Challenge Exercises and Problem

(20-30 min.) E 12-76

(All amounts in thousands)

Decrease in

Sales

+

Accounts Receivable

a.

Collections

=

$25,133

=

$25,118

+

($612 − $597)

Cost

Increase in

Increase in

− Accounts

b.

Payments for

of sales

+

Inventory

Payable

inventory

=

$18,248

=

$18,162

+

$267*

−

$181**

*$3,100 − $2,833 = $267

**$1,549 − $1,368 = $181

Other Operating

Increase in

c.

Payments for

Expenses

− Accrued Liabilities

other

operating

=

$3,582

=

$3,885

− ($939 − $636)

expenses

Increase in

d.

Payment of

Tax Expense −

Income Tax Payable

income tax

=

$529

=

$537 −

($198 − $190)

e.

Proceeds from

Beg. Common

End. Common

issuance of

Stock

+

Issuance

= Stock

stock

=

$75

=

$443

+

X

= $518

X

= $75

Beg. Ret.

Net

End. Ret.

f.

Payment of

Earnings

+

Income

− Dividends

= Earnings

dividends

=

$1,675

$3,783

+

$2,266

− X

= $4,374

X

= $1,675

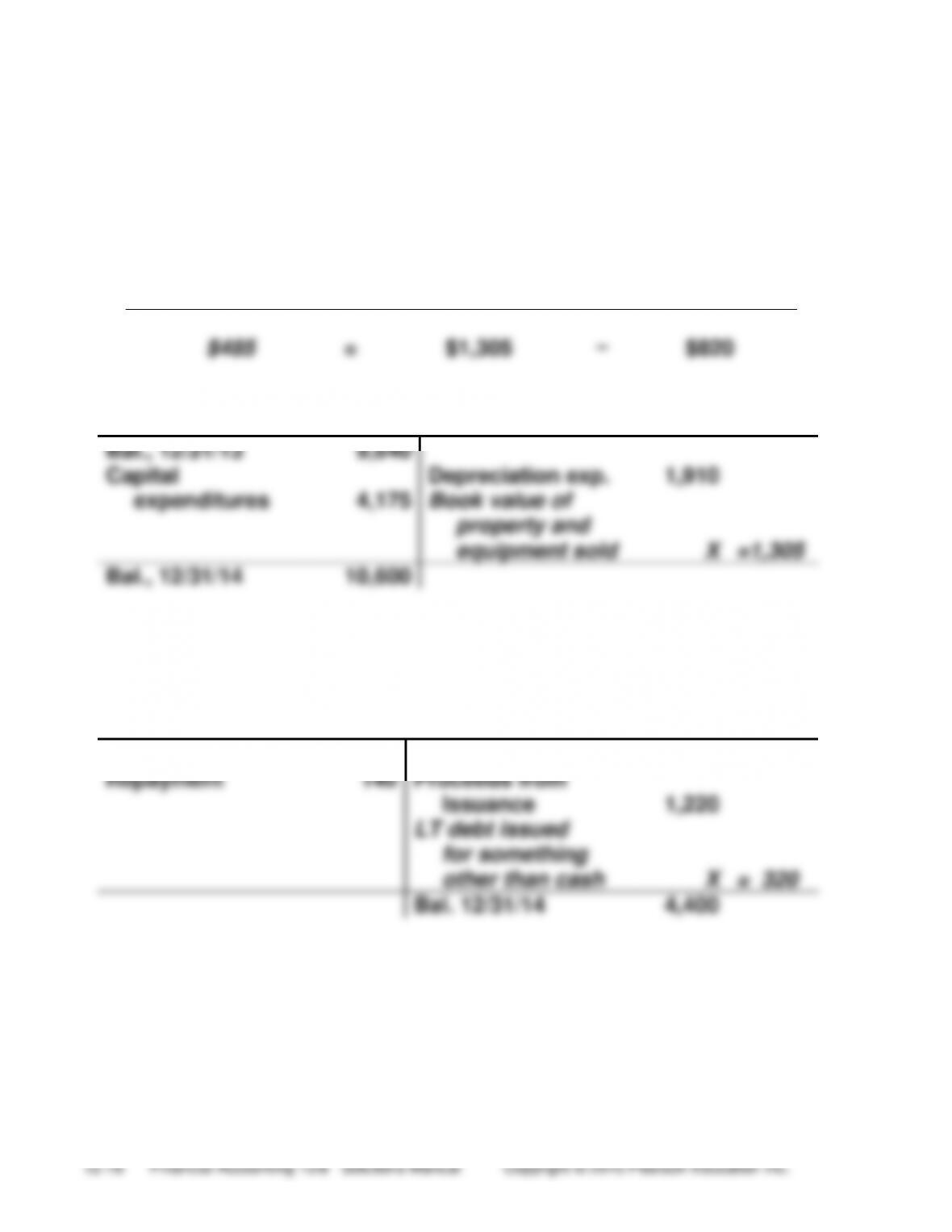

(20 min.) E 12-77

a.

(All in thousands)

Loss on sale of

Book value of

assets sold

Proceeds from

sale of assets

property and

=

−

equipment

$485

=

$1,305

−

$820

Property & Equipment, Net

Bal., 12/31/13

9,640

Capital

Depreciation exp.

1,910

expenditures

4,175

Book value of

property and

equipment sold

X

=1,305

Bal., 12/31/14

10,600

b.

Long-Term Notes Payable

Bal., 12/31/13

3,000

Repayment

140

Proceeds from

Issuance

1,220

LT debt issued

for something

other than cash

X

= 320

Bal. 12/31/14

4,400

P 12–78

Assets:

December

31, 2013

December

31, 2014

Cash and cash

equivalents

$11,000

$63,000

Given

Accounts receivable

(net)

92,000

82,000

($92,000 – $10,000)

Inventory

103,000

110,000

($103,000 + $7,000)

Prepaid expenses

6,000

5,000

($6,000 – $1,000)

Land

69,000

64,000

[$69,000 – ($11,000 –

$6,000)]

Machinery and

equipment (net)

59,000

44,000

[59,000 + $25,000 –

($9,000 + $15,000) –

$16,000]

Total assets

$340,000

$368,000

Liabilities:

Accounts payable

$66,000

$78,000

($66,000+ $12,000)

Unearned revenue

1,000

2,500

($1,000 + $1,500)

Dividends payable

-0-

2,000

($7,000 – $5,000)

Income taxes payable

4,000

1,500

($4,000 – $2,500)

Long-term debt

75,000

59,000

($75,000 – $16,000)

Total liabilities

146,000

143,000

Stockholders’ equity:

Common stock, no par

26,000

46,000

($26,000 + $20,000)

Retained earnings

168,000

179,000

($168,000 + $18,000 –

$7,000)

Total stockholders’ equity

194,000

225,000

Total liabilities and

stockholders’ equity

$340,000

$368,000

Decision Cases

(45-60 min.) Decision Case 1

Req. 1 (indirect method for operating activities)

T-Bar-M Camp, Inc.

Statement of Cash Flows

Year Ended December 31, 2014

Cash flows from operating activities:

(Thousands)

Net income …………………………………………………………..

$ 97

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense ……………………………………..

$ 46

Amortization of patents …………………………………..

11

Increase in accounts receivable ($72 − $61) ……..

(11)

Increase in inventories ($194 − $181) ……………….

(13)

Increase in accounts payable ($63 − $56) …………

7

Decrease in accrued liabilities ($17 − $12) ………..

(5)

35

Net cash provided by operating activities ……………

132

Cash flows from investing activities:

Purchase of property, plant, and

equipment ($369 − $259) …………………………………….

$(110)

Purchase of long-term investments ($31 − $0) ………..

(31)

Net cash used for investing activities ………………….

(141)

Cash flows from financing activities:

Issuance of common stock ($149 − $61) …………………

$ 88

Payment of cash dividends ($156 + $97 − $213) ………

(40)

Payment of long-term notes payable ($264 − $179) …

(85)

Net cash used for financing activities ………………….

(37)

Net (decrease) in cash ……………………………………………..

$ (46)

Cash balance, December 31, 2013 …………………………....

63

Cash balance, December 31, 2014 …………………………….

$ 17

(continued) Decision Case 1

Req. 2

The cash balance at the end of 2014 is low because:

• The camp paid $110,000 to buy new property, plant, and

equipment.

Req. 3

Year 2014 was a good year. Net income was $97,000, and operations

(15-25 min.) Decision Case 2

Four-Star Catering looks like the better investment because:

1. Operations provide far more cash for Four-Star than for Applied

Technology. Operations should be the main source of cash for a

healthy company.

Ethical Issue

Req. 1

Cash flows from operating

activities:

Without

Reclassification

With

Reclassification

Net income ……………………….

$ 37,000

$37,000

Increase in accounts

receivable ………………………..

(80,000)

—

Net cash (used for) provided

by operating activities …………..

$(43,000)

$37,000

Columbia looks better with the reclassification because net

cash flow from operations is positive.

(continued) Ethical case

Legal analysis: To reclassify receivables when, in fact, they are not truly

collectible, even in the long run, might leave the company open later to a

lawsuit for damages suffered by creditors who loan Columbia money

based on false information.

Focus on Financials: Amazon.com, Inc.

(40-50 min.)

Req. 1

Amazon.com uses the indirect method to report operating cash flows.

You can tell because the statement begins with net income.

Req. 2 (Amounts in millions)

a. Note 1 provides the balance of Allowance for Doubtful accounts

Gross Accounts Receivable, Vendors and Customers

Beg. Bal. ($2,571 + $82)

2,653

Sales (income statement)

61,093

Write-offs (see below)

271

Collections ($2,653 +

$61,093 – $3,480 – $271)

59,995

End. Bal. ($3,364 + $116)

3,480

Allowance for Doubtful Accounts

Beg. Bal.

82

Write-offs ($82 + $305 –

Doubtful accounts expense

$116)

271

($61,093 x .005)

305

End. Bal.

116

(continued) Amazon.com

b. Using the format provided in Exhibit 12-15: (Amounts in millions)

Payments for

=

Cost of

+

Increase in

−

Increase in

inventory

sales

Inventory

Accounts Payable

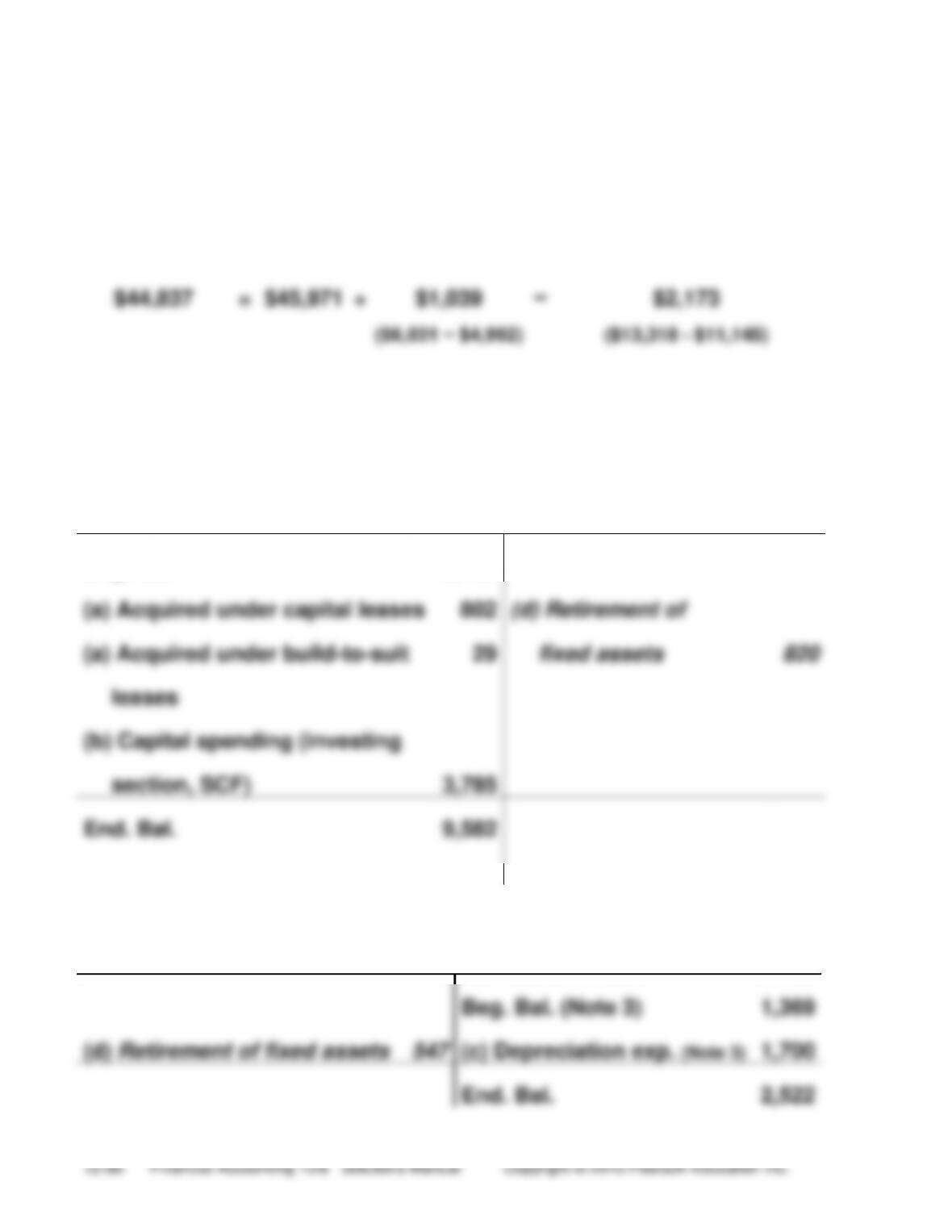

$44,837

=

$45,971

+

$1,039

−

$2,173

($6,031 − $4,992)

($13,318 – $11,145)

c. (Amounts in millions) From Note 3 and the Statement of Cash

Flows:

Gross Property and Equipment

Beg. Bal.

5,786

(a) Acquired under capital leases

802

(d) Retirement of

(a) Acquired under build-to-suit

29

fixed assets

820

leases

(b) Capital spending (investing

section, SCF)

3,785

End. Bal.

9,582

Accumulated Depreciation

Beg. Bal. (Note 3)

1,369

(d) Retirement of fixed assets

547

(c) Depreciation exp. (Note 3)

1,700

End. Bal.

2,522

(continued) Amazon.com

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

(a)

Leased Property and Equipment ………………

802

Built-to-suit Leases – Property & Eq. ………..

29

Long-term Debt ……………………………………

831

(b)

Property and Equipment ………………………….

3,785

Cash …………………………………………………..

3,785

(c)

Depreciation Expense ………………………………

1,700

Accumulated Depreciation …………………..

1,700

(d)

Accumulated Depreciation ……………………….

547

Loss on Retirement ………………………………….

273

Property and Equipment ………………………

820

The loss on retirement of fixed assets equals the remaining net book

value of the fixed asset retired. This loss would be reported in the

income statement as part of other income (expense).

d. In 2012, for Amazon.com, Inc.,

Focus on Analysis: YUM! Brands, Inc.

(20-30 min.)

(All amounts are in millions)

Req. 1

The main source of cash is operating activities ($2,294 million). This

indicates that YUM! Brands, Inc.’s basic operations are generating

Req. 2

The three most significant differences between net income and net cash

provided by operations are:

(continued) YUM! Brands

Req. 3

In 2012, YUM! Brands’ additions to property, plant, and equipment were

more than previous years’ additions. This is evident in the investing

Req. 4

The largest two items in YUM! Brands’ financing section of their

consolidated statement of cash flows are purchases of treasury stock

Req. 5

(continued) YUM! Brands

support the business and repayment of debt without borrowing any new

debt in 2012. However, we note a decrease in cash and cash equivalents

Group Projects

(2-3 hours)