(45-60 min.) P 3-64A

Req. 1

(All amounts in millions)

Current ratio

=

Total current assets

=

$15.8

=

1.84

Total current liabilities

$8.6

$13.9

Debt ratio

=

Total liabilities

=

$8.6 + $5.3

=

0.43

Total assets

$32.1

Req. 2

Current Ratio

Debt Ratio

a.

$15.8 + $2.4

=

2.12

$13.9

=

0.40

$8.6

$32.1 + $2.4

b.

$15.8 + $2.0

=

2.07

$13.9 + $2.0

=

0.47

$8.6

$32.1 + $2.0

c.

$15.8 − ($8.6 × 1/2)

=

2.67

$13.9 − ($8.6 × 1/2)

=

0.35

($8.6 × 1/2)

$32.1 − ($8.6 × 1/2)

d.

$15.8 − $.7

=

1.76

$13.9

=

0.44

$8.6

$32.1 − $.7

e.

$15.8

=

1.74

$13.9 + $0.5

=

0.45

$8.6 + $0.5

$32.1

f.

$15.8 − $1.5

=

1.66

$13.9 + $2.5

=

0.47

$8.6

$32.1 + $4.0 − $1.5

g.

$15.8

=

1.84

$13.9

=

0.44

$8.6

$32.1− $0.4

(continued) P 3-64A

Req. 3

a. Revenues usually increase the current ratio.

b. Revenues usually decrease the debt ratio.

(20-30 min.) P 3-65B

Req. 1

Hudson Tax Consulting

Amount of Revenue (Expense) for December

Date

Cash Basis

Accrual Basis

Dec.

1

Expense

$ (3,500)

Expense

$ 0

4

Expense

(900)

Expense

0

5

Revenue

1,500

Revenue

1,500

8

Expense

(140)

Expense

(140)

11

Revenue

0

Revenue

3,100

19

Expense

0

Expense

0

24

Revenue

3,100

Revenue

0

26

Expense

(2,800)

Expense

0

29

Expense

(800)

Expense

(800)

31

Expense

0

Expense ($3,500 / 5)

(700)

31

Revenue

0

Revenue

400

31

Expense

0

Expense

(210)

Req. 2

Income (loss)

before tax

$(3,540)

Income before tax

$3,150

Req. 3

The accrual-basis measure of net income is preferable because it accounts

for revenues and expenses when they occur, not when they are received or

(10-20 min.) P 3-66B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Dec.

31

a. Insurance Expense ……………………….

3,200*

Prepaid Insurance ……………………

3,200

To record insurance expense

31

b. Salary Expense ($5,500 × 1/5) …………

1,100

Salary Payable… ………………………

1,100

To accrue salary expense.

31

c. Interest Receivable ………………………..

500

Interest Revenue ………………………

500

To accrue interest revenue.

31

d. Supplies Expense ………………………….

6,680**

Supplies ………………………………….

6,680

To record supplies expense.

31

e. Unearned Service Revenue

($11,900 × 60%) ……………………………..

7,140

Service Revenue ………………………

7,140

To record revenue that was collected

in advance.

31

f. Depreciation Expense – Office ………

Furniture ……………………………..

Depreciation Expense – Equipment

3,500

5,800

Accumulated Depreciation –

Office Furniture ……………………

3,500

Accumulated Depreciation –

Equipment …………………………. .

5,800

To record depreciation expense.

_____

* $800 + $3,600 − $1,200 = $3,200

** $2,700 + $6,400 − $2,420 = $6,680

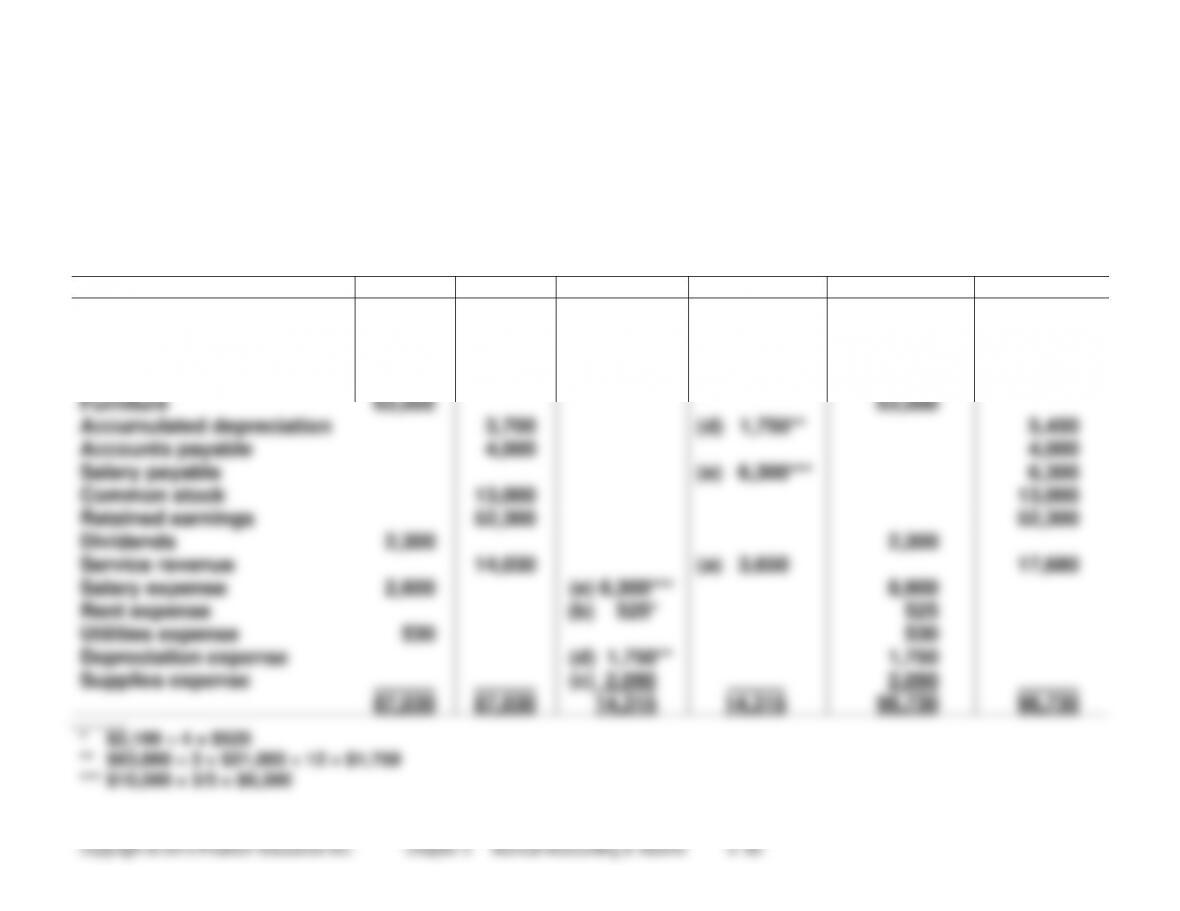

(45-60 min.) P 3-67B

Req. 1

Kingston, Inc.

Adjusted Trial Balance

March 31, 2015

TRIAL BALANCE

ADJUSTMENTS

ADJUSTED

TRIAL BALANCE

ACCOUNT TITLE

DEBIT

CREDIT

DEBIT

CREDIT

DEBIT

CREDIT

Cash

11,200

11,200

Accounts receivable

2,900

(a) 3,650

6,550

Prepaid rent

2,100

(b) 525*

1,575

Supplies

2,400

(c) 2,090

310

Furniture

63,000

63,000

Accumulated depreciation

3,700

(d) 1,750**

5,450

Accounts payable

4,000

4,000

Salary payable

(e) 6,300***

6,300

Common stock

13,000

13,000

Retained earnings

52,300

52,300

Dividends

2,300

2,300

Service revenue

14,030

(a) 3,650

17,680

Salary expense

2,600

(e) 6,300***

8,900

Rent expense

(b) 525*

525

Utilities expense

530

530

Depreciation expense

(d) 1,750**

1,750

Supplies expense

(c) 2,090

_____

2,090

87,030

87,030

14,315

14,315

98,730

98,730

* $2,100 ÷ 4 = $525

** $63,000 ÷ 3 = $21,000 ÷ 12 = $1,750

*** $10,500 × 3/5 = $6,300

(continued) P 3-67B

Req. 2 (continued)

Kingston, Inc.

Income Statement

Month Ended March 31, 2015

Revenues:

Service revenue

$17,680

Expenses:

Salary expense

$8,900

Supplies expense

2,090

Depreciation expense

1,750

Utilities expense

530

Rent expense

525

Total expenses

13,795

Net income

$ 3,885

Kingston, Inc.

Statement of Retained Earnings

Month Ended March 31, 2015

Retained earnings, March 1, 2015

$52,300

Add: Net income

3,885

Subtotal

56,185

Less: Dividends declared

(2,300)

Retained earnings, March 31, 2015

$53,885

(continued) P 3-67B

Req. 2 (continued)

Kingston, Inc.

Balance Sheet

March 31, 2015

ASSETS

LIABILITIES

Current assets:

Current liabilities:

Cash

$11,200

Accounts payable

$ 4,000

Accounts receivable

6,550

Salary payable

6,300

Prepaid rent

1,575

Total current liabilities

10,300

Supplies

310

Total current assets

19,635

Furniture $63,000

STOCKHOLDERS’ EQUITY

Less: Accum.

Common stock

13,000

deprec. (5,450)

57,550

Retained earnings

53,885

Total stockholders’ equity

66,885

______

Total liabilities and

______

Total assets

$77,185

stockholders’ equity

$77,185

(10-20 min.) P 3-68B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Apr.

30

Accounts Receivable ($7,150 − $6,800) …………..

350

Rental Revenue ………………………………………..

350

To accrue rental revenue.

30

Interest Receivable ($400 − $0) ………………………

400

Interest Revenue ($700 − $300) ………………….

400

30

Supplies Expense ($500 − $0) ………………………..

500

Supplies ($1,300 − $800) …………………………..

500

To record supplies expense.

30

Insurance Expense ($1,500 − $0) ……………………

1,500

Prepaid Insurance ($2,400 − $900) …………….

1,500

To record insurance expense.

30

Depreciation Expense ($1,400 − $0) ………………..

1,400

Accumulated Depreciation

($10,200 − $8,800) …………………………………….

1,400

To record depreciation expense.

30

Wage Expense ($2,630 − $1,300) …………………….

1,330

Wages Payable ($1,330 − $0) …………………….

1,330

To accrue salary expense.

30

Unearned Rental Revenue ($2,000 − $950) ………

1,050

Rental Revenue* ………………………………………

1,050

To record revenue that was collected in

advance.

(continued) P 3-68B

Req. 2

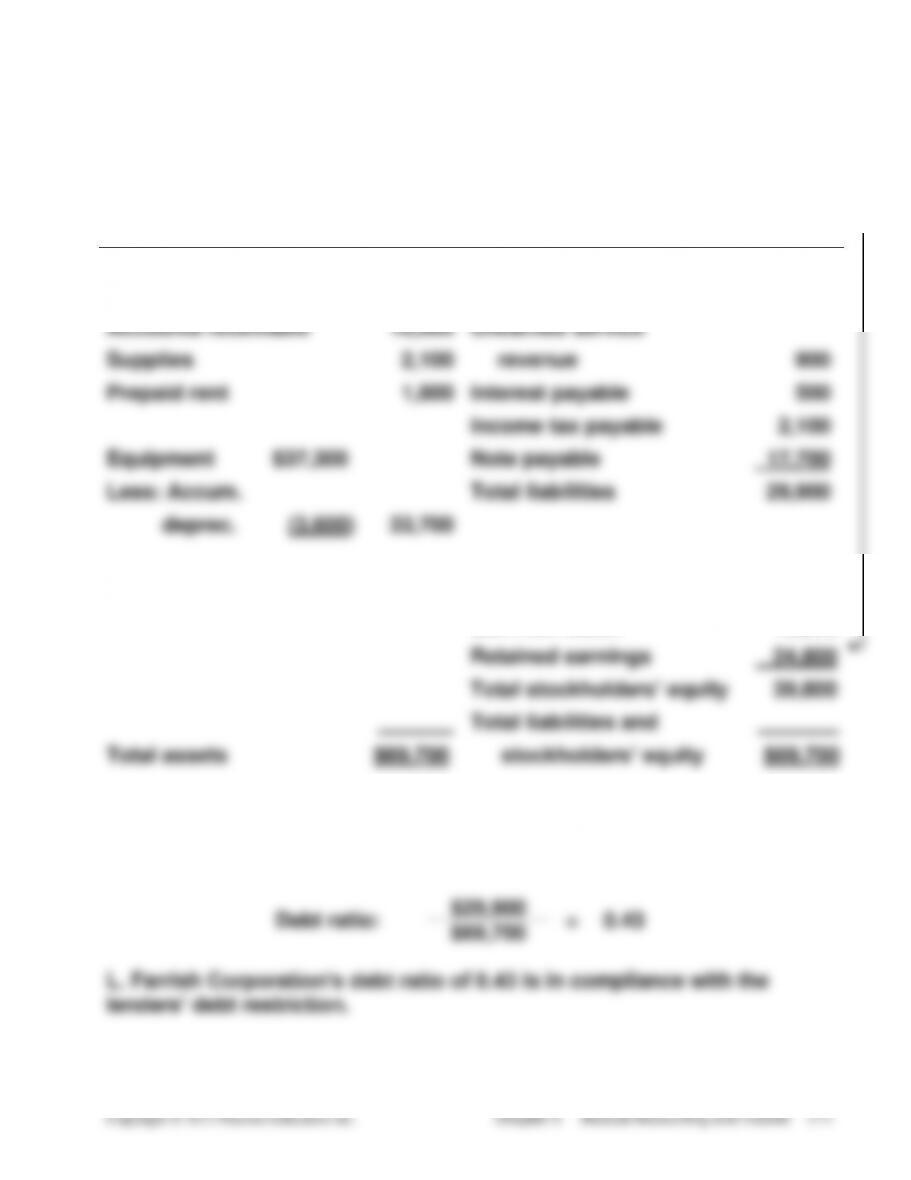

(20-30 min.) P 3-69B

Req. 1

L. Farrish Corporation

Income Statement

Year Ended May 31, 2014

Revenues:

Service revenue

$90,600

Expenses:

Salary expense

$36,200

Rent expense

10,100

Insurance expense

3,600

Interest expense

2,600

Supplies expense

2,500

Depreciation expense

1,200

56,200

Income before tax

34,400

Income tax expense

7,100

Net income

$27,300

L. Farrish Corporation

Statement of Retained Earnings

Year Ended May 31, 2014

Retained earnings, May 31, 2013

$ 3,500

Add: Net income

27,300

Subtotal

30,800

Less: Dividends declared

(6,000)

Retained earnings, May 31, 2014

$24,800

(continued) P 3-69B

Req. 1 (continued)

L. Farrish Corporation.

Balance Sheet

May 31, 2014

ASSETS

LIABILITIES

Cash

$21,500

Accounts payable

$ 8,700

Accounts receivable

10,600

Unearned service

Supplies

2,100

revenue

900

Prepaid rent

1,800

Interest payable

500

Income tax payable

2,100

Equipment

$37,300

Note payable

17,700

Less: Accum.

Total liabilities

29,900

deprec.

(3,600)

33,700

STOCKHOLDERS’ EQUITY

Common stock

15,000

Retained earnings

24,800

Total stockholders’ equity

39,800

Total liabilities and

Total assets

$69,700

stockholders’ equity

$69,700

Req. 2

(20 min.) P 3-70B

Req. 1

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Closing Entries

Jan.

31

Service Revenue ……………………………….

92,700

Retained Earnings ………………………….

92,700

31

Retained Earnings ……………………………..

40,400

Salary Expense ………………………………

21,700

Supplies Expense …………………………..

4,800

Advertising Expense ………………………

11,500

Depreciation Expense …………………….

2,000

Interest Expense …………………………….

400

31

Retained Earnings ……………………………..

22,300

Dividends ………………………………………

22,300

Req. 2

Retained Earnings

Jan. 31, 2014 Expenses

40,400

Jan. 31, 2013 Bal.

10,600

Jan. 31, 2014 Dividends

22,300

Jan. 31, 2014 Revenues

92,700

Jan. 31, 2014 Bal.

40,600

Net income = $52,300 ($92,700 – $40,400)

Req. 3

(30-40 min.) P 3-71B

Req. 1

Lazy River Services, Inc.

Balance Sheet

January 31, 2014

ASSETS

Current assets:

Cash …………………………………………………………….

$17,400

Accounts receivable ……………………………………..

17,200

Prepaid expenses …………………………………………

5,500

Supplies ……………………………………………………….

4,000

Total current assets ………………………………….

44,100

Plant assets:

Equipment ……………………………………………………

$42,800

Less: accumulated depreciation …………………….

(6,900)

35,900

Other assets ………………………………………………………

12,200

Total assets ……………………………………………………….

$92,200

LIABILITIES

Current liabilities:

Accounts payable …………………………………………

$13,900

Current portion of note payable ……………………..

2,700

Salary payable ………………………………………………

2,600

Unearned service revenue …………………………….

3,600

Total current liabilities ………………………………

22,800

Note payable, long-term ……………………………………..

15,600

Total liabilities …………………………………………………..

38,400

STOCKHOLDERS’ EQUITY

Common stock ………………………………………………….

13,200

Retained earnings … ………………………………………….

40,600*

Total stockholders’ equity… …………………………..…..

53,800

Total liabilities and stockholders’ equity ……………..

$92,200

*See next page

(continued) P 3-71B

Req. 1 (continued)

(45-60 min.) P 3-72B

Req. 1

(All amounts in millions)

(continued) P 3-72B

Req. 3

Challenge Exercises and Problem

(20-25 min.) E 3-73

(Dollar amounts in thousands)

December 31, 2014

Current assets = $11,100 ($1,500 + $5,900 + $2,700 + $1,000)

Current liabilities = $6,100 ($2,600 + $1,600 + $1,900)

Net working capital = $5,000 ($11,100 – $6,100)

Current

=

$11,100

=

1.82

ratio

$6,100

January 31, 2015

Current assets = $10,700 ($9001 + $6,8002 + $2,7003 + $3004)

Current liabilities = $5,200 ($1,2005 + $1,6006 + $2,4007)

Net working capital = $5,500 ($10,700 – $5,200)

Current

=

$10,700

=

2.06

ratio

$5,200

_____

Computations of January 31, 2015 balances:

1Cash = $1,500 − $7,300 + $8,100 − $1,400 = $900

2Receivables = $5,900 + $9,000 − $8,100 = $6,800

3No change in the Inventory balance.

4Prepaid expenses = $1,000 − $700 = $300

5Accounts payable = $2,600 − $1,400 = $1,200

6No change in the Unearned Revenues balance.

7Accrued expenses payable = $1,900 + $500 = $2,400

Conclusion: Baltimore’s net working capital and current ratio

(60 min.) E 3-74

a.

Net income:

Service revenue:

($161,000 + $1,650 + $32,200) ………………….

$194,850

Expenses:

Salary ($37,000 + $3,500) ………………………..

$ 40,500

Depreciation – building ………………………….

2,600

Supplies ………………………………………………..

3,100

Insurance ………………………………………………

1,500

Advertising ……………………………………………

7,300

Utilities ………………………………………………….

2,000

57,000

Net income …………………………………………………

$137,850

b.

Total assets:

Cash ………………………………………………………….

$ 7,300

Accounts receivable ($7,500 + $32,200) ………..

39,700

Supplies ($4,600 − $3,100) …………………………..

1,500

Prepaid insurance ($3,500 − $1,500) …………….

2,000

Building ……………………………………………………..

$110,000

Less: Accum. Depr. ($15,600 + $2,600) …………

(18,200)

91,800

Land …………………………..………………………………

53,000

Total assets …………………………………………..

$195,300

(continued) E 3-74

c.

Total liabilities:

Accounts payable ………………………………….

$ 6,100

Salary payable ……………………………………….

3,500

Unearned service revenue

($5,500 − $1,650) ………………………………..

3,850

Total liabilities ……………………………………….

$ 13,450

d.

Total stockholders’ equity:

Common stock ………………………………………

$ 14,000

Retained earnings, beginning …………………

$ 46,000

Add: Net income……………………………………

137,850

Subtotal

183,850

Less: Dividends declared. ……………………..

(16,000)

167,850

Total stockholders’ equity ………………………

$181,850

e.

Total assets

= Total liabilities + Total stockholders’ equity

$195,300

= $13,450 + $181,850

(20 min.) P 3-75

Mobile Detail Inc.

Balance Sheet

January 31, 2014

ASSETS

LIABILITIES

Cash (a)

$ 15,300

Accounts payable (g)

$ 3,000

Accounts receivable (c)

1,400

Advertising payable(h)

500

Supplies (d)

1,000

Salary payable (i)

500

Total current assets

Equipment (e) $35,000

Less: Accum.

deprec.(f) (12,000)

17,700

23,000

Unearned gift certificate

revenue (b)

Total liabilities

1,200

5,200

STOCKHOLDERS’ EQUITY

Total assets

______

$40,700

Common stock (j)

Retained earnings (k)

Total stockholders’

equity

Total liabilities and

stockholders’ equity

18,000

17,500

35,500

______

$40,700