Chapter 9

Liabilities

Short Exercises

(10 min.) S 9-1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

July

31

Inventory …………………………………………………

22,500

Note Payable, Short-Term ……………………

22,500

Purchased inventory by issuing a

note payable.

2015

Apr.

30

Interest Expense ($22,500 × .06 × 9/12) ………

1,013

Interest Payable ………………………………….

1,013

Accrued interest expense.

July

31

Note Payable, Short-Term …………………………

22,500

Interest Payable ……………………………………….

1,013

Interest Expense ($22,500 × .06 × 3/12) ………

337

Cash …………………………………………………..

23,850

Paid note payable and interest at

maturity.

(5-10 min.) S 9-2

Req. 1

2014

2013

Accounts payable turnover:

Purchases*

Average accounts payable

$2,900,000 = 9.1

$317,600

$2,500,000 = 9.9

$252,600

Days payable outstanding:

365

Accounts payable turnover

365 = 40 days

9.1

365 = 37 days

9.9

*Purchases = COGS + Ending inventory – Beginning inventory

2014 = $2,600,000 + $1,000,000 – $700,000 = $2,900,000

2013 = $2,400,000 + $700,000 – $600,000 = $2,500,000

Req. 2

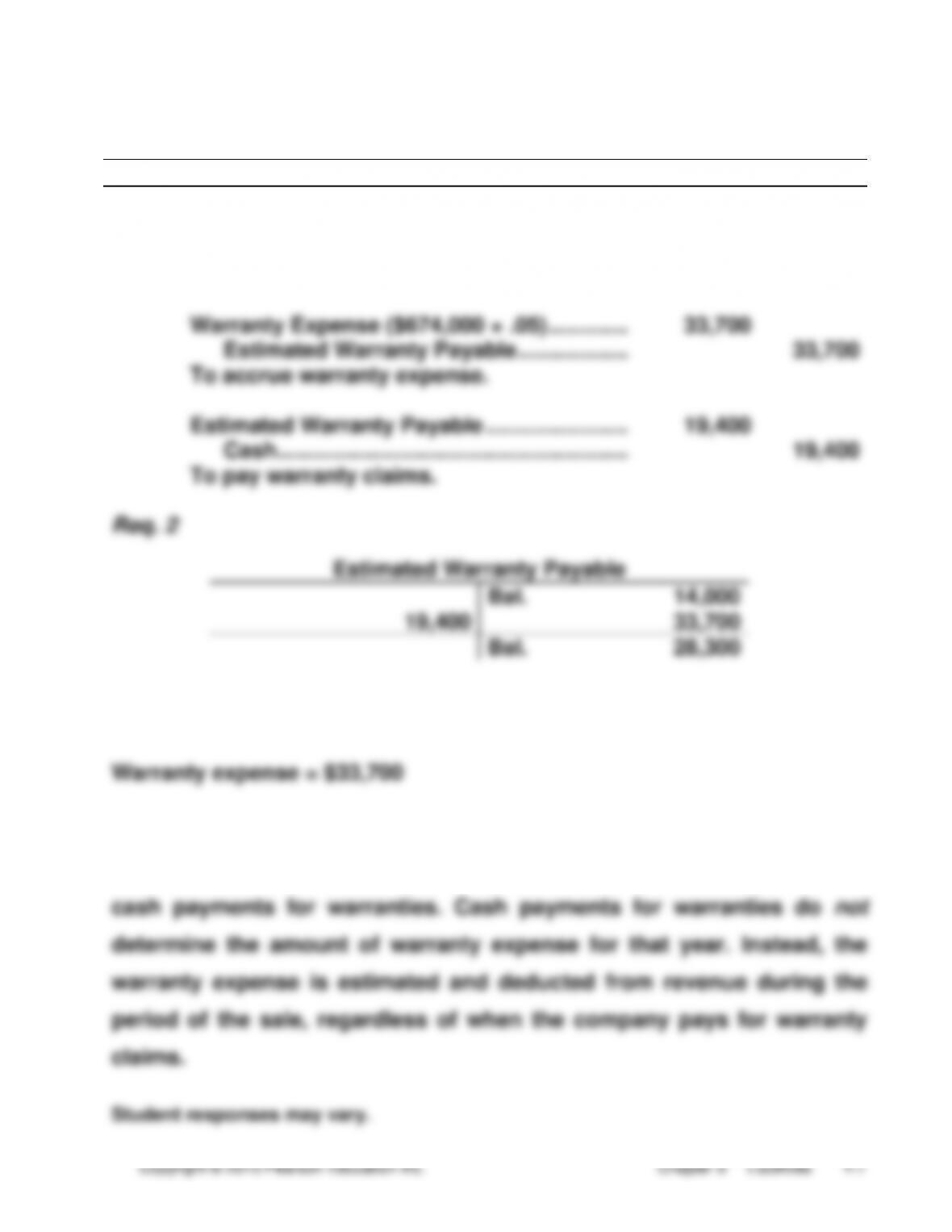

(10 min.) S 9-3

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Cash ($674,000 × .35) ……………………………..

235,900

Notes Receivable ($674,000 − $235,900) ….

438,100

Sales Revenue ………………………………….

674,000

To record sales on account.

Warranty Expense ($674,000 × .05) ………….

33,700

Estimated Warranty Payable ………………

33,700

To accrue warranty expense.

Estimated Warranty Payable …………………..

19,400

Cash…………………………………………………

19,400

To pay warranty claims.

(5-10 min.) S 9-5

1. These are contingent liabilities, because, at the time of the note,

Wheels, Inc., was not liable for any of these product losses.

(5-10 min.) S 9-6

1. False – the cash received is equal to the present value of the future

cash flows.

2. False – the contract (stated) rate, not the market rate, is always used

to calculate the cash interest payment.

(5 min.) S 9-7

(5-10 min.) S 9-8

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

a.

July

1

Cash …………………………………………………..

150,000

Bonds Payable ……………………………….

150,000

To issue bonds at par.

b.

Dec.

31

Interest Expense ($150,000 × .04 × 6/12) …..

3,000

Interest Payable ……………………………..

3,000

To accrue interest expense.

2015

c.

Jan.

1

Interest Payable ………………………………….

3,000

Cash ………………………………………………

3,000

To pay semiannual interest on bonds.

2021

d.

July

1

Bonds Payable ……………………………………

150,000

Cash ………………………………………………

150,000

To pay bonds at maturity.

(10-15 min.) S 9-9

Req. 1 Using the PV function in EXCEL, the bond price is $535,964.

Req. 2 Amortization table

A

B

C

D

E

Semiannual

Interest Date

Interest

Payment

(1.25% of

Maturity

Value)

Interest

Expense

(1.5% of

Preceding

Bond

Carrying

Amount)

Discount

Amortization

(B – A)

Discount

Account

Balance

(Preceding

D – C)

Bond

Carrying

Amount

($560,000

– D)

Mar. 31, 2014

24,036

535,964

Sept. 30, 2014

7,000

8,039

1,039

22,997

537,003

Mar. 31, 2015

7,000

8,055

1,055

21,942

538,058

Sept. 30, 2015

7,000

8,071

1,071

20,871

539,129

Req. 3

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Mar.

31

Cash (from Req. 1) ……………………….

535,964

Discount on Bonds Payable …………

24,036

Bonds Payable ……………………….

560,000

Sept.

30

Interest Expense ………………………….

8,039

Discount on Bonds Payable …….

1,039

Cash ………………………………………

7,000

(10 min.) S 9-10

Req. 1— Borrowed $535,964. Maturity value is $560,000.

Req. 2—Cash interest is $7,000.

Req. 3—Interest expense September 30, 2014 is $8,039.

(10-15 min.) S 9-11

Req. 1—Borrowed $1,950,000:

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

July

1

Cash ($2,000,000 × .975) ……………….

1,950,000

Discount on Bonds Payable ………….

50,000

Bonds Payable ………………………..

2,000,000

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Dec.

31

Interest Expense …………………………….

42,500

Discount on Bonds Payable ……….

2,500

Interest Payable ………………………..

40,000

2015

Jan.

1

Interest Payable ……………………………..

40,000

Cash …………………………………………

40,000

(10-15 min.) S 9-12

Req. 1

Best Buy

Co.

Wal-Mart

Stores

5

Leverage

ratio

$16,787 / $3,061

5.48

$203,105 / $76,343

2.66

6

Total

debt

$16,787 − $3,061

$13,726

$203,105 − $76,343

$126,762

7

Debt

ratio

$13,726 / $16,787

.82

$126,762 / $203,105

.62

8

Times

interest

earned

$1,085 / $134

8.1 times

$27,801 / $2,064

13.5 times

Req. 2

Best Buy has a higher leverage ratio and debt ratio, and a lower times–

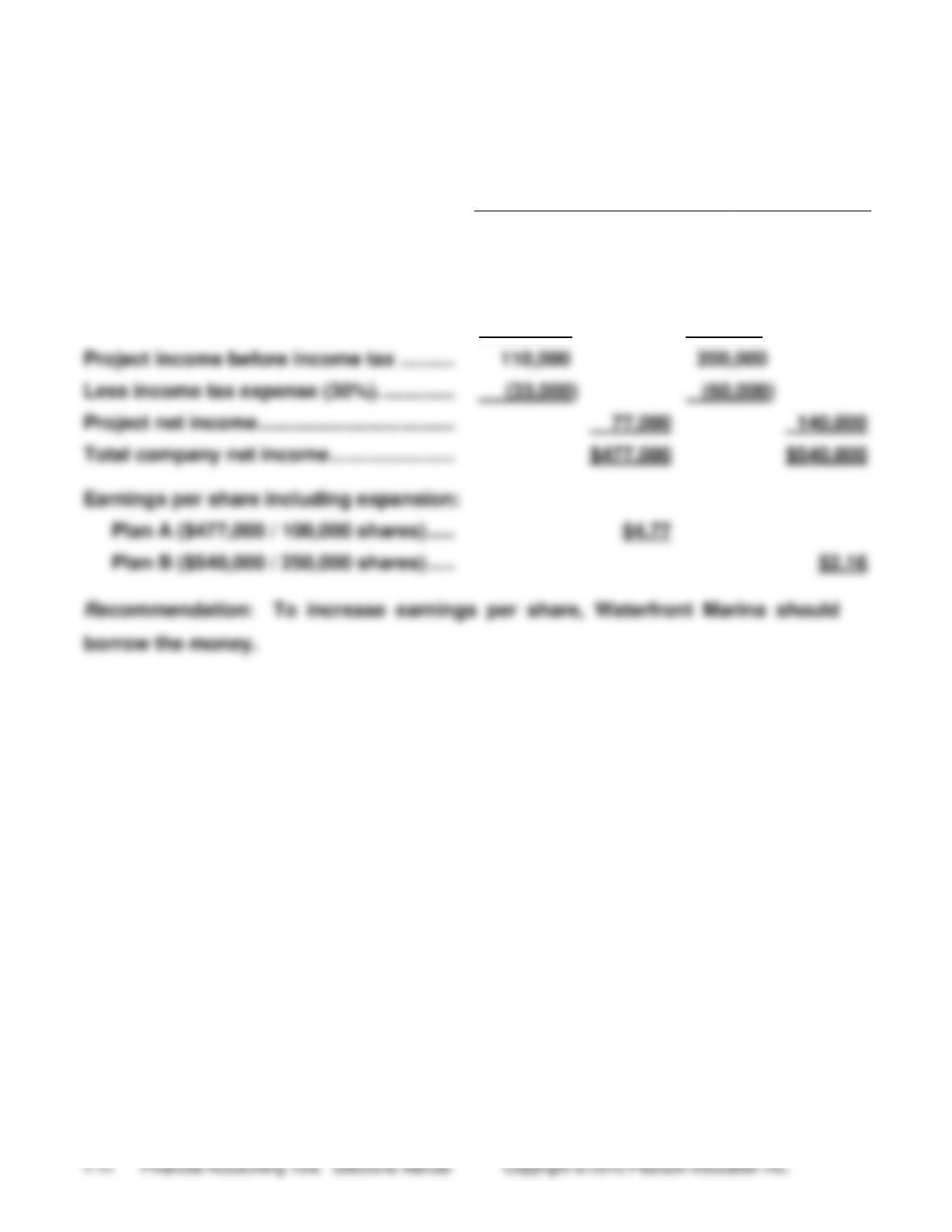

(10-15 min.) S 9-13

Plan A

Issue $1,500,000 of

6% Bonds Payable

Plan B

Issue $1,500,000

of Common Stock

Net income before expansion ………………

$400,000

$400,000

Project income before interest

and income tax ……………………………….

$ 200,000

$200,000

Less: interest expense ($1,500,000 × .06)

(90,000)

-0-

Project income before income tax ……….

110,000

200,000

Less income tax expense (30%). ………….

(33,000)

(60,000)

Project net income ………………………………

77,000

140,000

Total company net income …………………..

$477,000

$540,000

Earnings per share including expansion:

Plan A ($477,000 / 100,000 shares) …..

$4.77

Plan B ($540,000 / 250,000 shares) …..

$2.16

(5-10 min.) S 9-14

Req. 1

Leverage

ratio

$100.0 / $40.0

=

2.5

This means that Ferguson has $2.50 of assets for every

dollar of stockholders’ equity.

Debt ratio

$60.0 / $100.0

=

.60

This means that Ferguson has $.60 in liabilities (debt) for

every dollar of assets.

Times interest

earned

$4.1 / $1.1

=

3.73 times

This means that for every dollar of interest expense

Ferguson has earned $3.73 of operating income.

Ferguson’s debt ratio is about average and can cover its

existing interest expense. I would be willing to lend

Ferguson $1 million.

(10 min.) S 9-15

LIABILITIES

Current:

Accounts payable ………………………………….

$ 28,500

Current portion of bonds payable …………..

56,000

Interest payable …………………………………….

1,600

Total current liabilities ……………………….

86,100

Long term:

Notes payable, long-term ……………………….

125,000

Bonds payable ………………………………………

$350,000

Less: Discount on bonds payable …………..

(11,250)

338,750

Total liabilities …………………………..………………

$549,850

Exercises

(5-15 min.) E 9-16A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Warranty Expense ($108,000 × .08) ……….

8,640

Estimated Warranty Payable …………….

8,640

Estimated Warranty Payable …………………

7,100

Cash ……………………………………………….

7,100

Req. 2

INCOME STATEMENT

Sales revenue ………………………………………………….

$108,000

Warranty expense ……………………………………………

8,640

BALANCE SHEET

Current liabilities

Estimated warranty payable

($4,500 + $8,640 − $7,100) …………………………

$ 6,040

Req. 3

(10-15 min.) E 9-17A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Oct.

1

Cash ………………………………………………………..

1,962

Unearned Subscription Revenue……………

1,800

Sales Tax Payable ($1,800 × .09) ……………

162

Nov.

15

Sales Tax Payable …………………………………….

162

Cash…………………………………………………….

162

Dec.

31

Unearned Subscription Revenue ……………….

450

Subscription Revenue ($1,800 × 3/12) …….

450

BALANCE SHEET

Current liabilities:

Unearned subscription revenue ($1,800 − $450) …………….

$1,350

(10 min.) E 9-18A

INCOME STATEMENT

Expenses:

Payroll expense ………………………………………………………

$125,000

Payroll tax expense ($125,000 × .08) …………………………

10,000

BALANCE SHEET

Current liabilities:

Salary payable ………………………………………………………..

$9,500

Payroll tax payable …………………………..……………………..

920

(5-10 min.) E 9-19A

Req. 1

Accrued interest,

Dec. 31, 2014

=

$58,000 × .04 × 9/12

=

$1,740

Req. 2

Final payment

=

$58,000 + ($58,000 × .04)

=

$60,320

on April 1, 2015

Req. 3

Interest expense for:

2014

=

$58,000 × .04 × 9/12

=

$1,740

2015

=

$58,000 × .04 × 3/12

=

$ 580

(10-15 min.) E 9-20A

Bracken’s balance sheet at Dec. 31, 2015, reported:

Income tax payable ………………………………………..

$ 94,600*

Bracken’s 2015 income statement reported:

Income tax expense ($680,000 × .29) ……………….

$197,200

_____

* Beginning income tax payable ….. ……………………..

$ 75,000

+ Income tax expense (and payable) for the year

($680,000 × .29) …………………………………………………..

197,200

− Income tax payments during the year ……………………

(177,600)

= Ending income tax payable ……………………………………

$ 94,600

(10-20 min.) E 9-21A

Req. 1

Accounts payable are amounts owed to suppliers for products or

services that have been purchased on account.

Accrued expenses are expenses that the company has incurred but not

(continued) E 9-21A

Req. 2

Total assets = $3,701 million, the sum of total liabilities and

stockholders’ equity.

(in millions) 2014

Leverage

ratio

=

Total assets ($3,701)

Total stockholders’ equity ($1,951)

=

1.90

Debt ratio

=

Total liabilities ($3,701 − $1,951)*

=

0.47

Total assets ($3,701)

For 2013, the leverage ratio was 2.25 and the debt ratio was .56.

Both the leverage ratio and debt ratio improved in 2014. Therefore, the

company improved.

____

*Or, $256 + $1,384 + $102 + $8 = $1,750

Req. 3

2014 2013

Accounts

payable

turnover

Cost of goods sold

$1,546

= 10.8

$1,650

= 8.9

Average Accounts

payable

$143*

$185**

*($107 + $179) / 2

**($179 + $190) / 2

Days

payable

outstanding

365

365

= 33.8

365

= 41.0

Accts. payable

turnover

10.8

8.9

Current

ratio

Current assets

$658

= 2.57

$603

= 1.54

Current liabilities

$256

$391

The company’s ability to cover accounts payable and current liabilities

over the year improved.

(5-10 min.) E 9-22A

Req. 1

Strong Security Systems should report this situation in a note to the

financial statements. It is the company’s policy to disclose legal

Req. 2

Strong would report:

INCOME STATEMENT

Estimated loss (or expense) due to lawsuit

contingency …………………………………..

$2,100,000

BALANCE SHEET

Estimated liability due to lawsuit contingency

$2,100,000

The note disclosure would be similar to Requirement 1.

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Estimated Loss due to Lawsuit Contingency …..

2,100,000

Estimated Liability due to Lawsuit

Contingency ……………………………………………

2,100,000

(15-20 min.) E 9-23A

Best Electronics

Balance Sheet (partial)

March 31, 2014

Current liabilities:

a. Estimated warranty payable

[$41,000 + ($1,800,000 × .04) − $67,000] …………….

$ 46,000

b. Current portion of long-term note payable …………….

15,000

Interest payable ($75,000 × .03 × 1/12) …………………..

188

c. Unearned sales revenue ($110,000 − $80,000) ………..

30,000

d. Employee withheld income tax payable ………………..

27,900

FICA tax payable ($260,000 × .0765)… …………………..

19,890

Total current liabilities …………………………………….

$138,978

Long-term liabilities:

Note payable ($75,000 − $15,000) ………………………….

$ 60,000