Chapter 4

Internal Control & Cash

Short Exercises

(5 min.) S 4-1

Fraud is an intentional misrepresentation of facts, made for the

purpose of persuading another party to act in such a way that causes

injury or damage to that party.

The Three Components of the Fraud Triangle

1. Motive — Fraud generally results from either critical need or greed on

2. Opportunity — The opportunity to commit fraud usually arises

through weak internal controls.

3. Rationalization — The perpetrator(s) is (are) convinced, in their own

(5 min.) S 4-2

Clyde should report the errors to Lusk because Lusk is Clyde’s

(10 min.) S4-3

A computer virus enters program code without your consent and

performs destructive action to your computer files or programs.

(5-10 min.) S 4-4

COMPONENTS OF INTERNAL CONTROL

1. Control environment — Top managers must set the “tone at the top”

to establish a control environment.

5. Information system — Accurate information is essential for success

in business. Accounting information enters and exits through the

information system.

Student responses may vary for the descriptions.

(5-10 min.) S 4-5

Separation of duties is essential for safeguarding assets. The person

Student responses may vary.

(5-10 min.) S 4-6

There are several major internal control procedures as discussed in the

chapter besides separation of duties:

1. Smart hiring practices. The company should be careful to hire both

2. Comparisons and compliance monitoring. No person or department

should be allowed to completely process a transaction from beginning

(continued) S 4-6

5. Proper approvals. No transaction should be processed without

management’s general or specific approval. Generally, the larger the

transaction, the higher the organizational level of approval necessary.

Notice that the first letters of these attributes spell the acronym SCALP.

(20-30 min.) S 4-8

Punching a hole through supporting documents reduces the

opportunity for fraud. Without this control procedure, a dishonest

(10 min.) S 4-9

Vincente Corp.

Bank Reconciliation

August 31, 2014

BANK

BOOKS

Balance, August 31

$4,775

Balance, August 31

$3,640

Add: Deposit in transit

300

Add: Bank collection

685

5,075

Interest revenue

20

4,345

Less:

Less:

Outstanding checks

(800)

Service charge

(15)

NSF check

(55)

Adjusted bank balance

$4,275

Adjusted book balance

$4,275

Vincente has cash of $4,275.

(5 min.) S 4-10

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Aug.

31

Cash………………………………………..

685

Accounts Receivable…………………

685

Collection on account.

31

Cash………………………………………..

20

Interest Revenue………………………

20

Interest earned on bank balance.

31

Miscellaneous Expense…………………

15

Cash…………………………………….

15

Bank service charge.

31

Accounts Receivable……………………

55

Cash……………………………………..

55

NSF check.

(5 min.) S 4-11

It appears that the employee has stolen $710 (adjusted book balance,

$3,300 − adjusted bank balance, $2,590). The adjusted bank balance is

1. Paying by check carries three controls over cash:

• The check provides a record of the payment.

2. A dishonest purchasing agent could:

Companies avoid this internal control weakness by separating the

following duties related to the purchase of, and payment for, goods:

(5-10 min.) S 4-14

Farm-to-Market (FM)

Cash Budget

Year 2015

Millions

Cash balance, beginning

$ 7

Estimated cash receipts—total

103

110

Estimated cash payments—total

(97)

Cash available (needed) before new financing

13

Budgeted cash balance needed

(11)

Cash available for additional investments

$ 2

(5 min.) S 4-15

“Cash and cash equivalents” includes liquid assets such as time

Exercises

(5-20 min.) E 4-16A

a. Higaredo has access to the cash collected, and he also prepares the

(10 min.) E 4-17A

Cash payments:

a. Strong internal control. There is a good separation of duties.

Cash receipts:

a. Weak internal control. There is not a good separation of duties. The

(10 min.) E 4-18A

To prevent Munson’s embezzlement, Downtown Columbia’s board of

directors could have:

a. Not permitted Munson to write checks for Downtown Columbia.

Instead, appoint a board member to write the checks.

(10-20 min.) E 4-19A

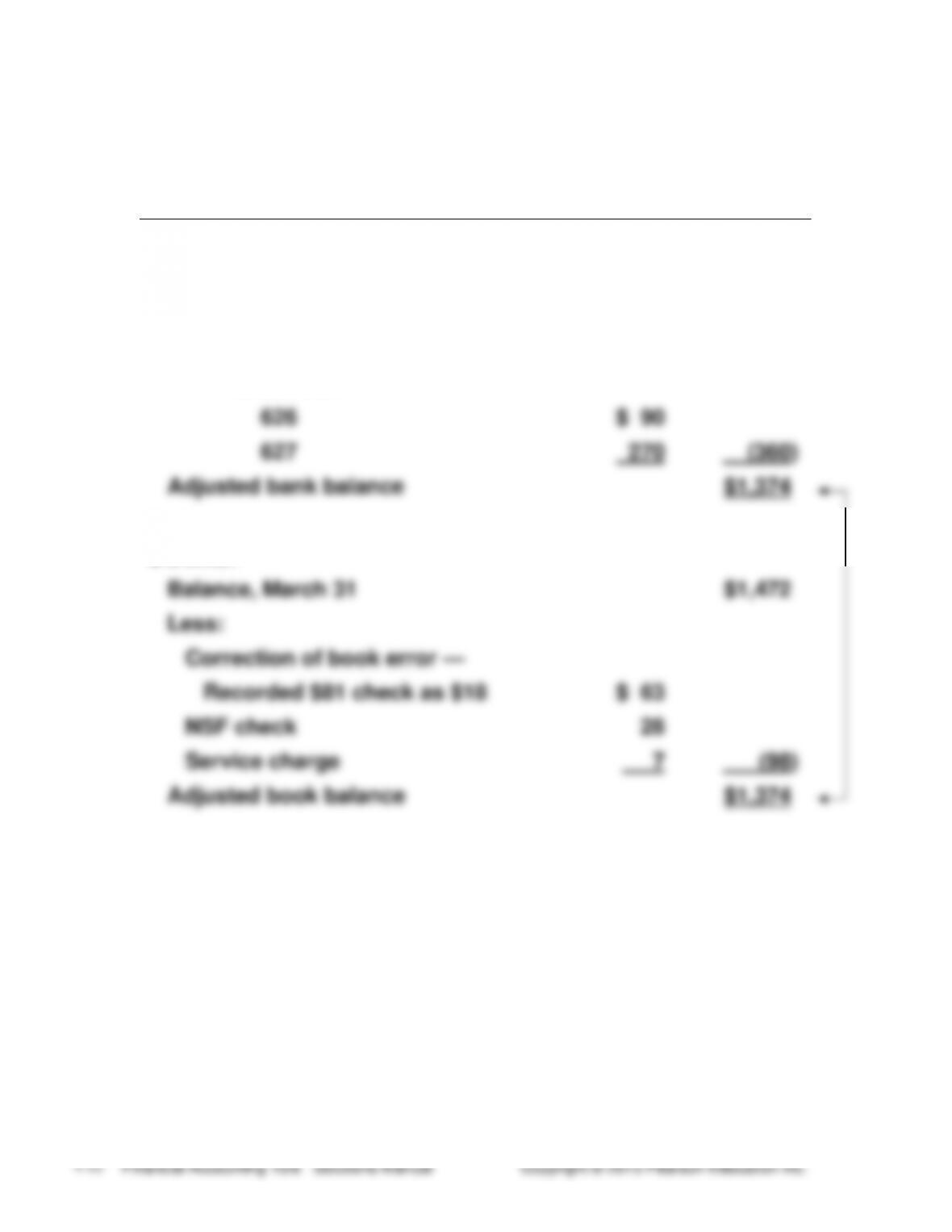

F.L. Callan

Bank Reconciliation

March 31, 2015

BANK:

Balance, March 31

$ 409

Add: Deposit in transit

1,325

Less: Outstanding checks:

Check No.

626

$ 90

627

270

(360)

Adjusted bank balance

$1,374

BOOKS:

Balance, March 31

$1,472

Less:

Correction of book error —

Recorded $81 check as $18

$ 63

NSF check

28

Service charge

7

(98)

Adjusted book balance

$1,374

(10-20 min.) E 4-20A

Ryan Patrick

Bank Reconciliation

June 30, 2014

BANK:

Balance, June 30

$ 750

Add: Deposit in transit

1,765

2,515

Less: Outstanding checks

(610)

Adjusted bank balance

$1,905

BOOKS:

Balance, June 30

$1,876

Add: EFT collection — rent

409

2,285

Less:

Service charge

$ 7

NSF checks

120

Charge for printed checks

10

Correction of book error —

recorded $270 check as $27

243

(380)

Adjusted book balance

$1,905

Patrick’s actual cash balance is $1,905.

(10-15 min.) E 4-21A

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

June

30

Cash ……………………………………………………..

409

Rent Revenue ……………………………………

409

EFT collection of rent.

30

Miscellaneous Expense ($7 + $10) …………..

17

Cash…………………………………………………

17

Bank service charge and charge

for printed checks.

30

Accounts Receivable ……………………………..

120

Cash…………………………………………………

120

NSF checks returned by bank.

30

Salary Expense ($270 − $27) …………………..

243

Cash…………………………………………………

243

Correction of book error.

(10-15 min.) E 4-22A

TO: Store Manager

FROM: Student

SUBJECT: Evaluation of internal control and plan for improvement

There is a weakness in internal control over cash receipts. The cash

registers do not keep a record of sales. With no record, there is no way

(10-15 min.) E 4-23A

The main internal control weakness is that the payroll department both

(20-30 min.) E 4-24A

Dexter Communications, Inc.

Cash Budget

Year Ended December 31, 2015

Millions

Cash balance, December 31, 2014

$ 68

Budgeted cash receipts:

Collections from customers

11,325

Sale of assets

157

11,550

Budgeted cash payments:

Payments for cost of

services and products

$6,196

Payments of operating expenses

2,553

Investment in equipment

1,822

Payment of debt

538

Payment of dividends

348

11,457

Cash available (needed) before financing

93

Budgeted cash balance, December 31, 2015

(70)

Cash available for additional investments, or

(New financing needed)

$ 23

Dexter Communications expects to have cash available for additional

investments of $23 million during 2015.

(5-20 min.) E 4-25B

a. Kennedy has access to the cash collected, and he also prepares the

(10 min.) E 4-26B

Cash payments:

a. Strong internal control. There is a good separation of duties.

Supervisors request equipment, and the home office purchases the

equipment.

(10 min.) E 4-27B

To prevent Henry’s embezzlement, Downtown Huntsville’s board of

(10-20 min.) E 4-28B

A.C. Mazanek

Bank Reconciliation

May 31, 2014

BANK:

Balance, May 31

$ 405

Add: Deposit in transit

1,320

Less: Outstanding checks:

Check No.

626

$ 75

627

265

(340)

Adjusted bank balance

$1,385

BOOKS:

Balance, May 31

$1,452

Less:

Correction of book error —

Recorded $85 check as $58

$ 27

NSF check

37

Service charge

3

(67)

Adjusted book balance

$1,385