, 2013

as originally reported …………………………………………………

$202,000

Prior-period adjustment (debit) ………………………………………..

(9,300)

Retained earnings balance, December 31, 2013

as adjusted ………………………………………………………………..

192,700

Net income for 2014 ………………………………………………………..

94,450

Subtotal

287,150

Dividends declared for 2014 …………………………………………….

(38,800)*

Retained earnings balance, December 31, 2014 ………………..

$248,350

* Dividends for 2014: $37,000 + ($30,000 x 6%) = $38,800

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–45

(10-15 min. — after working P 11-55B) P 11-57B

Estimated value

of Midler

common stock

Estimated annual

Income from continuing

=

income in the future

=

operations ($90,250)

=

$1,289,286

Investment

.07

capitalization rate

(30-40 min.) P 11-58B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

May

1

Accounts Receivable (€65,000 × $1.33) ……

86,450

Sales Revenue ………………………………….

86,450

10

Supplies………………………………………………..

37,440

Accounts Payable (C$52,000 × $.72) …..

37,440

17

Accounts Receivable (₤125,000 × $1.93) ….

241,250

Sales Revenue ………………………………….

241,250

22

Cash (€65,000 × $1.36) …………………………...

88,400

Accounts Receivable ………………………..

86,450

Foreign-Currency Transaction Gain……

1,950

June

18

Accounts Payable ………………………………….

37,440

Cash (C$52,000 × $.71) ………………………

36,920

Foreign-Currency Transaction Gain……

520

24

Cash (₤125,000 × $1.90) ………………………….

237,500

Foreign-Currency Transaction Loss ……….

3,750

Accounts Receivable ………………………..

241,250

Income statement (partial):

Other loss and expense:

Foreign-currency transaction (loss), net

($1,950 + $520 − $3,750) ………………………………………..

$(1,280)

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–47

(continued) P 11-58B

Req. 2

This problem demonstrates that the final amount of a cash receipt or

cash payment on an international transaction may differ from the initial

(20-25 min.) P 11-59B

Req. 1

Earnings per share:

Income from continuing operations

[($449,000 − $45,000) / 245,000]……………………………

$1.65

Loss on discontinued operations ($57,000 / 245,000)…….

(.23)

Income before extraordinary items

[($392,000 − $45,000) / 245,000]……………………………

1.42

Extraordinary gain ($94,000 / 245,000)………………………

.38

Net income [($486,000 − $45,000) / 245,000]………………..

$1.80

_____

Computations:

Preferred dividends: 20,000 × $2.25 = $45,000

Req. 2

Investment Capitalization Rates

6%

8%

10%

Estimated value

of BEL

=

$1.65

$1.65

$1.65

common stock

.06

.08

.10

=

$27.50

$20.63

$16.50

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–49

(30-40 min.) P 11-60B

Req. 1

Southern Harvest Foods, Inc.

Income Statement

Year Ended June 30, 2014

Revenues:

Sales revenue …………………………………………..

$897,000

Less: Sales returns ……………………………..

$21,000

Sales discounts ………………………….

12,000

(33,000)

Net sales revenue …………………………………………

864,000

Expenses:

Cost of goods sold ……………………………………

$363,000

Selling expenses ………………………………………

49,000

General expenses……………………………………..

75,000

Income tax expense ………………………………….

113,100

Total expenses ……………………………………..

600,100

Income from continuing operations ……………….

263,900

Loss on discontinued operations,

$28,000, less income tax saving, $8,400 ……..

(19,600)

Income before extraordinary item ………………….

244,300

Extraordinary gain, $44,000,

less income tax of $13,200 ………………………..

30,800

Net income …………………………………………………..

$275,100

Earnings per share:

Income from continuing operations ($263,900 / 30,000*) ….

$8.80

Loss from discontinued operations ($19,600 / 30,000) ……..

(0.65)

Income before extraordinary item ($244,300 / 30,000) ………

8.14

Extraordinary gain ($30,800 / 30,000)………………………………

1.03

Net income ($275,100 / 30,000) ……………………………………….

$9.17

_____

(continued) P 11-60B

Req. 2

Southern Harvest Foods, Inc.

Statement of Comprehensive Income

Year Ended June 30, 2014

Net income ……………………………………………………

$275,100

Other comprehensive income:

Unrealized loss on investments in AFSS,

$14,000, less income tax savings, $4,200 ..

(9,800)

Comprehensive income …………………………………

$265,300

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–51

(25-35 min.) P 11-61B

Req. 1

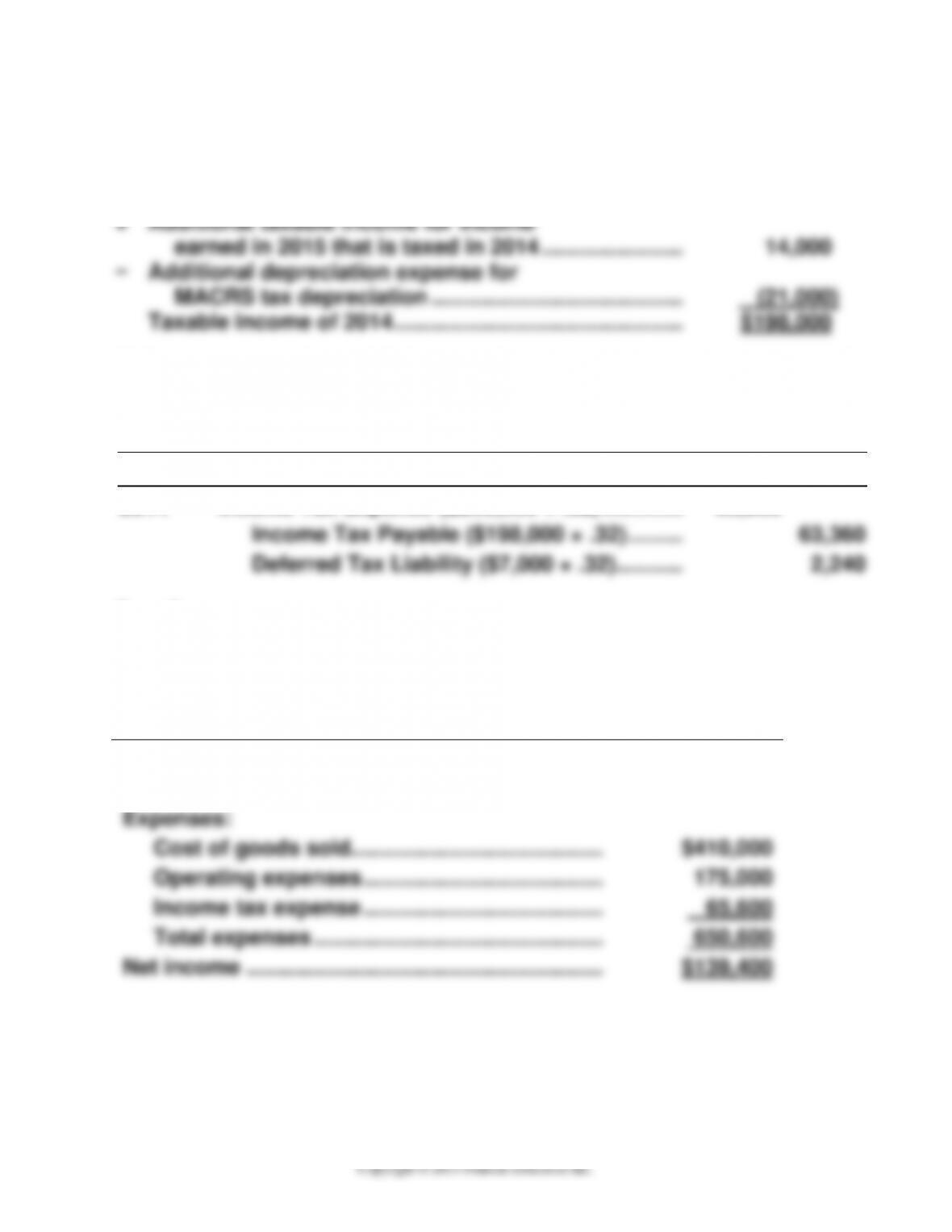

Pretax accounting income of 2014 ………………………..

$205,000

+

Additional taxable income for income

earned in 2015 that is taxed in 2014 …………………..

14,000

−

Additional depreciation expense for

MACRS tax depreciation …………………………………..

(21,000)

Taxable income of 2014 ………………………………………..

$198,000

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Income Tax Expense ($205,000 × .32) ………….

65,600

Income Tax Payable ($198,000 × .32) ………

63,360

Deferred Tax Liability ($7,000 × .32) ………..

2,240

Req. 3

Neighbors Publications, Inc.

Income Statement

For the Year 2014

Total revenue……………………………………………….

$790,000

Expenses:

Cost of goods sold…………………………………..

$410,000

Operating expenses …………………………………

175,000

Income tax expense …………………………………

65,600

Total expenses ………………………………………..

650,600

Net income ………………………………………………….

$139,400

Challenge Exercises and Problem

(20 min.) P 11-62

Req. 1

Transaction

Operating

Income

Income

before

Tax

Net

Income

Earnings

per

Share

a.*

NE

NE

NE

NE

b.

+ $45,000

+ $45,000

+ $27,000

+

c.

NE

NE

NE

NE

d.

NE

– $3,000

– $1,800

–

e.

NE

NE

NE

–

f.

– $5,000

– $5,000

– $3,000

–

g.

NE

+ $20,000

+ $12,000

+

h.

NE

NE

NE

–

i.

NE

NE

NE

–

*Assuming the company uses the perpetual inventory method, the

omitted entry only affects balance sheet accounts (Inventory and

Accounts Payable).

Req. 2

Operating

Income

Income

before

Tax

Net

income

Earnings

per

Share

Totals

$440,000

$507,000

$304,200

$4.24*

*($304,200 – $50,000)/ (50,000 + 5,000 + 5,000)