1) On January 1, 2014, Bucket Company purchased as an investment a $1,000, 7%

bond for $980. Bucket plans to hold the bond until the maturity date of January 1, 2024.

The bond pays interest on January 1 and July 1. The company’s fiscal year ends on

December 31. The journal entry on December 31, 2014 is:

A) debit Interest Receivable for $35, debit Held-to-Maturity Investment in Bond for $1

and credit Interest Revenue for $36

B) debit Cash for $35 and credit Interest Revenue for $35

C) debit Interest Receivable for $36, credit Held-to-Maturity Investment in Bonds for

$1 and credit Interest Revenue for $35

D) debit Held-to-Maturity Investment in Bonds for $35 and credit Interest Revenue for

$35

2) Which of the following statements is TRUE for a limited liability company?

A) Members have unlimited liability for the debts of the business

B) Members have limited liability for the debts of the business

C) Only the limited partners have limited liability for the debts of the business

D) The general partner has unlimited liability for the debts of the business

3) Which of the following items from the bank reconciliation require a journal entry?

A) Bank errors

B) Deposits in transit

C) Outstanding checks

D) Charge for printing of checks

4) A company purchased supplies during the year totaling $20,000. At the end of the

year, they made an adjusting entry to record $15,000 of supplies that had been used

during the year. The ending balance in the Supplies account after the adjustment was

$12,000. The beginning balance in the Supplies account was:

A) $5,000

B) $7,000

C) $8,000

D) $12,000

5) On January 1, 2015, Roadway Delivery Company purchased a truck for $10,000.

Depreciation Expense is $1,000 per year. During the first year of use, the company paid

$1,000 to repaint the truck and $2,000 for new tires. What amount is expensed in the

first year of use of the truck?

A) $1,000

B) $2,000

C) $3,000

D) $4,000

6) Mr. Jorgensen, a shareholder in the Best Corporation, owns 1,000 shares of their

common stock. Mr. Jorgensen receives a 5% stock dividend. After the stock dividend,

Mr. Jorgensen will have a:

A) total of 50 shares of Best Corporation’s common stock

B) total of 950 shares of Best Corporation’s common stock

C) total of 1,000 shares of Best Corporation’s common stock

D) total of 1,050 shares of Best Corporation’s common stock

7) The quick ratio and the number of days’ sales in receivables measure:

A) a company’s cash conversion cycle

B) a company’s profitability

C) a company’s liquidity

D) all of the above

8) Which transaction decreases stockholders’ equity?

A) sale of common stock

B) purchase of equipment with cash

C) Total revenues for the period exceed total expenses for the period

D) Total expenses for the period exceed total revenues for the period

9) Sales revenue is based on the ________ of the inventory, while cost of goods sold is

based on the ________ of the inventory.

A) cost, selling price

B) cost, cost

C) selling price, retail price

D) selling price, cost

10) A measure of the ability of an entity to pay all of its current liabilities if they came

due immediately is the:

A) debt ratio

B) quick ratio

C) liquidity ratio

D) accounts receivable turnover

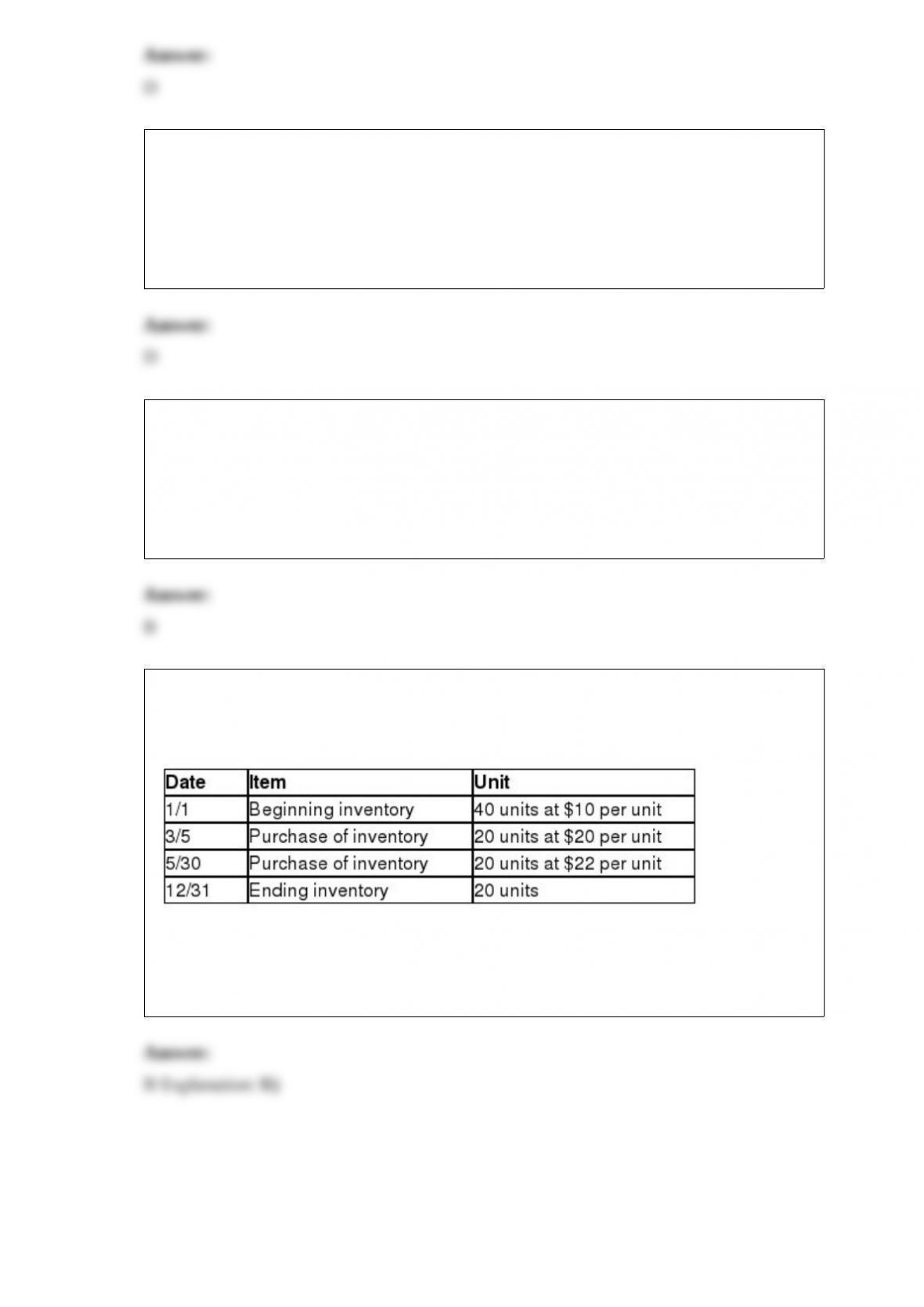

11) Given the following data, calculate the cost of ending inventory using the average

cost method. Round all calculations to the nearest two decimal places.

A) $200

B) $310

C) $400

D) $440

12) The aging-of-receivables method for computing uncollectible accounts:

A) uses an income statement approach

B) focuses on the amount of receivables that will not be collected

C) uses a balance sheet approach

D) B and C

13) The entry made to close Service Revenue would include a debit to:

A) Retained Earnings and a credit to Service Revenue

B) Service Revenue and a credit to Retained Earnings

C) Service Revenue and a credit to Dividends

D) Service Revenue and a credit to Net Income

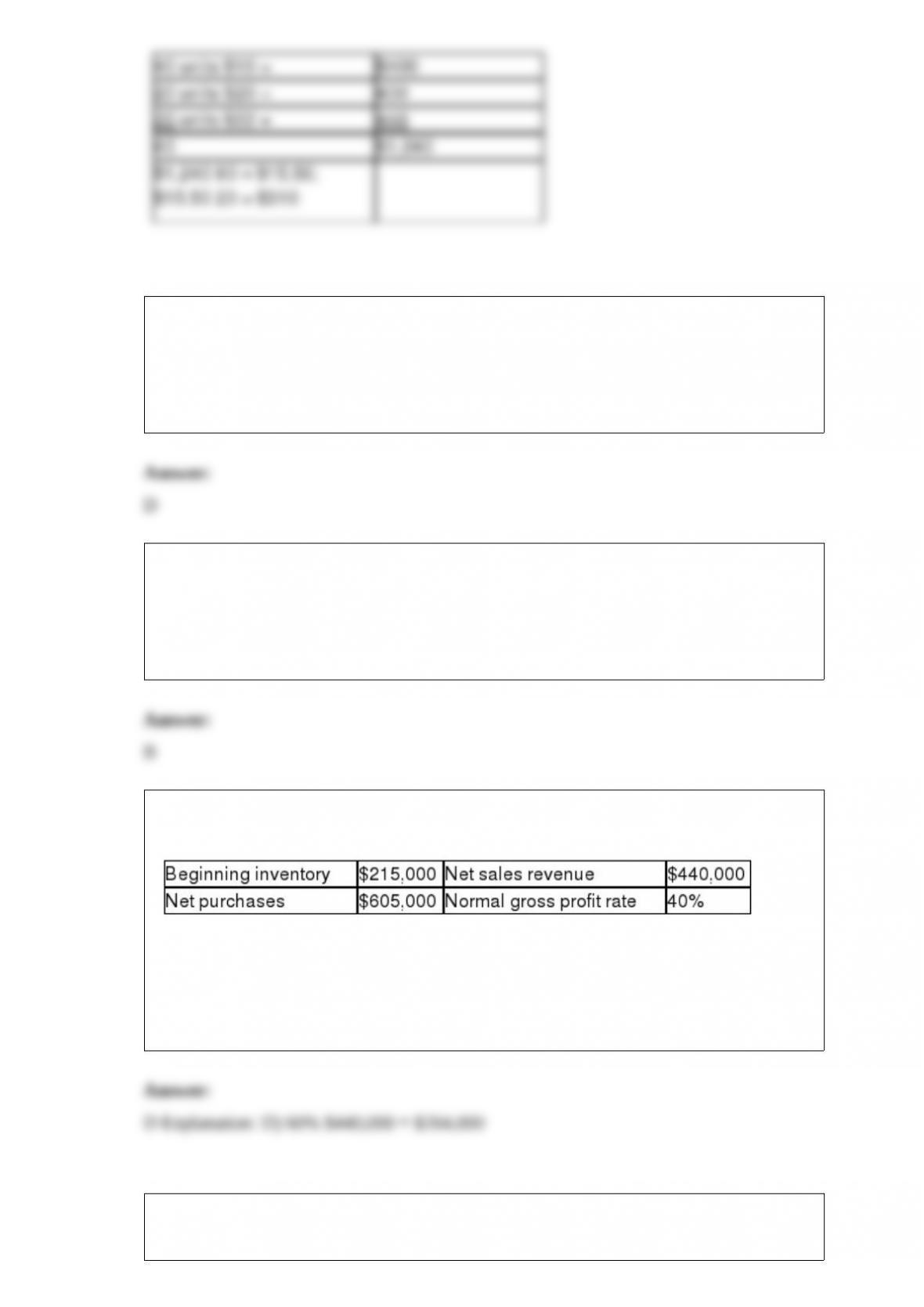

14) The following data are for Jessee’s Candy Store for January:

What is the company’s estimated cost of goods sold for the month?

A) $165,000

B) $176,000

C) $225,000

D) $264,000

15) A bond was issued at a discount. The journal entry to record payment of this bond

payable at maturity will include a:

A) debit to Bonds Payable, credit to Discount on Bonds Payable and a credit to Cash

B) debit to Cash and a credit to Bonds Payable

C) debit to Bonds Payable and a credit to Cash

D) debit to Bonds Payable, debit to Discount on Bonds Payable and a credit to Cash

16) For a plant asset that wears out because of physical use rather than obsolescence,

which depreciation method best meets the expense recognition principle?

A) straight-line

B) double-declining-balance

C) modified accelerated

D) units-of-production

17) A company exchanges an old machine for a new machine and cash is paid for the

new machine. Assume there is a Gain on Exchange of Machine. In the journal entry to

record the exchange by the owner of the old machine, what accounts will the accountant

debit?

A) Machine and Accumulated Depreciation

B) Cash and Machine

C) Accumulated Depreciation, Cash and Machine

D) Accumulated Depreciation, Cash, Machine and Gain on Exchange of Machine

18) An account will have a debit balance if:

A) the amount of the credits exceeds the amount of the debits

B) the amount of the debits exceeds the amount of the credits

C) the account has more debit entries than credit entries

D) it is a liability account

19) Net income is computed as:

A) revenues – expenses – dividends

B) revenues + expenses

C) revenues – expenses

D) revenues – expenses + dividends

20) The depreciation process follows the ________ principle.

A) revenue recognition

B) expense recognition

C) disclosure

D) consistency

21) All of the following are needed to measure depreciation, EXCEPT for:

A) cost

B) market value

C) estimated useful life

D) estimated residual value

22) The journal entry to record accrued interest on a short-term note payable must

include a debit to:

A) Interest Payable and a credit to Cash

B) Interest Expense and a credit to Cash

C) Interest Expense and a credit to Interest Payable

D) Interest Payable and a credit to Notes Payable

23) Dammer Corporation wants to raise $2,000,000. The corporation plans to sell 7%,

10-year bonds at the face value of $2,000,000. Dammer Corporation currently has

150,000 shares of stock outstanding and net income of $1,500,000. The $2,000,000

from the bond sale is expected to generate additional income of $500,000 before

interest and taxes. The income tax rate is 30%. What are the earnings per share after the

sale of bonds?

A) $10.00

B) $11.68

C) $12.33

D) $12.40

24) The independent auditors’ report is addressed to:

A) management

B) board of directors only

C) stockholders only

D) board of directors and stockholders

25) Marjorie Company’s cash balance per the books at the end of the month was $6,500.

After comparing the company’s records with the monthly bank statement, Marjorie’s

accountant identified the following reconciling items: outstanding checks, $800;

deposits in transit, $700; bank service charge, $30; and NSF check, $500. The bank

collection of a note receivable was $1,000 plus interest of $100. There also was an EFT

payment of $100. What is the adjusted book balance at the end of the month?

A) $5,970

B) $6,400

C) $6,500

D) $6,970

26) Assume it is the first year of operations. When pretax accounting income exceeds

taxable income, a:

A) Deferred Tax Asset is debited

B) Deferred Tax Liability is credited

C) Deferred Tax Asset is credited

D) Deferred Tax Liability is debited

27) Brankov Company has current assets of $105,000 and current liabilities of $40,000.

The company decides to issue stock and receives cash of $70,000. After this

transaction, the company’s current ratio will be:

A) 0.68

B) 1.88

C) 3.62

D) 4.38

28) A potential investor interested in predicting the earnings of a company in the future

should examine the:

A) Balance Sheet only

B) Income Statement only

C) Statement of Retained Earnings

D) statement of Retained Earnings and Balance Sheet

29) Leno Company sells goods to the Fallon Company for $10,000. It offers credit

terms of 5/10, n/30. If Fallon Company pays the invoice within the discount period,

Leno Company will record a debit to Cash in the amount of:

A) $0

B) $9,000

C) $9,500

D) $10,000

30) At the end of the current accounting period, account balances were as follows:

Cash, $25,000; Accounts Receivable, $40,000; Common Stock, $18,000; Retained

Earnings, $14,000. Liabilities for the period were:

A) $13,000

B) $20,000

C) $27,000

D) $33,000

31) When preparing a cash budget, the budgeted balance is:

A) the beginning cash balance

B) the budgeted cash payments

C) the minimum amount of cash the company needs

D) the budgeted cash receipts

32) On a bank reconciliation, electronic fund transfers are:

A) additions or deductions to the bank balance

B) additions or deductions to the book balance

C) not put on the bank reconciliation

D) only used for journal entries

33) A recent cash budget showed estimated cash receipts of $159,000, estimated cash

disbursements of $155,000, and a desired ending cash balance of $6,000, with no

borrowing of funds. The beginning cash balance was:

A) $2,000

B) $4,000

C) $10,000

D) unknown

34) A conservative policy with regard to capitalizing or expensing costs associated with

plant assets avoids _________.

A) understating profits and assets

B) overstating profits and assets

C) overstating profits and understating assets

D) understating profits and overstating assets

35) Using the indirect method to calculate net cash provided by operating activities, a

decrease in prepaid expenses is:

A) subtracted from net income

B) added to net income

C) ignored since it does not affect expenses

D) ignored since it does not affect net income

36) The net realizable value of accounts receivable is the difference between gross

accounts receivable and:

A) Sales Discounts

B) Sales Returns and Allowances

C) Uncollectible-Account Expense

D) Allowance for Uncollectible Accounts

37) Footnotes about a company’s segments provide information about the:

A) different types of business activities

B) geographic areas covered

C) product lines offered

D) all of the above

38) In performing vertical analysis, the base for income tax expense is:

A) net sales

B) gross revenues

C) net income

D) gross profit

39) Yellow Company had a balance of $30,000 in Accounts Payable at the beginning of

June, and purchased $100,000 of merchandise on account during the month At the end

of June, Yellow’s Account Payable balance was $28,000 What amount did Yellow pay

on account during June?

A) $62,000

B) $72,000

C) $100,000

D) $102,000