(20-30 min.) E 13-62

ORDER OF

COMPUTATION

Millions

5

Sales ($1,700 ÷ 0.25) …………………………………………

$6,800

6

Operating expenses ($6,800 − $1,700) ……………….

5,100

4

Operating income …………………………………………….

1,700

Given

Interest expense ………………………………………………

800

2

Pretax income [$540 ÷ (1 − 0.40)] ……………………….

900

3

Income tax expense ($900 × 0.40) ………………………

360

1

Net income ($5,400 × .10) ………………………………….

$ 540

(30-40 min.) P 13–63

Amherst Corporation

Comparative Income Statements

Years Ended December 31, 2014 and 2013

2014 2013

Sales revenue ………………………………… $2,100,000

$2,000,000

Cost of goods sold (a) …………………….. 1,365,000

1,400,000

Gross profit (b) ………………………………. 735,000

600,000

Operating expense (d) …………………….. 465,000

400,000

Operating income (c)………………………. 270,000

200,000

Interest expense …………………………….. 40,000

40,000

Income before income tax (e) ………….. 230,000

160,000

Income tax expense (30%) (f) ………….. 69,000

48,000

Net income (g) ……………………………….. $ 161,000

$ 112,000

(continued) P 13-63

Amherst Corporation

Comparative Balance Sheets

December 31, 2014 and 2013

2014 2013

ASSETS

Current:

Cash (l) ……………………………………………. $ 35,000

$ 30,000

Accounts receivable, net (k) ……………… 165,000

135,000

Inventory (j) ……………………………………… 240,000

180,000

Total current assets (h) ………………… 440,000

345,000

Plant and equipment, net …………………….. 760,000

555,000

Total assets ………………………………………… $1,200,000

$900,000

LIABILITIES

Current liabilities ………………………………… $ 160,000

$140,000

10% Bonds payable (r) ………………………… 400,000

400,000

Total liabilities (q) ……………………………….. 560,000

540,000

STOCKHOLDERS’ EQUITY

Common stock, $5 par (o)…………………. 360,000

220,000

Retained earnings (p) ……………………….. 280,000

Total stockholders’ equity (n) ………………. 640,000

140,000

360,000

Total liabilities and stockholders’ equity (m) $1,200,000

$900,000

Computations (alternate order of calculations is possible)

(a) Cost of goods sold ($1,365,000) = Sales x COGS % ($2,100,000 × 65%)

(b) Gross profit ($735,000) = Sales – COGS ($2,100,000 – $1,365,000)

(c) Operating income ($270,000) = Operating income in 2014 × 2013 Trend %

($200,000 × 135%)

(d) Operating expenses ($465,000) = Gross profit – Operating Income ($735,000 –

$270,000)

(continued) P 13–63

(e) Income before income tax ($230,000) = Operating income – Interest expense

($270,000 – $40,000)

(f) Income tax expense ($69,000) = Income before income tax × tax rate ($230,000 ×

30%)

(g) Net income ($161,000) = Income before income tax – Income tax expense

($230,000 – $69,000)

Decision Cases

(30 min.) Decision Case 1

Req. 1

Trans-

action

Current

Ratio

Debt

Ratio

Times-

Interest-

Earned

Ratio

Return

on

Equity

Book

Value

Per Share

1

Increase

Decrease

No effect

Increase

Increase

2

Increase

Increase

No effect

No effect

No effect

3

Decrease

Increase

No effect

Increase

Indeterminate

4

No effect

Increase

Decrease

Decrease

Decrease

5

Increase

Decrease

Increase

Increase

Increase

6

Decrease

Increase

No effect

No effect

No effect

Req. 2

Transaction

Overall Effect on the Company

1

Positive (due to gain)

2

Unclear

3

Unclear*

4

Negative (due to loss)

5

Positive (due to gross profit)

6

Unclear

____

*May be negative because of decreasing assets to shrink the

company.

(20-30 min.) Decision Case 2

Ratio

CNH

Caterpillar

1.

Current ratio

Higher

Lower

2.

Quick (acid-test) ratio

No effect

No effect

3.

Inventory turnover

Lower

Higher

4.

Receivable turnover

No effect

No effect

and

Days’ sales outstanding

5.

Debt ratio

Lower

Higher

6.

Times-interest-earned

Higher

Lower

7.

Return on sales, total assets,

Higher

Lower

and equity,

and earnings per share

8.

Price/earnings ratio

Lower*

Higher*

_____

*Assuming stock price is unaffected by the accounting

difference. If stock price is affected, the price/earnings

ratio could be higher (lower) for either company.

9.

Dividend yield

No effect

No effect

10.

Book value per share

Higher

Lower

11.

Accounts payable turnover

Lower

Higher

12.

Gross profit percentage

Higher

Lower

13.

Operating profit percentage

Higher

Lower

14.

Asset turnover

Lower

Higher

(continued) Decision Case 2

CONCLUSION:

Overall, CNH will look better than Caterpillar because of:

(20-30 min.) Decision Case 3

To reduce losses and establish profitable operations, Outward Bound

should take the following steps:

1. Make a dedicated effort to collect receivables and consider extending

less credit to customers. Receivables make up 15.2% of assets,

compared to 11.0% for the industry average. The company’s inability

to collect its receivables may explain the shortage of cash (3.0% of

total assets compared to 6.8% for the industry).

2. Reduce the amount of the company’s interest-bearing debt. The

company’s short-term notes payable equal 17.1% of total assets,

Ethical Issue

Req. 1

The ethical issue is: Should Turnberry reclassify its investments from

long-term to short-term?

Req. 2 and Req. 3

(continued) Ethical Issue

Ethical analysis: Reclassifying a long-term investment as current to

Req. 4.

Reclassifying the investments from current back to long-term may

suggest to some observers that managers are playing a shell game.

However, the case states that sales subsequent to the first

Focus on Financials: Amazon.com, Inc.

(1-2 hours)

Req. 1

1. Ability to pay current liabilities

Ratio

Computation

2012

2011

Interpretation

Current

CA*

$21,296

$17,490

CL

$19,002

$14,896

declined

= 1.12

= 1.17

slightly; less

liquid

Acid-test

QA**

($8,084 + $3,364

+ $3,364)

($5,269 + $4,307

+ $2,571)

(Quick)

CL

$19,002

$14,896

declined

= 0.78

= 0.82

slightly; less

liquid

CA = Current Assets

QA = Quick Assets (Cash and equivalents + Marketable securities + Receivables)

2. Ability to sell inventory and collect receivables

Ratio

Computation

2012

2011

Interpretation

Inventory

COGS

$45,971

$37,288

turnover

Avg.

5,512

4,097

declined

inventory*

= 8.34

= 9.10

slightly

Days sales

in

Avg.

receivables**

2,968

2,079

receivables

One days’

sales

($61,093 /

365)

($48,077 /

365)

unfavorable;

= 17.73 days

= 15.78 days

lengthened

*Avg. inventory: 2012: ($6,031 + 4,992) / 2

2011: ($4,992 + 3,202) / 2

**Avg. receivables 2012: ($3,364 + 2,571) / 2

2011: ($2,571 + 1,587) / 2

(continued) Amazon.com

3. Ability to pay long-term debt

Ratio

Computation

2012

2011

Interpretation

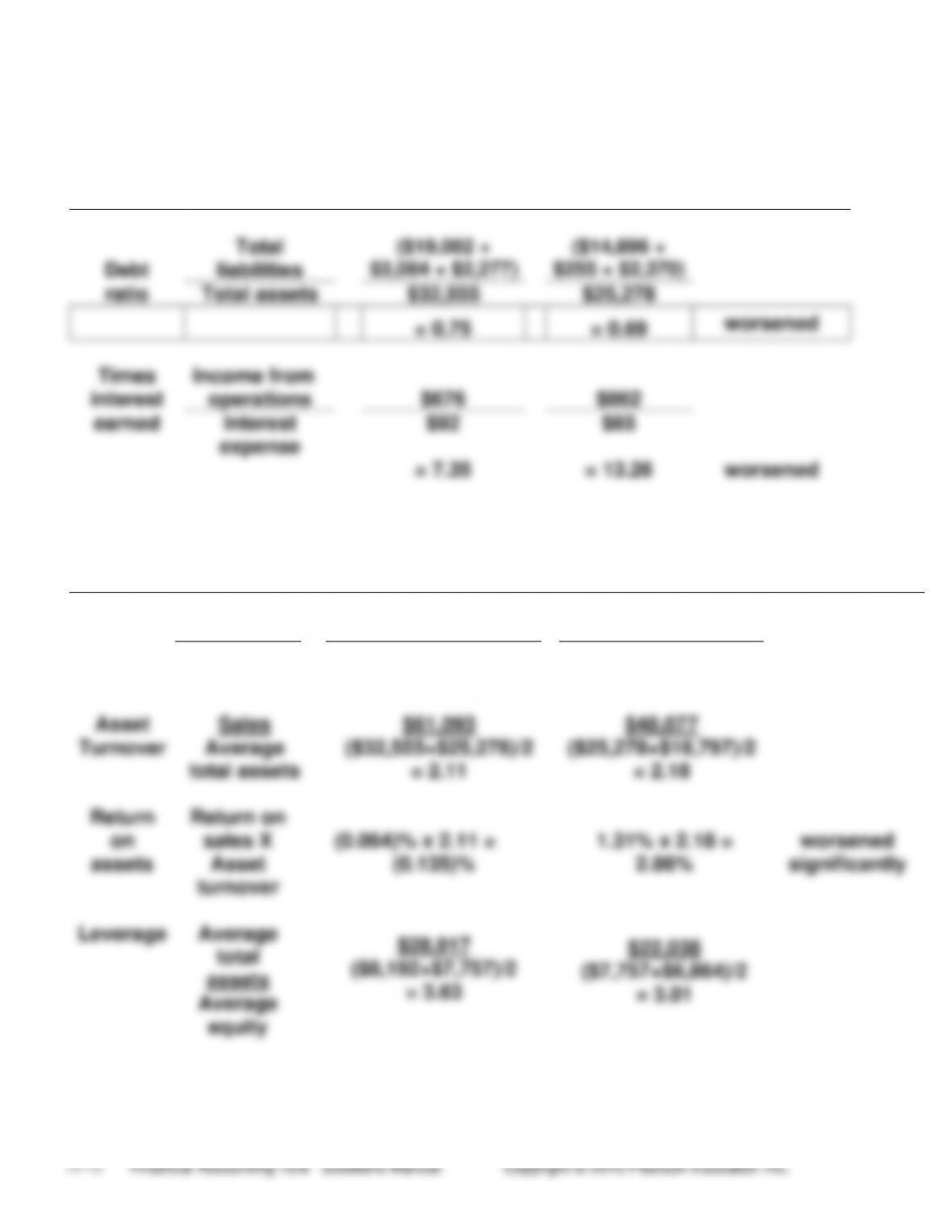

Debt

Total

liabilities

($19,002 +

$3,084 + $2,277)

($14,896 +

$255 + $2,370)

ratio

Total assets

$32,555

$25,278

= 0.75

= 0.69

worsened

Times

Income from

interest

operations

$676

$862

earned

Interest

expense

$92

$65

= 7.35

= 13.26

worsened

4. Profitability

Ratio

Computation

2012

2011

Interpretation

Return

Net income

($39)

$631

On

Net sales

$61,093

$48,077

worsened

Sales

= (0.064) %

= 1.31 %

significantly

Asset

Turnover

Sales

Average

total assets

$61,093

($32,555+$25,278)/2

= 2.11

$48,077

($25,278+$18,797)/2

= 2.18

Return

on

assets

Return on

sales X

Asset

turnover

(0.064)% x 2.11 =

(0.135)%

1.31% x 2.18 =

2.86%

worsened

significantly

Leverage

Average

total

assets

Average

equity

$28,917

($8,192+$7,757)/2

= 3.63

$22,038

($7,757+$6,864)/2

= 3.01

(continued) Amazon.com

Ratio

Computation

2012

2011

Interpretation

Earnings

Net income –

per

Pfd. Div.

($39) – $0

$631 – $0

share

Avg. common

453

453

shares

outstanding

= ($0.09)

= $1.39

slightly

improved

5. Net cash flow from operations: