(15-20 min.) E 9-41B

Req. 1 Using the PV function in EXCEL, the issue price of the bonds is

$3,072,290.

Req. 2 (amortization table)

A

B

C

D

E

Semiannual

Interest Date

Interest

Payment

(2% of

Maturity

Value)

Interest

Expense

(2.25% of

Preceding

Bond

Carrying

Amount)

Discount

Amortization

(B – A)

Discount

Account

Balance

(Preceding

D – C)

Bond

Carrying

Amount

($3,200,000

– D)

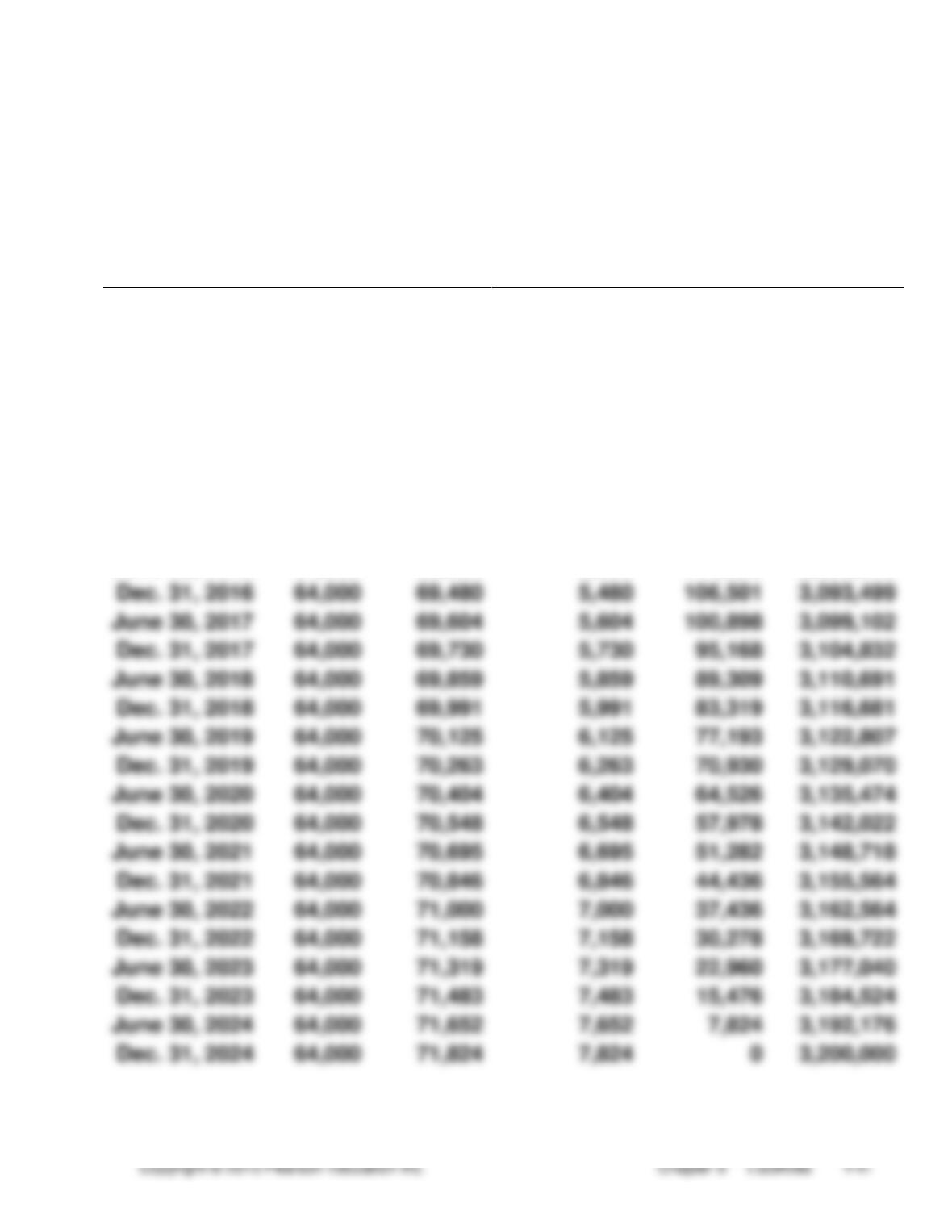

Dec. 31, 2014

127,710

3,072,290

June 30, 2015

64,000

69,127

5,127

122,583

3,077,417

Dec. 31, 2015

64,000

69,242

5,242

117,342

3,082,658

June 30, 2016

64,000

69,360

5,360

111,982

3,088,018

Dec. 31, 2016

64,000

69,480

5,480

106,501

3,093,499

June 30, 2017

64,000

69,604

5,604

100,898

3,099,102

Dec. 31, 2017

64,000

69,730

5,730

95,168

3,104,832

June 30, 2018

64,000

69,859

5,859

89,309

3,110,691

Dec. 31, 2018

64,000

69,991

5,991

83,319

3,116,681

June 30, 2019

64,000

70,125

6,125

77,193

3,122,807

Dec. 31, 2019

64,000

70,263

6,263

70,930

3,129,070

June 30, 2020

64,000

70,404

6,404

64,526

3,135,474

Dec. 31, 2020

64,000

70,548

6,548

57,978

3,142,022

June 30, 2021

64,000

70,695

6,695

51,282

3,148,718

Dec. 31, 2021

64,000

70,846

6,846

44,436

3,155,564

June 30, 2022

64,000

71,000

7,000

37,436

3,162,564

Dec. 31, 2022

64,000

71,158

7,158

30,278

3,169,722

June 30, 2023

64,000

71,319

7,319

22,960

3,177,040

Dec. 31, 2023

64,000

71,483

7,483

15,476

3,184,524

June 30, 2024

64,000

71,652

7,652

7,824

3,192,176

Dec. 31, 2024

64,000

71,824

7,824

0

3,200,000

(continued) E 9-41B

Req. 3 (journal entries)

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Dec.

31

Cash ……………………………………………..

3,072,290

Discount on Bonds Payable ……………

127,710

Bonds Payable ………………………….

3,200,000

To issue bonds at a discount.

2015

June

30

Interest Expense …………………………...

69,127

Cash …………………………………………

64,000

Discount on Bonds Payable ……….

5,127

To pay semiannual interest and

amortize bond discount.

2015

Dec.

31

Interest Expense …………………………...

69,242

Cash …………………………………………

64,000

Discount on Bonds Payable ……….

5,242

To pay semiannual interest and

amortize bond discount.

(15-20 min.) E 9-42B

Req. 1 Using the PV function in EXCEL, the issue price of the bonds is

$1,792,127.

Req. 2 (amortization table)

A

B

C

D

E

Semiannual

Interest Date

Interest

Payment

(2% of

Maturity

Value)

Interest

Expense

(1.5% of

Preceding

Bond

Carrying

Amount)

Premium

Amortization (A –

B)

Premium

Account

Balance

(Preceding D –

C)

Bond Carrying

Amount

($1,600,000 +

D)

June 30, 2014

192,127

1,792,127

Dec. 31, 2014

32,000

26,882

5,118

187,009

1,787,009

June 30, 2015

32,000

26,805

5,195

181,814

1,781,814

Dec. 31, 2015

32,000

26,727

5,273

176,541

1,776,541

June 30, 2016

32,000

26,648

5,352

171,189

1,771,189

Dec. 31, 2016

32,000

26,568

5,432

165,757

1,765,757

June 30, 2017

32,000

26,486

5,514

160,244

1,760,244

Dec. 31, 2017

32,000

26,404

5,596

154,647

1,754,647

June 30, 2018

32,000

26,320

5,680

148,967

1,748,967

Dec. 31, 2018

32,000

26,235

5,765

143,201

1,743,201

June 30, 2019

32,000

26,148

5,852

137,349

1,737,349

Dec. 31, 2019

32,000

26,060

5,940

131,410

1,731,410

June 30, 2020

32,000

25,971

6,029

125,381

1,725,381

Dec. 31, 2020

32,000

25,881

6,119

119,262

1,719,262

June 30, 2021

32,000

25,789

6,211

113,050

1,713,050

Dec. 31, 2021

32,000

25,696

6,304

106,746

1,706,746

June 30, 2022

32,000

25,601

6,399

100,347

1,700,347

Dec. 31, 2022

32,000

25,505

6,495

93,853

1,693,853

June 30, 2023

32,000

25,408

6,592

87,260

1,687,260

Dec. 31, 2023

32,000

25,309

6,691

80,569

1,680,569

June 30, 2024

32,000

25,209

6,791

73,778

1,673,778

Dec. 31, 2024

32,000

25,107

6,893

66,885

1,666,885

June 30, 2025

32,000

25,003

6,997

59,888

1,659,888

Dec. 31, 2025

32,000

24,898

7,102

52,786

1,652,786

June 30, 2026

32,000

24,792

7,208

45,578

1,645,578

Dec. 31, 2026

32,000

24,684

7,316

38,262

1,638,262

June 30, 2027

32,000

24,574

7,426

30,836

1,630,836

Dec. 31, 2027

32,000

24,463

7,537

23,298

1,623,298

June 30, 2028

32,000

24,349

7,651

15,648

1,615,648

Dec. 31, 2028

32,000

24,235

7,765

7,882

1,607,882

June 30, 2029

32,000

24,118

7,882

0

1,600,000

(continued) E 9-42B

Req. 3 (journal entries)

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

June

30

Cash ……………………………………………….

1,792,127

Bonds Payable …………………………...

1,600,000

Premium on Bonds Payable …………

192,127

To issue bonds at a premium.

Dec.

31

Interest Expense ……………………………..

26,882

Premium on Bonds Payable ……………..

5,118

Cash …………………………………………..

32,000

To pay semiannual interest and amortize

bond premium.

2015

June

30

Interest Expense ……………………………..

26,805

Premium on Bonds Payable ……………..

5,195

Cash …………………………………………..

32,000

To pay semiannual interest and amortize

bond premium.

(15-20 min.) E 9-43B

Req. 1

The company has the right to occupy space and operate out of leased

stores for several years to come. In return, the company is obligated to

Req. 2

The rights and obligations discussed in Req. 1 are classified as

Req. 3

In the future, the FASB and IASB are proposing to eliminate the current

accounting treatment of most operating leases. If this rule change

(20-25 min.) E 9-44B

Amounts in millions or billions

Company

Company

Company

Ratio

F

K

R

Current

=

Total current assets

=

$434

¥5,383

€148,526

ratio

Total current liabilities

$207

¥2,197

€72,600

= 2.10

= 2.45

= 2.05

F

K

R

Debt

=

Total liabilities

=

$207 + $116

¥2,197 + ¥2,318

€72,600 + €110,107

ratio

Total assets

$434 + $114

¥5,383 + ¥405

€148,526 + €49,525

= 0.59

= 0.78

= 0.92

F

K

R

Leverage

ratio

=

Total assets

=

$548

¥5,788

€198,051

Tot. stockholders’

equity

$225

¥1,273

€15,344

= 2.44

= 4.55

= 12.91

F

K

R

Times-

interest-

=

Operating income

=

$239

¥224

€5,692

earned

Interest expense

$46

¥33

€736

ratio

= 5.2 times

= 6.8 times

= 7.7 times

(15-20 min.) E 9-45B

Req. 1

PLAN A

BORROW

$900,000

AT 5%

PLAN B

ISSUE

$900,000

OF COMMON

STOCK

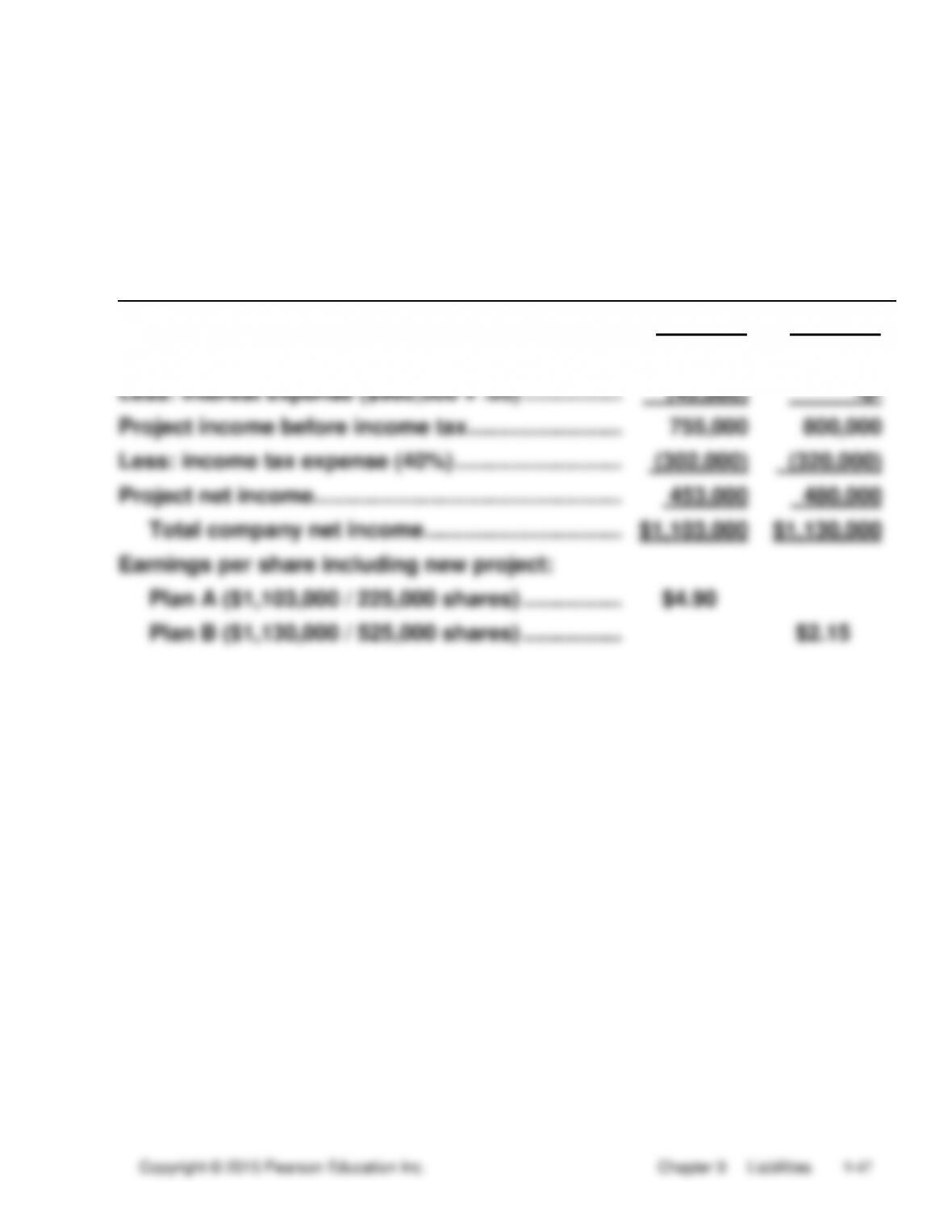

Net income before expansion …………………………..

$650,000

$650,000

Project income before interest and income tax ….

$800,000

$800,000

Less: interest expense ($900,000 × .05) …………….

(45,000)

-0-

Project income before income tax …………………….

755,000

800,000

Less: income tax expense (40%) ………………………

(302,000)

(320,000)

Project net income …………………………………………..

453,000

480,000

Total company net income …………………………..

$1,103,000

$1,130,000

Earnings per share including new project:

Plan A ($1,103,000 / 225,000 shares) …………….

$4.90

Plan B ($1,130,000 / 525,000 shares) …………….

$2.15

(continued) E 9-45B

Req. 2

MEMORANDUM

TO: Board of Directors of RRS Financial Services

FROM: Student Name

SUBJECT: Financing plan to expand operations

Plan A (borrowing) results in much higher earnings per share. Plan A

also allows the existing stockholders to retain control of the company

Quiz

Q9–46

b

Q9–47

c

Q9–48

a

Q9–49

d

Q9-50

c

Q9-51

d

[($650,000 + $850,000) × .07] – $5,200 − $42,500 = $57,300

Q9-52

a

Q9-53

b

Q9-54

f

Q9–55

a

Q9–56

c

Q9–57

c

($400,000 × .05) + [($400,000 − $388,000) / 10] = $21,200

Q9–58

Interest Expense…………………………………………

15,900

Discount on Bonds Payable

($12,000 / 10 × 9/12) ……………………………….

900

Interest Payable ($400,000 × .05 × 9/12) ……

15,000

Q9–59

Interest Payable ………………………………………….

15,000

Interest Expense…………………………………………

5,300

Discount on Bonds Payable

($12,000 / 10 × 3/12) ………………………………

300

Cash ($400,000 × .05) ……………………………..

20,000

Q9-60

b

($367,297 x .02) = $7,346

Q9-61

d

Q9-62

b

Q9-63

a

Q9-64

c

Problems

(15-20 min.) P 9-65A

a. Sales tax payable ($180,000 × .06) ………………………………….

$10,800

b. Note payable, short-term ……………………………………………….

$78,000

Interest payable ($78,000 × .04 × 4/12) …………………………….

1,040

c. Unearned service revenue ($5,000 × 2/6) ………………………..

$1,667

d. Estimated warranty payable

($9,600 + $32,000 − $29,900) ………………………………………

$11,700

e. Portion of long-term note payable due

within one year …………………………………………………………

$20,000

Interest payable ($100,000 × .035) …………………………………..

3,500

(30-40 min.) P 9-66A

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Mar.

3

Inventory ………………………………………………..

52,000

Note Payable, Short-term …………………….

52,000

May

31

Cash ………………………………………………………

96,000

Note Payable, Short-term …………………….

16,000

Note Payable, Long-term …………………….

80,000

Sept.

3

Note Payable, Short-term …………………………

52,000

Interest Expense ($52,000 × .04 × 6/12) ……..

1,040

Cash ………………………………………………….

53,040

Dec.

31

Warranty Expense ($216,000 × .025) …………

5,400

Estimated Warranty Payable ……………….

5,400

31

Interest Expense ($96,000 × .035 × 7/12) ……

1,960

Interest Payable ………………………………….

1,960

2015

May

31

Note Payable, Short-term …………………………

16,000

Interest Payable …………………………..………….

1,960

Interest Expense ($96,000 × .035 × 5/12) ……

1,400

Cash ………………………………………………….

19,360

(20-25 min.) P 9-67A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

a.

May

31

Cash ($6,000,000 × 1/2) ………………..

3,000,000

Bonds Payable ………………………..

3,000,000

To issue bonds at par.

b.

Nov.

30

Interest Expense ………………………….

75,000

Cash ($3,000,000 × .05 × 6/12) ….

75,000

To pay interest on bonds.

c.

Dec.

31

Interest Expense

($3,000,000 × .05 × 1/12) ……………….

12,500

Interest Payable ………………………

12,500

To accrue interest.

2015

d.

May

31

Interest Payable …………………………..

12,500

Interest Expense

($3,000,000 × .05 × 5/12) ……………….

62,500

Cash ($3,000,000 × .05 × 6/12) ….

75,000

To pay interest on bonds.

30-40 min.) P 9-68A

Req. 1

Req. 2

(continued) P 9-68A

Req. 3

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

a.

Feb.

28

Cash ($900,000 × .95) ………………………….

855,000

Discount on Bonds Payable ………………..

45,000

Bonds Payable ……………………………….

900,000

To issue bonds at a discount.

b.

Aug.

31

Interest Expense …………………………………

24,750

Cash ($900,000 × .05 × 6/12) ……………

22,500

Discount on Bonds Payable

($45,000 / 20) ……………………………….

2,250

To pay interest and amortize bond

discount.

c.

Dec.

31

Interest Expense …………………………………

16,500

Interest Payable ($22,500 × 4/6) ……….

15,000

Discount on Bonds Payable

($2,250 × 4/6) ……………………………….

1,500

To accrue interest and amortize bond

discount.

2015

d.

Feb.

28

Interest Payable (from Dec. 31) ……………

15,000

Interest Expense …………………………………

8,250

Cash ($900,000 × .05 × 6/12) ……………

22,500

Discount on Bonds Payable

($2,250 × 2/6) ……………………………….

750

To pay interest and amortize bond

discount.

Req. 4 (reporting the liabilities on the balance sheet at Dec. 31, 2014)

Current liabilities:

Interest payable ……………………………………

$ 15,000

Long-term liabilities:

Bonds payable ……………………………………..

$900,000

Less: Discount on bonds payable

($45,000 − $2,250 − $1,500) …………

(41,250)

858,750

(30-40 min.) P 9-69A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Jan.

1

Cash ($3,000,000 × .95) …………………………

2,850,000

Discount on Bonds Payable ………………….

150,000

Bonds Payable …………………………………

3,000,000

To issue bonds at a discount.

July

1

Interest Expense …………………………………..

67,500

Cash ($3,000,000 × .04 × 6/12) ……………

60,000

Discount on Bonds Payable

($150,000 / 20) ……………………………….

7,500

To pay interest and amortize bond discount.

Dec.

31

Interest Expense …………………………………..

67,500

Interest Payable

($3,000,000 × .04 × 6/12) …………………

60,000

Discount on Bonds Payable ……………

7,500

To accrue interest and amortize bond discount.

2015

Jan.

1

Interest Payable …………………………………..

60,000

Cash ……………………………………………….

60,000

To pay interest.

2024

Jan.

1

Bonds Payable ……………………………………..

3,000,000

Cash ………………………………………………..

3,000,000

To pay bonds at maturity.

(continued) P 9-69A

Req. 2

Carrying amount at Dec. 31, 2014:

Bonds payable, net

($3,000,000 − $150,000 + $7,500 + $7,500) ………………………

$2,865,000

Req. 3

(30-45 min.) P 9-70A

Req. 1

a. Using the PV function in EXCEL, the issue price of the bonds is

$4,943,165.

Req. 2 (amortization table)

A

B

C

D

E

Semiannual

Interest Date

Interest

Payment

(3% of

Maturity

Value)

Interest

Expense

(4% of

Preceding

Bond

Carrying

Amount)

Discount

Amortization

(B – A)

Discount

Account

Balance

(Preceding

D – C)

Bond

Carrying

Amount

($5,300,000

– D)

Jan. 1, Yr. 1

356,835

4,943,165

Dec. 31, Yr. 1

159,000

197,727

38,727

318,108

4,981,892

Dec. 31, Yr. 2

159,000

199,276

40,276

277,833

5,022,167

Dec. 31, Yr. 3

159,000

200,887

41,887

235,946

5,064,054

Dec. 31, Yr. 4

159,000

202,562

43,562

192,384

5,107,616

Dec. 31, Yr. 5

159,000

204,305

45,305

147,079

5,152,921

Dec. 31, Yr. 6

159,000

206,117

47,117

99,962

5,200,038

Dec. 31, Yr. 7

159,000

208,002

49,002

50,961

5,249,039

Dec. 31, Yr. 8

159,000

209,962

50,961

0

5,300,000

(continued) P 9-70A

Req. 3 (reporting the liabilities at Dec. 31, Year 4)

Current liabilities:

Current installment of notes payable …………

$ 55,000

Long-term liabilities:

Bonds payable …………………………………………

$5,300,000

Less: Discount on bonds payable …………..

(192,384)

5,107,616

Notes payable…………………………………………..

($330,000 – $55,000)

275,000

(40-50 min.) P 9-71A

Req. 1 Using the PV function in EXCEL, the issue price of the bonds is

$3,851,225.

Req. 2 (amortization table)

A

B

C

D

E

Semiannual

Interest Date

Interest

Payment

(2.75%

of

Maturity

Value)

Interest

Expense

(3% of

Preceding

Bond

Carrying

Amount)

Discount

Amortization

(B – A)

Discount

Account

Balance

(Preceding

D – C)

Bond

Carrying

Amount

($4,000,000

– D)

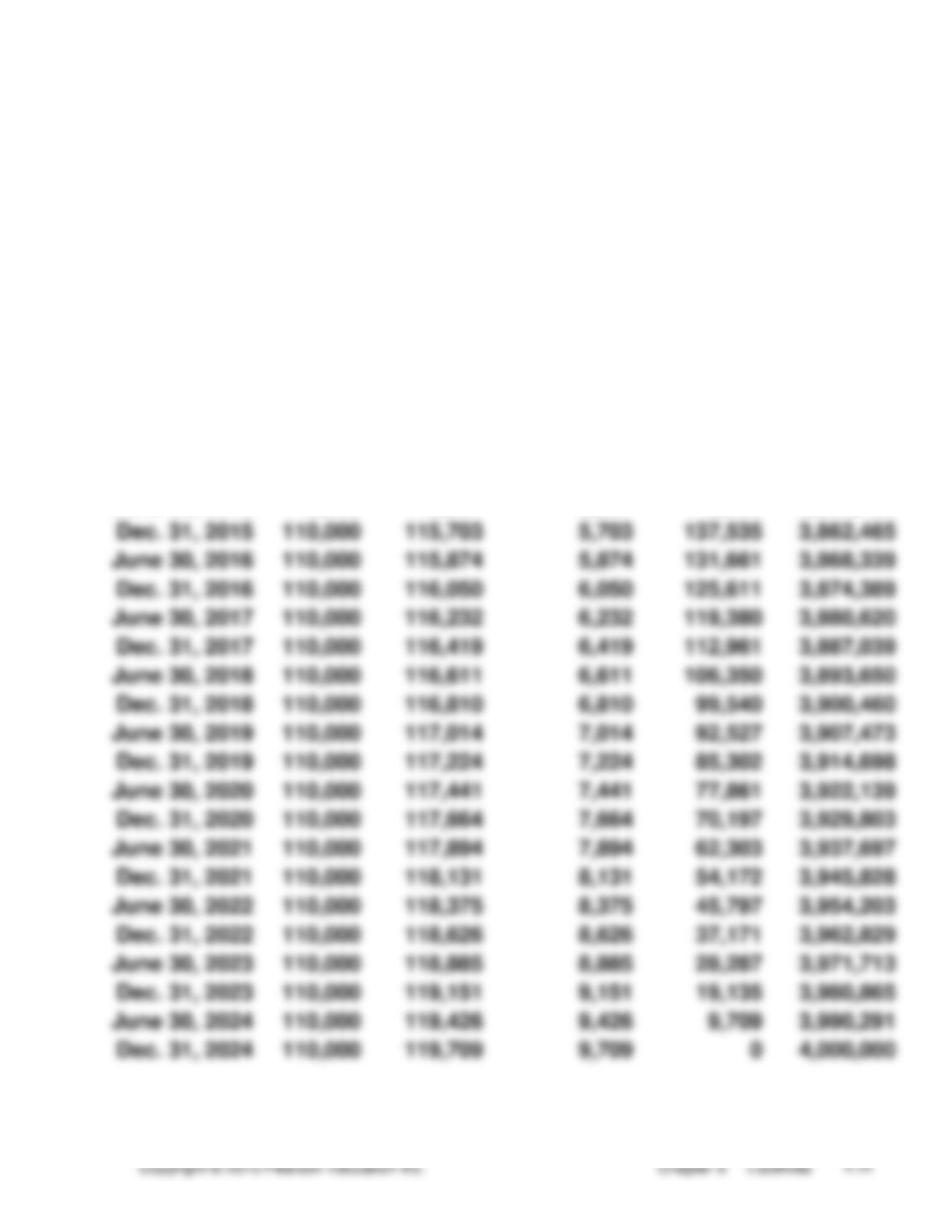

Dec. 31, 2014

148,775

3,851,225

June 30, 2015

110,000

115,537

5,537

143,238

3,856,762

Dec. 31, 2015

110,000

115,703

5,703

137,535

3,862,465

June 30, 2016

110,000

115,874

5,874

131,661

3,868,339

Dec. 31, 2016

110,000

116,050

6,050

125,611

3,874,389

June 30, 2017

110,000

116,232

6,232

119,380

3,880,620

Dec. 31, 2017

110,000

116,419

6,419

112,961

3,887,039

June 30, 2018

110,000

116,611

6,611

106,350

3,893,650

Dec. 31, 2018

110,000

116,810

6,810

99,540

3,900,460

June 30, 2019

110,000

117,014

7,014

92,527

3,907,473

Dec. 31, 2019

110,000

117,224

7,224

85,302

3,914,698

June 30, 2020

110,000

117,441

7,441

77,861

3,922,139

Dec. 31, 2020

110,000

117,664

7,664

70,197

3,929,803

June 30, 2021

110,000

117,894

7,894

62,303

3,937,697

Dec. 31, 2021

110,000

118,131

8,131

54,172

3,945,828

June 30, 2022

110,000

118,375

8,375

45,797

3,954,203

Dec. 31, 2022

110,000

118,626

8,626

37,171

3,962,829

June 30, 2023

110,000

118,885

8,885

28,287

3,971,713

Dec. 31, 2023

110,000

119,151

9,151

19,135

3,980,865

June 30, 2024

110,000

119,426

9,426

9,709

3,990,291

Dec. 31, 2024

110,000

119,709

9,709

0

4,000,000

(continued) P 9-71A

Req. 3

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

a.

Dec.

31

Cash ……………………………………………..

3,851,225

Discount on Bonds Payable ……………

148,775

Convertible Bonds Payable ………..

4,000,000

To issue bonds at a discount.

2015

b.

June

30

Interest Expense …………………………….

115,537

Cash …………………………………………

110,000

Discount on Bonds Payable ……….

5,537

To pay interest and amortize bond

discount.

c.

Dec.

31

Interest Expense …………………………….

115,703

Cash …………………………………………

110,000

Discount on Bonds Payable ……….

5,703

To pay interest and amortize bond

discount.

2016

d.

July

1

Convertible Bonds Payable …………….

1,600,000

Discount on Bonds Payable

($131,661 × 2/5) ……………………..

52,664

Common Stock (120,000 × $1) …….

120,000

Paid-in Capital in Excess of

Par — Common ……………………..

1,427,336

To record conversion of bonds.

Req. 4 (balance sheet presentation of bonds payable at

Dec. 31, 2016)

Convertible bonds payable

($4,000,000 − $1,600,000) ………………………

$2,400,000

Less: Discount on bonds payable

($125,611 × 3/5*) ……………………………………

(75,367)

2,324,633

_____

*3/5 of the bonds are outstanding, so 3/5 of the discount remains.