1) Orlando Corporation incorporated on January 2, 2015. During 2015, Orlando had the

following transactions:

issued 30,000 shares of common stock at $25 per share. The par value per share is $1.

purchased 5,000 shares of treasury stock at $28 per share

had net income of $400,000.

What is the total amount of stockholders’ equity as of December 31, 2015?

A) $610,000

B) $750,000

C) $1,010,000

D) $1,150,000

2) The income statement approach to estimating uncollectible accounts is called the

________ method. The balance sheet approach to estimating uncollectible accounts is

called the ________ method.

A) direct write-off; allowance

B) allowance; direct write-off

C) percent-of-sales; aging-of-receivables

D) aging-of-receivables; percent-of-sales

3) If the equity method is used to account for a long-term investment in common stock,

cash dividends received from the investee are recorded by the investor as:

A) a debit to Equity-Method Investment and a credit to Equity-Method Investment

Revenue

B) a debit to Cash and a credit to Dividend Revenue

C) a debit to Dividend Receivable and a credit to Dividend Revenue

D) a debit to Cash and a credit to Equity-Method Investment

4) The two most common types of fraud impacting the financial statements are:

A) fraudulent financial reporting and e-commerce fraud

B) misappropriation of assets and embezzlement

C) fraudulent financial reporting and misappropriation of assets

D) cooking the books and fraudulent financial reporting

5) Realized gains and losses from long-term available-for-sale investments arise from:

A) the purchase of an investment

B) the sale of the investment

C) changes in the fair value of the investment

D) investor’s share of investee’s net income or net loss

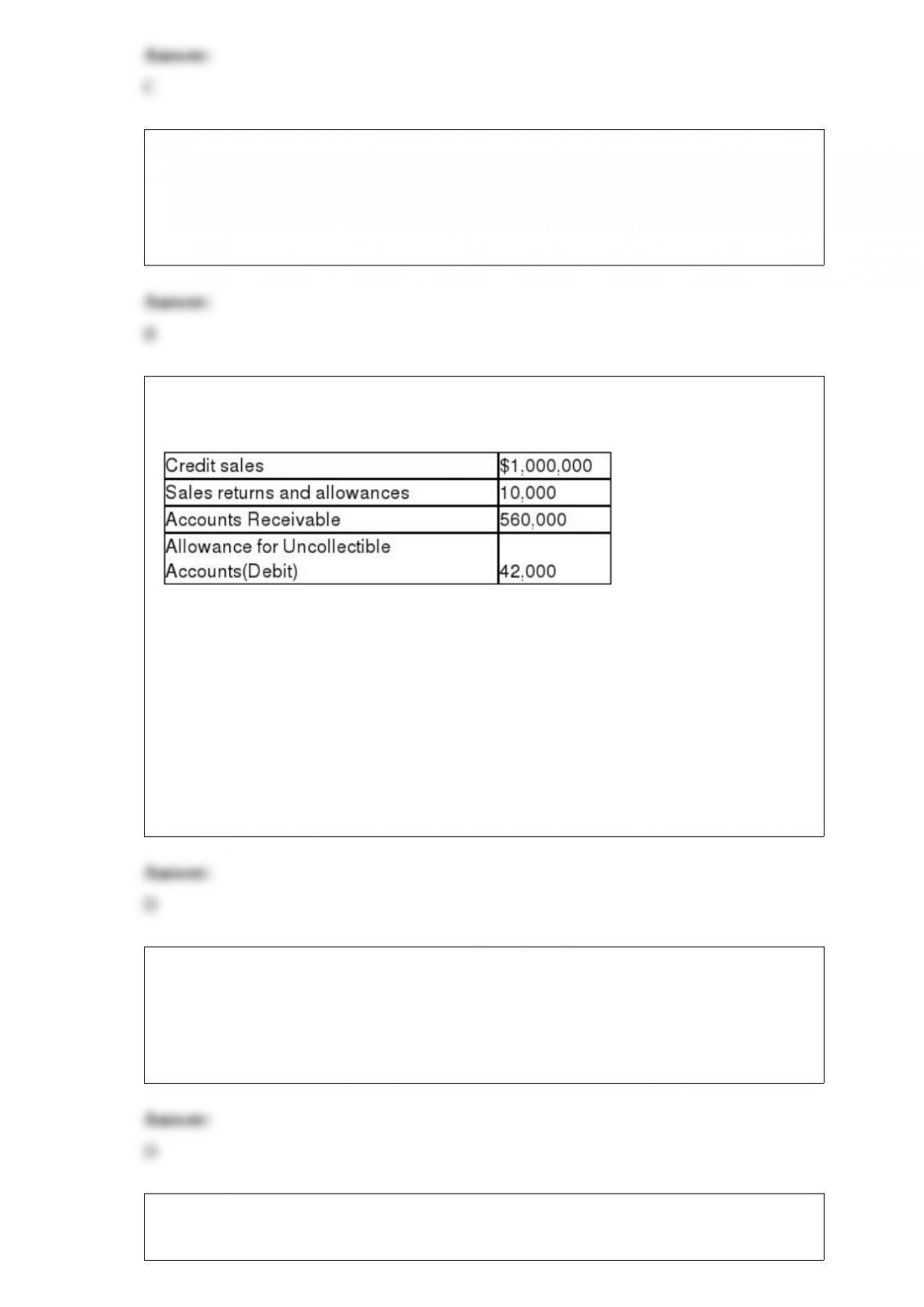

6) At the end of the year, Seidner Company has the following information available:

The company uses the percent-of-sales method to estimate bad debts and has not

prepared the adjusting journal entry for Uncollectible-Account Expense at year end.

What does the debit balance in the Allowance for Uncollectible Accounts indicate?

A) The company overestimated the amount of uncollectible accounts at the end of the

prior accounting period

B) The company underestimated the amount of uncollectible accounts at the end of the

prior accounting period

C) Write-offs of uncollectible accounts increased dramatically in the current accounting

period

D) B and C

7) A consolidated balance sheet excludes:

A) a subsidiary’s stockholders’ equity

B) a parent company’s Investment in Subsidiary account

C) intercompany note receivable and note payable

D) all of the above

8) When preparing the financial statements for a company:

A) the report format of the income statement lists liabilities before assets

B) the account format for the balance sheet lists the assets on the left and liabilities and

stockholders’ equity on the right

C) the multiple-step balance sheet lists assets in order of their liquidity

D) the single-step income statement reports a number of subtotals

9) Which of the following line items are reported net of tax on the income statement?

A) operating loss of discontinued operations

B) loss on sale of discontinued segment

C) extraordinary loss due to flood damage in factory in Phoenix, Arizona

D) all of the above

10) Mike’s Pharmacy sold merchandise with a selling price of $2,500 to customers for

cash. They also collected sales taxes of $300 for the day. The pharmacy uses the

perpetual inventory system but ignore Cost of Goods Sold. The journal entry to record

this information has:

A) debit to Cash of $2,800

B) debit to Sales Tax Expense $300

C) credit to Sales $2,800

D) debit to Sales Tax Payable $300

11) A journal entry that debits Cash and credits Accounts Receivable indicates that:

A) payment was received on account

B) payment was made on account

C) revenue increased

D) revenue decreased

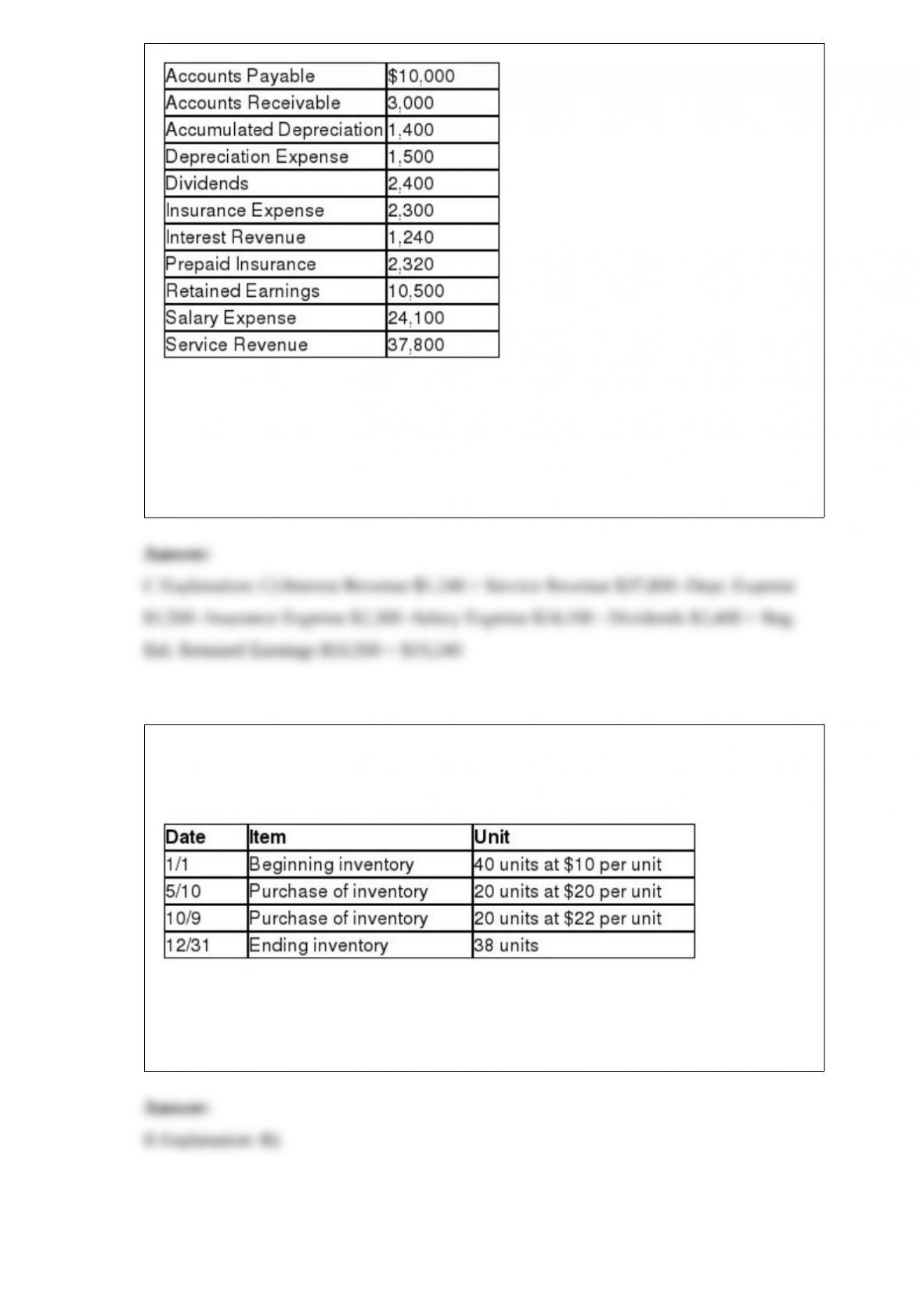

12) The following accounts and balances are taken from Moore Company’s adjusted

trial balance:

What is the ending balance in Retained Earnings after the closing entries are

completed?

A) $8,740

B) $11,140

C) $19,240

D) $39,040

13) Given the following data, calculate the cost of goods sold using the average-cost

method. Round your calculations to two decimal places.

A) $420

B) $651

C) $840

D) $924

14) A chart of accounts:

A) is used by an organization to determine the balance in all of their accounts

B) lists all of the accounts of an organization in alphabetical order

C) must be the same for all organizations

D) lists all of an organization’s accounts and account numbers

15) The authority to declare a dividend lies with the:

A) Chief Financial Officer

B) President of the company

C) Chief Executive Officer

D) Board of Directors

16) When an adjustment is made for prepaid rent:

A) an asset increases and an expense decreases

B) one asset increases and another decreases

C) an asset decreases and an expense increases

D) a liability decreases and an expense decreases

17) Cost of goods sold:

A) is considered a selling expense

B) is the direct cost of the product sold

C) is classified as revenue on the income statement

D) is the same as gross profit

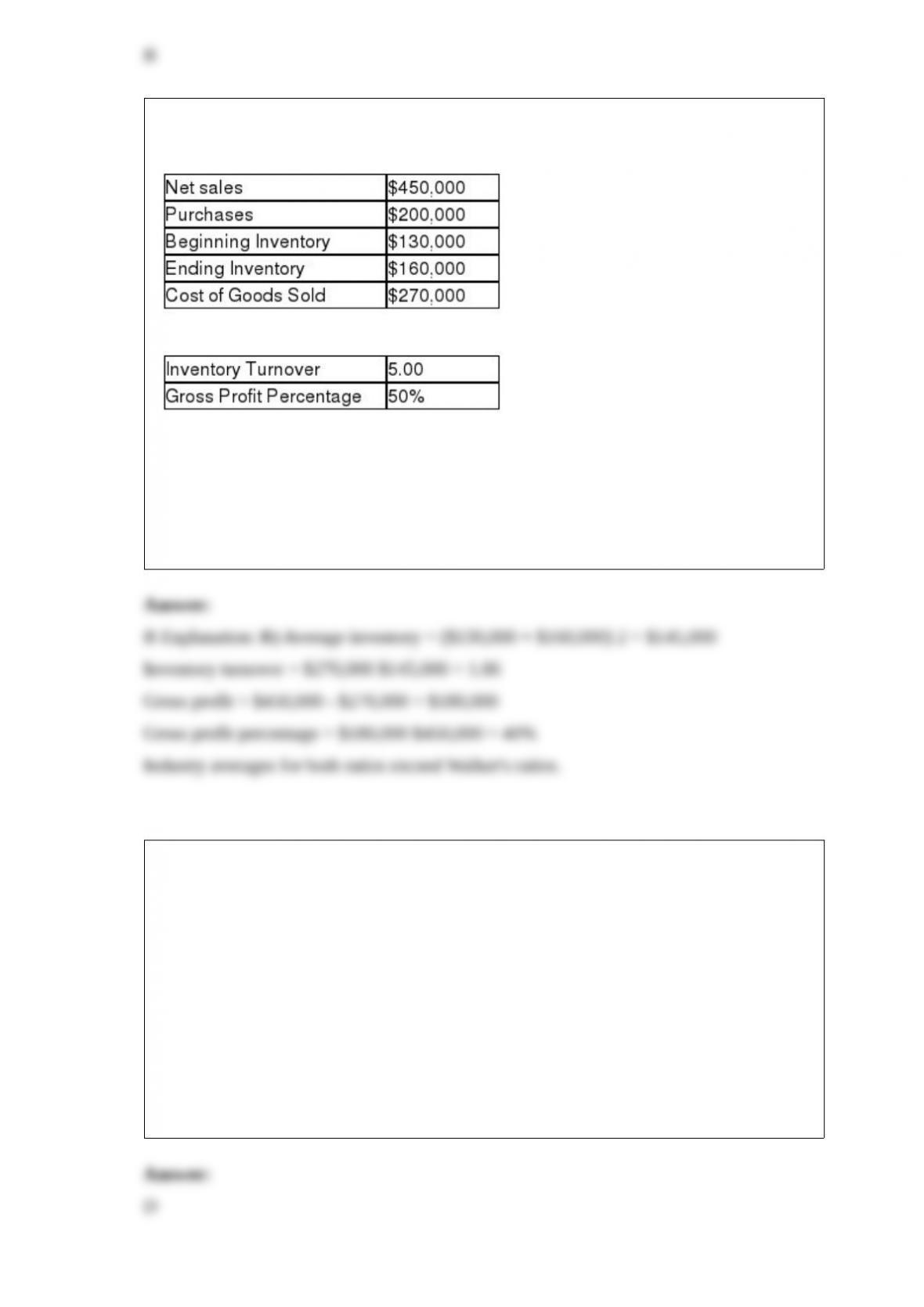

18) Scott Walker Company has the following data available for the past year:

Industry Averages available are:

How do the inventory turnover and gross profit percentage for Scott Walker Company

compare to the industry averages for the same ratios?

A) Walker Company is superior on both measures

B) Walker Company is inferior on both measures

C) Walker Company is inferior on one measure and superior on the other measure

D) There is not enough information

19) On June 1, Neighbor Company purchased inventory on account with a cost of

$5,000. The credit terms were 2/10, net 30. On June 2, Neighbor Company returned 50

percent of the inventory. Neighbor Company uses the perpetual inventory system. On

June 8, Neighbor Company paid for the inventory. What journal entry did Neighbor

Company prepare on June 8?

A) debit Purchase Discount for $50, debit Cash for $2,450 and credit Accounts Payable

for $2,500

B) debit Accounts Payable for $2,500 and credit Cash for $2,500

C) debit Accounts Payable for $2,500, credit Purchase Discount for $50 and credit Cash

for $2,450

D) debit Accounts Payable for $2,500, credit Inventory for $50 and credit Cash for

$2,450

20) Schmid Corporation issues $500,000, 10%, 5-year bonds on January 1, 2014 for

$479,000. Interest is paid semiannually on January 1 and July 1. If Schmid uses the

straight-line method of amortization of bond discount, the amount of bond interest

expense on July 1, 2014 is:

A) $22,900

B) $25,000

C) $27,100

D) $52,100

21) The book value of a plant asset is defined as:

A) historical cost minus residual value

B) historical cost minus accumulated deprecation

C) current sales value minus historical cost

D) historical cost minus annual maintenance expense

22) An investor purchased bonds and intends to hold them until the maturity date which

is 10 years into the future. The bonds were purchased at a discount and pay interest

semiannually. Which journal entry or entries is(are) needed at each interest date?

A) receipt of interest revenue only

B) amortization of bond discount only

C) amortization of bond premium only

D) A and B

23) Under U.S. GAAP, inventories are reported on the balance sheet at:

A) historical cost only

B) current replacement cost only

C) net realizable value only

D) A and B

24) The net loss for a company is reported on the:

A) Statement of Cash Flows

B) Statement of Retained Earnings

C) Income Statement

D) all of the above

25) Current liabilities as reported on the balance sheet do NOT include:

A) current maturities of long-term debt

B) income taxes payable

C) salaries payable

D) treasury stock

26) On December 2, a customer returned merchandise with a selling price of $500

purchased on account to a department store. Ignoring Cost of Goods Sold, what journal

entry did the department store prepare?

A) Debit Sales Revenue for $500 and credit Accounts Receivable for $500

B) Debit Sales Revenue for $500 and credit Cash for $500

C) Debit Sales Revenue for $500, credit Sales Discount for $10, and credit Cash for

$490

D) Debit Sales Returns and Allowances for $500 and credit Accounts Receivable for

$500

27) Using the indirect method to prepare the statement of cash flows, dividends paid

during the year are:

A) subtracted from net income in the operating activities section

B) added to net income in the operating activities section

C) shown as a cash outflow in the financing activities section

D) shown as a cash outflow in the investing activities section

28) The entry to record the purchase of supplies on account would include a credit to:

A) Supplies

B) Accounts Payable

C) Supplies Expense

D) Cash