(10-20 min.) E 3-25A

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Closing Entries

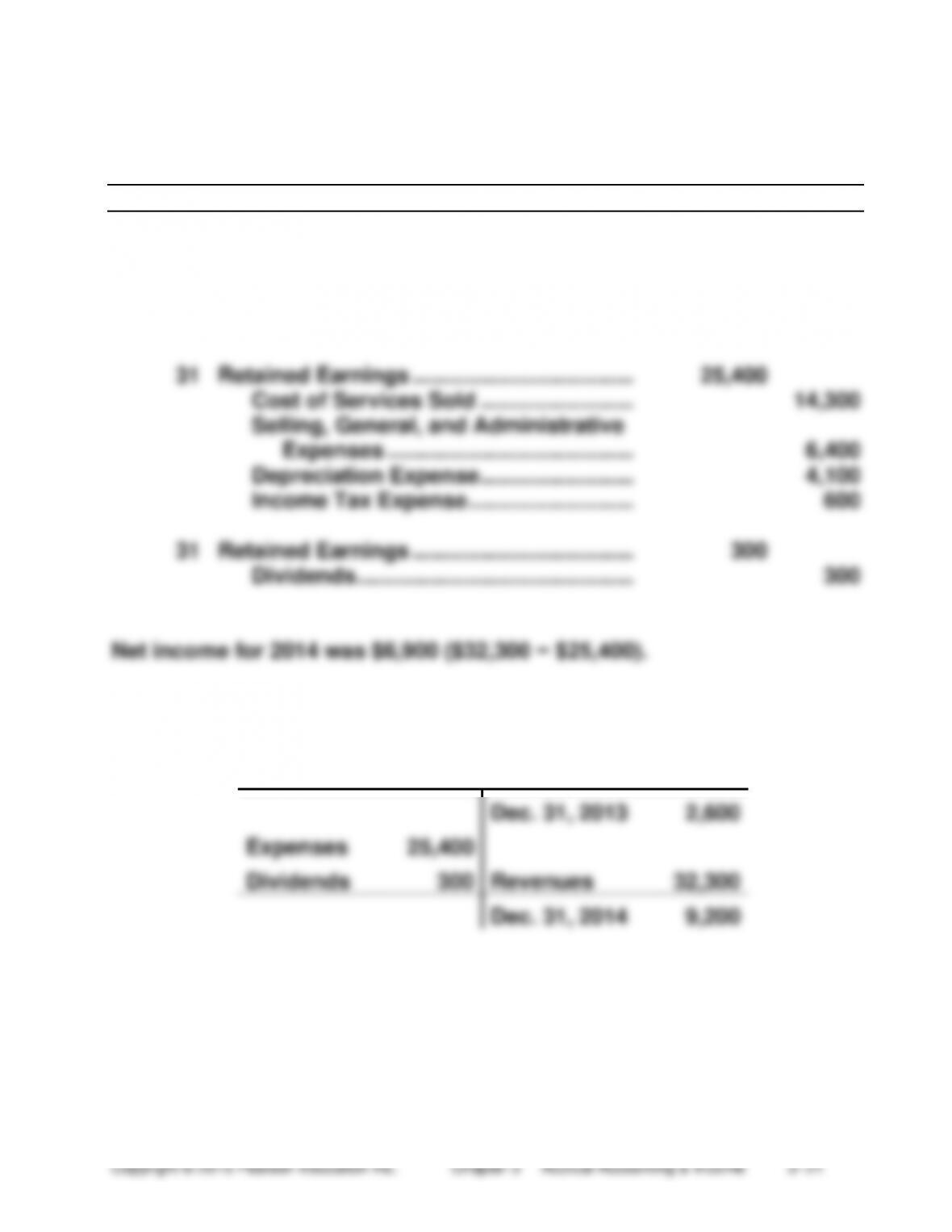

Dec.

31

Service Revenue …………………………………

31,900

Other Revenue ……………………………………

400

Retained Earnings ………………………….

32,300

31

Retained Earnings ………………………………

25,400

Cost of Services Sold …………………….

14,300

Selling, General, and Administrative

Expenses ………………………………….

6,400

Depreciation Expense …………………….

4,100

Income Tax Expense ………………………

600

31

Retained Earnings ………………………………

300

Dividends ………………………………………

300

Retained Earnings

Expenses

25,400

Dec. 31, 2013

2,600

Dividends

300

Revenues

32,300

Dec. 31, 2014

9,200

3-22 Financial Accounting 10/e Solutions Manual Copyright © 2015 Pearson Education Inc.

(15-25 min.) E 3-26A

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Adjusting Entries

Dec.

31

Unearned Service Revenue ……………………….

7,400

Service Revenue ($20,600 − $13,200) …….

7,400

31

Salary Expense ($4,600 − $4,200) ………………

400

Salary Payable …………………………………….

400

31

Rent Expense ($1,600 − $1,400) …………………

200

Prepaid Rent ……………………………………….

200

31

Depreciation Expense ($850 − $0) ……………..

850

Accumulated Depreciation …………………..

850

31

Income Tax Expense ($1,450 − $0) …………….

1,450

Income Tax Payable …………………………….

1,450

Closing Entries

31

Service Revenue ………………………………………

20,600

Retained Earnings ……………………………….

20,600

31

Retained Earnings ……………………………………

8,500

Salary Expense ……………………………………

4,600

Rent Expense ………………………………………

1,600

Depreciation Expense ………………………….

850

Income Tax Expense …………………………...

1,450

31

Retained Earnings ……………………………………

1,250

Dividends ……………………………………………

1,250

(20-30 min.) E 3-27A

Req. 1

Warfield Production Company

Balance Sheet

December 31, 2014

ASSETS

Current assets:

Cash ………………………………………………………………………….

$14,250

Prepaid rent ($1,800 − $200) ………………………………………..

1,600

Total current assets ……………………………………………….

15,850

Plant assets:

Equipment ……………………………………………….

$42,000

Less accumulated depreciation

($3,400 + $850) ……………………………………..

(4,250)

37,750

Total assets …………………………………………………………………….

$53,600

LIABILITIES

Current liabilities:

Accounts payable ………………………………………………………

$ 5,100

Salary payable ($4,600 − $4,200) ………………………………….

400

Unearned service revenue ($10,100 − $7,400) ……………….

2,700

Income tax payable …………………………………………………….

1,450

Total current liabilities ……………………………………………

9,650

Note payable, long-term …………………………………………………..

16,000

Total liabilities ………………………………………………………………..

25,650

STOCKHOLDERS’ EQUITY

Common stock… …………………………………………………………….

8,600

Retained earnings ($8,500 + $20,600 − $4,600 − $1,600 −

$850 − $1,450 − $1,250) …………………..

19,350

Total stockholders’ equity ……………………………………………….

27,950

Total liabilities and stockholders’ equity …………………………..

$53,600

3-24 Financial Accounting 10/e Solutions Manual Copyright © 2015 Pearson Education Inc.

(continued) E 3-27A

Req. 2

Current

Year

Prior

Year

Net working

capital

=

Total current assets −

current liabilities

=

$15,850 −

$9,650

=

$6,200

$6,400

Current ratio

=

Total current assets

=

$15,850

=

1.64

1.67

Total current liabilities

$9,650

Both net working capital and the current ratio have decreased slightly,

indicating that the ability to pay current liabilities with current assets has

deteriorated a little.

Debt ratio

=

Total liabilities

=

$25,650

=

0.48

0.40

Total assets

$53,600

An increase in the debt ratio indicates a deterioration in the ratio.

In summary, the overall ability to pay total liabilities deteriorated slightly.

(30 min.) E 3-28A

a.

Current ratio

=

$50

=

1.04

Debt ratio

=

$40 + $8

=

0.62

$40 + $8

$70 + $8

The purchase of equipment on account hurts both ratios.

Collecting cash in advance hurts both ratios.

(5-10 min.) E 3-29B

Millions

a.

Revenue …………………………..………………………………….

$860

The revenue principle says to record revenue when it has been

earned, regardless of when cash is collected. Therefore, report

the amount of revenue earned, regardless of when the company

collects cash.

b.

Total expense ……………………………………………………….

$610

The expense recognition principle governs accounting for

expenses.

c.

Revenue ($860 − $25) …………………………………………..

$835

Total expense ……………………………………………………….

$630

The accrual basis measures revenues as earned and expenses

as incurred, while the cash basis measures revenues collected in

cash and expenses paid in cash.

d.

The income statement reports revenues and expenses.

The statement of cash flows reports cash receipts and cash

payments.

(15-20 min.) E 3-30B

Req. 1

Adjusting Entries

DATE

ACCOUNT TITLES

DEBIT

CREDIT

a.

Insurance Expense …………………………………………..

1,550

Prepaid Insurance ($450 + $1,600 − $500) ………

1,550

b.

Interest Receivable …………………………………………..

2,700

Interest Revenue ………………………………………….

2,700

c.

Unearned Service Revenue ($1,400 − $300) ………..

1,100

Service Revenue ………………………………………….

1,100

d.

Depreciation Expense ………………………………………

5,400

Accumulated Depreciation …………………………...

5,400

e.

Salary Expense ($25,000 × 2/5) ………………………….

10,000

Salary Payable …………………………………………….

10,000

f.

Income Tax Expense ($26,000 × .35) ………………….

9,100

Income Tax Payable ……………………………………..

9,100

Req. 2

Net income understated by omission of:

Interest revenue ……………………………………………..

$ 2,700

Service revenue ……………………………………………..

1,100

Total understatement ……………………………………..

$ (3,800)

Net income overstated by omission of:

Insurance expense …………………………………………

$ 1,550

Depreciation expense …………………………………….

5,400

Salary expense ………………………………………………

10,000

Income tax expense ……………………………………….

9,100

Total overstatement ……………………………………….

26,050

Overall effect — net income overstated by ………….

$22,250

3-28 Financial Accounting 10/e Solutions Manual Copyright © 2015 Pearson Education Inc.

(10-15 min.) E 3-31B

Missing amounts in italics.

1

2

3

4

Beginning Supplies

$ 560

$ 1,400

$1,100

$ 900

Add: Purchases of supplies

during the year

1,480

1,100

1,500

600

Total amount to account for

2,040

2,500

2,600

1,500

Less: Ending Supplies

(200)

(400)

(1,000)

(300)

Supplies Expense

$1,840

$2,100

$1,600

$1,200

Journal entries:

Situation 1:

Supplies ……………………………………..

1,480

Cash or Accounts Payable ………

1,480

Situation 2:

Supplies Expense………………………..

2,100

Supplies …………………………..…….

2,100

(10-20 min.) E 3-32B

Adjusting Entries

DATE

ACCOUNT TITLES

DEBIT

CREDIT

a.

Interest Expense ………………………………………………

2,100

Interest Payable …………………………………………..

2,100

b.

Interest Receivable …………………………………………..

3,900

Interest Revenue ………………………………………….

3,900

c.

Unearned Rent Revenue ($14,000 / 2 × 6/12) ……….

3,500

Rent Revenue ………………………………………………

3,500

d.

Salary Expense ($2,300 × 3) ………………………………

6,900

Salary Payable …………………………………………….

6,900

e.

Supplies Expense …………………………………………….

1,510

Supplies ($3,110 − $1,600) …………………………….

1,510

f.

Depreciation Expense ($120,000 / 5) ………………….

24,000

Accumulated Depreciation …………………………...

24,000

3-30 Financial Accounting 10/e Solutions Manual Copyright © 2015 Pearson Education Inc.

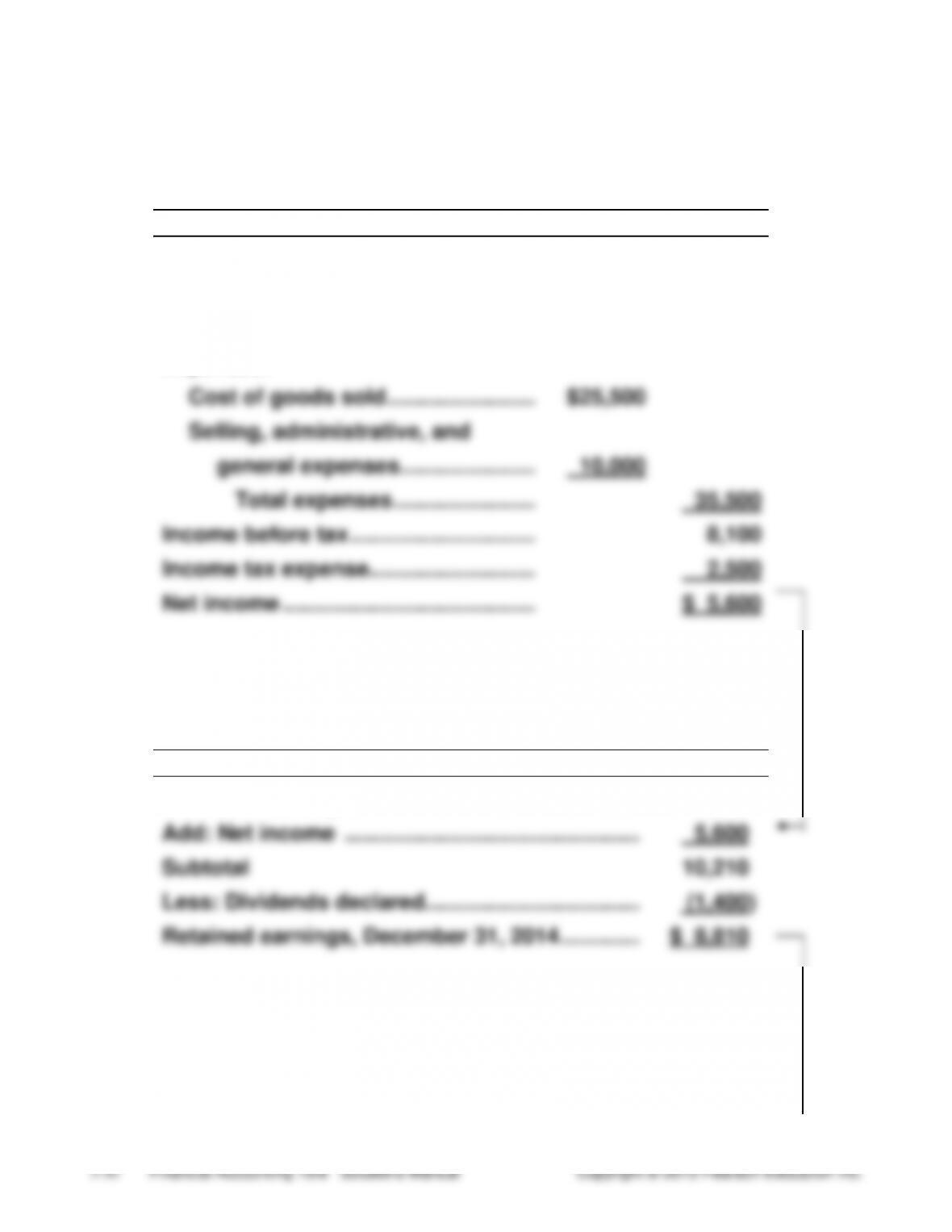

(20-30 min.) E 3-33B

Oregon Flowers, Inc.

Income Statement

Year Ended December 31, 2014

Thousands

Revenues:

Sales revenue …………………………..

$43,600

Expenses:

Cost of goods sold ……………………

$25,500

Selling, administrative, and

general expenses ………………….

10,000

Total expenses …………………..

35,500

Income before tax …………………………

8,100

Income tax expense ………………………

2,500

Net income …………………………………..

$ 5,600

Oregon Flowers, Inc.

Statement of Retained Earnings

Year Ended December 31, 2014

Thousands

Retained earnings, December 31, 2013 ………….

$ 4,610

Add: Net income …………………………………………

5,600

Subtotal

10,210

Less: Dividends declared……………………………..

(1,400)

Retained earnings, December 31, 2014 ………….

$ 8,810

(continued) E 3-33B

Oregon Flowers, Inc.

Balance Sheet

December 31, 2014

Thousands

ASSETS

LIABILITIES

Cash ………………………………..

$ 2,510

Accounts payable …………

$ 7,500

Accounts receivable …………

1,900

Income tax payable ……….

600

Inventories ………………………

3,800

Other liabilities ……………..

2,400

Prepaid expenses …………….

1,700

Total liabilities ………………

10,500

Prop., plant, equip.

$16,700

STOCKHOLDERS’

Less: Accum.

EQUITY

deprec ……

(2,500)

14,200

Common stock ……………..

14,500

Other assets …………………….

9,700

Retained earnings …………

8,810

Total stockholders’ equity

23,310

Total liabilities and

Total assets ……………………..

$33,810

stockholders’ equity …..

$33,810

3-32 Financial Accounting 10/e Solutions Manual Copyright © 2015 Pearson Education Inc.

(10-20 min.) E 3-34B

Amounts in millions

Receivables

Beg. bal.

210

Sales revenue

21,040

Collections

20,900

End. bal.

350

Prepaid Insurance

Beg. bal.

140

Payment

470

Insurance expense

410

End. bal.

200

Accrued Liabilities Payable

Beg. bal.

640

Payments

4,200

Other operating

expenses

4,280

End. bal.

720

(10-20 min.) E 3-35B

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Closing Entries

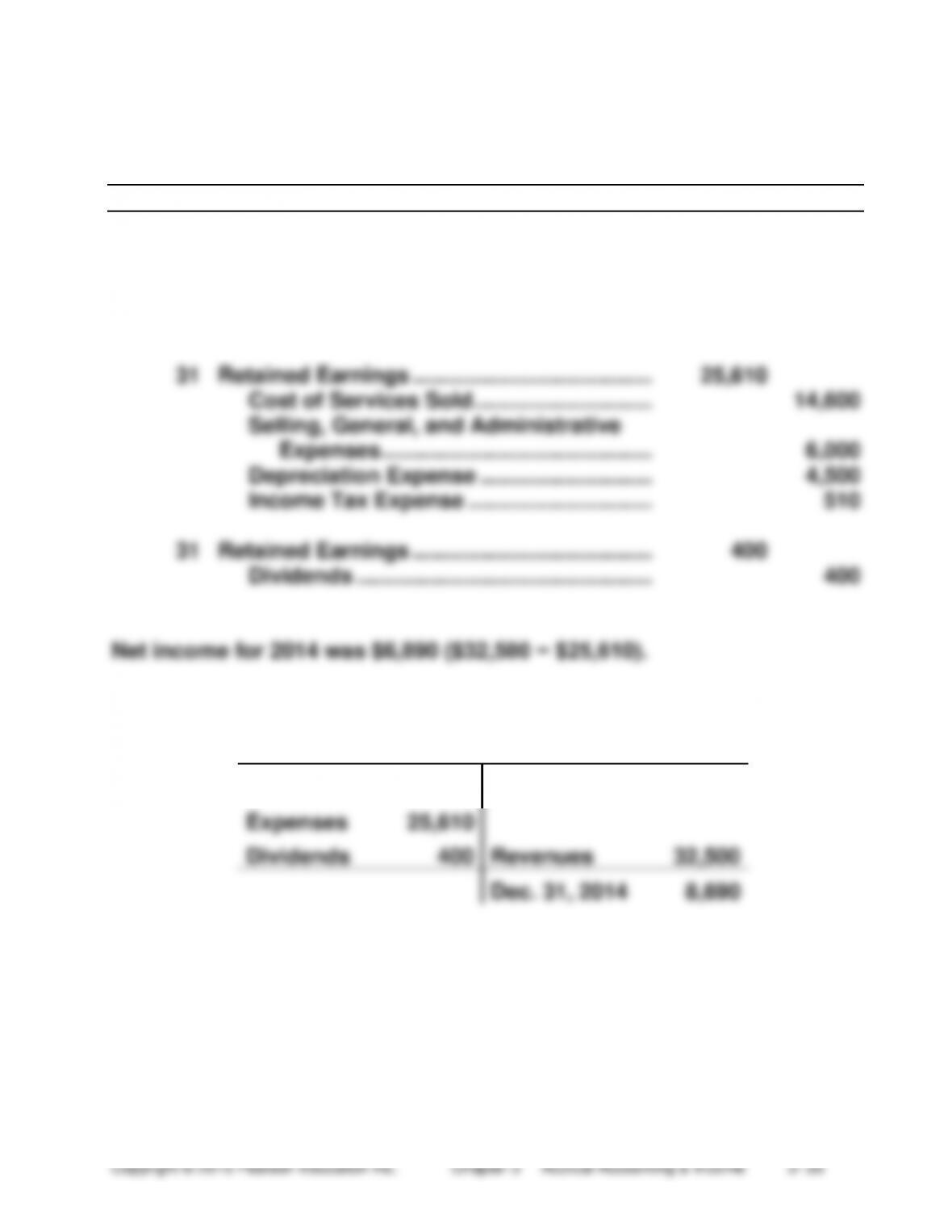

Dec.

31

Service Revenue ……………………………………

32,300

Other Revenue ………………………………………

200

Retained Earnings …………………………....

32,500

31

Retained Earnings …………………………………

25,610

Cost of Services Sold ………………………..

14,600

Selling, General, and Administrative

Expenses ……………………………………..

6,000

Depreciation Expense ……………………….

4,500

Income Tax Expense …………………………

510

31

Retained Earnings …………………………………

400

Dividends …………………………………………

400

Retained Earnings

Expenses

25,610

Dec. 31, 2013

2,200

Dividends

400

Revenues

32,500

Dec. 31, 2014

8,690

3-34 Financial Accounting 10/e Solutions Manual Copyright © 2015 Pearson Education Inc.

(15-25 min.) E 3-36B

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Adjusting Entries

Dec.

31

Unearned Service Revenue ………………………….

6,500

Service Revenue ($20,600 − $14,100) ……….

6,500

31

Salary Expense ($5,600 − $4,600) …………………

1,000

Salary Payable ………………………………………..

1,000

31

Rent Expense ($2,300 − $1,600) ……………………

700

Prepaid Rent …………………………………………..

700

31

Depreciation Expense ($750 − $0) ………………..

750

Accumulated Depreciation ………………………

750

31

Income Tax Expense ($1,360 − $0) ……………….

1,360

Income Tax Payable ………………………………..

1,360

Closing Entries

31

Service Revenue …………………………………………

20,600

Retained Earnings…………………………………..

20,600

31

Retained Earnings ………………………………………

10,010

Salary Expense ………………………………………

5,600

Rent Expense …………………………………………

2,300

Depreciation Expense ……………………………..

750

Income Tax Expense ……………………………….

1,360

31

Retained Earnings ………………………………………

1,110

Dividends ……………………………………………….

1,110

(20-30 min.) E 3-37B

Req. 1

Terrell Production Company

Balance Sheet

December 31, 2014

ASSETS

Current assets:

Cash ………………………………………………………………………….

$14,450

Prepaid rent ($2,500 − $700) ………………………………………..

1,800

Total current assets ……………………………………………….

16,250

Plant assets:

Equipment ………………………………………………….

$44,000

Less accumulated depreciation

($3,500 + $750) ………………………………………..

(4,250)

39,750

Total assets ……………………………………………………………………

$56,000

LIABILITIES

Current liabilities:

Accounts payable ……………………………………………………..

$ 4,700

Salary payable ($5,600 − $4,600) …………………………………

1,000

Unearned service revenue ($9,100 − $6,500) ……………….

2,600

Income tax payable ……………………………………………………

1,360

Total current liabilities ………………………………………….

9,660

Note payable, long-term ………………………………………………….

17,000

Total liabilities ……………………………………………………………….

26,660

STOCKHOLDERS’ EQUITY

Common stock ………………………………………………………………

8,700

Retained earnings ($11,160 + $10,590* − $1,110) ………………

20,640

Total stockholders’ equity ………………………………………………

29,340

Total liabilities and stockholders’ equity ………………………….

$56,000

(continued) E 3-37B

Req. 2

Current

Year

Prior

Year

Net working

capital

=

Total current assets −

current liabilities

=

$16,250 −

$9,660

=

$6,590

$7,000

Current

ratio

=

Total current assets

=

$16,250

=

1.68

1.72

Total current liabilities

$9,660

Both net working capital and the current ratio have decreased, indicating

that the ability to pay current liabilities with current assets has

deteriorated.

(30 min.) E 3-38B

a.

Current ratio

=

$60

=

1.00

Debt ratio

=

$70 + $10

=

0.80

$50 + $10

$90 + $10

The purchase of equipment on account hurts both ratios.

$50

Collecting cash in advance hurts both ratios.

$60

Accruing an expense hurts both ratios.

e.

Current ratio

=

=

1.36

Debt ratio

=

$70

=

0.71

$50

A cash sale improves both ratios.

3-38 Financial Accounting 10/e Solutions Manual Copyright © 2015 Pearson Education Inc.

Serial Exercise

(3 hours) E 3-39

Reqs. 1, 2, 5, and 7

Cash

Accounts Receivable

Jan. 2

11,000

Jan. 2

700

Jan. 18

1,500

Jan. 28

1,500

9

1,000

3

3,900

Bal.

0

21

2,400

12

200

Adj.

2,000

28

1,500

26

400

Bal.

2,000

31

1,200

Bal.

9,500

Supplies

Equipment

Jan. 5

400

Adj.

200

Jan. 3

3,900

Bal.

200

Bal.

3,900

Accumulated Depreciation –

Equipment

Furniture

Adj.

65

Jan. 4

4,700

Bal.

65

Bal.

4,700

Accumulated Depreciation –

Furniture

Accounts Payable

Adj.

78

Jan. 26

400

Jan. 4

4,700

Bal.

78

5

400

Bal.

4,700

(continued) E 3-39

Reqs. 1, 2, 5, and 7

Salary Payable

Unearned Service Revenue

Adj.

500

Adj.

800

Jan. 21

2,400

Bal.

500

Bal.

1,600

Common Stock

Retained Earnings

Jan. 2

11,000

Clo.

1,743

Clo.

5,300

Bal.

11,000

Clo.

1,200

Bal.

2,357

Jan. 31

Clo.

Jan. 9

1,000

18

1,500

Bal.

2,500

Adj.

2,000

Adj.

Jan. 2

700

Clo.

700

Jan. 12

Clo.

Salary Expense

Adj.

Clo.

Adj.

Clo.

3-40 Financial Accounting 10/e Solutions Manual Copyright © 2015 Pearson Education Inc.

(continued) E 3-39

Req. 1

January 2 through 18 entries are repeated from Solution to E 2-34.

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Jan.

2

Cash ………………………………………………….

11,000

Common Stock ……………………………….

11,000

2

Rent Expense ……………………………………..

700

Cash ……………………………………………….

700

3

Equipment ………………………………………….

3,900

Cash ……………………………………………….

3,900

4

Furniture …………………………………………….

4,700

Accounts Payable …………………………...

4,700

5

Supplies …………………………………………….

400

Accounts Payable …………………………...

400

9

Cash ………………………………………………….

1,000

Service Revenue ……………………………..

1,000

12

Utilities Expense …………………………………

200

Cash ……………………………………………….

200

18

Accounts Receivable ………………………….

1,500

Service Revenue ……………………………..

1,500

21

Cash ………………………………………………….

2,400

Unearned Service Revenue ………………

2,400

21

No entry; no transaction yet

26

Accounts Payable ……………………………….

400

Cash ……………………………………………….

400

28

Cash ………………………………………………….

1,500

Accounts Receivable ……………………….

1,500

31

Dividends …………………………………………..

1,200

Cash ……………………………………………….

1,200