Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–53

Decision Cases

(15-20 min.) Decision Case 1

EPS to use for predicting future profits:

Unaudited EPS …………………………………………………………………. $1.19

Include:

Gain on sale of building ……………………………………………….. .05

Restructuring expenses ……………………………………………….. (.29)

Loss on lawsuit settlement …………………………………………… (.12)

Lost income due to employee labor strike ……………………… (.24)

EPS to use for prediction ………………………………………………….. $0.59

Include all the preceding items for your prediction because all are

labeled by GAAP as normal business occurrences and are thus part of

(15-20 min.) Decision Case 2

Magid’s earnings are of higher quality than those of Bay Area. Magid

follows more conservative (and more realistic) accounting policies than

Bay Area. Here are some examples:

SALES REVENUE

INSURANCE REVENUE

Magid records insurance revenue over the life of the policy, while Bay

Area records insurance revenue up front when the customer signs the

Overall, Bay Area’s policies for recording revenue suggest that the

company may be overstating its revenue. Magid’s accounting policies

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–55

Ethical Issue

Req. 1

The ethical issue: Does it matter how a company reports its operating

Req. 2 and Req. 3

The stakeholders in this case include the bank, its officers and directors,

shareholders, prospective shareholders, its creditors, and stock

analysts.

(continued) Ethical Issue

and stockholders who buy the company’s stock based on the second

income statement can be hurt. They may lend to the company on too–

favorable terms, or they may pay too high a price for its stock. When the

Req. 4

The bank should report their results of operations in a way that

separates the recurring from the non-recurring items. This course of

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–57

Focus on Financials: Amazon.com, Inc.

(30-45 min.)

Req. 1

Amazon.com, Inc.’s income statement does not mention income from

continuing operations because there are no special items of income,

such as discontinued operations. All of Amazon.com, Inc.’s net income

results from continuing operations. To evaluate quality of earnings, we

Measures

of Quality

of Earnings

2012

2011

2010

Cost of

goods sold

to sales

ratio

$45,971/$51,733 =

0.89

$37,288/$42,000 =

0.89

$26,561/$30,792 =

0.86

Gross

margin to

sales ratio

$5,762/$51,733 =

0.11

$4,712/$42,000 =

0.11

$4,231/$30,792 =

0.14

Operating

expenses

to sales

$14,446/$51,733 =

0.28

$9,927/$42,000 =

0.24

$6,237/$30,792 =

0.20

ratio

Operating

income to

sales ratio

$676/$51,733 =

0.013

$862/$42,000 =

0.0205

$1,406/$30,792 =

0.046

From this analysis, we see the following:

(1) the cost of goods sold to sales ratio increased in 2011 and held

steady in 2012,

(2) the gross margin to sales ratio decreased in 2011 and held steady in

2012,

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–59

(continued) Amazon.com

Req. 2

Cash flows from operations per share = $4,180 / 454 = 9.21

Investment Capitalization Rates

5%

6%

7%

Estimated value

of a share of

Amazon stock

=

$9.21

= 184

$9.215

= 154

$9.21

= 132

.05

.06

.07

Req. 3

Student answers will vary depending on when this problem is assigned.

During the first six months of 2013, Amazon’s stock traded between

Safe investment

Risky investment

Focus on Analysis: YUM! Brands, Inc.

(30 min.)

Req. 1

Measures

of Quality

of Earnings

2012

2011

2010

Cost of

goods sold

to revenues

$3,874/$11,833 =

0.33

$3,633/$10,893 =

0.33

$3,091/$9,783 =

0.32

Gross

margin to

revenues

$7,959/$11,833 =

0.67

$7,260/$10,893 =

0.67

$6,642/$9,783 =

0.68

Operating

expenses

to revenues

ratio

($11,339 – $3,874)

$13,633 =

0.55

($10,811 – $3,633)

$12,626 =

0.57

($9,574 – $3,091)

$11,343 =

0.57

Operating

income to

revenues

ratio

$2,294/$13,633 =

0.17

$1,815/$12,626 =

0.144

$1,769/$11,343 =

0.156

This table examines four ratios that investigate earnings quality. Cost of

goods sold to revenues have been stable over 2011 and 2012, which is a

favorable sign. The same comment applies to gross margin to revenues.

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–61

(continued) YUM! Brands, Inc.

The notes about revenue and expense recognition are also in line with

generally accepted accounting principles, which is favorable for quality

of earnings. Revenues from Company-owned restaurants are

Req. 2

They define their segments by geographic region: China, India YRI

(international excluding India and China), and the U.S. China is the

largest. The financial information they provide by segments is: for

(continued) YUM! Brands, Inc.

Req. 3

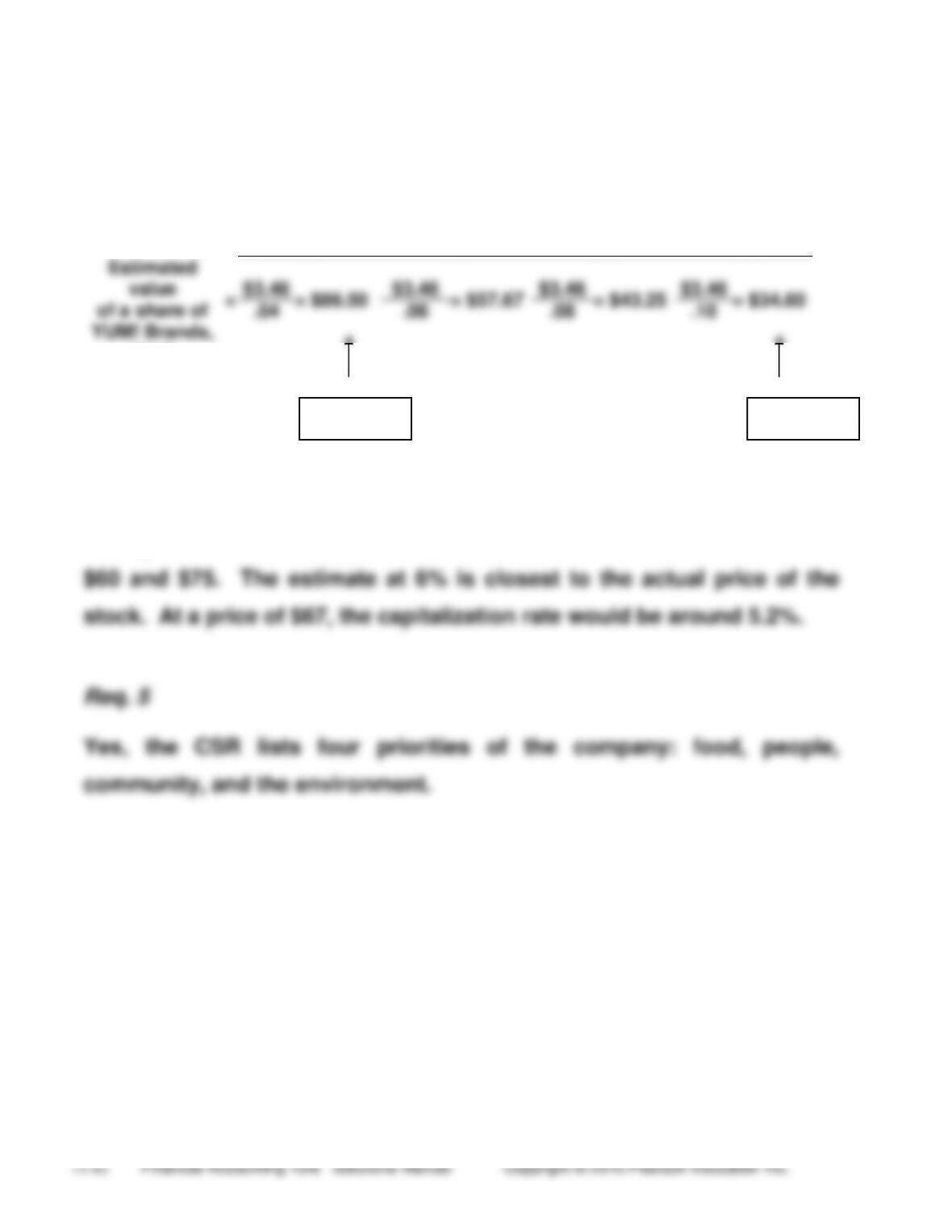

Investment Capitalization Rate

4%

6%

8%

10%

Estimated

value

of a share of

YUM! Brands,

stock

=

$3.46

= $86.50

$3.46

= $57.67

$3.46

= $43.25

$3.46

= $34.60

.04

.06

.08

.10

Req. 4

During the first six months of 2013, YUM! Brands’ stock traded between

Low Risk

High Risk

Chapter 11 Evaluating Performance: Earnings Quality, the Income Statement, & the Statement of Comprehensive Income

11–63

Group Project

1-2 hours