(20-25 min.) P 6-61A

Req. 1

Cost of sales, budgeted ($721,000 × 1.05) ………….

$ 757,050

+ Ending inventory, budgeted ……………………………..

86,000

= Cost of goods available ……………………………………

843,050

− Beginning inventory ………………………………………..

(64,000)

= Purchases, budgeted ……………………………………….

$ 779,050

Req. 2

Shorty’s Convenience Stores

Budgeted Income Statement

Year Ended December 31, 2014

Sales ($986,000 × 1.05) ……………………………………….

$1,035,300

Cost of sales ($721,000 × 1.05) …………………………...

757,050

Gross profit ……………………………………………………….

278,250

Operating expenses ($109,000 − $8,750) ……………..

100,250

Net income ………………………………………………………..

$ 178,000

(15-20 min.) P 6-62A

Req. 1 (corrected income statements)

Downton Home Store

Income Statement (adapted; amounts in millions)

Years Ended December 31, 2014, 2013, and 2012

2014

2013

2012

Net sales revenue …………………….

$47

$44

$41

Cost of goods sold:

Beginning inventory …………….

$13

$14

$ 8

Net purchases ……………………..

31

29

27

Cost of goods available ……….

44

43

35

Ending inventory …………………

(11)

(13)

(14)

Cost of goods sold ………………

33

30

21

Gross profit ……………………………..

14

14

20

Operating expenses ………………….

8

8

8

Net income ………………………………

$ 6

$ 6

$12

(continued) P 6-62A

Req. 2

Req. 3

Inc.

(20-30 min.) P 6-63B

Req. 1

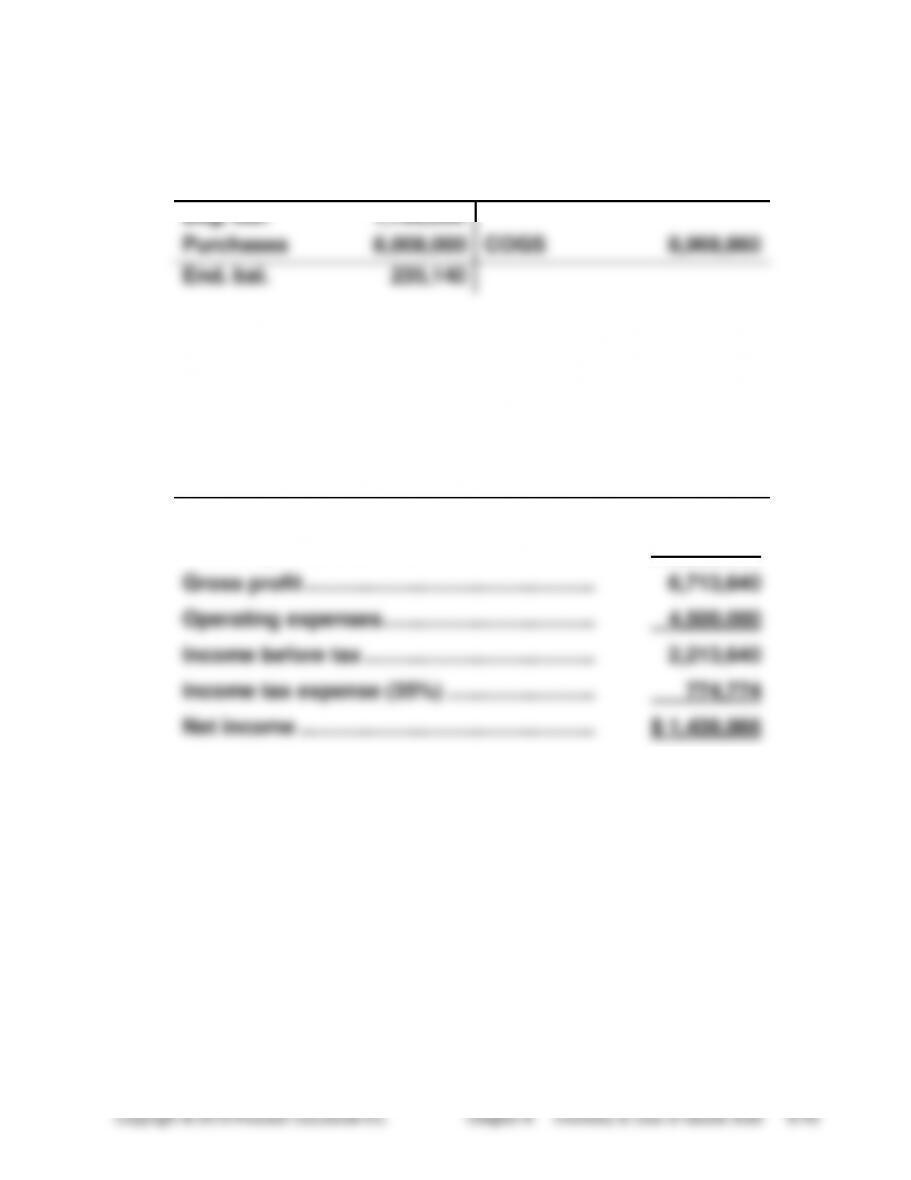

Inventory ………………………………………………….

8,008,000

Accounts Payable …………………………………

8,008,000

Accounts Payable ……………………………………..

7,860,000

Cash ……………………………………………………

7,860,000

Cash …………………………………………………………

5,400,000

Accounts Receivable …………………………………

10,282,500

Sales Revenue ……………………………………..

15,682,500

Cost of Goods Sold (153,000 × $58.62*) ………

8,968,860*

Inventory ……………………………………………..

8,968,860

Operating Expenses ………………………………….

4,500,000

Cash ($4,500,000 × 0.50) ……………………….

2,250,000

Accrued Liabilities ($4,500,000 × 0.50) ……

2,250,000

Income Tax Expense …………………………………

774,774

Income Tax Payable (see Req. 3) …………..

774,774

_____

*($1,196,000 + $8,008,000) ÷ (23,000 + 28,000 + 48,000 + 58,000) = $58.62

(continued) P 6-63B

Req. 2

Inventory

Beg. bal.

1,196,000

Purchases

8,008,000

COGS

8,968,860

End. bal.

235,140

Req. 3

Super Buy Store in San Diego

Income Statement

Year Ended June 30, 2014

Sales revenue ……………………………………….

$15,682,500

Cost of goods sold ……………………………….

8,968,860

Gross profit ………………………………………….

6,713,640

Operating expenses ………………………………

4,500,000

Income before tax …………………………………

2,213,640

Income tax expense (35%) …………………….

774,774

Net income …………………………………………..

$ 1,438,866

Inc.

(20-30 min.) P 6-64B

Req. 1

The store uses FIFO.

This is apparent from the flow of costs out of inventory. For example, the

Req. 2

Cost of goods sold:

15

×

$36

=

$ 540

27

×

36

=

972

6

×

38

=

228

29

×

38

=

1,102

$2,842

Sales [(42 units × $68) + (35 x $70)]…………………………….

$5,306

Cost of goods sold ……………………………………………………

(2,842)

Gross profit ………………………………………………………………

$2,464

Req. 3

Cost of January 31 inventory (47 x $38) + (25 × $40) =

$ 2,786

(20-30 min.) P 6-65B

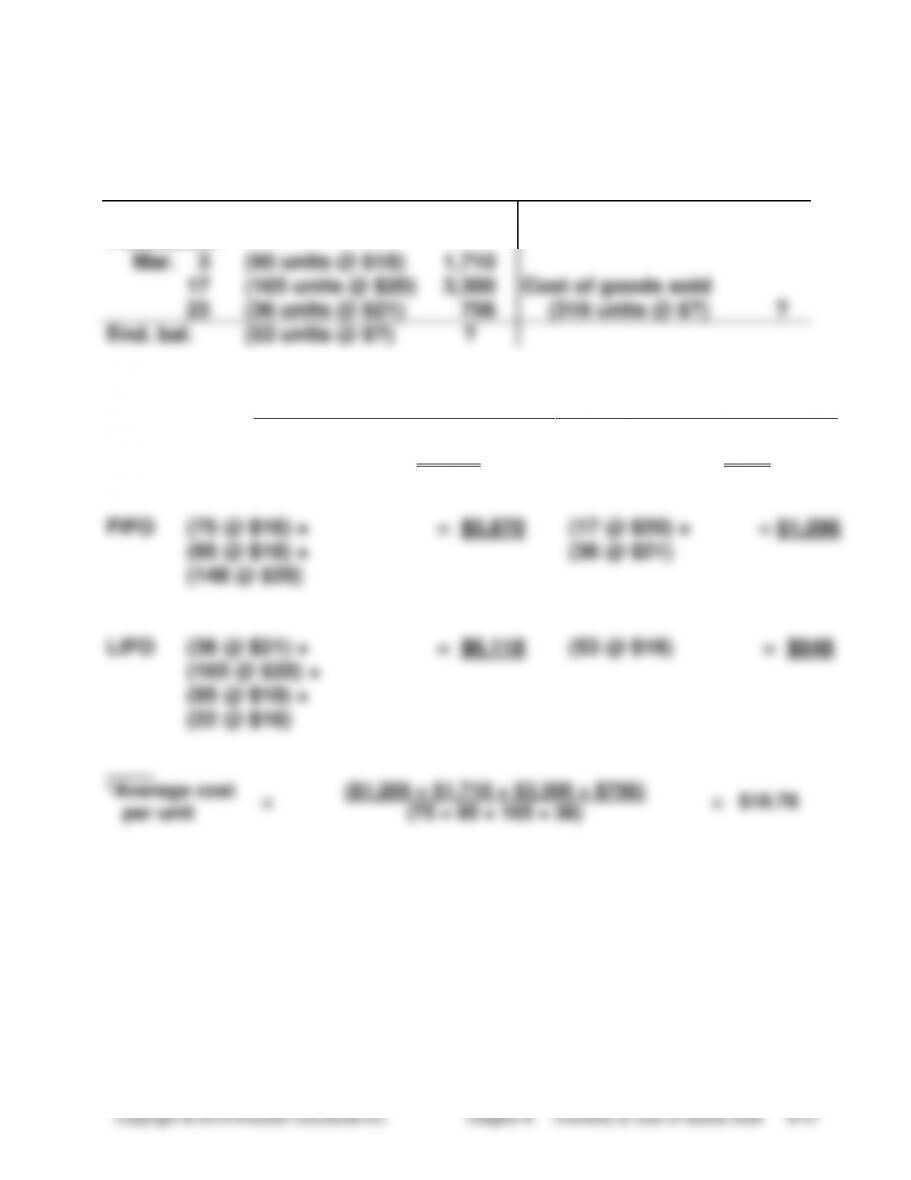

Req. 1

Inventory

Beg. bal.

(75 units @ $16) 1,200

Purchases:

Mar. 3

(95 units @ $18) 1,710

17

(165 units @ $20) 3,300

Cost of goods sold

23

(36 units @ $21) 756

(318 units @ $?)

?

End. bal.

(53 units @ $?) ?

Cost of Goods Sold

Ending Inventory

Average cost

318 × $18.78* = $5,972

53 × $18.78* = $995

Inc.

(continued) P 6-65B

Req. 2

LIFO results in the highest cost of goods sold because (a) the

company’s prices are rising and (b) LIFO assigns the cost of the latest

Req. 3

Army-Navy Surplus

Income Statement

Month Ended March 31, 2014

Sales revenue (318 × $47) ………………………………

$14,946

Cost of goods sold ………………………………………..

5,972

Gross profit ………………………………………………….

8,974

Operating expenses ………………………………………

2,755

Income before income taxes ………………………….

6,219

Income tax expense (30%) ……………………………..

1,866

Net income ……………………………………………………

$ 4,353

(30-40 min.) P 6-66B

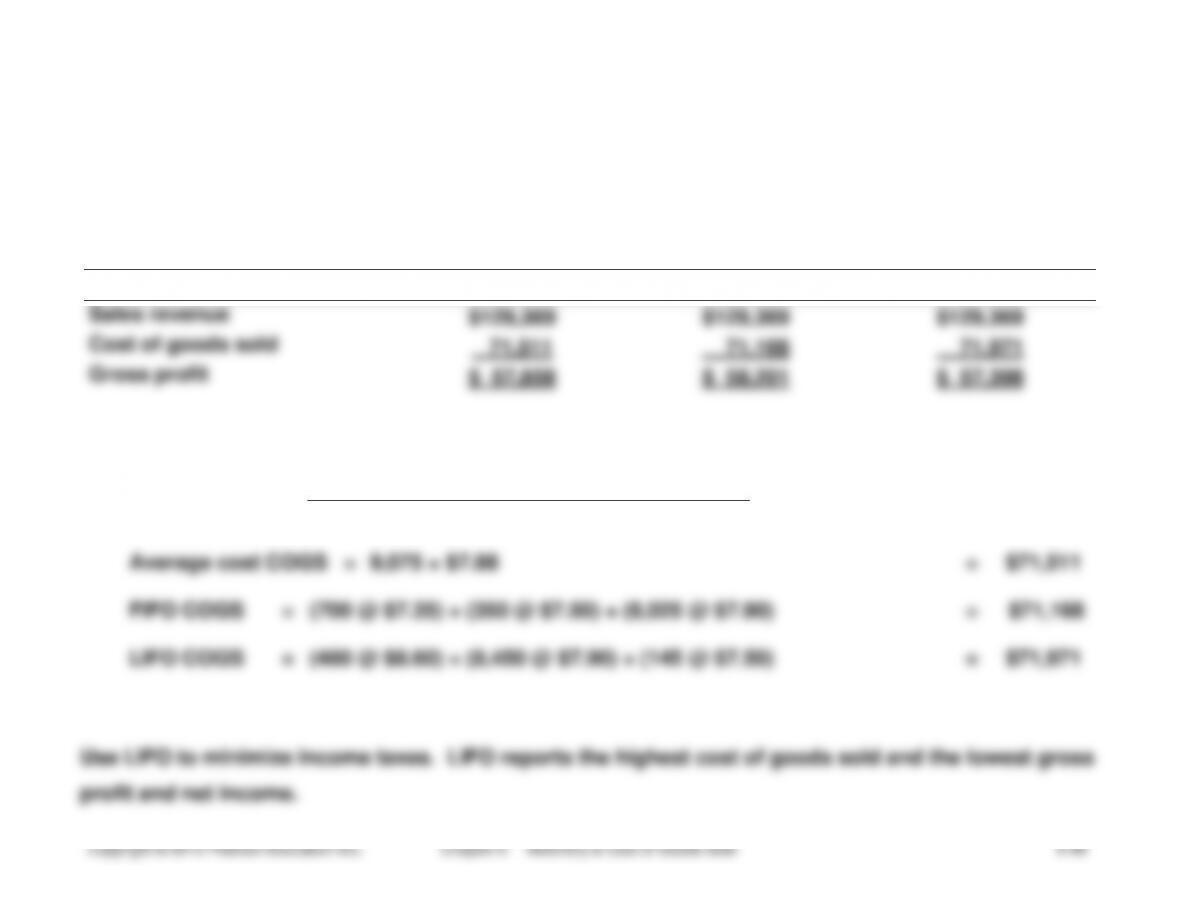

Req. 1 (partial income statements)

Parker Aviation

Income Statement

Year Ended October 31, 2014

AVERAGE

FIFO

LIFO

Sales revenue

$129,369

$129,369

$129,369

Cost of goods sold

71,511

71,168

71,971

Gross profit

$ 57,858

$ 58,201

$ 57,398

Computations of cost of goods sold:

Average cost

=

($5,145 + $2,625 + $66,755 + $4,128)

=

$7.88

per case

(700 + 350 + 8,450 + 480)

Average cost COGS = 9,075 × $7.88

=

$71,511

FIFO COGS

=

(700 @ $7.35) + (350 @ $7.50) + (8,025 @ $7.90)

=

$71,168

LIFO COGS

=

(480 @ $8.60) + (8,450 @ $7.90) + (145 @ $7.50)

=

$71,971

Req. 2

(15-20 min.) P 6-67B

a. Stillwater Trade Mart should apply the lower-of-cost-or-market rule to

b.

Cost of Goods Sold ……………..

8,000

Inventory ………………………..

8,000

To write inventory down to market value.

Stillwater Trade Mart should report the following in its financial

statements:

c.

BALANCE SHEET

Inventory, at market (which is lower than cost

of $101,000) ………………………………………………………

$93,000*

d.

INCOME STATEMENT

Cost of goods sold ($490,000 + $8,000) ………………….

$498,000

*$101,000 − $8,000 = $93,000

e. Relevance and representational faithfulness are the reasons to

account for inventory at the lower of cost or market value.

Student responses may vary.

(20-30 min.) P 6-68B

Req. 1

Magic Muffins, Inc.

Top Roast Coffee

Corp.

Millions

Millions

Gross profit percentage:

Sales…………………….

$540

$7,710

Cost of sales……………

470

3,170

Gross profit…………….

$ 70

$4,540

Gross profit

$70

= 13.0%

$4,540

= 58.9%

percentage:

$540

$7,710

Inventory turnover:

Cost of goods sold

=

$470

$3,170

Average inventory

($30 + $18) / 2

($540+ $630) / 2

= 19.6 times

= 5.4 times

Req. 2

From these statistics, it’s hard to tell whether Magic Muffins or Top

(25-30 min.) P 6-69B

Req. 1 (estimate of ending inventory by the gross profit method)

Beginning inventory …………………………………

$ 67,300

Purchases ……………………………………………….

$410,700

Less: Purchase discounts …………………..

(17,000)

Purchase returns ……………………….

(10,500)

Net purchases ………………………………………

383,200

Cost of goods available …………………………….

450,500

Cost of goods sold:

Sales revenue ………………………………………

$690,000

Less: Sales returns …………………………..

(13,000)

Net sales ………………………………………………

677,000

Less: Estimated gross profit of 44% ………

(297,880)

Estimated cost of goods sold ………………..

379,120

Estimated cost of ending inventory …………..

$ 71,380

(continued) P 6-69B

Req. 2 (income statement through gross profit)

Sternberg Company

Income Statement (partial)

Two Week Period ending March 15 (date of the fire)

Sales revenue …………………………..………….

$690,000

Less: Sales returns ………………………….

(13,000)

Net sales revenue …………………………...

677,000

Cost of goods sold ……………………………….

379,120*

Gross profit …………………………………………

$297,880

_____

*Cost of goods sold:

Beginning inventory …………………………..……….

$67,300

Purchases ……………………………………..

$410,700

Less: Purchases discounts ……………

(17,000)

Purchase returns …………………

(10,500)

Net purchases …………………………………………….

383,200

Cost of goods available ……………………………….

450,500

Less: Ending inventory …………………………..……

(71,380)

Cost of goods sold ………………………………………

$379,120

(20-25 min.) P 6-70B

Req. 1

Cost of sales, budgeted ($724,000 × 1.10) ……….

$ 796,400

+ Ending inventory, budgeted …………………………..

84,000

= Cost of goods available …………………………………

880,400

− Beginning inventory ……………………………………..

(69,000)

= Purchases, budgeted …………………………………….

$ 811,400

Req. 2

Chuck’s Convenience Stores

Budgeted Income Statement

Year Ended December 31, 2014

Sales ($975,000 × 1.10) ………………………………….

$1,072,500

Cost of sales ($724,000 × 1.10) ………………………

796,400

Gross profit ………………………………………………….

276,100

Operating expenses ($113,000 − $2,900)…………

110,100

Net income …………………………………………………..

$ 166,000

(15-20 min.) P 6-71B

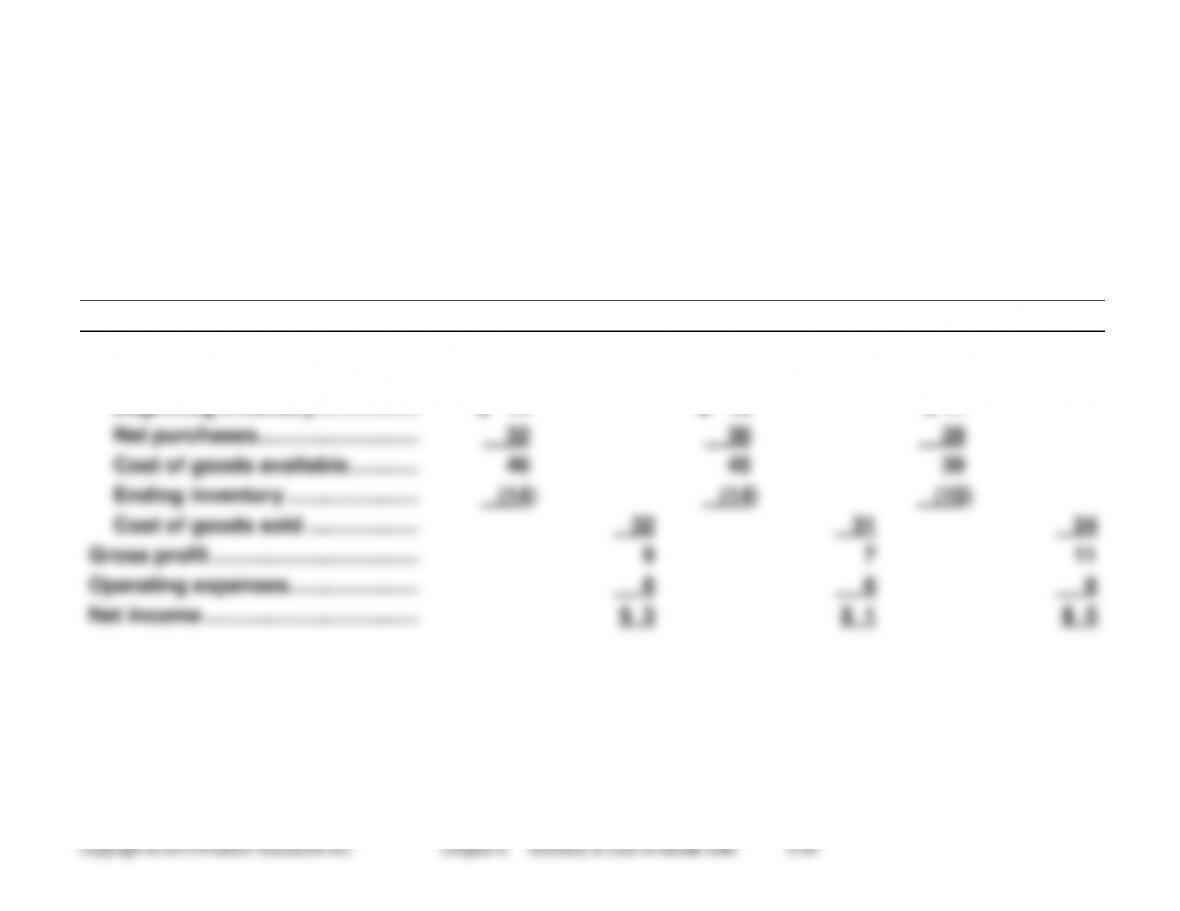

Req. 1 (corrected income statements)

Durango Furniture

Income Statement (adapted; amounts in millions)

Years Ended December 31, 2014, 2013, and 2012

2014

2013

2012

Net sales revenue …………………….

$41

$38

$35

Cost of goods sold:

Beginning inventory ……………..

$ 14

$ 15

$ 11

Net purchases ………………………

32

30

28

Cost of goods available…………

46

45

39

Ending inventory ………………….

(14)

(14)

(15)

Cost of goods sold ……………….

32

31

24

Gross profit ……………………………..

9

7

11

Operating expenses ………………….

6

6

6

Net income ………………………………

$ 3

$ 1

$ 5

(continued) P 6-71B

Req. 2

Req. 3

Challenge Exercises and Problem

(5–10 min.) E 6-72

a. Buy inventory late in the year.

b. Company is using LIFO.

(20-30 min.) E 6-73

Req. 1

LIFO cost of goods sold =

1.

From purchase in December (31 @ $1,200) ………………..

$ 37,200

2.

From purchase in June (55 @ $1,100) ……………………….

60,500

3.

From purchase in February (19 @ $1,050) ………………….

19,950

4.

From beginning inventory (12 @ $975) ………………………

11,700

LIFO cost of goods sold …………………………..………….

$129,350

Req. 2

Cost of goods sold with the additional year-end purchase

(this would have avoided a LIFO liquidation—that is,

kept year-end inventory at the same level it was at the

beginning of the year)

1.

From purchase in December (43* @ $1,200) ………………

$ 51,600

2.

From purchase in June (55 @ $1,100) ……………………….

60,500

3.

From purchase in February (19 @ $1,050) ………………….

19,950

Cost of goods sold (with no LIFO liquidation) ………..

$132,050

_____

*Must purchase a total of 43 units in December to keep ending inventory

at 44 units, which was the level of beginning inventory.

(20-30 min.) E 6-74

Sales increased, the gross profit increased then dropped, and net

income slid into a net loss, as shown here:

Dollars in millions

2014

2013

2012

Sales

$36.6

$35.3

$34.3

Cost of sales

29.4

27.6

26.8

Gross profit

7.2

7.7

7.5

Net income (net loss)

(0.4)

0.5

0.8

Gross

profit

=

$7.2 =

19.7%

$7.7 =

21.8%

$7.5 =

21.9%

percentage

$36.6

$35.3

$34.3

Inventory

=

$29.4

=

3.7

$27.6

=

3.8

$26.8

=

3.9

turnover

($8.6 + $7.2)

/ 2

($7.2 + $7.2)

/ 2

($7.2 + $6.4)

/ 2

Both the gross profit percentage and the rate of inventory turnover

dropped during this period. The gross profit percentage dropped