(15 min.) E 10-25A

Preferred

Common

Total

2014

Total dividend

$ 86,000

Preferred dividends in arrears:

2012: 90,000 shares × $1.00(par)

per share × .05 =

$4,500

2013: 90,000 shares × $1.00(par)

per share × .05 =

4,500

Preferred dividends, current year :

2014: 90,000 shares × $1.00(par)

per share × .05 =

4,500

Total to preferred

$13,500

Remainder to common

$72,500

2015

Total dividend

$264,000

Preferred dividends, current year:

2015: 90,000 shares × $1.00(par)

per share × .05 =

$4,500

Remainder to common

$259,500

(15-20 min.) E 10-26A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Apr.

16

Retained Earnings (750,000 × .15 × $20) ………

2,250,000

Common Stock (750,000 × .15 × $0.30) ……

33,750

Paid-in Capital in Excess of

Par – Common ……………………………………

2,216,250

To declare and distribute a common stock dividend.

Req. 2

Stockholders’ equity:

Common stock, $0.30 par, 2,600,000 shares authorized,

862,500 issued ($225,000 + $33,750) …………………..

$ 258,750

Paid-in capital in excess of par – common

($1,614,400 + $2,216,250) …………………………………..

3,830,650

Retained earnings ($7,154,000 − $2,250,000) …………..

4,904,000

Accumulated other comprehensive income (loss) …..

(200,000)

Total stockholders’ equity …………………………………

$8,793,400

Req. 3

The stock dividend did not change total stockholders’ equity because

Req. 4

(15-20 min.) E 10-27A

a. Decrease stockholders’ equity by $58 million.

b. No effect.

(10-15 min.) E 10-28A

Req. 1

Common:

Total stockholders’ equity ……………………………………….

$111,500

Less: Preferred equity — redemption value ………………

(40,000)

Total common equity……………………………………………….

$71,500

Book value per share ($71,500 / 6,000 shares) …………..

$ 11.92

Req. 2

Common:

Total stockholders’ equity …………………………………………

$ 111,500

Less: Preferred equity [$40,000 + ($31,500 × .05 × 3)]…..

(44,725)

Total common equity…………………………………………………

$ 66,775

Book value per share ($66,775 / 6,000 shares) …………….

$ 11.13

Req. 3

(10-15 min.) E 10–29A

Req. 1

Net

profit

=

Net income

=

$1,884

=

3.14%

margin

Net sales

$60,000

ratio

Asset

Net sales

=

$60,000

=

$60,000

=

1.11

turnover

=

Average total

($52,058* + $55,798**)/2

$53,928

assets

Leverage

Avg. total assets

=

$53,928

=

2.88

ratio

=

Avg. common

stkholders’ equity

($14,035 + $23,479) /2

Net profit

x

Asset

=

margin ratio

turnover

ROA

3.14%

x

1.11

=

3.5%

ROA

x

Leverage

=

ROE

ratio

3.5%

x

2.88

=

10.1%

_____

(continued) E 10-29A

Req. 2

These rates of return suggest relative weakness. The company is

generating a 3.14% net profit margin ratio (moderate effectiveness). The

Req. 3

(10 min.) E 10-30A

Cash flows from financing activities:

Payment of long-term debt ………………………………………

$(8,145)

Proceeds from issuance of common stock ……………….

9,420

Borrowings …………………………………………………………….

4,580

Dividends paid ………………………………………………………..

(324)

(20-25 min.) E 10-31A

Req. 1

(Thousands)

$3.50 Par

Common

Stock

Additional

Paid In

Capital

Retained

Earnings

Accum. Other

Comprehensive

Income

Total

Shareholders’

Equity

Balance, Dec. 31, 2013 ..

$395

$1,505

$4,700

$8

$6,608

Net earnings ………………

1,050

1,050

Other comprehensive

income ………………….

1

1

Issuance of stock ……….

140

70

210

Cash dividends …………..

(80)

(80)

Balance, Dec. 31, 2014 ..

$535

$1,575

$5,670

$9

$7,789

Req. 2

Req. 3

The year was profitable, as indicated by net earnings.

Req. 4

(10-15 min.) E 10–32B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

July

23

Cash …………………………………………………….

56,700

Common Stock …………………………………

4,200

Paid-in Capital in Excess of Par –

Common ………………………………………….

52,500*

Aug.

12

Inventory ………………………………………………

13,000

Equipment ……………………………………………

54,000

Common Stock …………………………………

3,300

Paid-in Capital in Excess of Par –

Common …………………………………………..

63,700*

Req. 2

Stockholders’ Equity

Common stock, $1.00 par, 13,000 shares authorized,

7,500 shares issued and outstanding………………………...

$ 7,500

Paid-in capital in excess of par − common …………………………

116,200*

Retained earnings …………………………………………………………….

51,600

Total stockholders’ equity …………………………………………….

$175,300

_____

*Computations:

July 23: 4,200 shares × ($13.50 − $1.00) = ……………………………….

$ 52,500

Aug. 12: $13,000 + $54,000 − (3,300 shares × $1.00) = …………….

63,700

$116,200

(10 min.) E 10-33B

Paid-in capital consists of:

Issued common stock for legal services …………………..

$ 21,000

Issued common stock for patent ………………………………

67,000

Issued preferred stock (2,000 shares × $120) …………….

Issued common stock for cash (16,000 shares × $6) ….

240,000

96,000

Total paid-in capital ………………………………………………….

$424,000

Unused data:

Net income

Dividends declared

Alternative short-cut solution:

1.

$ 21,000

2.

67,000

3.

240,000 (2,000 × $120)

4.

96,000 (16,000 × $6)

$424,000 = Total paid-in capital

(10-15 min.) E 10-34B

Stockholders’ Equity (Thousands)

Common stock, $2.50 par, 1,000 shares

authorized, 350 shares issued, 210 shares outstanding

$ 875

Paid-in capital in excess of par …………………………………….

900

Retained earnings ……………………………………………………….

2,341

Treasury stock, common, 140 shares at cost …………………

(1,820)

Accumulated other comprehensive income (loss) …………

(727)

Total stockholders’ equity ………………………………………..

$1,569

Treasury Stock has a larger balance than the sum of Common Stock

and Paid-in Capital in Excess of Par because Buffette Software paid a

higher price to acquire treasury stock than the price Buffette received

when it issued its stock.

(10 min.) E 10-35B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Millions

b.

Cash (9 million × $11.00) …………………………...

99

Common Stock (9 million × $2.00) ………….

18

Paid-in Capital in Excess of Par Value ……

81

c.

Treasury Stock ………………………………………….

12

Cash …………………………………………………….

12

d.

Cash …………………………………………………………

7

Treasury Stock ……………………………………..

6

Paid-in Capital from Treasury Stock

Transactions ……………………………………

1

e.

Retained Earnings …………………………………….

23

Dividends Payable ………………………………..

23

Dividends Payable …………………………………….

23

Cash …………………………………………………….

23

or one entry only:

Retained Earnings …………………………………….

23

Cash …………………………………………………….

23

*$12 / 1 = $12 cost per share of treasury stock

$12 x 0.50 = $6

Req. 2

(10 min.) E 10-36B

Dollars in

Millions

Stockholders’ Equity:

Common stock, $2.00 par value,

2,309 million shares issued ($4,600 + $18) ………………

$4,618

Paid in capital in excess of par value ($4,100 + $81) ..

4,181

Paid-in capital from treasury stock transactions …………

1

Retained earnings ($1,565 + $374 − $23) ……………………..

1,916

Treasury stock, at cost ($48 + $12 − $6) ………………………

(54)

Total stockholders’ equity ……………………………………..

$10,662

(20-30 min.) E 10-37B

Req. 1

Possible causes for preferred stock decrease:

Req. 2

Possible causes for common stock increase:

Common stock issued—

• To preferred stockholders who converted their preferred

Req. 3

(Millions

of shares

of stock)

Dec. 31, 2015

Common shares issued……………………………..

300

Less: Treasury stock, number of shares………

(24)

Common shares outstanding……………………….

276

(continued) E 10-37B

Req. 4

Retained Earnings (Millions)

Dec. 31, 2014

Bal.

5,135

Dividends

308

Net income

1,368

Dec. 31, 2015

Bal.

6,195

Req. 5 (All amounts in millions)

December 31,

Purchases

2015

2014

During 2015

Cost of treasury stock ……………………….

$270

−

$130

=

$ 140

Treasury stock, number of shares ……..

24

−

12

=

÷ 12

Average price per share paid for

treasury stock purchased during 2015 ……….

$11.67

(15 min.) E 10-38B

Preferred

Common

Total

2014

Total dividend

$109,000

Preferred dividends in arrears:

2012: 70,000 shares × $2.00(par)

per share × .06 =

$ 8,400

2013: 70,000 shares × $2.00(par)

per share × .06 =

8,400

Preferred dividends, current year :

2014: 70,000 shares × $2.00(par)

per share × .06 =

8,400

Total to preferred

$25,200

Remainder to common

$83,800

2015

Total dividend

$364,000

Preferred dividends, current year:

2015: 70,000 shares × $2.00(par)

per share × .06 =

$ 8,400

Remainder to common

$355,600

(15-20 min.) E 10-39B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

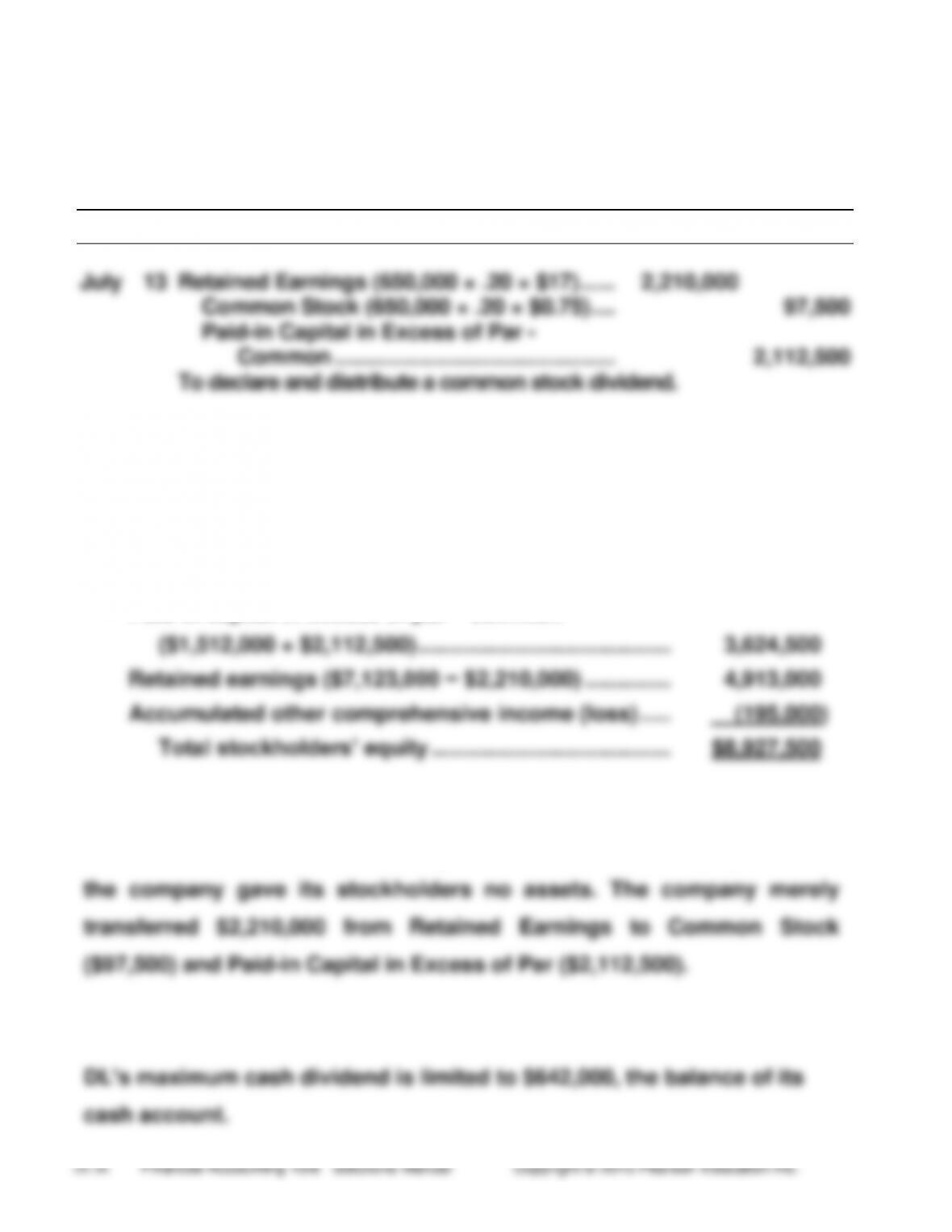

July

13

Retained Earnings (650,000 × .20 × $17) ……

2,210,000

Common Stock (650,000 × .20 × $0.75) ….

97,500

Paid-in Capital in Excess of Par –

Common ………………………………………..

2,112,500

To declare and distribute a common stock dividend.

Req. 2

Stockholders’ equity:

Common stock, $0.75 par, 2,700,000 shares authorized,

780,000 issued and outstanding ($487,500 + $97,500)

$ 585,000

Paid-in capital in excess of par − common

($1,512,000 + $2,112,500) …………………………………..

3,624,500

Retained earnings ($7,123,000 − $2,210,000) …………..

4,913,000

Accumulated other comprehensive income (loss) …..

(195,000)

Total stockholders’ equity …………………………………

$8,927,500

Req. 3

The stock dividend did not change total stockholders’ equity because

Req. 4

(15-20 min.) E 10-40B

a. Decrease stockholders’ equity by $58 million.

(10-15 min.) E 10-41B

Req. 1

Common:

Total stockholders’ equity ……………………………………….

$ 82,500

Less: Preferred equity — redemption value ………………

(30,000)

Total common equity……………………………………………….

$ 52,500

Book value per share ($52,500 / 5,000 shares) …………..

$10.50

Req. 2

Common:

Total stockholders’ equity ……………………………………….

$ 82,500

Less: Preferred equity [$30,000 + ($22,500 × .06 × 3)] ..

(34,050)

Total common equity ………………………………………………

$ 48,450

Book value per share ($48,450 / 5,000 shares)…………..

$9.69

Req. 3

Bleu Door’s stock is not necessarily a good buy. Investment decisions

should be based on more than one ratio.

(10-15 min.) E 10–42B

Req. 1

Net

profit

=

Net income

=

$2,200

=

3.4%

margin

Net sales

$65,000

ratio

Asset

=

Net sales

=

$65,000

=

$65,000

=

1.21

turnover

Average total

($52,070* + $55,780**)/2

$53,925

assets

Leverage

=

Avg. total assets

=

$53,925

=

2.88

ratio

Avg. common

stkholders’

equity

($14,037 + $23,471) /2

Net profit

x

Asset

=

margin ratio

turnover

ROA

3.4%

x

1.21

=

4.1%

ROA

x

Leverage

=

ROE

ratio

4.1%

x

2.88

=

11.8%

_____

(continued) E 10-42B

Req. 2

These rates of return suggest relative weakness. The company is