(20-30 min.) P 9-72A

Alternative

Alternative

1

2

Borrow $6.75

Issue 100,000

mil at 6%

shares of stock

Net income 2 years from

now

$2,880,000

$2,880,000

Less interest expense

405,000

-0-

Projected net income

before tax

2,475,000

2,880,000

Less income tax expense

(35%)

866,250

1,008,000

Projected net income 2

years from now

$1,608,750

$1,872,000

Earnings per share:

$1,608,750/100,000

$16.09

$1,872,000/(100,000 +

100,000)

$9.36

Req. 2

TO: Management of Hillside Medical Goods

FROM: Student Name

SUBJECT: Advantages and disadvantages of borrowing

versus issuing stock to raise cash for expansion

Raising money by borrowing has at least two advantages over issuing

common stock. Borrowing does not change the present ownership of the

(continued) P 9-72A

earnings per share of common stock, because the interest expense on the

debt is tax-deductible. And higher earnings per share usually lead to higher

stock prices for company owners.

(20-30 min.) P 9-73A

Req. 1

Arroya Foods, Inc.

Partial Balance Sheet

Dec. 31, 2014

Property, plant, and

equipment:

Current liabilities:*

Equipment ……………..

$784,000

Mortgage note

Accumulated

payable, current ………….

$ 86,000

depreciation ………..

(167,000)

Bonds payable,

617,000

current portion…………….

515,000

Interest payable ……………..

43,000

Total current liabilities ………

644,000

Long-term liabilities:

Mortgage note

payable ……………………….

$ 386,000

Bonds payable…. $200,000

Discount on

bonds payable... (25,000)*

175,000

Pension liability ……………..

41,000**

Total long-term liabilities …..

602,000

Notes:

* The order of listing current liabilities and long-term liabilities is optional. However,

Discount on Bonds Payable should come immediately after Bonds Payable. Also, it

is customary to report Interest Payable after the related liability accounts, Mortgage

Note Payable and Bonds Payable, Current Portion.

(continued) P 9-73A

Req. 2

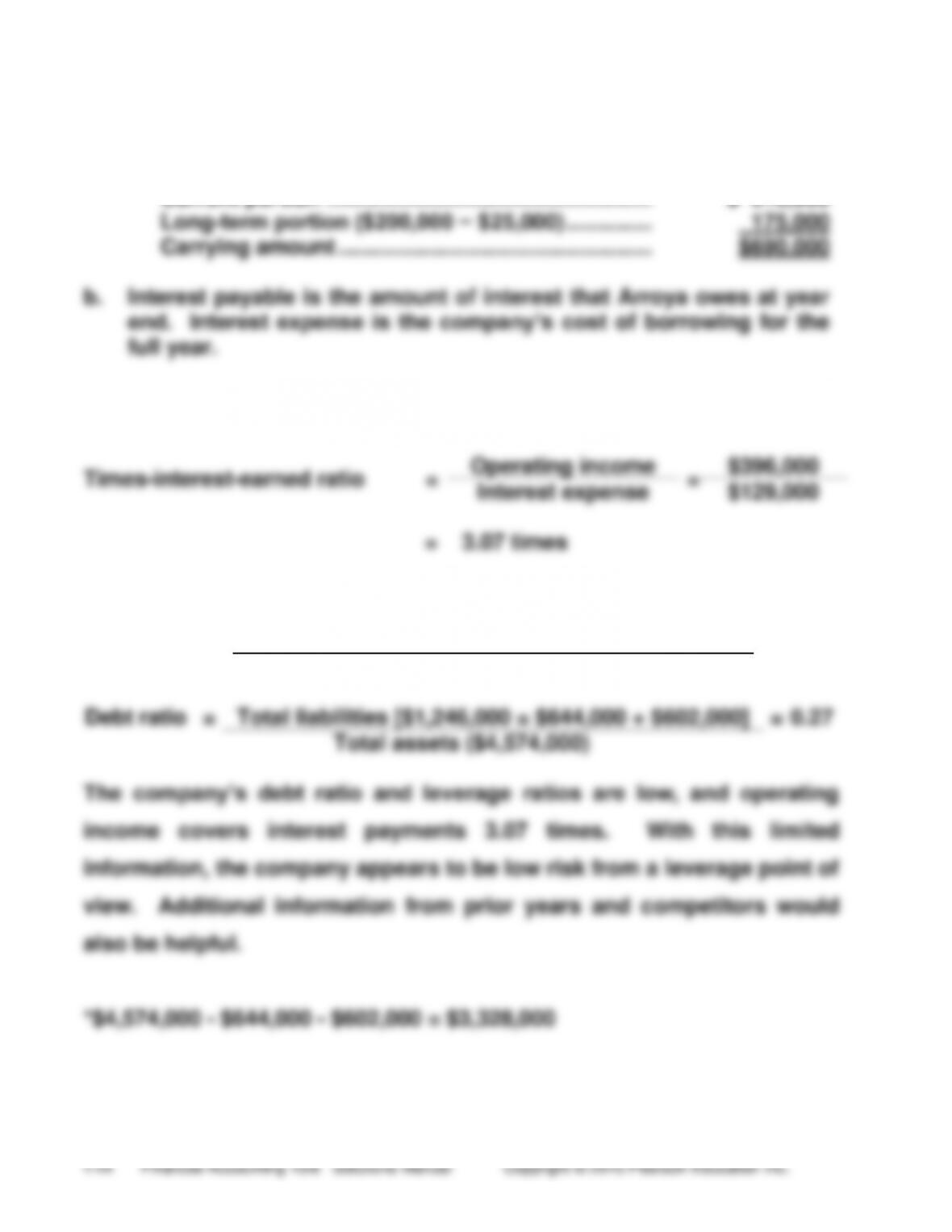

a.

Carrying amount of bonds payable:

Current portion ……………………………………………..

$ 515,000

Long-term portion ($200,000 − $25,000) …………..

175,000

Carrying amount ……………………………………………

$690,000

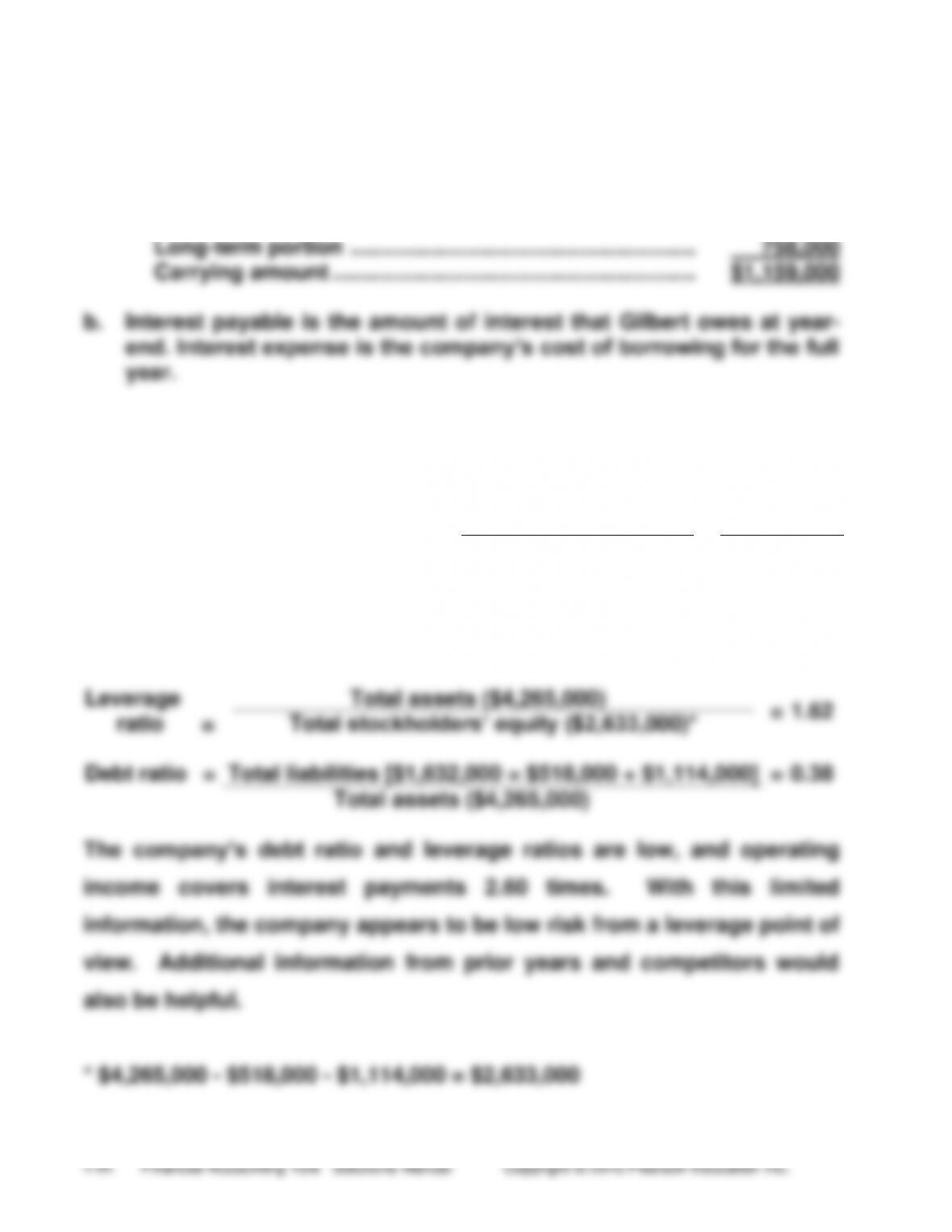

b.

Interest payable is the amount of interest that Arroya owes at year

end. Interest expense is the company’s cost of borrowing for the

full year.

Req. 3

(continued) P 9-73A

Req. 5

Leverage

ratio

=

Total assets ($7,574,000)

Total stockholders’ equity ($3,328,000)

=

2.28

Debt ratio

=

Total liabilities ($4,246,000)

=

0.56

Total assets ($7,574,000)

The leverage ratio and debt ratio would increase. The company would

still be considered healthy (average risk) from a leverage point of view.

(15-20 min.) P 9-74B

a. Sales tax payable ($145,000 × .07) ………………………………..

$10,150

b. Note payable, short-term ……………………………………………..

$76,000

Interest payable ($76,000 × .06 × 4/12) …………………………..

1,520

c. Unearned service revenue ($3,600 × 2/6) ………………………

$1,200

d. Estimated warranty payable

($9,700 + $34,000 − $31,100) …………………………..……….

$12,600

e. Portion of long-term note payable due

within one year …………………………..…………………………..

$30,000

Interest payable ($90,000 × .04)…………………………………….

3,600

(30-40 min.) P 9-75B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Mar.

3

Inventory ……………………………………………..

72,000

Note Payable, Short-term ………………….

72,000

May

31

Cash ……………………………………………………

85,000

Note Payable, Short-term ………………….

17,000

Note Payable, Long-term ………………….

68,000

Sept.

3

Note Payable, Short-term ………………………

72,000

Interest Expense ($72,000 × .04 × 6/12) …..

1,440

Cash ……………………………………………….

73,440

Dec.

31

Warranty Expense ($214,000 × .02) ………..

4,280

Estimated Warranty Payable ……………..

4,280

Dec.

31

Interest Expense ($85,000 × .05 × 7/12) …..

2,479

Interest Payable ……………………………….

2,479

2015

May

31

Note Payable, Short-term ………………………

17,000

Interest Payable ……………………………………

2,479

Interest Expense ($85,000 × 0.05 × 5/12) …

1,771

Cash ………………………………………………..

21,250

(20-25 min.) P 9-76B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

a.

May

31

Cash ………………………………………….

3,500,000

Bonds Payable……………………….

3,500,000

To issue bonds at par.

b.

Nov.

30

Interest Expense ………………………..

105,000

Cash ($3,500,000 × .06 × 6/12) …

105,000

To pay interest on bonds.

c.

Dec.

31

Interest Expense

($3,500,000 × .06 × 1/12) ………………

17,500

Interest Payable ……………………..

17,500

To accrue interest.

2015

d.

May

31

Interest Payable ………………………….

17,500

Interest Expense

($3,500,000 × .06 × 5/12) ………………

87,500

Cash ……………………………………..

105,000

To pay interest on bonds.

Req. 2 (reporting the liabilities on the balance sheet at

Dec. 31, 2014)

Current liabilities:

Interest payable ………………………………………..

$ 17,500

Long-term liabilities:

Bonds payable ………………………………………….

$3,500,000

(30-40 min.) P 9-77B

Req. 1

The 4% bonds issued when the market interest rate is 3% will be priced

Req. 2

(continued) P 9-77B

Req. 3

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

a.

Feb.

28

Cash ($1,200,000 × 0.94) …………………………...

1,128,000

Discount on Bonds Payable ……………………..

72,000

Bonds Payable …………………………………….

1,200,000

To issue bonds payable at a discount.

b.

Aug.

31

Interest Expense ………………………………………

31,200

Discount on Bonds Payable ($72,000 / 10)

7,200

Cash ($1,200,000 × .04 × 6/12) ………………

24,000

To pay interest and amortize bond

discount.

c.

Dec.

31

Interest Expense ………………………………………

20,800

Discount on Bonds Payable ($7,200 × 4/6)

4,800

Interest Payable ($24,000 4/6) …………….

16,000

To accrue interest and amortize bond discount.

2015

d.

Feb.

28

Interest Payable (from Dec. 31) …………………

16,000

Interest Expense ………………………………………

10,400

Discount on Bonds Payable ($7,200 × 2/6)

2,400

Cash ($1,200,000 × .04 × 6/12) ………………

24,000

To pay interest and amortize bond discount.

Req. 4 (reporting the liabilities on the balance sheet at

Dec. 31, 2014)

Current liabilities:

Interest payable ……………………………………….

$ 16,000

Long-term liabilities:

Bonds payable …………………………………………

$1,200,000

Less: Discount on bonds payable

($72,000 − $7,200 − $4,800) ……………………

(60,000)

1,140,000

(30-40 min.) P 9-78B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Jan.

1

Cash ($4,000,000 × .94) ………………………….

3,760,000

Discount on Bonds Payable ………………….

240,000

Bonds Payable …………………………………

4,000,000

To issue bonds at a discount.

July

1

Interest Expense …………………………………..

112,000

Cash ($4,000,000 × .05 × 6/12) ……………

100,000

Discount on Bonds Payable

($240,000 / 20) …………………………………..

12,000

To pay interest and amortize bond

discount.

Dec.

31

Interest Expense …………………………………..

112,000

Interest Payable ($4,000,000 × .05 × 6/12) ..

100,000

Discount on Bonds Payable

($240,000 / 20) ………………………………

12,000

To accrue interest and amortize bond

discount.

2015

Jan.

1

Interest Payable ……………………………………

100,000

Cash ………………………………………………..

100,000

To pay interest.

2024

Jan.

1

Bonds Payable ……………………………………..

4,000,000

Cash ………………………………………………..

4,000,000

To pay off bonds at maturity.

(continued) P 9-78B

Req. 2

Carrying amount at Dec. 31, 2014:

Req. 3

(30-45 min.) P 9-79B

Req. 1

a. Using the PV function in EXCEL, the issue price of the bonds is

$3,939,189.

Req. 2 (amortization table)

A

B

C

D

E

Semiannual

Interest Date

Interest

Payment

(5% of

Maturity

Value)

Interest

Expense

(6% of

Preceding

Bond

Carrying

Amount)

Discount

Amortization

(B – A)

Discount

Account

Balance

(Preceding

D – C)

Bond

Carrying

Amount

($4,200,000

– D)

Jan. 1, Yr. 1

260,811

3,939,189

Dec. 31, Yr. 1

210,000

236,351

26,351

234,460

3,965,540

Dec. 31, Yr. 2

210,000

237,932

27,932

206,527

3,993,473

Dec. 31, Yr. 3

210,000

239,608

29,608

176,919

4,023,081

Dec. 31, Yr. 4

210,000

241,385

31,385

145,534

4,054,466

Dec. 31, Yr. 5

210,000

243,268

33,268

112,266

4,087,734

Dec. 31, Yr. 6

210,000

245,264

35,264

77,002

4,122,998

Dec. 31, Yr. 7

210,000

247,380

37,380

39,622

4,160,378

Dec. 31, Yr. 8

210,000

249,623

39,622

4,200,000

(continued) P 9-79B

Req. 3 (reporting the liabilities at Dec. 31, Year 4)

Current liabilities:

Current portion of notes payable …………….

$ 40,000

Long-term liabilities:

Bonds payable ………………………………………

$4,200,000

Less: Discount on bonds payable………..

(145,534)

4,054,466

Notes payable($200,000 – $40,000) ………….

160,000

(40-50 min.) P 9-80B

Req. 1 Using the PV function in EXCEL, the issue price of the bonds is

$4,610,271.

Req. 2 (amortization table)

A

B

C

D

E

Semiannual

Interest Date

Interest

Payment

(2% of

Maturity

Value)

Interest

Expense

(2.5% of

Preceding

Bond

Carrying

Amount)

Discount

Amortization

(B – A)

Discount

Account

Balance

(Preceding

D – C)

Bond

Carrying

Amount

($5,000,000

– D)

Dec. 31, 2014

389,729

4,610,271

June 30, 2015

100,000

115,257

15,257

374,472

4,625,528

Dec. 31, 2015

100,000

115,638

15,638

358,834

4,641,166

June 30, 2016

100,000

116,029

16,029

342,805

4,657,195

Dec. 31, 2016

100,000

116,430

16,430

326,375

4,673,625

June 30, 2017

100,000

116,841

16,841

309,534

4,690,466

Dec. 31, 2017

100,000

117,262

17,262

292,273

4,707,727

June 30, 2018

100,000

117,693

17,693

274,580

4,725,420

Dec. 31, 2018

100,000

118,136

18,136

256,444

4,743,556

June 30, 2019

100,000

118,589

18,589

237,855

4,762,145

Dec. 31, 2019

100,000

119,054

19,054

218,802

4,781,198

June 30, 2020

100,000

119,530

19,530

199,272

4,800,728

Dec. 31, 2020

100,000

120,018

20,018

179,253

4,820,747

June 30, 2021

100,000

120,519

20,519

158,735

4,841,265

Dec. 31, 2021

100,000

121,032

21,032

137,703

4,862,297

June 30, 2022

100,000

121,557

21,557

116,146

4,883,854

Dec. 31, 2022

100,000

122,096

22,096

94,049

4,905,951

June 30, 2023

100,000

122,649

22,649

71,401

4,928,599

Dec. 31, 2023

100,000

123,215

23,215

48,186

4,951,814

June 30, 2024

100,000

123,795

23,795

24,390

4,975,610

Dec. 31, 2024

100,000

124,390

24,390

(0)

5,000,000

(continued) P 9-80B

Req. 3

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

a.

Dec.

31

Cash …………………………..……………………..

4,610,271

Discount on Bonds Payable ……………….

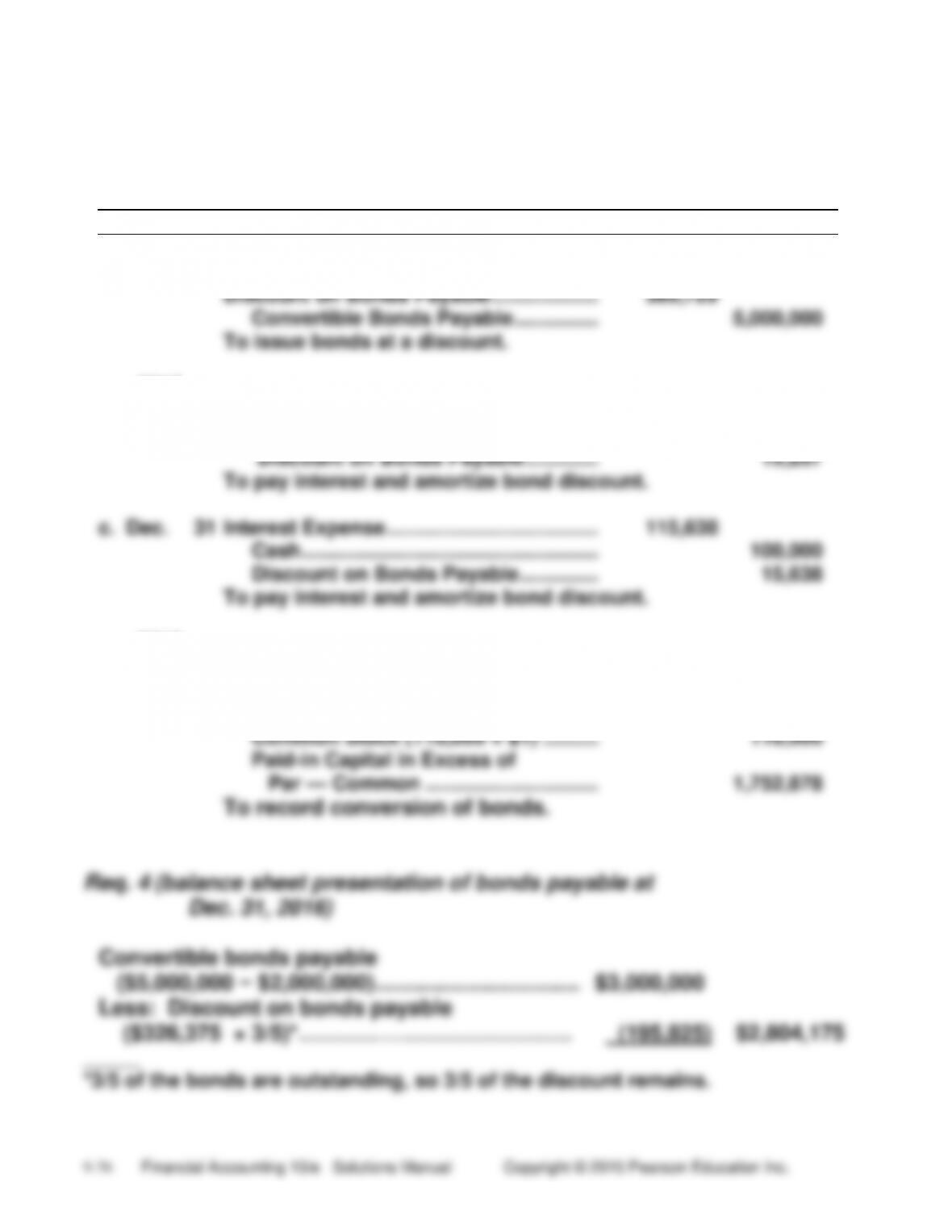

389,729

Convertible Bonds Payable ……………

5,000,000

To issue bonds at a discount.

2015

b.

June

30

Interest Expense ………………………………..

115,257

Cash …………………………………………….

100,000

Discount on Bonds Payable ………….

15,257

To pay interest and amortize bond discount.

c.

Dec.

31

Interest Expense ………………………………..

115,638

Cash ……………………………………………..

100,000

Discount on Bonds Payable …………..

15,638

To pay interest and amortize bond discount.

2016

d.

July

1

Convertible Bonds Payable ………………..

2,000,000

Discount on Bonds Payable

($342,805 × 2/5) …………………………..

137,122

Common Stock (110,000 × $1) ……….

110,000

Paid-in Capital in Excess of

Par — Common ………………………….

1,752,878

To record conversion of bonds.

Req. 4 (balance sheet presentation of bonds payable at

Dec. 31, 2016)

Convertible bonds payable

($5,000,000 − $2,000,000) ………………………………

$3,000,000

Less: Discount on bonds payable

($326,375 × 3/5)*…………………………….….

(195,825)

$2,804,175

_____

*3/5 of the bonds are outstanding, so 3/5 of the discount remains.

(15-30 min.) P 9-81B

Req. 1

Alternative

Alternative

1

2

Borrow $7.75

Issue 100,000

mil at 5%

shares of stock

Net income 2 years from

now

$3,630,000

$3,630,000

Less interest expense

387,500

-0-

Projected net income

before tax

3,242,500

3,630,000

Less income tax expense

(35%)

1,134,875

1,270,500

Projected net income 2

years from now

$2,107,625

$2,359,500

Earnings per share:

$2,107,625/100,000

$21.08

$2,359,500/(100,000 +

100,000)

$11.80

Req. 2

TO: Management of Marcell Medical Goods

FROM: Student Name

SUBJECT: Advantages and disadvantages of borrowing

versus issuing stock to raise cash for expansion

Raising money by borrowing has at least two advantages over issuing

(continued) P 9-81B

in the business and to carry out their plans without interference from a new

group of stockholders. Under normal conditions, borrowing results in a higher

that may pose difficulties for the original stockholder group. Another

disadvantage of issuing stock is that earnings per share are usually lower

because of (1) the greater number of shares of stock outstanding, and (2) the

non-tax-deductibility of dividends paid on the stock.

(20-30 min.) P 9-82B

Req. 1

Gilbert Foods, Inc.

Partial Balance Sheet

Dec. 31, 2014

Property, plant,

and equipment:

Current liabilities:*

Equipment ……….

$731,000

Bonds payable,

Accumulated

current portion ……………….

$ 401,000

Depreciation ….

(165,000)

Mortgage note payable,

566,000

current portion ………………

83,000

Interest payable ……………….

34,000

Total current liabilities ………..

518,000

Long-term liabilities:

Mortgage note

payable …………………………..

$ 314,000

Bonds payable ….. $1,080,000

Less: Discount on

bonds payable ….. (322,000)*

758,000

Pension liability ……………….

42,000**

Total long-term liabilities ……

1,114,000

_____

Notes:

* The order of listing long-term liabilities is optional. However, Discount on

Bonds Payable should come immediately after Bonds Payable. Also, it is

customary to report Interest Payable after the related liability accounts.

Less: Pension plan assets, at market value …………………..

Pension liability to be reported on the balance sheet …….

(continued) P 9-82B

Req. 2

a. Carrying amount of bonds payable:

Current portion ……………………………………………………. $ 401,000

Req. 3

Times-interest-earned ratio

=

Operating income

=

$590,000

Interest expense

$227,000

=

2.60 times

Req. 4