Chapter 6

Inventory & Cost of Goods Sold

Short Exercises

(10-15 min.) S 6-1

1. (Journal entries)

Inventory ………………………………………………

120,000

Accounts Payable ……………………………..

120,000

Accounts Receivable …………………………….

165,000

Sales Revenue …………………………………..

165,000

Cost of Goods Sold ……………………………….

84,000

Inventory ($120,000 × .70) …………………..

84,000

Cash ($165,000 × .35) …………………………….

57,750

Accounts Receivable …………………………

57,750

2. (Financial statements)

BALANCE SHEET

Current assets:

Inventory ($120,000 − $84,000) ………………………..

$ 36,000

INCOME STATEMENT

Sales revenue ……………………………………………………..

$165,000

Cost of goods sold ………………………………………………

84,000

Gross profit ………………………………………………………..

$ 81,000

Inc.

(10-15 min.) S 6-2

City Copy Center

Income Statement

Year Ended December 31

Average

FIFO

LIFO

Sales revenue (600 × $19.50)

$11,700

$11,700

$11,700

Cost of goods sold (600 × $9.70*)

5,820

(100 × $8.40) + (500 × $9.90)

5,790

(600 × $9.90)

5,940

Gross profit

5,880

5,910

5,760

Operating expenses

3,750

3,750

3,750

Net income

$ 2,130

$ 2,160

$ 2,010

_____

*Average cost per unit:

Beginning inventory (100 @ $8.30) ……………………………..

$ 830

Purchases (700 @ $9.90) …………………………………………….

6,930

Cost of goods available ……………………………………………..

$7,760

Average cost per unit $7,760 / 800 units …………………

$ 9.70

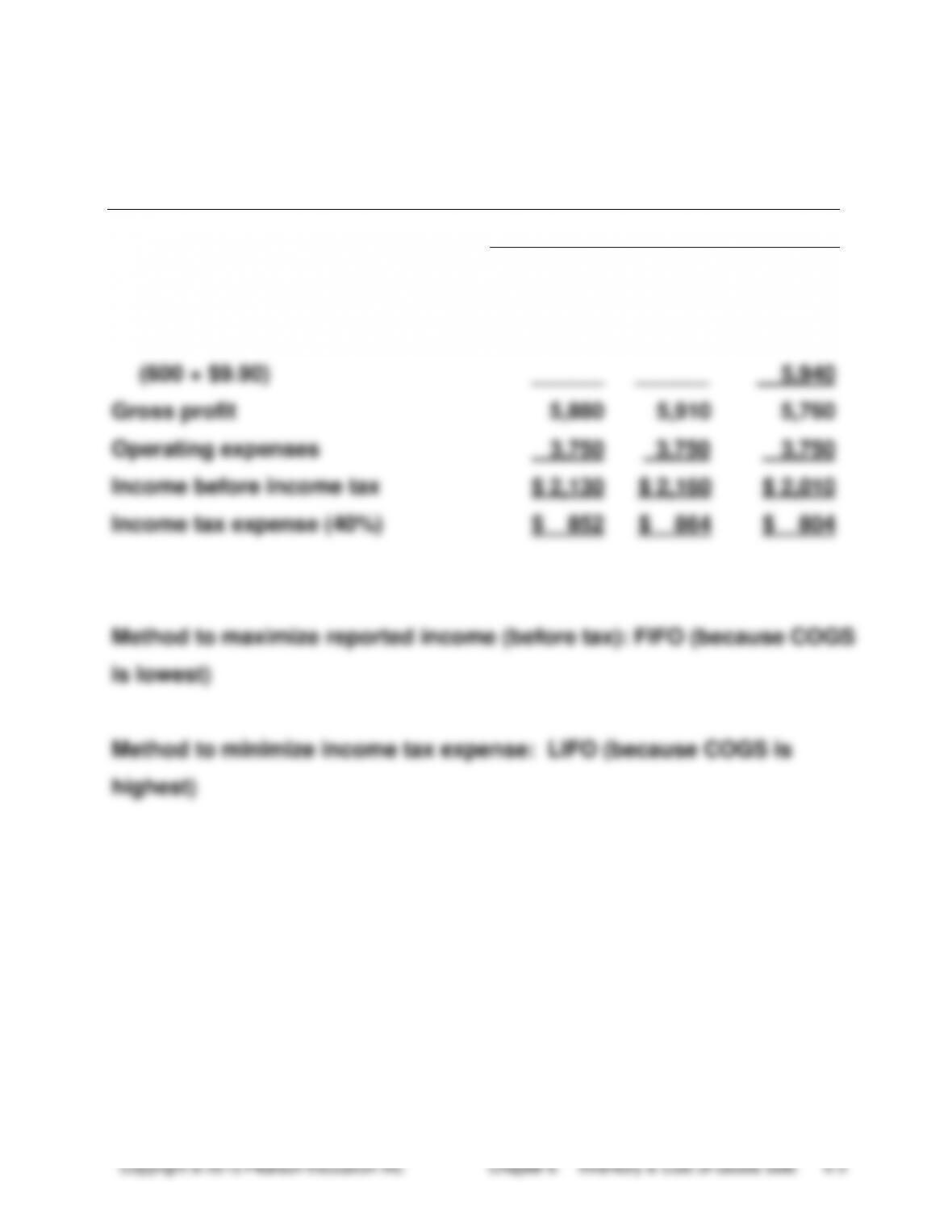

(10-15 min.) S 6-3

City Copy Center

Income Statement

Year Ended December 31

Average

FIFO

LIFO

Sales revenue (600 × $19.50)

$11,700

$11,700

$11,700

Cost of goods sold (600 × $9.70*)

5,820

(100 × $8.40) + (500 × $9.90)

5,790

(600 × $9.90)

______

______

5,940

Gross profit

5,880

5,910

5,760

Operating expenses

3,750

3,750

3,750

Income before income tax

$ 2,130

$ 2,160

$ 2,010

Income tax expense (40%)

$ 852

$ 864

$ 804

*From S 6-2

Inc.

(5 min.) S 6-4

Univision.com managers can purchase a large amount of inventory

before year end. Under LIFO, these high inventory costs go directly to

(5-10 min.) S 6-5

BALANCE SHEET

Current assets:

Inventories, at market (which is lower than cost) ………..

$ 52,000

INCOME STATEMENT

Cost of goods sold [$380,000 + ($56,000 − $52,000)] ……….

$384,000

(10-15 min.) S 6-6

FIFO 1. Maximizes reported income.

Specific

unit cost 2. Used to account for automobiles, jewelry, and art

objects.

FIFO 3. Results in a cost of ending inventory that is close to

the current cost of replacing the inventory.

Inc.

(5-10 min.) S 6-7

Dollars in Millions

Gross profit percentage

=

$53,376 − $24,437

=

54.2%

$53,376

Inventory turnover

=

$24,437

=

8.8 times

($2,672 + $2,908) / 2

(5-10 min.) S 6-8

Beginning inventory ………………………………………….

$ 15,000

+

Purchases ………………………………………………………..

420,000

=

Cost of goods available …………………………………….

435,000

−

Cost of goods sold:

Sales revenue ………………………………….

$870,000

Less estimated gross profit (60%) ……..

(522,000)

Estimated cost of goods sold …………………………

(348,000)

=

Estimated cost of ending inventory ……………………

$ 87,000

(5 min.) S 6-9

1. Last year’s reported gross profit was understated.

Correct gross profit last year was $3.8 million ($2.7 + $1.1).

(5-10 min.) S 6-10

1. Unethical. The company falsified its purchases, cost of goods sold,

and net income in order to evade taxes.

Inc.

Exercises

(15-20 min.) E 6-11A

Req. 1

Perpetual System

1.

Purchases:

Inventory ………………………………………………..

68,000

Accounts Payable ……………………………….

68,000

2.

Sales:

Cash ($115,000 × .17) ………………………………

19,550

Accounts Receivable ($115,000 × .83) ………

95,450

Sales Revenue …………………………………….

115,000

Cost of Goods Sold …………………………………

57,000

Inventory …………………………………………….

57,000

Req. 2

BALANCE SHEET

Current assets:

Inventory……………………………….

$26,000

INCOME STATEMENT

Sales revenue…………………………….

$115,000

Cost of goods sold………………………

57,000

Gross profit……………………………….

$58,000

(15-25 min.) E 6-12A

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Req. 1

Inventory ($1,248 + $2,145) ……………………..

3,393

Accounts Payable ………………………………

3,393

Req. 2

Accounts Receivable (17 @ $600) ……………

10,200

Sales Revenue …………………………………..

10,200

Cost of Goods Sold ………………………………..

2,683*

Inventory …………………………………………..

2,683

Req. 3

Sales revenue …………………………..………..

$10,200

Cost of goods sold ……………………………..

2,683

Gross profit ………………………………………..

$ 7,517

Ending inventory

($775 + $1,248 + $2,145 − $2,683) …….

$1,485**

_____

*(5 @ $155) + (8 @ $156) + (4 @ $165) = $2,683

**Or, (9 @ $165) = $1,485

Inc.

(10-15 min.) E 6-13A

Req. 1

Inventory

Beg. bal.

(5 units @ $155) 775

Purchases

Jan. 15

(8 units @ $156) 1,248

Cost of goods sold

26

(13 units @ $165) 2,145

(17 units @ $?)

?

End. bal.

(9 units @ $?) ?

Cost of Goods Sold

Ending Inventory

(a) Specific

unit cost

(2 @ $155) +

(8 @ $156) +

(7 @ $165)

=

$2,713

(3 @ $155) +

(6 @ $165)

=

$1,455

(b)Average

cost

(17 × $160.31*)

=

$2,725

(9 × $160.31*)

=

$1,443

(c) FIFO

(5 @ $155) +

(8 @ $156) +

(4 @ $165)

=

$2,683

(9 @ $165)

=

$1,485

(d) LIFO

(13 @ $165) +

( 4 @ $156)

=

$2,769

(5 @ $155) +

(4 @ $156)

=

$1,399

_____

*Average cost per

unit

=

($775 + $1,248 + $2,145)

=

$160.31

(5 + 8 + 13)

Req. 2

LIFO produces the highest cost of goods sold, $2,769.

(10 min.) E 6-14A

Cost of goods sold:

LIFO ($2,769) − FIFO ($2,683) …………………………………..

$ 86

× Income tax rate ……………………………………………………

× .28

Tax savings advantage of LIFO ……………………………………

$ 24

Inc.

(15 min.) E 6-15A

Req. 1

a.

FIFO

Cost of goods sold:

(11 @ $45) …………………………………….

$495

Ending inventory:

(4 @ $69) + (3 @ $45) …………………….

$411

b.

LIFO

Cost of goods sold:

(4 @ $69) + (7 @ $45) …………………….

$591

Ending inventory:

(7 @ $45) ………………………………………

$315

Req. 2

MusicWorld.net

Income Statement

Month Ended June 30, 2014

Sales revenue (11 @ $112) ……………………………………..

$1,232

Cost of goods sold ………………………………………………..

495

Gross profit …………………………………………………………..

737

Operating expenses ………………………………………………

340

Income before income tax………………………………………

397

Income tax expense (40%) ……………………………………..

159

Net income ……………………………………………………………

$ 238

(15 min.) E 6-16A

Req. 1

Gross profit:

FIFO

LIFO

Sales revenue …………………………………………….

$850,000

$850,000

Cost of goods sold

FIFO: 65,000 × $7 ……………………………………

455,000

LIFO: (40,000 × $4.20) + (10,000 × $5.10)

+ (15,000 × $7) …………………………….

324,000

Gross profit ……………………………………………….

$395,000

$526,000

Req. 2

Gross profit under FIFO and LIFO differ because inventory costs

decreased during the period.

(5-10 min.) E 6-17A

Debbie’s Garden Supplies

Income Statement (partial)

Year Ended October 31, 2014

Sales revenue ………………………………………………………………..

$246,000

Cost of goods sold [$120,000 + ($33,000 − $31,500)] …………

121,500

Gross profit ……………………………………………………………………

$124,500

Note: Cost is used for beginning inventory because cost is lower than

Inc.

(15-20 min.) E 6-18A

a.

$136,000

$41,000 + $132,000 − $37,000 = $136,000

b.

$117,000

$253,000 − $136,000 = $117,000

c.

Must first solve for d

d.

$ 93,000

$137,000 − $44,000 = $93,000

c.

$ 88,000

$26,000 + c − $93,000 = $21,000;

c = $88,000

e.

$ 97,000

$62,000 + $35,000 = $97,000

f.

$ 32,000

f + $54,000 − $24,000 = $62,000; f = $32,000

g.

$ 5,000

$9,000 + $29,000 − g = $33,000; g = $5,000

h.

$ 49,000

$82,000 − $33,000 = $49,000

Req. 1

Cailley Company

Income Statement

Year Ended December 31, 2014

Net sales ……………………………………….

$253,000

Cost of goods sold

Beginning inventory…………………..

$ 41,000

Net purchases …………………………..

132,000

Cost of goods available ……………..

173,000

Ending inventory ……………………….

(37,000)

Cost of goods sold …………………….

136,000

Gross profit ……………………………………

117,000

Operating and other expenses ………..

72,000

Net income …………………………………….

$ 45,000

(20-30 min.) E 6-19A

Req. 1

Company

Gross Profit

Percentage

Inventory Turnover

Cailley

$117

=

46.2%

$136

=

3.5 times

$253

($41 + $37) / 2

Durango

$44

=

32.1%

$93

=

4 times

$137

($26 + $21) / 2

Hartt

$35

=

36.1%

$62

=

2.2 times

$97

($32 + $24) / 2

Rosen

$49

=

59.8%

$33

=

4.7 times

$82

($9 + $5) / 2

Req. 2

Rosen has the highest gross profit percentage, 59.8%. Durango has the

lowest gross profit percentage, 32.1%.

Inc.

(15 min.) E 6-20A

Req. 1 and 2

1

2

FIFO

LIFO

Gross profit percentage

=

$154,000 − $80,900

$154,000 − $84,900

$154,000

$154,000

= 47.5%

= 44.9%

Inventory turnover

=

$80,900

$84,900

($18,000 + $23,000) / 2

($8,000 + $19,000) / 2

= 3.9 times

= 6.3 times

Req. 3

Req. 4

(10-15 min.) E 6-21A

Year ended January 31, 2014

Millions

Budgeted cost of goods sold ($6,500 × 1.12) …………………….

$7,280

Budgeted ending inventory ……………………………………………..

2,100

Budgeted cost of goods available ……………………………………

9,380

Actual beginning inventory ……………………………………………..

(1,800)

Budgeted purchases ………………………………………………………

$7,580

(10-15 min.) E 6-22A

Beginning inventory ………………………………………..

$ 45,700

Net purchases ………………………………………………..

62,300

Cost of goods available …………………………………..

108,000

Estimated cost of goods sold:

Net sales revenue ………………………………………

$107,600

Less: estimated gross profit of 45% …………….

(48,420)

Estimated cost of goods sold ……………………..

59,180

Estimated cost of inventory destroyed ……………..

$ 48,820

Another reason that managers use the gross profit method to estimate

ending inventory is to test the reasonableness of ending inventory.

Inc.

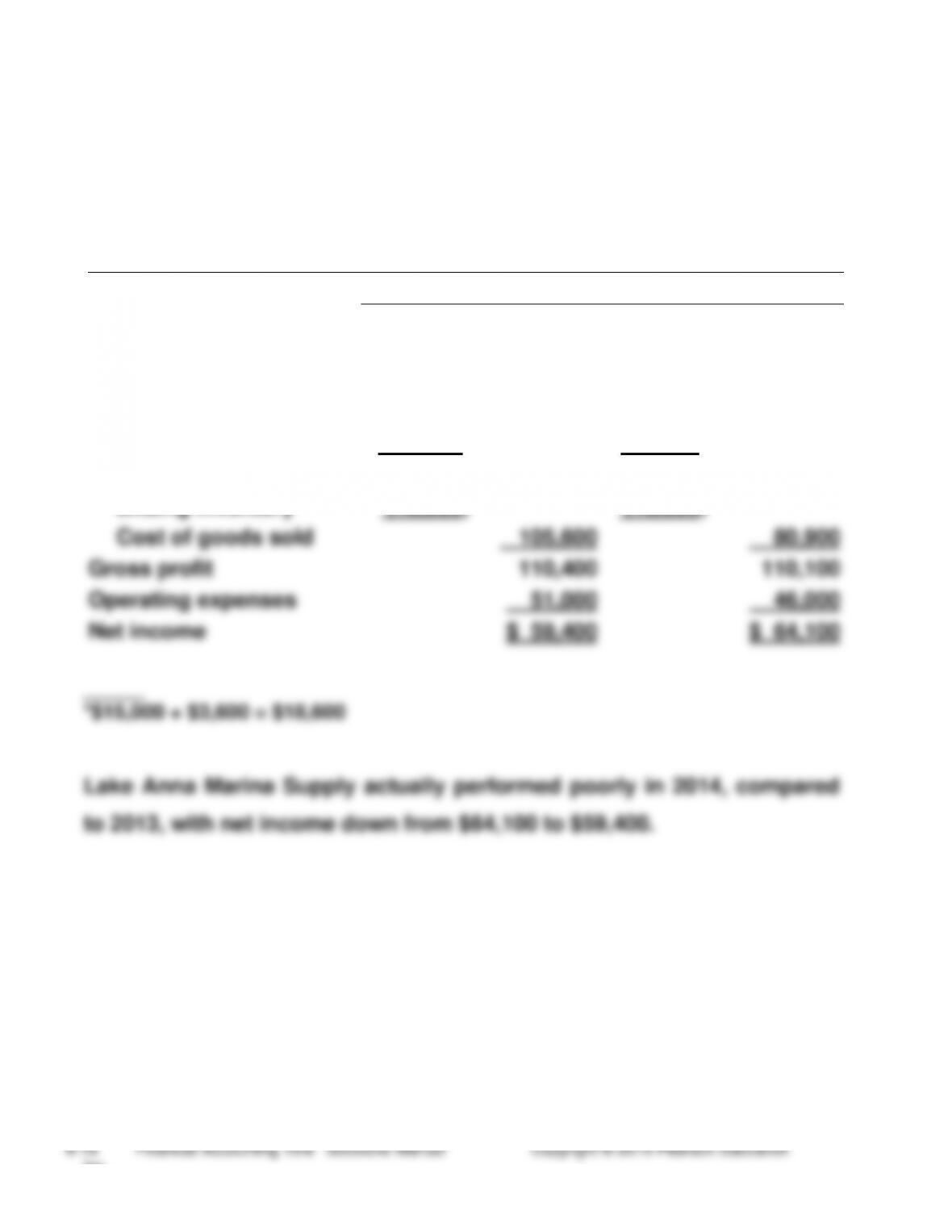

(10-15 min.) E 6-23A

Lake Anna Marine Supply

Income Statement (Corrected)

Years Ended June 30, 2014 and 2013

2014

2013

Sales revenue

$216,000

$191,000

Cost of goods sold:

Beginning inventory

$18,600

$ 11,500

Net purchases

105,000

88,000

Cost of goods avail.

123,600

99,500

Ending inventory

(18,000)

(18,600)*

Cost of goods sold

105,600

80,900

Gross profit

110,400

110,100

Operating expenses

51,000

46,000

Net income

$ 59,400

$ 64,100

_____

*$15,000 + $3,600 = $18,600

Lake Anna Marina Supply actually performed poorly in 2014, compared

to 2013, with net income down from $64,100 to $59,400.

(15-20 min.) E 6-24B

Req. 1

Perpetual System

1.

Purchases:

Inventory ………………………………………………..

72,000

Accounts Payable ……………………………….

72,000

2.

Sales:

Cash ($108,000 × .21)……………………………….

22,680

Accounts Receivable ($108,000 × .79) ……….

85,320

Sales Revenue …………………………………….

108,000

Cost of Goods Sold …………………………………

56,000

Inventory …………………………………………….

56,000

Req. 2

BALANCE SHEET

Current assets:

Inventory …………………………………………..

$ 28,000

INCOME STATEMENT

Sales revenue ………………………………………..

$108,000

Cost of goods sold …………………………………

56,000

Gross profit …………………………………………..

$ 52,000

Inc.

(15-25 min.) E 6-25B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Req. 1

Inventory ($1,376 + $2,520) ………………………..

3,896

Accounts Payable ………………………………..

3,896

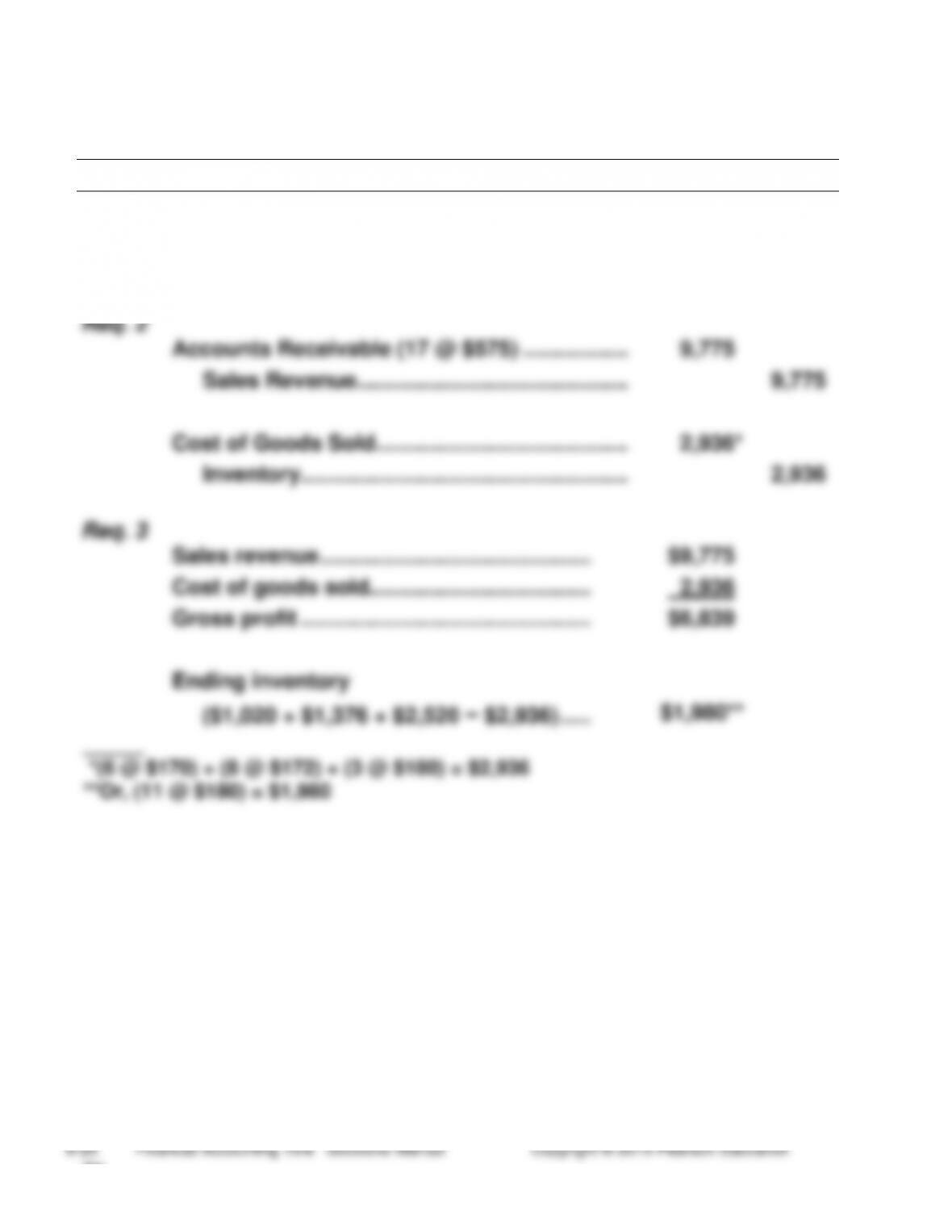

Req. 2

Accounts Receivable (17 @ $575) ……………..

9,775

Sales Revenue ……………………………………..

9,775

Cost of Goods Sold…………………………………..

2,936*

Inventory ……………………………………………..

2,936

Req. 3

Sales revenue ……………………………………..

$9,775

Cost of goods sold………………………………

2,936

Gross profit ………………………………………..

$6,839

Ending inventory

($1,020 + $1,376 + $2,520 − $2,936) …..

$1,980**