(10-15 min.) E 6-26B

Req. 1

Inventory

Beg. bal.

(6 units @ $170) 1,020

Purchases

Aug. 15

(8 units @ $172) 1,376

Cost of goods sold

26

(14 units @ $180) 2,520

(17 units @ $?)

?

Ending bal.

(11 units @ $?) ?

Cost of Goods Sold

Ending Inventory

(a) Specific

unit cost

(1 @ $170) +

(8 @ $172) +

(8 @ $180)

=

$2,986

(5 @ $170) +

(6 @ $180)

=

$1,930

(b)Average

cost

(17 × $175.57*)

=

$2,985

(11 × $175.57*)

=

$1,931

(c) FIFO

(6 @ $170) +

(8 @ $172) +

(3 @ $180)

=

$2,936

(11 @ $180)

=

$1,980

(d) LIFO

(14 @ $180) +

(3 @ $172)

=

$3,036

(6 @ $170) +

(5 @ $172)

=

$1,880

_____

*Average cost per

unit

=

($1,020 + $1,376 + $2,520)

=

$175.57

(6 + 8 + 14)

Req. 2

LIFO produces the highest cost of goods sold, $3,036.

Inc.

(10 min.) E 6-27B

Cost of goods sold:

LIFO ($3,036) − FIFO ($2,936) ……………………….

$ 100

× Income tax rate …………………………………………

× .40

Tax savings advantage of LIFO ………………………..

$ 40

(15 min.) E 6-28B

Req. 1

a.

FIFO

Cost of goods sold:

(12 @ $62) ……………………………………..

$744

Ending inventory:

(5 @ $62) + (3 @ $71) ……………………..

$523

b.

LIFO

Cost of goods sold:

(3 @ $71) + (9 @ $62) ……………………..

$771

Ending inventory:

(8 @ $62) ……………………………………….

$496

Req. 2

MusicMagic.net

Income Statement

Month Ended September 30, 2014

Sales revenue (12 @ $114) …………………………..………..

$1,368

Cost of goods sold ………………………………………………..

744

Gross profit… ……………………………………………………….

624

Operating expenses ………………………………………………

320

Income before income tax ……………………………………..

304

Income tax expense (35%) ……………………………………..

106

Net income……………………………………………………………

$ 198

Inc.

(15 min.) E 6-29B

Req. 1

Gross profit:

FIFO

LIFO

Sales revenue ……………………………………………

$1,235,000

$1,235,000

Cost of goods sold

FIFO: 95,000 × $7.20 ………………………………

684,000

LIFO: (60,000 × $5.20) + (20,000 × $6.10)

+ (15,000 × $7.20) …………………………

542,000

Gross profit ……………………………………………….

$551,000

$693,000

Req. 2

Gross profit under FIFO and LIFO differ because inventory costs

decreased during the period.

(5-10 min.) E 6-30B

Rose Tree Garden Supplies

Income Statement (partial)

Year Ended August 31, 2014

Sales revenue ……………………………………………………………….

$251,000

Cost of goods sold [$118,000 + ($34,000 − $32,000)] ……….

120,000

Gross profit ………………………………………………………………….

$131,000

Note: Cost is used for beginning inventory because cost is lower than

(15-20 min.) E 6-31B

a.

$ 122,000

$41,000 + $120,000 − $39,000 = $122,000

b.

$ 118,000

$240,000 − $122,000 = $118,000

c.

Must first solve for d

d.

$ 96,000

$137,000 − $41,000= $96,000

c.

$ 88,000

$28,000 + c − $96,000 = $20,000;

c = $88,000

e.

$ 97,000

$60,000 + $37,000 = $97,000

f.

$ 26,000

f + $55,000 − $21,000 = $60,000; f = $26,000

g.

$ 8,000

$10,000 + $33,000 − g = $35,000; g = $8,000

h.

$ 45,000

$80,000 − $35,000 = $45,000

Req. 1

Epperson Company

Income Statement

Year Ended December 31, 2014

Net sales ………………………………………..

$240,000

Cost of goods sold …………………………

Beginning inventory …………………..

$ 41,000

Net purchases …………………………...

120,000

Cost of goods available ……………..

161,000

Ending inventory ……………………….

(39,000)

Cost of goods sold …………………….

122,000

Gross profit ……………………………………

118,000

Operating and other expenses ………..

72,000

Net income …………………………………….

$46,000

(20-30 min.) E 6-32B

Req. 1

Company

Gross Profit

Percentage

Inventory Turnover

Epperson

$118

=

49.2%

$122

=

3.1 times

$240

($41 + $39) / 2

Griffith

$41

=

29.9%

$96

=

4 times

$137

($28 + $20) / 2

Norse

$37

=

38.1%

$60

=

2.6 times

$97

($26 + $21) / 2

Victory

$45

=

56.3%

$35

=

3.9 times

$80

($10 + $8) / 2

Req. 2

Victory has the highest gross profit percentage, 56.3%. Griffith has the

lowest gross profit percentage, 29.9%.

Griffith has the highest rate of inventory turnover, 4 times. Norse has

(15 min.) E 6-33B

Req. 1 and 2

1

2

FIFO

LIFO

Gross profit percentage

=

$158,000 − $80,800

$158,000 − $90,800

$158,000

$158,000

= 48.9%

= 42.5%

Inventory turnover

=

$80,800

$90,800

($12,000 + $24,000) / 2

($7,000 + $14,000) / 2

= 4.5 times

= 8.6 times

Req. 3

FIFO produces a higher gross profit percentage.

Req. 4

LIFO produces a higher rate of inventory turnover.

(10-15 min.) E 6-34B

Year ended January 31, 2014:

Millions

Budgeted cost of goods sold ($6,600 × 1.12) …………….

$7,392

Budgeted ending inventory ……………………………………..

1,900

Budgeted cost of goods available…………………………….

9,292

Actual beginning inventory ……………………………………..

(1,600)

Budgeted purchases ……………………………………………….

$7,692

(10-15 min.) E 6-36B

Lake Travis Marine Supply

Income Statement (Corrected)

Years Ended June 30, 2014 and 2013

2014

2013

Sales revenue

$146,000

$124,600

Cost of goods sold:

Beginning inventory

$19,000

$ 9,500

Net purchases

82,000

79,000

Cost of goods avail.

101,000

88,500

Ending inventory

(16,500)

(19,000)*

Cost of goods sold

84,500

69,500

Gross profit

61,500

55,100

Operating expenses

29,000

21,000

Net income

$ 32,500

$ 34,100

_____

*$12,000 + $7,000 = $19,000

Lake Travis Marine Supply actually performed poorly in 2014, compared

to 2013, with net income down from $34,100 to $32,500.

Quiz

Q6–37

a

($3,400 + $6,700 − $5,500 = $4,600)

Q6–38

c

($7,700 − $5,500 = $2,200)

Q6–39

d

Q6–40

a

[(700 @ $11.00) + (1,200 @ $11.50) = $21,500]

Q6-41

b

[(1,200 @ $11.50) + (200 @ $11) = $16,000]

Q6-42

d

Q6-43

c

($153,000 + $213,000 = $366,000)

Q6-44

a

Q6–45

b

Q6–46

c

[$627,000 − ($61,000 + $430,000 − $40,000) =

$176,000]

Q6–47

d

($25,000 + X − $17,000 = $92,000; X = $84,000)

Q6–48

b

Q6–49

a

[$310,000 ÷ {($23,000 + $38,000) ÷ 2}] = 10.2 times

Q6-50

b

Net sales = $486,000 ($490,000 − $4,000)

COGS = $55,000 + ($202,000 + $21,000 −

$4,600 − $6,000) − $44,000

= $223,400

GP% = ($486,000 − $223,400) / $486,000

= 54%

Q6-51

c

$56,000 + $79,000 − $95,000 (1 − .40) = $78,000

Q6-52

a

Q6-53

b

Problems

(20-30 min.) P 6-54A

Req. 1

Inventory ………………………………………………..

9,296,000

Accounts Payable ………………………………

9,296,000

Accounts Payable …………………………………..

8,968,000

Cash ………………………………………………….

8,968,000

Cash ………………………………………………………

5,500,000

Accounts Receivable ………………………………

10,285,000

Sales Revenue ……………………………………

15,785,000

Cost of Goods Sold (154,000 × $62.39*) ……

9,608,060

Inventory ……………………………………………

9,608,060

Operating Expenses ………………………………..

3,750,000

Cash ($3,750,000 × .70) ……………………….

2,625,000

Accrued Liabilities ($3,750,000 × .30) …..

1,125,000

Income Tax Expense ……………………………….

970,776

Income Tax Payable (see Req. 3) …………

970,776

_____

*($1,060,000 + $9,296,000) ÷ (20,000 + 32,000 + 52,000 + 62,000) = $62.39

Inc.

(continued) P 6-54A

Req. 2

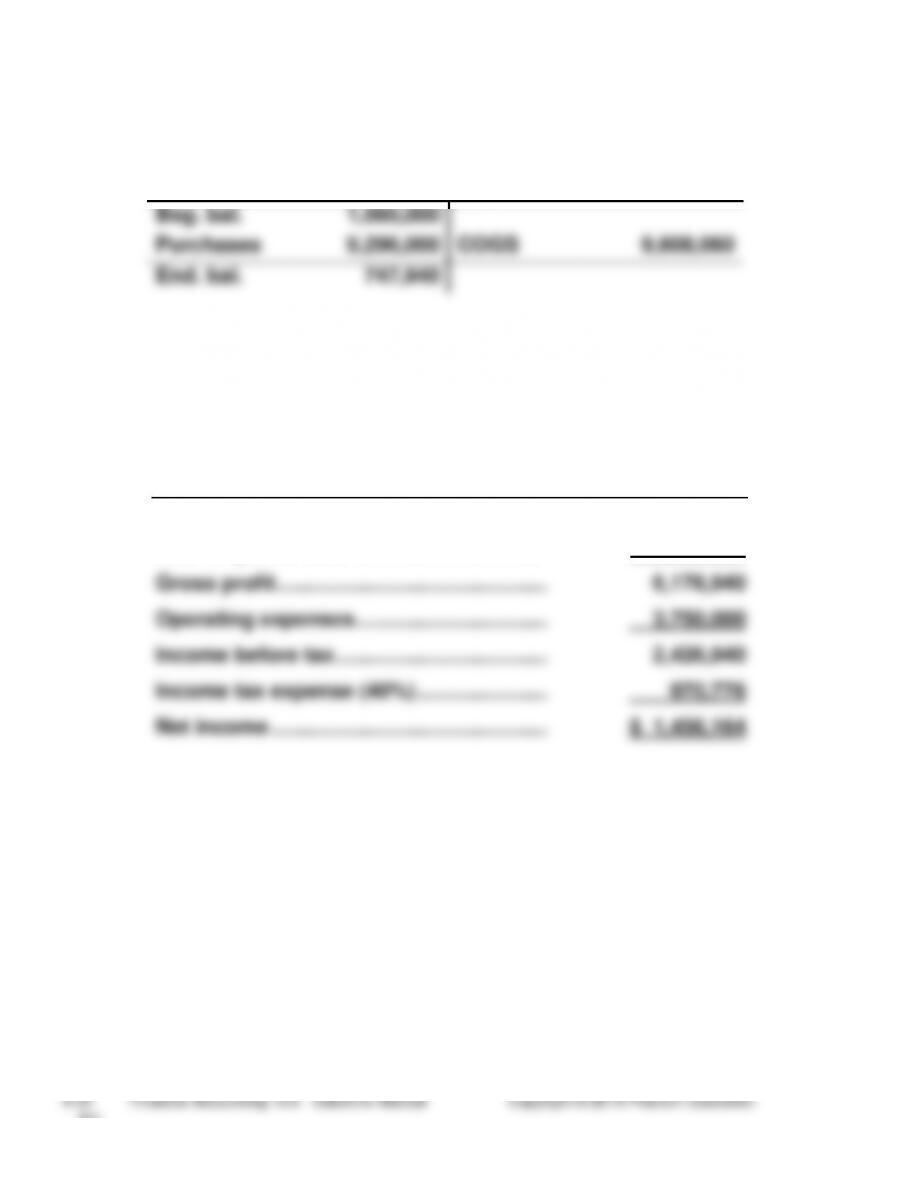

Inventory

Beg. bal.

1,060,000

Purchases

9,296,000

COGS

9,608,060

End. bal.

747,940

Req. 3

Big Buy Store, Miami

Income Statement

Year Ended January 31, 2014

Sales revenue ……………………………………

$15,785,000

Cost of goods sold …………………………….

9,608,060

Gross profit ……………………………………….

6,176,940

Operating expenses… ………………………..

3,750,000

Income before tax ………………………………

2,426,940

Income tax expense (40%) ………………….

970,776

Net income ………………………………………..

$ 1,456,164

(20-30 min.) P 6-55A

Req. 1

The store uses FIFO.

This is apparent from the flow of costs out of inventory. For example, the

Req. 2

Cost of goods sold:

15

×

$32

=

$ 480

29

×

32

=

928

11

×

34

=

374

30

×

34

=

1,020

$2,802

Sales [(44 units × $67) + (41 units x $68)] ………………………

$5,736

Cost of goods sold ……………………………………………………..

(2,802)

Gross profit ………………………………………………………………..

$2,934

Req. 3

Cost of August 31 inventory (38 × $34) + (26 × $36)

$2,228

Inc.

(20-30 min.) P 6-56A

Req. 1

Inventory

Beg. bal.

(67 units @ $25) 1,675

Purchases:

May 6

(101 units @ $27) 2,727

18

(163 units @ $29) 4,727

Cost of goods sold

26

(41 units @ $30) 1,230

(323 units @ $?)

?

End. bal.

(49 units @ $?) ?

Cost of Goods Sold

Ending Inventory

Average cost

323 × $27.85* = $8,996

49 × $27.85* = $1,365

____

*Average cost

=

($1,675 + $2,727 + $4,727 + $1,230)

= $27.85

per unit

(67 + 101 + 163 + 41)

FIFO

(67 @ $25) + (101 @ $27)

(41 @ $30) +

+ (155 @ $29)

= $8,897

(8 @ $29)

= $1,462

LIFO

(41 @ $30) + (163 @ $29) +

(101 @ $27) + (18 @ $25)

= $9,134

49 @ $25

= $1,225

(continued) P 6-56A

Req. 2

LIFO cost of goods sold is highest because (a) prices are rising and (b)

Req. 3

Camp Surplus

Income Statement

Month Ended May 31, 2014

Sales revenue (323 x $51) ……………………………………

$16,473

Cost of goods sold ……………………………………………..

8,996

Gross profit ………………………………………………………..

7,477

Operating expenses ……………………………………………

3,250

Income before income taxes ………………………………..

4,227

Income tax expense (30%) …………………………………..

1,268

Net income …………………………………………………………

$ 2,959

(30-40 min.) P 6-57A

Req. 1 (partial income statements)

Fisher Aviation

Partial Income Statement

Year Ended July 31, 2014

AVERAGE

FIFO

LIFO

Sales revenue

$128,560

$128,560

$128,560

Cost of goods sold

68,652

68,258

69,020

Gross profit

$ 59,908

$ 60,302

$ 59,540

Computations of cost of goods sold:

Average cost

=

($5,148 + $2,880 + $63,992 + $3,984)

=

$7.59

per unit

(720 + 400 + 8,420 + 480)

Average cost COGS = 9,045 × $7.59

=

$68,652

FIFO COGS

=

(720 @ $7.15) + (400 @ $7.20) + (7,925 @ $7.60)

=

$68,258

LIFO COGS

=

(480 @ $8.30) + (8,420 @ $7.60) + (145 @ $7.20)

=

$69,020

Req. 2

(15-30 min.) P 6-58A

a. Canton Trade Mart should apply the lower-of-cost-or-market rule to

b.

Cost of Goods Sold ……………………..

7,000

Inventory ………………………………

7,000

To write inventory down to market value.

Canton Trade Mart should report the following amounts in its financial

statements:

c.

BALANCE SHEET

Inventory at market (which is lower than

cost of $98,000) ………………………………………………..

$91,000*

d.

INCOME STATEMENT

Cost of goods sold ($410,000 + $7,000) …………………

$417,000

_____

*$98,000 − $7,000 = $91,000

e. Relevance and Representational faithfulness are the reasons to account

for inventory at the lower of cost or market value. Representational

Student responses may vary.

Inc.

(20-25 min.) P 6-59A

Req. 1

Sweet Treats, Inc.

Coffee Time Corp.

Dollars in Millions

Gross profit percentage:

Sales ………………………….

$542

$7,777

Cost of goods sold ……..

474

3,180

Gross profit ………………..

$ 68

$4,597

Gross profit

$68

= 12.5%

$4,597

= 59.1%

percentage:

$542

$7,777

Inventory turnover:

Cost of goods sold

=

$474

$3,180

Average inventory

($36 + $20) / 2

($541 + $625) / 2

= 16.9 times

= 5.5 times

Req. 2

These statistics are unclear. The numbers suggest that Coffee Time

Corp. should be more profitable because it has a higher gross profit

(25-30 min.) P 6-60A

Req. 1 (estimate of ending inventory by the gross profit method)

Beginning inventory ………………………………..

$ 67,200

Purchases ………………………………………………

$410,800

Less: Purchase discounts ……………………

(15,000)

Purchase returns ………………………..

(10,600)

Net purchases …………………………………….

385,200

Cost of goods available …………………………..

452,400

Cost of goods sold:

Sales revenue ……………………………………..

$695,000

Less: Sales returns …………………………..

(12,000)

Net sales …………………………………………….

683,000

Less: Estimated gross profit of 45%……..

(307,350)

Estimated cost of goods sold ………………

375,650

Estimated cost of ending inventory ………….

$ 76,750

(continued) P 6-60A

Req. 2 (income statement through gross profit)

Whitfield Company

Income Statement (partial)

Two Week Period Ending August 15 (date of the fire)

Sales revenue ……………………………………………

$695,000

Less: Sales returns …………………………………….

(12,000)

Net sales revenue ………………………………….

683,000

Cost of goods sold …………………………………….

375,650*

Gross profit ……………………………………………….

$307,350

_____

*Cost of goods sold:

Beginning inventory ………………………………………..

$ 67,200

Purchases ………………………………..

$410,800

Less: Purchases discounts ……….

(15,000)

Purchase returns ……………..

(10,600)

Net purchases ………………………………………………..

385,200

Cost of goods available for sale ………………………

452,400

Less: Ending inventory …………………………………..

(76,750)

Cost of goods sold …………………………………………

$375,650