(5-10 min.) E 7-27A

Req. 1

Net profit margin ratio

for the years ended:

January 31, 2013

January 31, 2012

Net earnings

$ 2,010

=

4.12%

$ 1,783

=

3.78%

Net sales

$48,815

$47,220

The net profit margin ratio improved from 2012 to 2013.

Req. 2

Asset turnover for

the years ended:

January 31, 2013

January 31, 2012

Net sales

$48,815

=

1.45

$47,220

=

1.43

Average total assets

$33,699

$33,005

The asset turnover improved slightly from 2012 to 2013.

Req. 3

Return on assets

for the years

ended:

January 31, 2013

January 31, 2012

Net earnings

$ 2,010

=

5.96%

$ 1,783

=

5.40%

Average total

assets

$33,699

$33,005

or

4.12% x 1.45

=

5.97%*

3.78% x 1.43

=

5.41%*

The return on assets improved from 2012 to 2013; the increase in the

net profit margin ratio was mostly responsible for this.

_____

*difference due to rounding

(10 min.) E 7-28A

a.

Sale of building (or disposal of building) ………………………

$740,000

b.

Insurance proceeds from fire (or disposal of building) …..

185,000

c.

Renovation of store (or capital expenditures) ………………..

(203,000)

d.

Purchase of store fixtures (or capital expenditures) ………

(68,000)

(5-10 min.) E 7-29B

(10-15 min.) E 7-30B

Allocation of cost to individual machines:

Machine

Appraised

Value

Percentage of Total

Appraised (Market) Value

Total

Cost

Cost of

Each

Machine

1

$ 68,000

$68,000 / $210,000

=

.324

$175,000 × .324

=

$ 56,700

2

54,000

54,000 / 210,000

=

.257

175,000 × .257

=

44,975

3

88,000

88,000 / 210,000

=

.419

175,000 × .419

=

73,325

Totals

$210,000

1.00

$175,000

Sale price of machine no. 3 ……………………..

$ 88,000

Cost ……………………………………………………….

(73,325)

Gain on sale of machine ………………………….

$ 14,675

(5-10 min.) E 7-31B

(a) Purchase price

(b) Transportation and insurance

(c) Sales tax

(d) Installation

Capital Expenditure

Capital Expenditure

Capital Expenditure

Capital Expenditure

(e) Training of personnel

(f) Reinforcement to platform

(g) Income tax

Capital Expenditure

Capital Expenditure

Immediate Expense

(h) Major overhaul

(i) Ordinary recurring repairs

Capital Expenditure

Immediate Expense

(j) Lubrication before machine is placed in

service

Capital Expenditure

(k) Periodic lubrication

Immediate Expense

(15 min.) E 7-32B

Req. 1

Journal

ACCOUNT TITLES

DEBIT

CREDIT

a.

Land …………………………………………………………..

315,000

Cash ……………………………………………………..

315,000

b.

Building

($1,700 + $15,700 + $718,000 + $35,900) ………..

771,300

Note Payable ………………………………………….

718,000

Cash ($1,700 + $15,700 + $35,900) ……………

53,300

c.

Depreciation Expense – Building …………………

4,263

Accumulated Depreciation – Building

($771,300 − $323,650) / 35 × 4/12 ……………..

4,263

Req. 2

BALANCE SHEET

Plant assets:

Land ……………………………………………………..

$315,000

Building ………………………………………………..

$771,300

Less: Accumulated depreciation …………….

(4,263)

Building, net ………………………………………….

767,037

Req. 3

INCOME STATEMENT

Expense:

Depreciation expense – Building …………….

$ 4,263

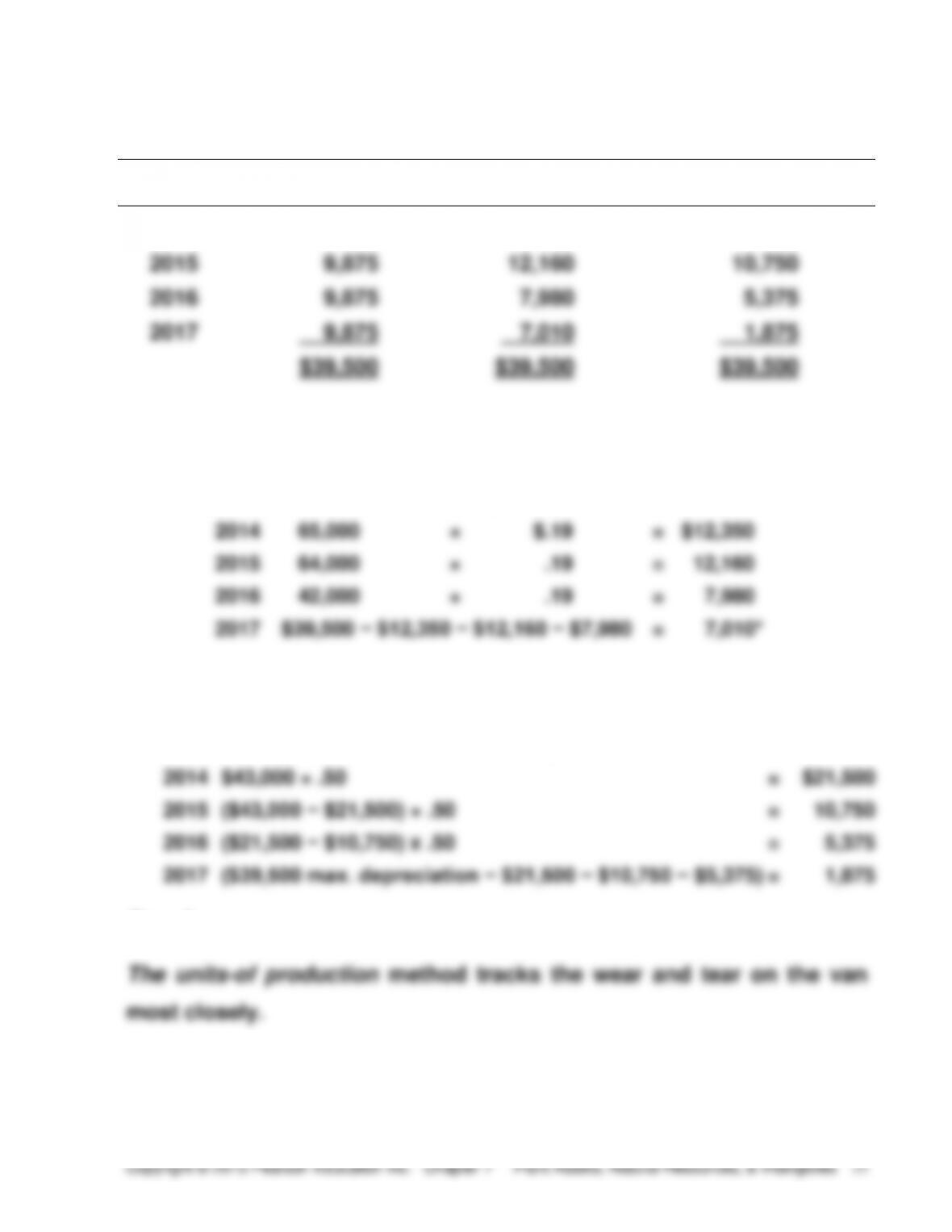

(15-20 min.) E 7-33B

Req. 1

Year

Straight-Line

Units–of–

Production

Double-Declining-

Balance

2014

$ 9,875

$12,350

$21,500

2015

9,875

12,160

10,750

2016

9,875

7,980

5,375

2017

9,875

7,010

1,875

$39,500

$39,500

$39,500

_____

Computations:

Straight–line: ($43,000 − $3,500) ÷ 4 = $9,875 per year.

Units–of–production: ($43,000 − $3,500) ÷ 208,000 miles = $.19 per mile;

2014

65,000

×

$.19

=

$12,350

2015

64,000

×

.19

=

12,160

2016

42,000

×

.19

=

7,980

2017

$39,500 − $12,350 − $12,160 − $7,980

=

7,010*

*Total depreciation cannot exceed $39,500, therefore the last year is limited,

due to rounding differences.

Double-declining-balance — Twice the straight-line rate: 1/4 × 2 = 50%

2014

$43,000 × .50

=

$21,500

2015

($43,000 − $21,500) × .50

=

10,750

2016

($21,500 − $10,750) x .50

=

5,375

2017

($39,500 max. depreciation − $21,500 − $10,750 − $5,375)

=

1,875

Req. 2

(continued) E 7-33B

Req. 3

(15 min.) E 7-34B

INCOME STATEMENT

Expenses:

Depreciation expense — Building

[($158,000 + $65,000) − $50,000] / 25 ………………………..

$ 6,920

Depreciation expense — Furniture and Fixtures

($51,000 × 2/5) …………………………..…………………………...

20,400

Supplies expense

($9,000 − $1,600) …………………………………………………….

7,400

BALANCE SHEET

Current assets:

Supplies …………………………………………………………………….

$ 1,600

Plant assets:

Building ($158,000 + $65,000) …………………..

$223,000

Less: Accumulated depreciation ………………

(6,920)

$216,080

Furniture and fixtures ………………………………

51,000

Less: Accumulated depreciation ………………

(20,400)

30,600

STATEMENT OF CASH FLOWS

Cash flows from investing activities:

Purchase of buildings ($54,000* + $65,000) ……………….

$(119,000)

Purchase of furniture and fixtures…………………………….

(51,000)

_____

*Does not include the $104,000 note payable because Early Risers Café

paid no cash on the note.

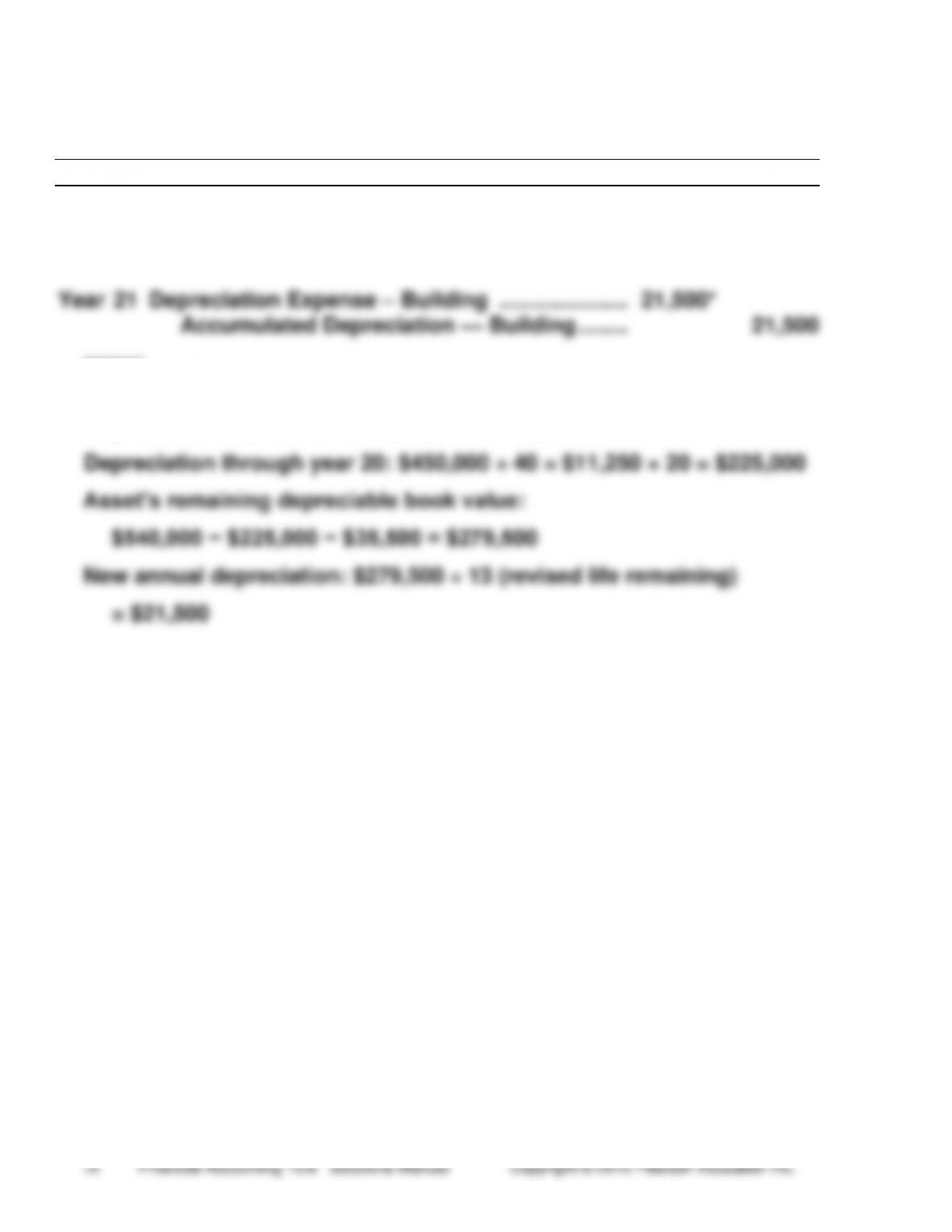

(10-15 min.) E 7-35B

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Year

20

Depreciation Expense – Building ($450,000 ÷ 40)

11,250

Accumulated Depreciation — Building ……..

11,250

Year

21

Depreciation Expense – Building …………………

21,500*

Accumulated Depreciation — Building ……..

21,500

*Computations:

Depreciable cost: $540,000 − $90,000 = $450,000

(15-20 min.) E 7-36B

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

2015

Depreciation for 10 months:

Oct.

31

Depreciation Expense – Fixtures …………

1,840*

Accumulated Depreciation —

Fixtures ……………………………………..

1,840

Sale of fixtures:

31

Cash ………………………………………………….

2,700

Accumulated Depreciation —

Fixtures ($3,680 + $1,840) …………………

5,520

Loss on Sale of Fixtures …………………….

980**

Fixtures ………………………………………..

9,200

_____

*2014 depreciation: $9,200 × 2/5 = $3,680

2015 depreciation: ($9,200 − $3,680) × 2/5 × 10/12 = $1,840

**Loss on sale of fixtures:

Sale price of old fixtures ………………………………….

$ 2,700

Book value of old fixtures:

Cost ……………………………………………………………

$9,200

Less: Accumulated depreciation ($3,680 +

$1,840) ……………………………………………………

(5,520)

(3,680)

Loss on sale ……………………………………………………

$ (980)

(10-15 min.) E 7-37B

Cost of old truck …………………………………………………..

$430,000

Less: Accumulated depreciation:

($430,000 − $20,000) ×

81+ 111 + 141 + 75

(167,280)*

1,000

_______

Book value of old truck ………………………………………..

$262,720

_____

*Alternate solution setup for accumulated depreciation:

($430,000 − $20,000)

=

$.41 per mile

1,000,000 miles

81,000 + 111,000 + 141,000 + 75,000 = 408,000 miles driven

Accumulated depreciation

=

408,000 miles × $.41

=

$167,280

Calculation of gain or loss:

Purchase price of Freightliner truck ……….. $280,000

Cash paid for Freightliner truck ……………… (25,000)

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

2017

Truck – Freightliner ……………………….

280,000

Accumulated Depreciation – Mack

Truck ……………………………………….

167,280

Loss on Disposal of Mack Truck……

7,720

Truck – Mack ………………………..

430,000

Cash…………………………………….

25,000

(10-15 min.) E 7-38B

Journal

DATE

ACCOUNT TITLES AND

EXPLANATION

DEBIT

CREDIT

(a)

Purchase of mineral assets:

Mineral Asset………………………………..

628,000

Cash ……………………………………….

628,000

(b)

Payment of fees and other costs:

Mineral Asset ($930 + $2,300) ………..

3,230

Cash ……………………………………….

3,230

Mineral Asset………………………………..

66,820

Cash ……………………………………….

66,820

(c)

Depletion for the year

Mineral Asset Inventory …………………

124,700*

Mineral Asset …………………………..

124,700

(d)

Sales of ore

Cost of Mineral Asset Sold …………….

113,950**

Mineral Asset Inventory ……………

113,950

_____

*$628,000 + $930 + $2,300 + $66,820 = $698,050

$698,050 ÷ 325,000 tons = $2.15 per ton

58,000 tons × $2.15 = $124,700

**53,000 tons x $2.15 = $113,950

(10-15 min.) E 7-39B

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Req.

1

(a)

Purchase of patent:

Patents ……………………………………..

1,200,000

Cash……………………………………..

1,200,000

(b)

Amortization for each year:

Amortization Expense — Patents

($1,200,000 ÷ 12) ………………………..

100,000

Patents …………………………………

100,000

Req.

2

Impairment loss in year 8:

Impairment Loss on Patents ………

400,000

Patents …………………………………

400,000

The asset is impaired because the net book value ($400,000*) is greater

than the estimated future cash flows ($350,000). The amount of the

impairment loss is $400,000 (net book value minus fair value of $-0-).

*Asset remaining book value: $1,200,000 – ($100,000 x 8) = $400,000

(5-10 min.) E 7-40B

Req. 1

Cost of goodwill purchased:

Millions

Purchase price paid for Southwest.com ………………………..

$28

Market value of Southwest’s net assets:

Market value of Southwest’s assets ($14 + $32) ………..

$46

Less: Southwest’s liabilities ……………………………………

(29)

Market value of Southwest’s net assets …………………..

17

Cost of goodwill ………………………………………………………….

$11

Req. 2

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Current Assets ……………………………………………….

14

Long-Term Assets ………………………………………….

32

Goodwill ………………………………………………………..

11

Liabilities …………………………………………………

29

Cash ………………………………………………………..

28

Req. 3

Hurd Co. will determine whether its goodwill has been impaired in

(5-10 min.) E 7-41B

Req. 1

Net profit margin ratio

for the years ended:

January 31, 2013

January 31, 2012

Net earnings

$ 1,116

=

1.36%

$ 70

=

0.09%

Net sales

$82,189

$76,733

The net profit margin ratio improved from 2012 to 2013.

Req. 2

Asset turnover for

the years ended:

January 31, 2013

January 31, 2012

Net sales

$82,189

=

3.50

$76,733

=

3.32

Average total assets

$23,505

$23,126

The asset turnover improved slightly from 2012 to 2013.

Req. 3

Return on assets

for the years

ended:

January 31, 2013

January 31, 2012

Net earnings

$ 1,116

=

4.75%

$ 70

=

0.30%

Average total

assets

$23,505

$23,126

or

1.36% x 3.50

=

4.76%*

0.09% x 3.32

=

0.30%

The return on assets improved from 2012 to 2013; the increase in the

net profit margin ratio was mostly responsible for this.

_____

*difference due to rounding

(10 min.) E 7-42B

a.

Sale of building (or disposal of building) ……………………..

$710,000

b.

Insurance proceeds from fire (or disposal of building) ….

108,000

c.

Renovation of store (or capital expenditures) ……………….

(201,000)

d.

Purchase of store fixtures (or capital expenditures) ……..

(73,000)

Quiz

Q7-43

a

Q7-44

b

Q7-45

c

[$480,000 / ($480,000 + $270,000) × ($3,000,000 +

$1,000,000)] ÷ 15 = $170,667

Q7–46

d

Q7–47

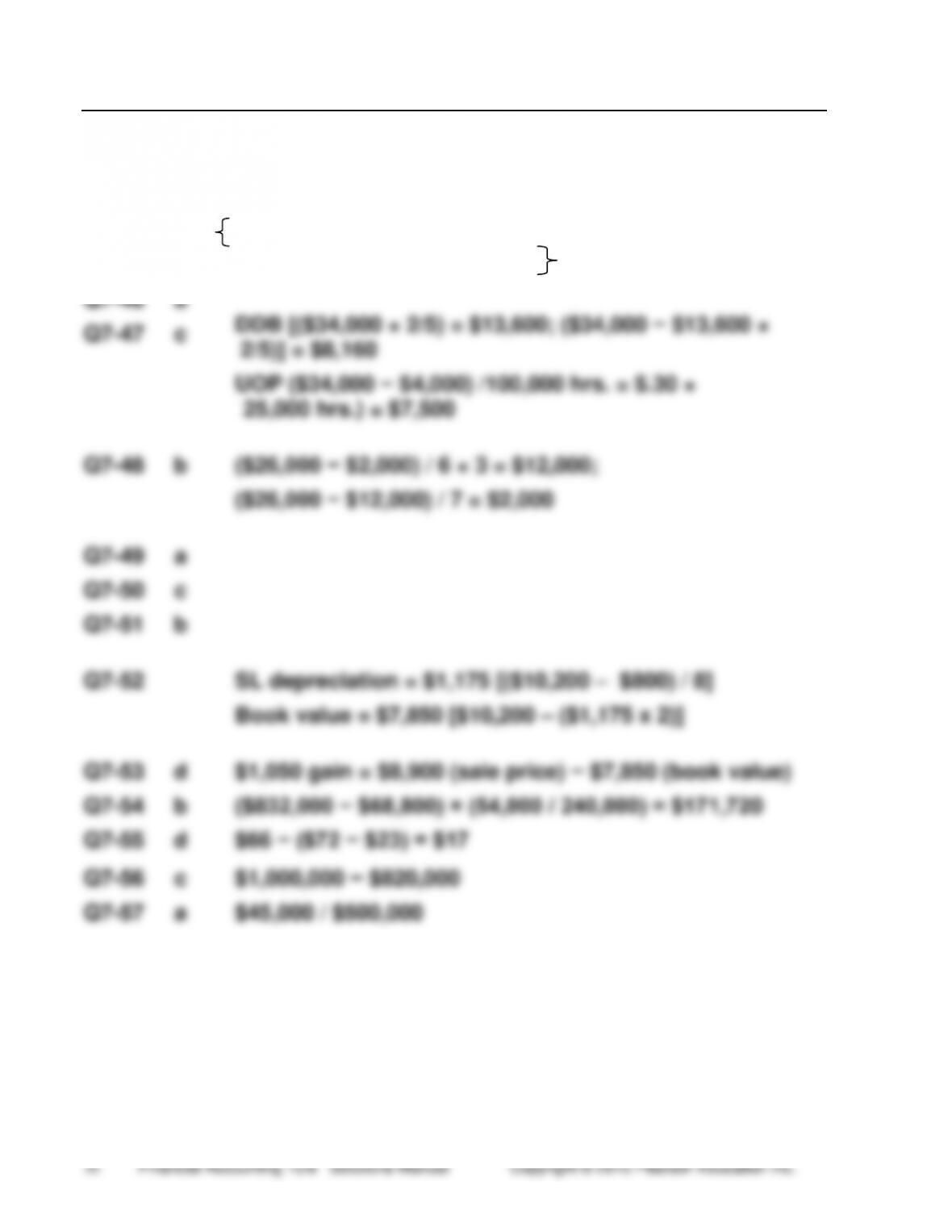

c

DDB [($34,000 × 2/5) = $13,600; ($34,000 − $13,600 ×

2/5)] = $8,160

UOP ($34,000 − $4,000) /100,000 hrs. = $.30 ×

25,000 hrs.) = $7,500

Q7–48

b

($26,000 − $2,000) / 6 × 3 = $12,000;

($26,000 − $12,000) / 7 = $2,000

Q7–49

a

Q7–50

c

Q7-51

b

Q7-52

SL depreciation = $1,175 [($10,200 – $800) / 8]

Book value = $7,850 [$10,200 – ($1,175 x 2)]

Q7-53

d

$1,050 gain = $8,900 (sale price) − $7,850 (book value)

Q7–54

b

($832,000 − $68,800) × (54,000 / 240,000) = $171,720

Q7–55

d

$66 − ($72 − $23) = $17

Q7–56

c

$1,000,000 − $820,000

Q7–57

a

$45,000 / $500,000

Problems

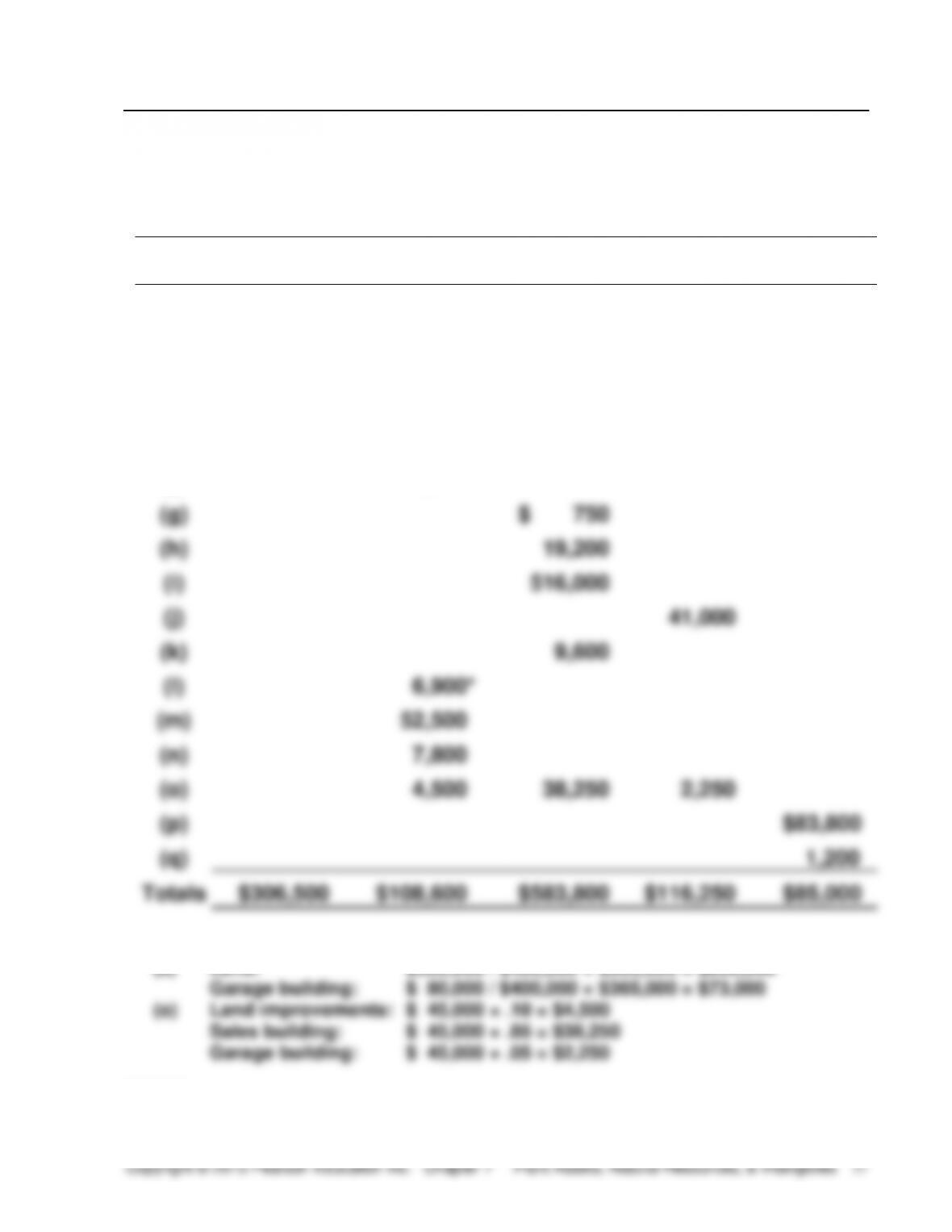

(20-30 min.) P 7-58A

Req. 1

ITEM

LAND

LAND

IMPROVEMENTS

SALES

BUILDING

GARAGE

BUILDING

FURNITURE

(a)

$292,000

$ 73,000

(b)

8,300

(c)

$ 35,400

(d)

300

(e)

5,900

(f)

1,500

(g)

$ 750

(h)

19,200

(i)

516,000

(j)

41,000

(k)

9,600

(l)

6,900*

(m)

52,500

(n)

7,800

(o)

4,500

38,250

2,250

(p)

$83,800

(q)

1,200

Totals

$306,500

$108,600

$583,800

$116,250

$85,000

Computations:

(a) Land: $320,000 / $400,000 × $365,000 = $292,000

_____

*Some accountants would debit this cost to the Land account.

(continued) P 7-58A

Req. 2

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Dec.

31

Depreciation Expense — Land

Improvements ($108,600 / 20 × 9/12) ………..

4,073*

Accumulated Depreciation —

Land Improvements …………………………

4,073

31

Depreciation Expense — Sales Building

($583,800 / 50 × 9/12) ………………………………

8,757

Accumulated Depreciation —

Sales Building …………………………………

8,757

31

Depreciation Expense — Garage

Building ($116,250 / 50 × 9/12) …………………

1,744

Accumulated Depreciation —

Garage Building ………………………………

1,744

31

Depreciation Expense — Furniture

($85,000 / 12 × 9/12) ………………………………..

5,312

Accumulated Depreciation —

Furniture …………………………………………

5,312

____

*$3,814 ($101,700 / 20 × 9/12) if $6,900 (l in Req. 1) is debited to Land.

(continued) P 7-58A

Req. 3

This problem shows how to determine the cost of a plant asset. It also

demonstrates the computation of depreciation for a variety of plant

assets. Because virtually all businesses use plant assets, a manager

(15 min.) P 7-59A

Req. 1

Journal

ACCOUNT TITLES

DEBIT

CREDIT

Equipment …………………………………………………………..

145,000

Cash …………………………………………………………….

145,000

Depreciation Expense — Buildings ………………………

32,600

Accumulated Depreciation — Buildings ………….

32,600*

Depreciation Expense — Equipment …………………….

44,300

Accumulated Depreciation — Equipment ………..

44,300**

*($739,000 − $87,000) / 20

**[($412,000 − $263,000) × 2/10 + ($145,000 × 2/10 × 6/12)]

Req. 2

BALANCE SHEET

Property, plant, and equipment:

Land ………………………………………………………….

$151,000

Buildings …………………………………………………..

$ 739,000

Less: Accumulated Depreciation

($348,000 + $32,600) ……………………….

(380,600)

358,400

Equipment ($412,000 + $145,000) ………………..

$ 557,000

Less: Accumulated Depreciation

($263,000 + $44,300) ……………………….

(307,300)

249,700

Total property, plant, and equipment ……………….

$759,100