(20-30 min) P 6-75

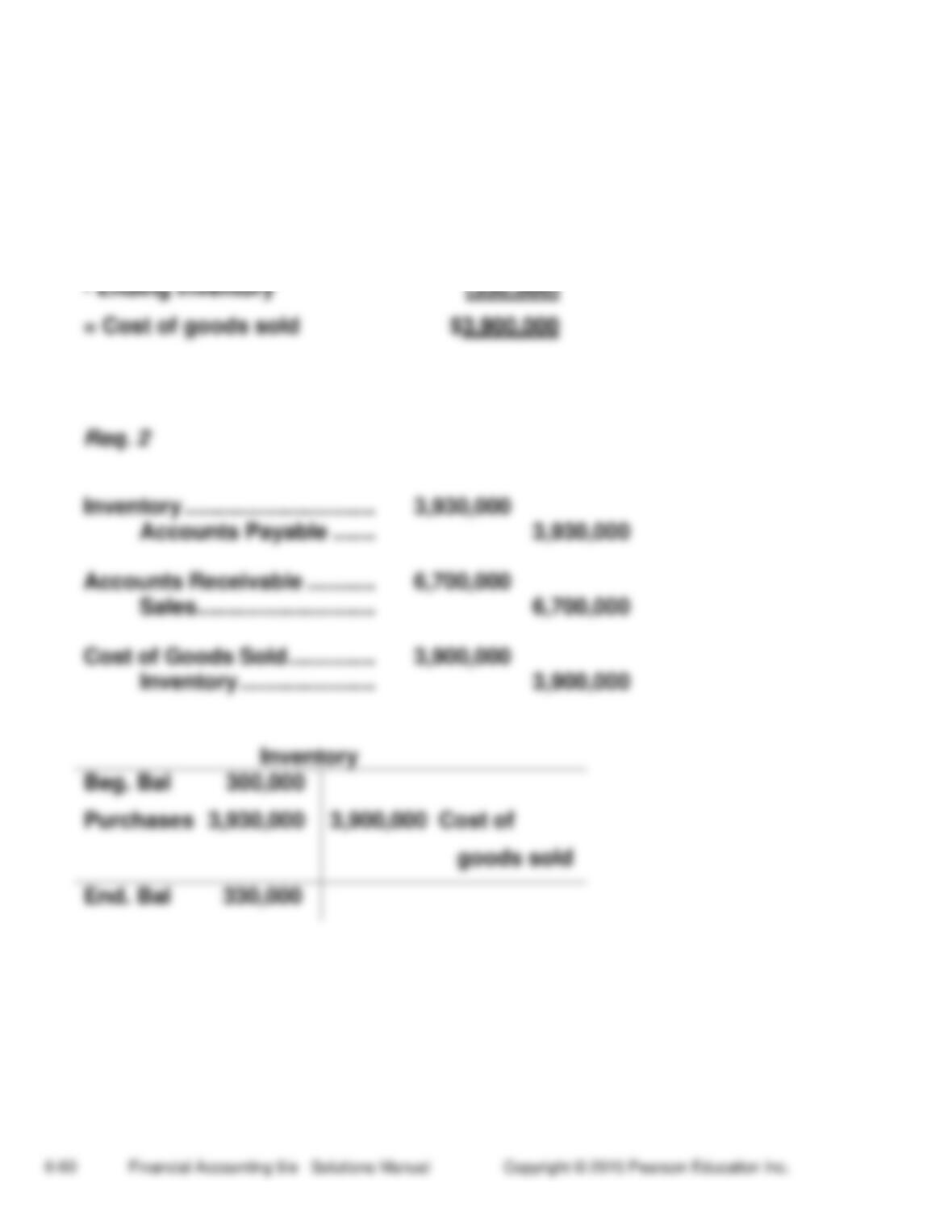

Req. 1

Beginning inventory $ 300,000

+ Purchases ? $3,930,000

(continued) P 6-75

Req. 3

Beginning inventory ($20,000 higher under FIFO) $ 320,000

has a gross profit of $.40 of every sales dollar. GeneTech has a lower

inventory turnover than HeartStart, although both appear strong.

Decision Cases

(50-60 min.) Decision Case 1

Req 1

Duracraft Corporation

Income Statement

FIFO

LIFO

Sales revenue

$1,200,000

$1,200,000

Cost of goods sold:

585,000*

645,000**

Gross profit

615,000

555,000

Operating expenses

200,000

200,000

Income before income

tax expense

415,000

355,000

Income tax expense

($415,000 × .40)

166,000

($355,000 × .40)

142,000

Net income

$ 249,000

$ 213,000

_____

*$100,000 + $485,000 = $585,000

**$160,000 + $485,000 = $645,000

Req. 2

FIFO

LIFO

Net income…………

$249,000

$213,000

FIFO net income is higher because (1) prices are rising (from $100 to

(15-25 min.) Decision Case 2

Req. 1

This question provides a rich setting for a class discussion. There’s no

single correct answer to this question. Some students may favor Company

B because it reports higher net income than Company A. B may be

Req. 2

Yes, the authors would prefer managers to be faithful in representing the

disclosures for inventory — for all the reasons accountants are transparent

Ethical Issue

Req. 1

Changing accounting methods year after year hurts a company’s

Req. 2

The consistency principle is violated.

Req. 3

Creditors and outside investors could be harmed by accounting

changes year after year. It becomes difficult to tell which changes in the

Focus on Financials: Amazon.com, Inc.

(30 min.)

Req. 1

Millions

December 31,

December 31,

2012

2011

Inventory (from the balance sheet)

$6,031

$4,992

In addition to these inventories that Amazon.com, Inc. owns,

Amazon.com, Inc. handles a significant amount of sellers’ inventory on

consignment. Note 1 of the Consolidated Financial Statements

Req. 2

Note 1 of the Consolidated Financial Statements (Description of

(continued) Focus on Financials: Amazon.com, Inc.

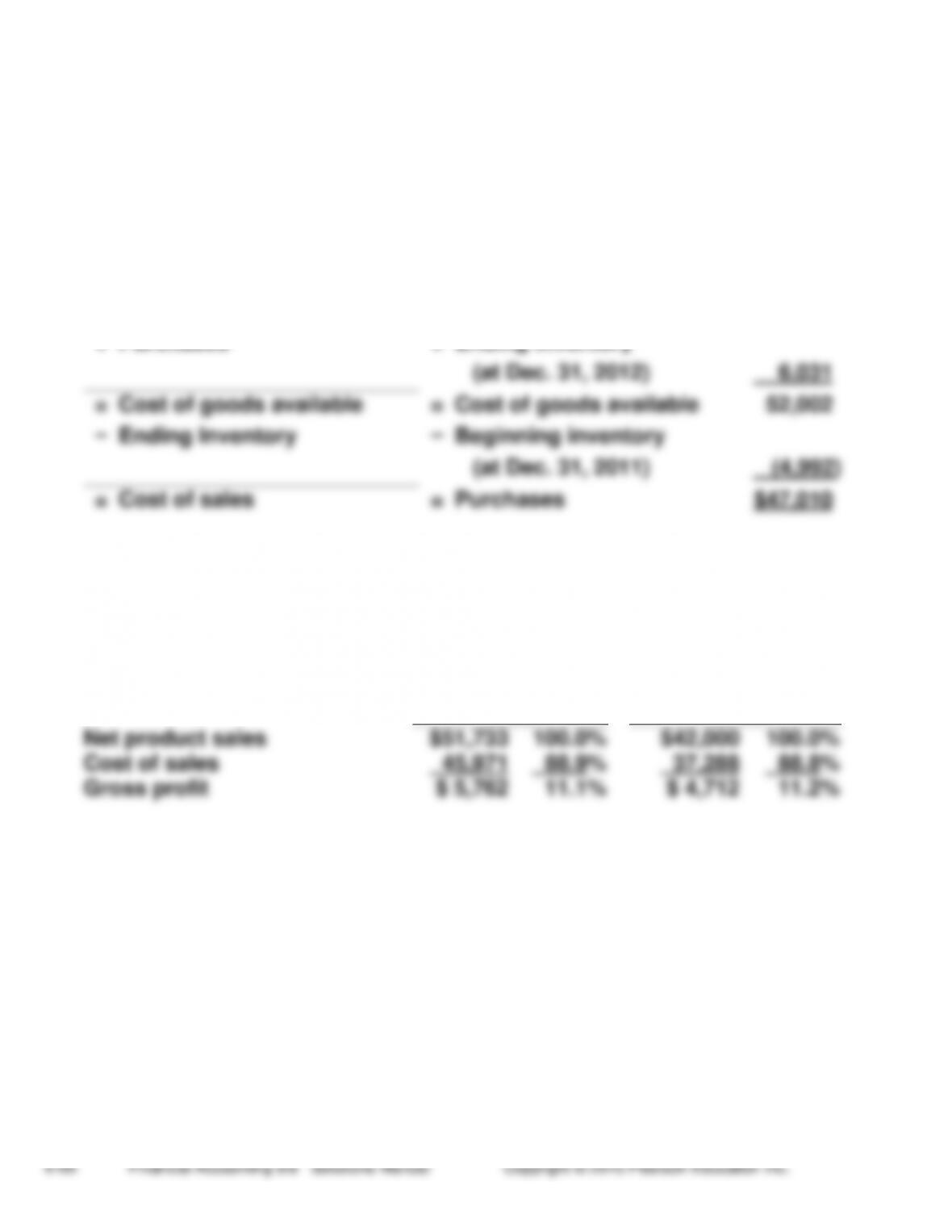

Req. 3

Millions

Rearranging,

Beginning Inventory

Cost of sales

(2012 income statement)

$45,971

+

Purchases

+

Ending inventory

(at Dec. 31, 2012)

6,031

=

Cost of goods available

=

Cost of goods available

52,002

−

Ending Inventory

−

Beginning inventory

(at Dec. 31, 2011)

(4,992)

=

Cost of sales

=

Purchases

$47,010

Req. 4

The gross profit percentage decreased slightly during 2012:

2012

2011

Net product sales

$51,733

100.0%

$42,000

100.0%

Cost of sales

45,971

88.9%

37,288

88.8%

Gross profit

$ 5,762

11.1%

$ 4,712

11.2%

(continued) Focus on Financials: Amazon.com, Inc.

Req. 5

Amazon.com, Inc.’s rate of inventory turnover for 2012 is 8.34 times.

Cost of sales

=

$45,971

=

8.34

times

Average inventory

($4,992 +

$6,031) / 2

2011 Inventory turnover is 9.1 times.

Cost of sales

=

$37,288

=

9.10

times

Average inventory

($4,992 +

$3,202) / 2

Req. 6

Answers to this question will vary, depending on when the exercise is

Focus on Analysis: YUM! Brands, Inc.

(30-40 min.)

Req. 1

a.

Inventory on hand at fiscal 2012 year end, $313 million.

b.

Cost of sales, $3,874 million.

Millions

c.

Purchases

=

Ending inventory ………………………..

$ 313

+

Cost of goods sold ……………………..

3,874

−

Beginning inventory ……………………

(273)

=

Purchases ………………………………….

$3,914

Req. 2

Req. 3

Millions

Accounts payable, beginning of 2012

(ending balance for fiscal 2011) …………………………………

$1,874

+

Purchases 2012 (Req. 1) ……………………………………………

3,914

−

Cash payments on account 2012 ……………………………….

(X)

=

Accounts payable, end of 2012 ………………………………….

$1,945

2012 Cash payments (X) = $3,843 million

(continued) Focus on Analysis: YUM! Brands, Inc.

Req. 4

Note 2 of the Consolidated Financial Statements (Summary of

Significant Accounting Policies), under Inventories, states: “We value or

inventories at the lower of cost…or market”. The company uses the

First-in, First-out (FIFO) method.

Req. 5

(Dollars in millions)

2012

2011

Gross profit

=

$11,833 − $3,874

$10,893 − $3,633

percentage

$11,833

$10,893

=

67.3%

66.6%

Inventory

turnover

=

$3,874

($313 + $273) / 2

$3,633

($273 + $189) / 2

=

13.2

15.7

Inventory turnover declined slightly. Overall, YUM! Brands’ (a) gross

Group Project

Chapter 6 Appendix

Appendix Short Exercises

(10-15 min.) S6A-1

(Journal entries)

General Journal

1.

Purchases

1,190

Accounts Payable

1,190

Purchased inventory on account.

2.

Accounts Receivable

2,900

Sales Revenue

2,900

Sold inventory on account.

3.

End-of–period entries to update inventory

and record Cost of Goods sold:

a.

Cost of Goods Sold

580

Inventory (beginning balance)

580

Transfer beginning inventory to COGS.

b.

Inventory (ending balance)

650

Cost of Goods Sold

650

Set up ending inventory based on physical

count.

c.

Cost of Goods Sold

1,190

Purchases

1,190

Transfer purchases to COGS.

(10-15 min.) S6A-2

Req. 1 Posting general journal entries

Inventory

580*

580

650

650

* Beginning inventory was $580

Cost of Goods Sold

580

650

1,190

1,120

Req. 2

Cost-of-Goods-Sold Model

Beginning inventory

$ 580

+ Purchases

1,190

= Cost of goods available

1,770

– Ending inventory

650

= Cost of goods sold

$1,120

Req. 3

Flexon Technologies

Income Statement (Partial)

Sales revenue

$2,900

Cost of goods sold:

Beginning inventory

$ 580

Purchases

1,190

Cost of goods available

1,770

Ending inventory

(650)

Cost of goods sold

1,120

Gross profit

$1,780

Appendix Exercises

(10-15 min.) E6A-3A

Inventory

Begin. Bal.

(5 units @ $60) 300

Purchases

Oct. 8

(4 units @ $60) 240

Cost of goods sold

15

(10 units @ $70) 700

26

(1 unit @ $80) 80

(13 units @ $?)

?

Ending Bal.

(7 units @ $?) ?

Cost of

Goods Sold

Ending Inventory

(1) Specific

unit

cost

(6 @ $60) + (6 @

$70) + (1 @ $80)

=

$860

(3 @ $60) + (4 @

$70)

=

$460

(2) Average

cost

(13 × $66*)

=

$858

(7 × $66*)

=

$462

($300 + $240 + $700 + $80)

(3)

(4)

(1 @ $80) + (10 @

(10-15 min.) E6A-4A

Reqs. 1, 2, & 3 (Journal entries)

General Journal

1.

Purchases

1,020

Accounts Payable

1,020

Purchased inventory on account.

2.

Accounts Receivable

3,900

Sales Revenue

3,900

Sold inventory on account.

3.

End-of–period entries to update inventory

and record Cost of Goods Sold:

a.

Cost of Goods Sold

300

Inventory (beginning balance)

300

Transfer beginning inventory to COGS.

b.

Inventory (ending balance)

420

Cost of Goods Sold

420

Set up ending inventory based on physical

count.

c.

Cost of Goods Sold

1,020

Purchases

1,020

Transfer purchases to COGS.

Posting general journal entries

Cost of Goods Sold

Beginning inventory 300

Ending Inventory 420

Purchases 1,020

Cost of goods sold 900

Req. 4 Cost-of-Goods-Sold Model

Beginning inventory

$ 300

+ Purchases

1,020

= Cost of goods available

1,320

– Ending inventory

420

= Cost of goods sold

$ 900

Appendix Problems

(20-25 min.) P6A-5A

Req. 1

Inventory

Begin. Bal.

(52 units @ $13) 676

Purchases

Aug. 8

(78 units @ $14) 1,092

Cost of goods sold

30

(20 units @ $15) 300

(100 units @ $?)

?

Ending Bal.

(50 units @ $?) ?

Cost of Goods Sold

Ending Inventory

FIFO

(52 @ $13) + (48 @$14)

=

$1,348

(20 @ $15) + (30 @

$14)

=

$720

Req. 2

Date

Units Sold

Selling

Price

Total Revenue

Aug 3

14

$67

$ 938

Aug 11

38

$67

2,546

Aug 19

7

$69

483

Aug 24

32

$69

2,208

Aug 31

9

$69

621

Total

100

$6,796

Waverly Outlet

Income Statement (Partial)

Sales revenue

$6,796

Cost of goods sold:

Beginning inventory

$ 676

Purchases

1,392

Cost of goods available

2,068

Ending inventory

(720)

Cost of goods sold

1,348

Gross profit

$5,448

(20-30 min.) P6A–6A

Req. 1 (Journal entries)

General Journal

(thousands)

1.

Purchases

2,000

Accounts Payable

2,000

Purchased inventory on account

2.

Accounts Receivable

2,550

Cash

850

Sales Revenue

3,400

Sold inventory for cash and on account

3.

End-of–period entries to update inventory

and record Cost of Goods Sold:

a.

Cost of Goods Sold

490

Inventory (beginning balance)

490

Transfer beginning inventory to COGS

b.

Inventory (ending balance)

620

Cost of Goods Sold

620

Set up ending inventory based on physical

count

c.

Cost of Goods Sold

2,000

Purchases

2,000

Transfer purchases to COGS

(continued) P6A-6A

Req. 2

Total Desserts, Inc.

Income Statement (Partial)

Sales revenue

$3,400

Cost of goods sold:

Beginning inventory

$ 490

Purchases

2,000

Cost of goods available

2,490

Ending inventory

(620)

Cost of goods sold

1,870

Gross profit

$1,530

Cost-of-Goods-Sold Model

Beginning inventory

$ 490

+ Purchases

2,000

= Cost of goods available

2,490

– Ending inventory

620

= Cost of goods sold

$1,870