(10-15 min.) E 9-24A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

a.

Jan.

31

Cash ($6,000,000 × 0.96) …………………..

5,760,000

Discount on Bonds Payable …………….

240,000

Bonds Payable ………………………….

6,000,000

To issue bonds at a discount.

b.

July

31

Interest Expense ……………………………..

129,000

Cash ($6,000,000 × .035 × 6/12) …..

105,000

Discount on Bonds Payable

($240,000 / 10) ……………………….

24,000

To pay interest and amortize bond

discount.

c.

Dec.

31

Interest Expense ……………………………..

107,500

Interest Payable

($6,000,000 × .035 × 5/12) ……….

87,500

Discount on Bonds Payable

($240,000 / 10 × 5/6) ……………….

20,000

To accrue interest and amortize bond

discount.

(10-15 min.) E 9-25A

1.

Cash received = $200,000 × 1.06 =

$212,000

2.

Principal ……………………………………………………………..

$200,000

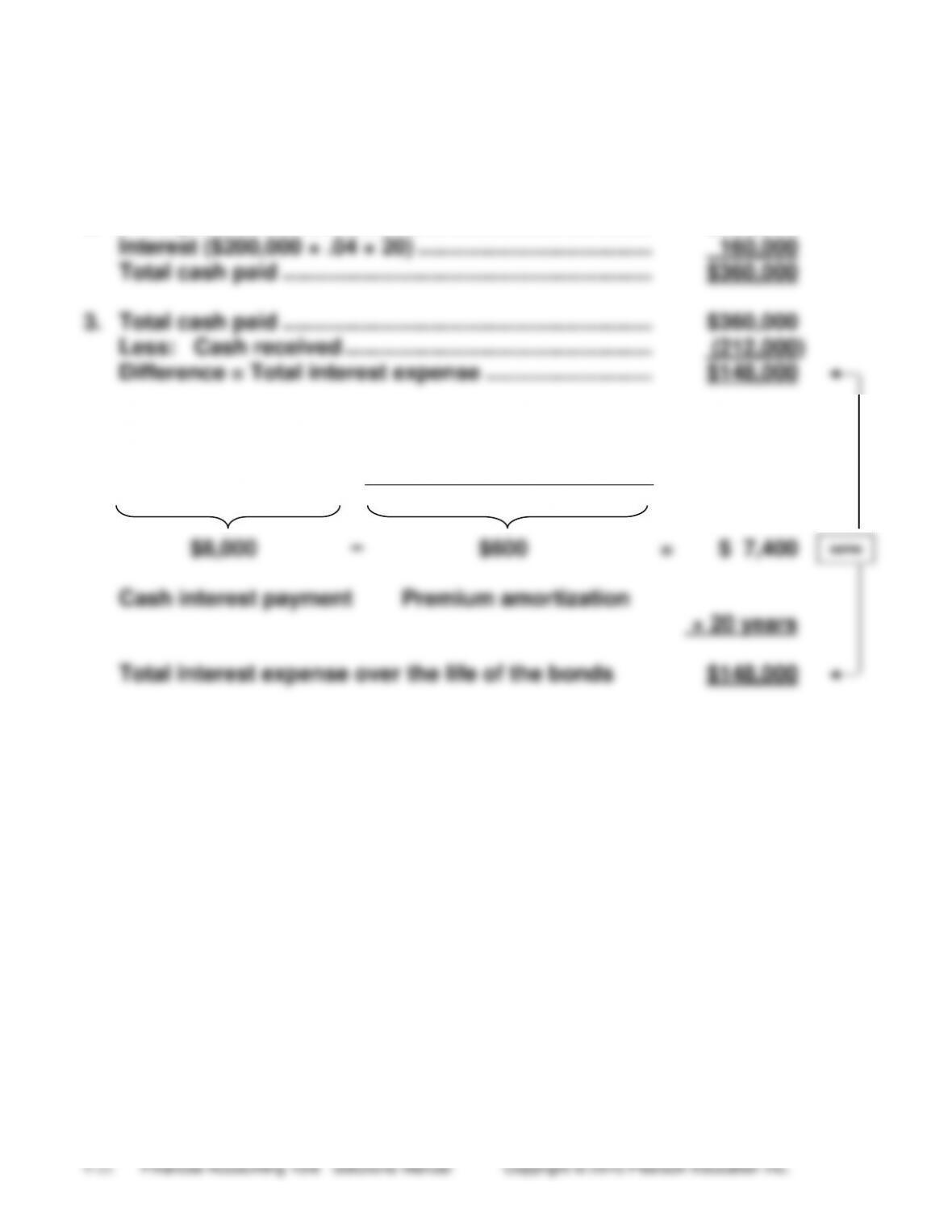

Interest ($200,000 × .04 × 20) ………………………………..

160,000

Total cash paid ……………………………………………………

$360,000

3.

Total cash paid ……………………………………………………

$360,000

Less: Cash received …………………………………………..

(212,000)

Difference = Total interest expense ………………………

$148,000

4.

Annual interest expense by the straight-line amortization method:

$200,000 × .04

$200,000 × (1.06 − 1.00)

20

$8,000

−

$600

=

$ 7,400

Cash interest payment

Premium amortization

× 20 years

Total interest expense over the life of the bonds

$148,000

same

(15-20 min.) E 9-26A

Req. 1 Using the PV function in EXCEL, the issue price of the bonds is

$3,688,217.

Req. 2 (amortization table)

A

B

C

D

E

Semiannual

Interest Date

Interest

Payment

(2% of

Maturity

Value)

Interest

Expense

(2.5% of

Preceding

Bond

Carrying

Amount)

Discount

Amortization

(B – A)

Discount

Account

Balance

(Preceding

D – C)

Bond

Carrying

Amount

($4,000,000

– D)

Dec. 31, 2014

311,783

3,688,217

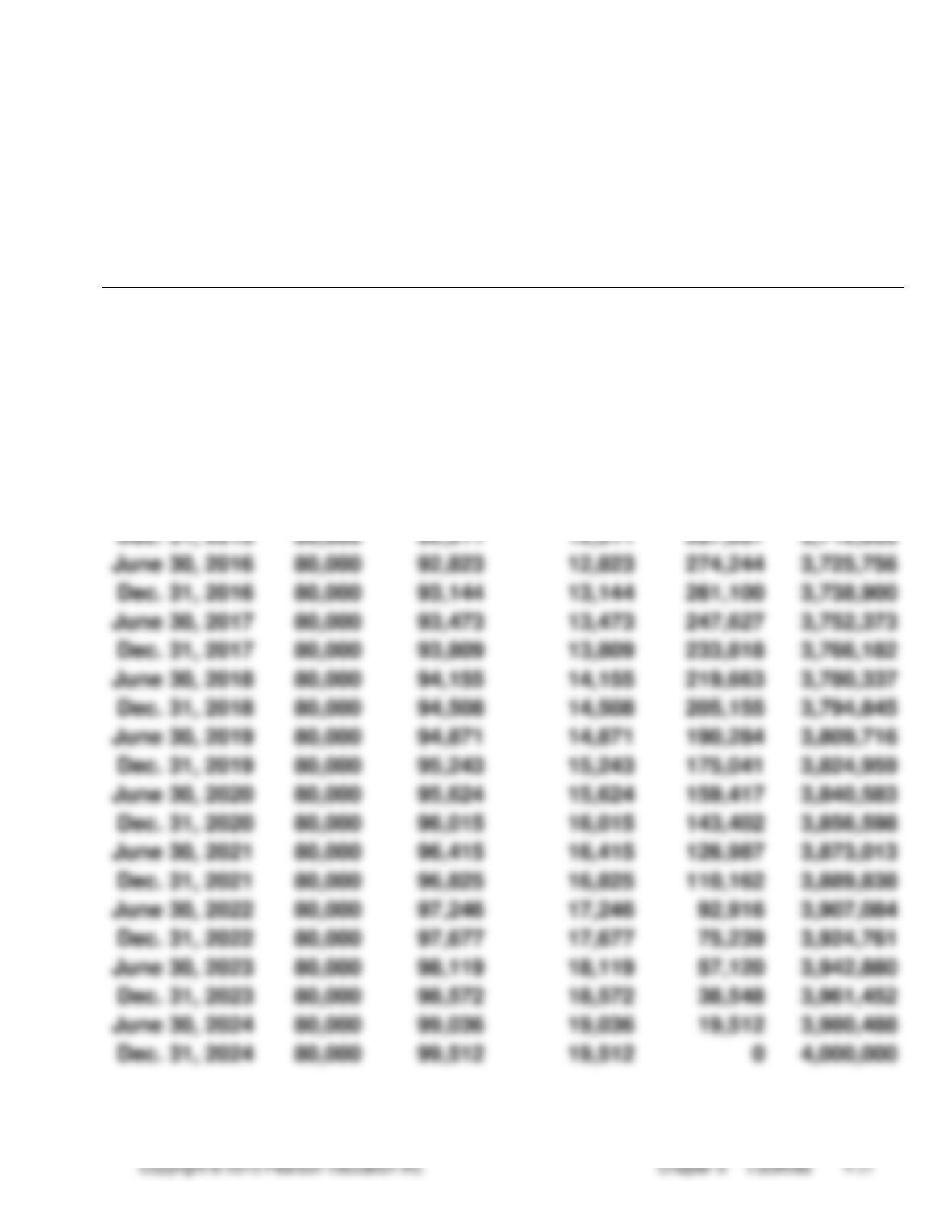

June 30, 2015

80,000

92,205

12,205

299,578

3,700,422

Dec. 31, 2015

80,000

92,511

12,511

287,067

3,712,933

June 30, 2016

80,000

92,823

12,823

274,244

3,725,756

Dec. 31, 2016

80,000

93,144

13,144

261,100

3,738,900

June 30, 2017

80,000

93,473

13,473

247,627

3,752,373

Dec. 31, 2017

80,000

93,809

13,809

233,818

3,766,182

June 30, 2018

80,000

94,155

14,155

219,663

3,780,337

Dec. 31, 2018

80,000

94,508

14,508

205,155

3,794,845

June 30, 2019

80,000

94,871

14,871

190,284

3,809,716

Dec. 31, 2019

80,000

95,243

15,243

175,041

3,824,959

June 30, 2020

80,000

95,624

15,624

159,417

3,840,583

Dec. 31, 2020

80,000

96,015

16,015

143,402

3,856,598

June 30, 2021

80,000

96,415

16,415

126,987

3,873,013

Dec. 31, 2021

80,000

96,825

16,825

110,162

3,889,838

June 30, 2022

80,000

97,246

17,246

92,916

3,907,084

Dec. 31, 2022

80,000

97,677

17,677

75,239

3,924,761

June 30, 2023

80,000

98,119

18,119

57,120

3,942,880

Dec. 31, 2023

80,000

98,572

18,572

38,548

3,961,452

June 30, 2024

80,000

99,036

19,036

19,512

3,980,488

Dec. 31, 2024

80,000

99,512

19,512

0

4,000,000

(continued) E 9-26A

Req. 3

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Dec.

31

Cash ……………………………………………..

3,688,217

Discount on Bonds Payable ……………

311,783

Bonds Payable ………………………….

4,000,000

To issue bonds at a discount.

2015

June

30

Interest Expense …………………………...

92,205

Cash …………………………………………

80,000

Discount on Bonds Payable ……….

12,205

To pay semiannual interest and

amortize bond discount.

2015

Dec.

31

Interest Expense …………………………...

92,511

Cash …………………………………………

80,000

Discount on Bonds Payable ……….

12,511

To pay semiannual interest and

amortize bond discount.

(15-20 min.) E 9-27A

Req. 1 Using the PV function in EXCEL, the issue price of the bonds is

$4,571,885.

Req. 2 (amortization table on next page)

Req. 3 (journal entries)

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

June

30

Cash ………………………………………………….

4,571,885

Bonds Payable ……………………………….

4,000,000

Premium on Bonds Payable ……………

571,885

To issue bonds at a premium.

Dec.

31

Interest Expense …………………………………

80,008

Premium on Bonds Payable ………………..

9,992

Cash ……………………………………………..

90,000

To pay semiannual interest and amortize

bond premium.

2015

June

30

Interest Expense …………………………………

79,833

Premium on Bonds Payable ………………..

10,167

Cash ……………………………………………..

90,000

To pay semiannual interest and amortize

bond premium.

A

B

C

D

E

Semiannual

Interest Date

Interest

Payment

(2.25% of

Maturity Value)

Interest Expense

(1.75% of Preceding

Bond Carrying

Amount)

Premium

Amortization

(A – B)

Premium

Account Balance

(Preceding D – C)

Bond Carrying

Amount

($4,000,000 + D)

June 30, 2014

571,885

4,571,885

Dec. 31, 2014

90,000

80,008

9,992

561,893

4,561,893

June 30, 2015

90,000

79,833

10,167

551,726

4,551,726

Dec. 31, 2015

90,000

79,655

10,345

541,381

4,541,381

June 30, 2016

90,000

79,474

10,526

530,855

4,530,855

Dec. 31, 2016

90,000

79,290

10,710

520,145

4,520,145

June 30, 2017

90,000

79,103

10,897

509,248

4,509,248

Dec. 31, 2017

90,000

78,912

11,088

498,160

4,498,160

June 30, 2018

90,000

78,718

11,282

486,878

4,486,878

Dec. 31, 2018

90,000

78,520

11,480

475,398

4,475,398

June 30, 2019

90,000

78,319

11,681

463,717

4,463,717

Dec. 31, 2019

90,000

78,115

11,885

451,833

4,451,833

June 30, 2020

90,000

77,907

12,093

439,740

4,439,740

Dec. 31, 2020

90,000

77,695

12,305

427,435

4,427,435

June 30, 2021

90,000

77,480

12,520

414,915

4,414,915

Dec. 31, 2021

90,000

77,261

12,739

402,176

4,402,176

June 30, 2022

90,000

77,038

12,962

389,214

4,389,214

Dec. 31, 2022

90,000

76,811

13,189

376,026

4,376,026

June 30, 2023

90,000

76,580

13,420

362,606

4,362,606

Dec. 31, 2023

90,000

76,346

13,654

348,952

4,348,952

June 30, 2024

90,000

76,107

13,893

335,058

4,335,058

Dec. 31, 2024

90,000

75,864

14,136

320,922

4,320,922

June 30, 2025

90,000

75,616

14,384

306,538

4,306,538

Dec. 31, 2025

90,000

75,364

14,636

291,902

4,291,902

June 30, 2026

90,000

75,108

14,892

277,011

4,277,011

Dec. 31, 2026

90,000

74,848

15,152

261,858

4,261,858

June 30, 2027

90,000

74,583

15,417

246,441

4,246,441

Dec. 31, 2027

90,000

74,313

15,687

230,753

4,230,753

June 30, 2028

90,000

74,038

15,962

214,792

4,214,792

Dec. 31, 2028

90,000

73,759

16,241

198,551

4,198,551

June 30, 2029

90,000

73,475

16,525

182,025

4,182,025

Dec. 31, 2029

90,000

73,185

16,815

165,211

4,165,211

June 30, 2030

90,000

72,891

17,109

148,102

4,148,102

Dec. 31, 2030

90,000

72,592

17,408

130,694

4,130,694

June 30, 2031

90,000

72,287

17,713

112,981

4,112,981

Dec. 31, 2031

90,000

71,977

18,023

94,958

4,094,958

June 30, 2032

90,000

71,662

18,338

76,620

4,076,620

Dec. 31, 2032

90,000

71,341

18,659

57,960

4,057,960

June 30, 2033

90,000

71,014

18,986

38,975

4,038,975

Dec. 31, 2033

90,000

70,682

19,318

19,657

4,019,657

June 30, 2034

90,000

70,344

19,657

0

4,000,000

(15-20 min.) E 9-28A

Req. 1

The company has the right to occupy space and operate out of leased

(20-25 min.) E 9-29A

Amounts in millions or billions

Company

Company

Company

Ratio

B

N

V

Current

=

Total current assets

=

$429

¥5,321

€144,720

ratio

Total current liabilities

$227

¥2,217

€ 72,500

= 1.89

= 2.40

= 2.00

B

N

V

Debt

= =

Total liabilities

=

$227 + $86

¥2,217 + ¥2,277

€72,500 + €111,177

ratio

Total assets

$429 + $99

¥5,321 + ¥592

€144,720 + €65,828

= 0.59

= 0.76

= 0.87

B

N

V

Leverage

ratio

=

Total assets

=

$528

¥5,913

€210,548

Tot. stockholders’

equity

$215

¥1,419

€26,871

= 2.46

= 4.17

= 7.84

B

N

V

Times-

interest-

=

Operating income

=

$259

¥230

€5,746

earned

Interest expense

$41

¥27

€655

ratio

= 6.3 times

= 8.5 times

= 8.8 times

Student responses may vary, but based on the information given,

company B looks the least risky, with relatively high current ratio and

times-interest earned coverage, and relatively low debt ratio.

(15-20 min.) E 9-30A

Req. 1

PLAN A

BORROW

$600,000

AT 4%

PLAN B

ISSUE

$600,000

OF COMMON

STOCK

Net income before expansion ……………………

$350,000

$350,000

Project income before interest and income tax

$500,000

$500,000

Less interest expense ($600,000 × .04) ………

24,000

-0-

Project income before income tax……………..

476,000

500,000

Less: income tax expense (25%) ……………….

(119,000)

(125,000)

Project net income …………………………………..

357,000

375,000

Total company net income ……………………

$707,000

$725,000

Earnings per share including new project:

Plan A ($707,000 / 120,000 shares) ………..

$5.89

Plan B ($725,000 / 320,000 shares) ………..

$2.27

(continued) E 9-30A

Req. 2

MEMORANDUM

TO: Board of Directors of BBS Financial Services

FROM: Student Name

SUBJECT: Financing plan to expand operations

Plan A (borrowing) results in much higher earnings per share. Plan A

also allows the existing stockholders to retain control of the company

(5-15 min.) E 9-31B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Warranty Expense ($147,000 × .09) …………

13,230

Estimated Warranty Payable ………………

13,230

Estimated Warranty Payable …………………..

9,200

Cash …………………………………………………

9,200

Req. 2

INCOME STATEMENT

Sales revenue ……………………………………………………

$147,000

Warranty expense ……………………………………………..

13,230

BALANCE SHEET

Current liabilities

Estimated warranty payable

($2,800 + $13,230 − $9,200) …………………………..

$ 6,830

Req. 3

(10-15 min.) E 9-32B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Oct.

1

Cash ……………………………………………………….

2,354

Unearned Subscription Revenue…………..

2,200

Sales Tax Payable ($2,200 × .07) …………..

154

Nov.

15

Sales Tax Payable ……………………………………

154

Cash……………………………………………………

154

Dec.

31

Unearned Subscription Revenue ………………

550

Subscription Revenue ($2,200 × 3/12) ……

550

BALANCE SHEET

Current liabilities:

Unearned subscription revenue ($2,200 − $550) ………………

$1,650

(10 min.) E 9-33B

INCOME STATEMENT

Expenses:

Payroll expense ………………………………………………………

$168,000

Payroll tax expense ($168,000 × .08) …………………………

13,440

BALANCE SHEET

Current liabilities:

Salary payable ………………………………………………………..

$ 7,900

Payroll tax payable ………………………………………………….

915

(5-10 min.) E 9-34B

Req. 1

Interest to

accrue at

=

$54,000 × .03 × 3/12

=

$405

Dec. 31, 2014

Req. 2

Final payment

=

$54,000 + ($54,000 × .03)

=

$55,620

on October 1, 2015

Req. 3

Interest expense for:

2014

=

$54,000 × .03 × 3/12

=

$ 405

2015

=

$54,000 × .03 × 9/12

=

$1,215

(10-15 min.) E 9-35B

Branson’s balance sheet at Dec. 31, 2015 reported:

Income tax payable ………………………………………………..

$146,200*

Branson’s 2015 income statement reported:

Income tax expense ($1,040,000 × .36) …………………….

$374,400

_____

* Beginning income tax payable ………………………………………

$105,000

+ Income tax expense (and payable) for the year

($1,040,000 × .36) …………………………………………………………

374,400

− Income tax payments during the year …………………………...

(333,200)

= Ending income tax payable …………………………………………..

$146,200

(10-20 min.) E 9-36B

Req. 1

Accounts payable are amounts owed to suppliers for products or

services that have been purchased on account.

(continued) E 9-36B

Req. 2

Total assets = $4,037 million, the sum of total liabilities and

stockholders’ equity.

(in millions) 2014

Leverage

ratio

=

Total assets ($4,037)

Total stockholders’ equity ($2,027)

=

1.99

Debt ratio

=

Total liabilities ($4,037 − $2,027)*

=

0.50

Total assets ($4,037)

For 2013, the leverage ratio was 2.24 and the debt ratio was .55.

____

*Or, $365 + $1,487 + $138 + $20 = $2,010

Req. 3

2014 2013

Accounts

payable

turnover

Cost of goods sold

$1,765

= 11.4

$2,046

= 11.0

Average accounts

payable

$155*

$186**

*($134 + $176) / 2

**($176 + $195) / 2

Days

payable

outstanding

365

365

= 32.0

365

= 33.2

Accts. payable

turnover

11.4

11.0

Current

ratio

Current assets

$638

= 1.75

$604

= 1.63

Current liabilities

$365

$371

(5-10 min.) E 9-37B

Req. 1

Nguyen Security Systems should report this situation in a note to the

financial statements. It is the company’s policy to disclose legal

Req. 2

Nguyen would report:

INCOME STATEMENT

Estimated loss (or expense) due to lawsuit

contingency …………………………………….

$1,700,000

BALANCE SHEET

Estimated liability due to lawsuit contingency

$1,700,000

The note disclosure would be similar to Requirement 1.

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Estimated Loss from Lawsuit Contingency ………

1,700,000

Estimated Liability from Lawsuit Contingency

1,700,000

(15-20 min.) E 9-38B

Pippin Electronics

Balance Sheet (partial)

June 30, 2014

Current liabilities:

a. Estimated warranty payable

[$29,000 + ($1,900,000 × .06) − $46,000] ………………..

$97,000

b. Current portion of long-term note payable ………………..

10,500

Interest payable ($42,000 × .04 × 1/12) ………………………

140

c. Unearned sales revenue ($125,000 − $85,000) ……………

40,000

d. Employee withheld income tax payable ……………………

28,300

FICA tax payable ($270,000 × .0765) ………………………….

20,655

Total current liabilities ………………………………………..

$196,595

Long-term liabilities:

Note payable ($42,000 − $10,500) ……………………………..

$ 31,500

(10-15 min.) E 9-39B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

a.

Jan.

31

Cash ($8,000,000 × 0.93) ………………..

7,440,000

Discount on Bonds Payable …………..

560,000

Bonds Payable …………………………

8,000,000

To issue bonds at a discount.

b.

July

31

Interest Expense …………………………..

228,000

Cash ($8,000,000 × .05 × 6/12) ……

200,000

Discount on Bonds Payable

($560,000 / 20) ………………………

28,000

To pay interest and amortize bond

discount.

c.

Dec.

31

Interest Expense …………………………..

190,000

Interest Payable

($8,000,000 × .05 × 5/12) ………..

166,667

Discount on Bonds Payable

($28,000 × 5/6) ………………………

23,333

To accrue interest and amortize bond

discount.

(10-15 min.) E 9-40B

1.

Cash received = $400,000 × 1.02 =

$408,000

2.

Principal ……………………………………………………………..

$400,000

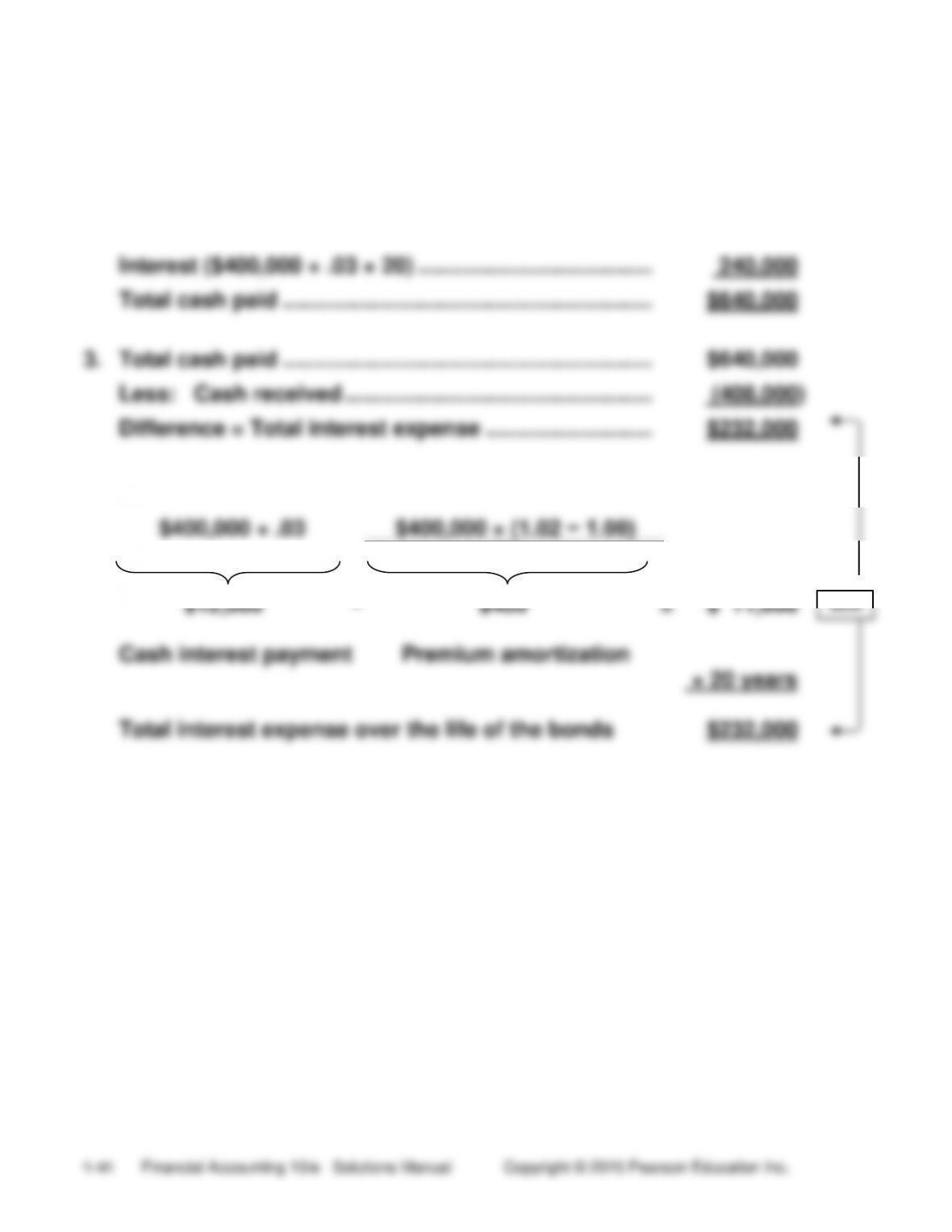

Interest ($400,000 × .03 × 20) ………………………………..

240,000

Total cash paid ……………………………………………………

$640,000

3.

Total cash paid ……………………………………………………

$640,000

Less: Cash received …………………………………………..

(408,000)

Difference = Total interest expense ………………………

$232,000

4.

Annual interest expense by the straight-line amortization method:

$400,000 × .03

$400,000 × (1.02 − 1.00)

20

$12,000

−

$400

=

$ 11,600

Cash interest payment

Premium amortization

× 20 years

Total interest expense over the life of the bonds

$232,000

same