Chapter 8 Long-Term Investments & International Operations

8-41

(20-30 min.) P 8-54B

Req. 1

Current fair value is used to account for the available-for-sale

investment in Sydney, Inc., because the investor expects to sell the

(continued) P 8-54B

Req. 2

Balance sheet:

ASSETS

Total current assets ……………………………………………………

$ XXX

Long-term assets:

Equity-method investment ………………………………………..

552,370*

Investment in AFSS ………………………………………………….

31,600

Property, plant, and equipment, net …………………………….

XXX

STOCKHOLDERS’ EQUITY

Common stock …………………………………………………………..

$ XXX

Retained earnings ………………………………………………………

XXX

Accumulated other comprehensive income:

Unrealized (loss) on investment in AFSS

[(1,100 × $41.75) − $31,600] ………………………………………

(14,325)

Income statement and Statement of other comprehensive income:

Income from operations ……………………………………………..

$ XXX

Other revenue:

Equity-method investment revenue ($465,000 × .45)….

209,250

Dividend revenue (1,100 × $.36) ………………………………..

396

Net income ………………………………………………………………..

XXX

Other comprehensive income:

Unrealized (loss) on investment in AFSS …………………..

(14,325)

_____

*Equity-Method Investment

Purchase

370,000

Net income

Dividends received

($465,000 × .45)

209,250

(21,000 × $1.28)

26,880

Balance

552,370

Chapter 8 Long-Term Investments & International Operations

8-43

(45-60 min.) P 8-55B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Mar.

16

Investment in AFSS (2,900 × $12.50) ……………

36,250

Cash ……………………………………………………..

36,250

Purchased investment.

May

21

Cash (2,900 × $1.20) …………………………………..

3,480

Dividend Revenue ………………………………….

3,480

Received cash dividend.

Aug.

17

Cash …………………………………………………………

63,000

Equity-Method Investment ………………………

63,000

Received cash dividend on equity-method

investment.

Dec.

31

Equity-Method Investment

($603,000 × .30) ………………………………………….

180,900

Equity-Method Investment Revenue ………..

180,900

To record investment revenue.

31

Allowance to Adjust Investment in AFSS

to Market ($39,400 − $36,250) …………………….. 3,150

Unrealized Gain on Investment in AFSS …..

3,150

Adjusted investment to market value.

(continued) P 8-55B

Req. 2

Equity-Method Investment

Jan.

1

Balance

585,000

Aug.

17

Dividends

63,000

Dec.

31

Net income

180,900

Dec.

31

Balance

702,900

Req. 3

Total current assets …………………………………………………….

$ XXX

Long-term assets:

Investment in AFSS ……………………………………………………

39,400

Equity-method investment ………………………………………….

702,900

(20-30 min.) P 8-56B

Req. 1

Req. 2

Race

RMCC

Eliminations

Consolidated

Totals

Debit

Credit

(a) $1.3

Total assets ……………….

$78.1

$163.3

(b) 8.0

$232.1

Total liabilities ……………

$63.8

$155.3

(a) $1.3

$217.8

Total stockholders’

equity ……………………..

14.3

8.0

(b) 8.0

14.3

Total liabilities and

equity ……………………..

$78.1

$163.3

$9.3

$9.3

$232.1

Req. 3

(35-45 min.) P 8-57B

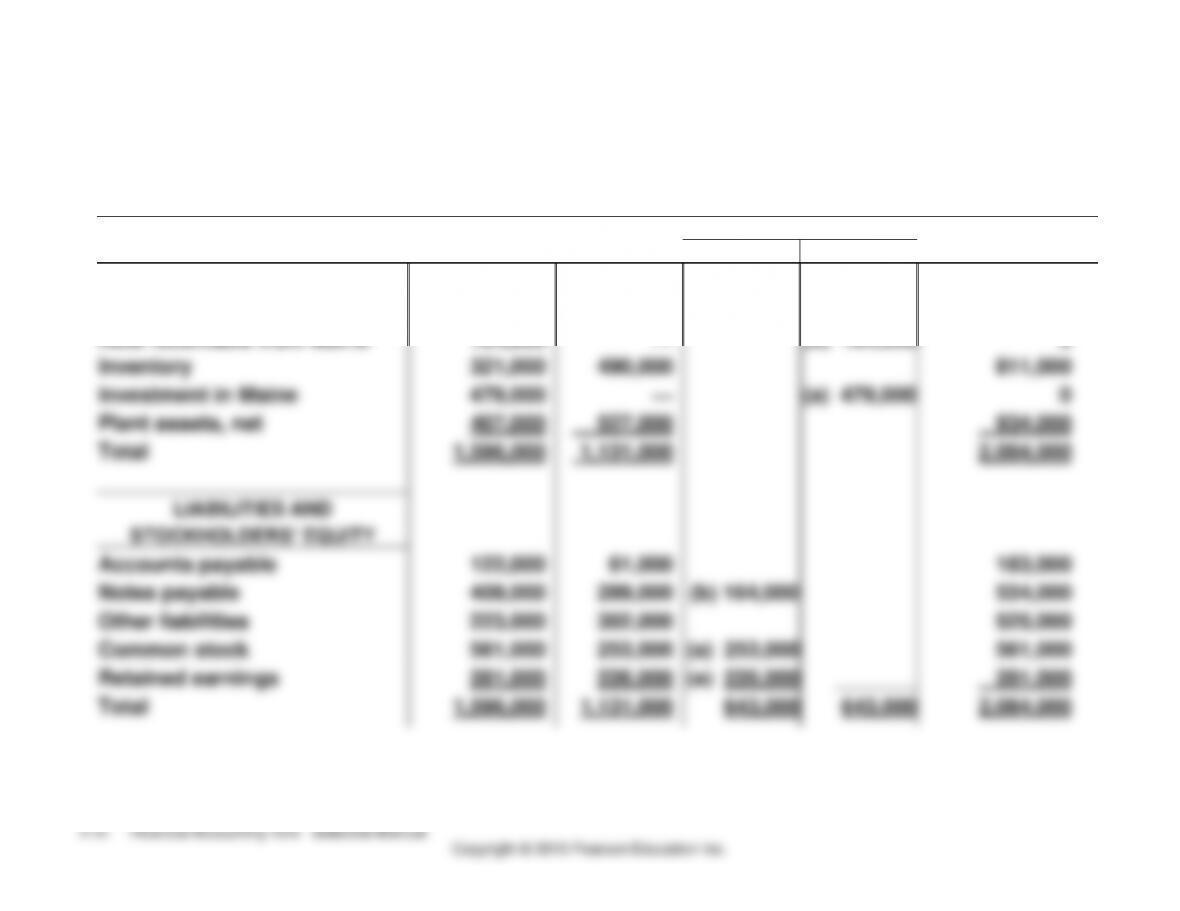

Abbey, Inc.

Consolidation Work Sheet

September 30, 2014

ELIMINATION

CONSOLIDATED

ASSETS

ABBEY

MAINE

DEBIT

CREDIT

AMOUNTS

Cash

56,000

28,000

84,000

Accounts receivable, net

169,000

86,000

255,000

Note receivable from Maine

164,000

—

(b) 164,000

0

Inventory

321,000

490,000

811,000

Investment in Maine

479,000

—

(a) 479,000

0

Plant assets, net

407,000

527,000

934,000

Total

1,596,000

1,131,000

2,084,000

LIABILITIES AND

STOCKHOLDERS’ EQUITY

Accounts payable

122,000

61,000

183,000

Notes payable

409,000

289,000

(b) 164,000

534,000

Other liabilities

223,000

302,000

525,000

Common stock

561,000

253,000

(a) 253,000

561,000

Retained earnings

281,000

226,000

(a) 226,000

_______

281,000

Total

1,596,000

1,131,000

643,000

643,000

2,084,000

Chapter 8 Long-Term Investments and International Operations

47

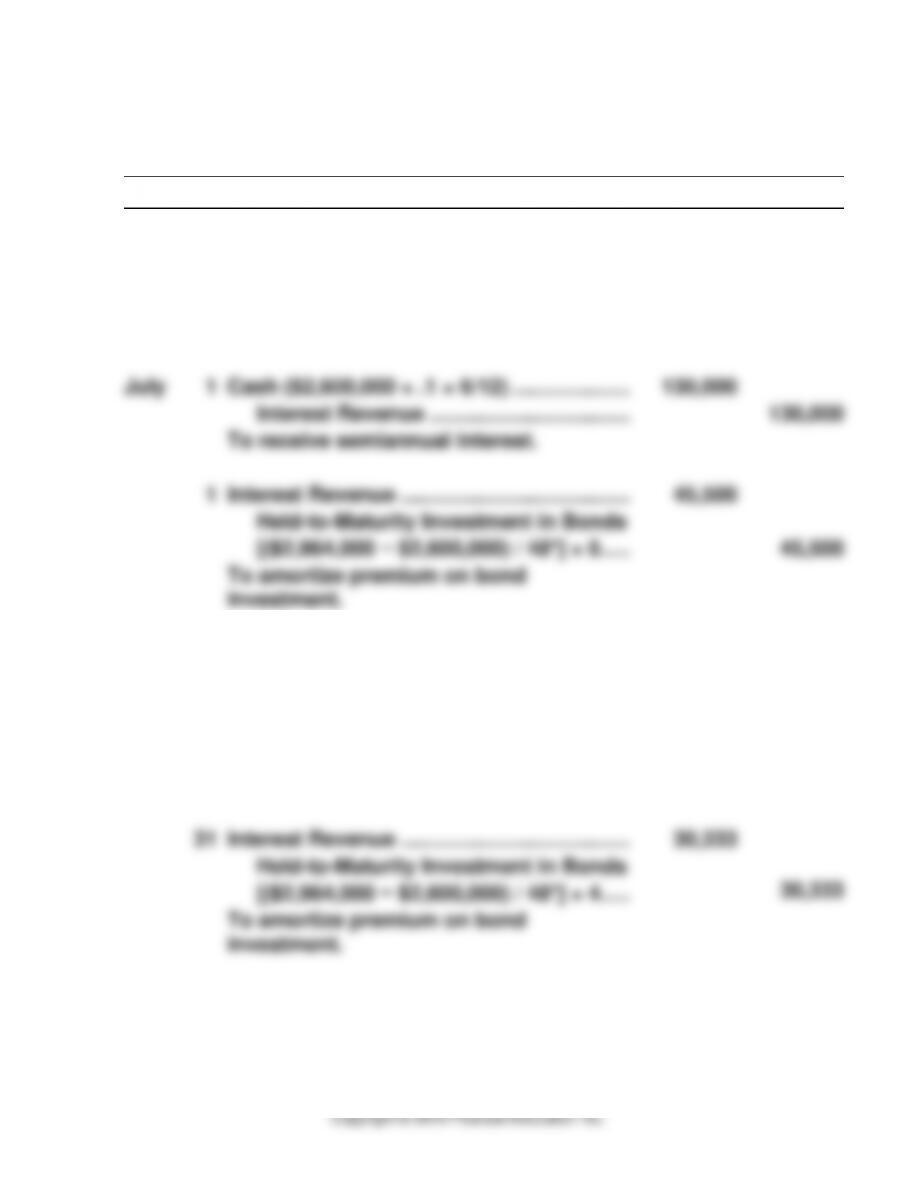

(45-60 min.) P 8-58B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Jan.

1

Held-to–Maturity Investment in Bonds

($2,600,000 × 1.14) ……………………………….

2,964,000

Cash ………………………………………………

2,964,000

To purchase bond investment.

July

1

Cash ($2,600,000 × .1 × 6/12) ………………..

130,000

Interest Revenue …………………………….

130,000

To receive semiannual interest.

1

Interest Revenue …………………………………

45,500

Held-to-Maturity Investment in Bonds

[($2,964,000 − $2,600,000) / 48*] × 6 …..

45,500

To amortize premium on bond

investment.

Req. 2

Oct.

31

Interest Receivable

($2,600,000 × .1 × 4/12) …………………………

86,667

Interest Revenue …………………………….

86,667

To accrue interest revenue.

31

Interest Revenue …………………………………

30,333

Held-to-Maturity Investment in Bonds

[($2,964,000 − $2,600,000) / 48*] × 4 …..

30,333

To amortize premium on bond

investment.

_____

*Amortization period: 48 months, from January 1, 2014 to January 1, 2018.

(continued) P 8-58B

Req. 3

Balance sheet at October 31, 2014:

Current assets:

Interest receivable ……………………………………………

$ 86,667

Long-term assets:

Held-to-maturity investment in bonds

($2,964,000 − $45,500 − $30,333) ………………………..

2,888,167

Property, plant, and equipment, net ……………………..

XXX,XXX

Income statement for the year ended October 31, 2014:

Other revenues:

Interest revenue ($130,000 − $45,500 + $86,667 − $30,333)…

$140,834

Chapter 8 Long-Term Investments and International Operations

49

(15-20 min.) P 8-59B

Req. 1

Investment Opportunity X

Year

Cash

Flow

x

Factor

=

PV of

Cash Flow

1

$17,000

x

.909

=

$15,453

2

10,000

x

.826

=

8,260

3

6,000

x

.751

=

4,506

$33,000

$28,219

Investment Opportunity Y

(20-25 min.) P 8-60B

Req. 1

This situation will generate a positive translation adjustment, which is like a

gain. The gain occurs because the yen’s current exchange rate, which is

used to translate the subsidiary’s net assets, is greater than the historical

exchange rates at which Deepa Corp. invested in the Japanese subsidiary.

YEN

EXCHANGE

RATE

DOLLARS

Assets

390,000,000

$0.0103

$4,017,000

Liabilities

145,000,000

0.0103

$1,493,500

Stockholders’ equity:

Common stock

21,000,000

0.0088

184,800

Retained earnings

224,000,000

0.0092

2,060,800

Accumulated other

comprehensive income:

Foreign-currency

translation adjustment

277,900

390,000,000

$4,017,000

The foreign currency translation adjustment is reported in accumulated other

comprehensive income in stockholders’ equity on the balance sheet and other

comprehensive income on the statement of comprehensive income or the

statement of other comprehensive income.

Req. 2

The translation adjustment “belongs” to Deepa, the parent company.

Challenge Exercises and Problem

(15-20 min.) E 8-61

Req. 1

(20 min.) E 8-62

Req. 1

Two components of accumulated other comprehensive income are:

Req. 2

An unrealized gain (loss) on available-for-sale investments produces a

positive (negative) balance.

Req. 3

Millions

Accumulated other comprehensive (loss) at

December 31, 2014 ………………………………………………………….

$(57)

Foreign-currency translation adjustment ………………………………

25

Unrealized loss on investments in AFSS ………………………………

(15)

Accumulated other comprehensive (loss) at

December 31, 2015 ………………………………………………………...

$(47)