(10-20 min.) E 4-29B

Joe Donney

Bank Reconciliation

August 31, 2014

BANK:

Balance, August 31

$ 638

Add: Deposit in transit

1,695

2,333

Less: Outstanding checks

(756)

Adjusted bank balance

$1,577

BOOKS:

Balance, August 31

$1,620

Add: EFT collection — rent

375

1,995

Less:

Service charge

$ 9

NSF checks

137

Charge for printed checks

20

Correction of book error —

recorded $280 check as $28

252

(418)

Adjusted book balance

$1,577

Donney’s actual cash balance is $1,577.

(10-15 min.) E 4-30B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Aug

31

Cash …………………………………………………

375

Rent Revenue ……………………………….

375

EFT collection of rent.

31

Miscellaneous Expense ($9 + $20) ………

29

Cash…………………………………………….

29

Bank service charge and charge

for printed checks.

31

Accounts Receivable …………………………

137

Cash…………………………………………….

137

NSF checks returned by bank.

31

Salary Expense ($280 − $28) ………………

252

Cash…………………………………………….

252

Correction of book error.

(10-15 min.) E 4-31B

TO: Store Manager

FROM: Student

SUBJECT: Evaluation of internal control and plan for improvement

There is a weakness in internal control over cash receipts. The cash

registers do not keep a record of sales. With no record, there is no way

(10-15 min.) E 4-32B

The main internal control weakness is that the payroll department both

(20-30 min.) E 4-33B

Carron Communications, Inc.

Cash Budget

Year Ended December 31, 2015

Millions

Cash balance, December 31, 2014

$ 72

Budgeted cash receipts:

Collections from customers

11,233

Sale of assets

108

11,413

Budgeted cash payments:

Payments for cost of

services and products

$6,129

Payments of operating expenses

2,756

Investment in equipment

1,543

Payment of debt

611

Payment of dividends

316

11,355

Cash available (needed) before financing

58

Budgeted cash balance, December 31, 2015

(65)

Cash available for additional investments, or

(New financing needed)

$ (7)

Carron expects to need new financing of $7 million during 2015.

Quiz

Q4–34

c

Q4–35

a

Q4–36

b

Q4–37

d

Q4–38

b

Q4–39

c

Q4–40

c

Q4–41

d

Q4–42

a

Q4–43

d

Q4–44

Q4–45

c [$14,000 + $81,000 − $44,000 − $34,000 − $25,000 −

$13,000 = ($21,000); arrange financing for this

amount.]

e

Problems

(15-20 min.) P 4-46A

The internal control weaknesses in English Imports’ system are:

1. O’Hara controls the content of the invoices. With no supervision of

2. Luck has both cash handling and accounting duties. With both

responsibilities, Luck could steal incoming cash and cover her theft

1. Make the purchase and pay arrangements with the English artisans

(10-20 min.) P 4-47A

Requirement 1

Requirement 2

Requirement 3

Missing Internal

Control

Characteristic

Possible Problem

Solution

a.

Separation of

duties

Theft of diamonds

— the purchasing agent

could have diamonds

sent to a location he

controls.

Separate

purchasing,

approval, and

check-signing

duties.

b.

Assignment of

responsibility

Lost revenue, because

too many employees

are managing the office

and neglecting their

duties.

Assign a single

employee to

manage the office

when the owner is

absent.

c.

Separation of

duties

Theft of cash.

Separate

accounting and

cash-handling

duties.

(20-30 min.) P 4-48A

Req. 1

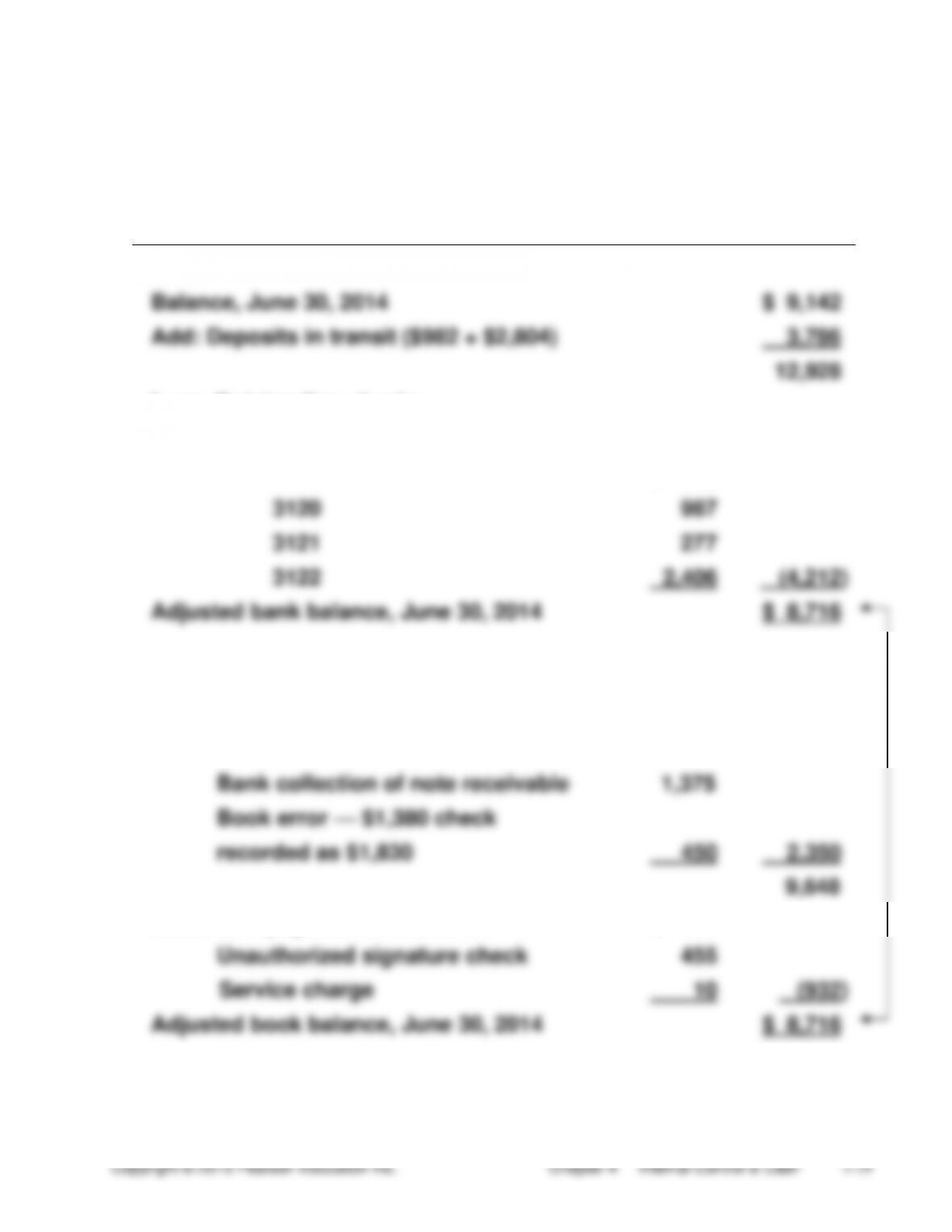

Richmond Automotive

Bank Reconciliation

June 30, 2014

BANK:

Balance, June 30, 2014

$ 9,142

Add: Deposits in transit ($982 + $2,804)

3,786

12,928

Less: Outstanding checks —

Check No.

3119

$ 542

3120

987

3121

277

3122

2,406

(4,212)

Adjusted bank balance, June 30, 2014

$ 8,716

BOOKS:

Balance, June 30, 2014

$ 7,298

Add: EFT collection of rent

$ 525

Bank collection of note receivable

1,375

Book error — $1,380 check

recorded as $1,830

450

2,350

9,648

Less: EFT payment of insurance

$ 467

Unauthorized signature check

455

Service charge

10

(932)

Adjusted book balance, June 30, 2014

$ 8,716

(continued) P 4-48A

Req. 2 (entries based on the reconciliation)

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

June

30

Cash …………………………………………………………

525

Rent Revenue ……………………………………….

525

EFT deposit for rent revenue earned.

30

Cash …………………………..…………………………….

1,375

Note Receivable …………………………..……….

1,375

Note receivable collected by bank.

30

Cash …………………………..…………………………….

450

Accounts Payable …………………………………

450

Correction for check #3115 recorded

incorrectly.

30

Insurance Expense …………………………………….

467

Cash …………………………………………………….

467

EFT for payment of insurance.

30

Accounts Receivable …………………………………

455

Cash …………………………………………………….

455

US customer check returned by bank.

30

Miscellaneous Expense ……………………………..

10

Cash …………………………………………………….

10

Bank service charge.

(continued) P 4-48A

Req. 3

A bank account helps control cash by providing a place for safekeeping.

The bank also provides a detailed list of the company’s cash

(30-45 min.) P 4-49A

Dallas Wireless

Cash Budget

2015

Thousands

Cash balance, beginning

$ 1,600

Budgeted cash receipts:

Collections from customers ($61,000 × 1.25)

76,250

Receipt of interest

400

78,250

Budgeted cash payments:

Cash paid for inventory ($46,000 × 1.26)

$57,960

Cash paid for operating expenses

13,200

Purchases of equipment

4,500

Purchases of investments

800

Payment of dividends

500

Payment of long-term debt

200

(77,160)

Cash available (needed) before financing

1,090

Budgeted cash balance, ending

(4,675)

Cash available for additional investments, or

(New financing needed)

$ (3,585)

(15-20 min.) P 4-50B

The internal control weaknesses in Finnish Imports’ system are:

1. Martin controls the content of the invoices. With no supervision of her

2. Moore has both cash handling and accounting duties. With both

responsibilities, Moore could steal incoming cash and cover her theft

1. Make the purchase and pay arrangements with the artisans who

2. Ferguson could assign either cash handling or accounting duties to

Moore and then hire someone else to do the other (accounting or

(10-20 min.) P 4-51B

Requirement 1

Requirement 2

Requirement 3

Missing Internal

Control

Characteristic

Possible Problem

Solution

a.

Separation of duties

Theft of cash or

diamonds by the

purchasing agent.

Have a manager, not

the purchasing agent,

approve invoices for

payment and sign the

checks.

b.

Assignment of

responsibilities

Lost revenue due to

delay of architectural

drawings.

Assign one senior

architect to fulfill

management duties

while Klepper is absent.

Other senior architect

should focus on

producing architectural

drawings.

c.

Separation of duties

Theft of cash.

Keep accounting and

cash handling duties

separate.

(20-30 min.) P 4-52B

Req. 1

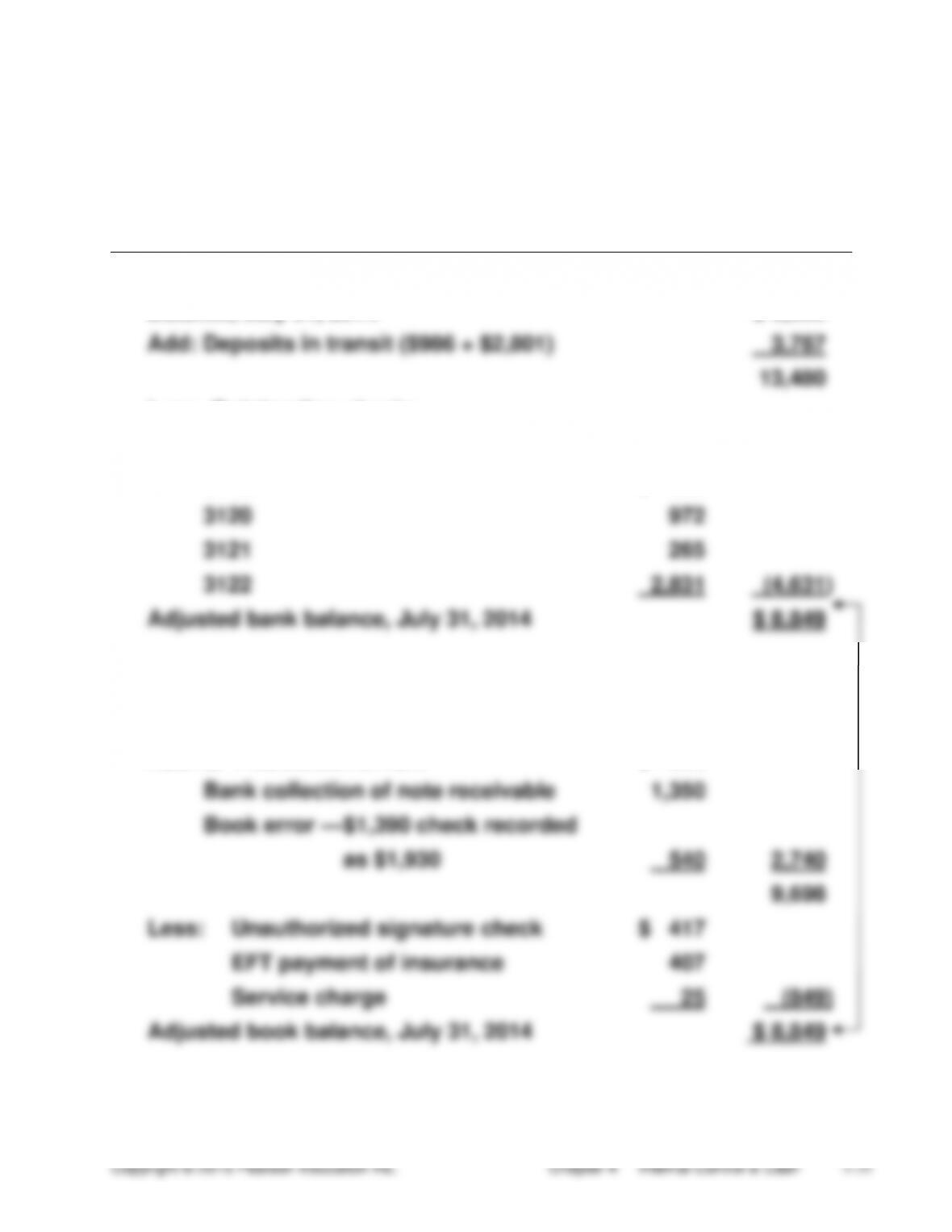

Big City Automotive

Bank Reconciliation

July 31, 2014

BANK:

Balance, July 31, 2014

$ 9,693

Add: Deposits in transit ($986 + $2,801)

3,787

13,480

Less: Outstanding checks

Check No.

3119

$ 563

3120

972

3121

265

3122

2,831

(4,631)

Adjusted bank balance, July 31, 2014

$ 8,849

BOOKS:

Balance, July 31, 2014

$ 6,958

Add: EFT collection of rent

$ 850

Bank collection of note receivable

1,350

Book error — $1,390 check recorded

as $1,930

540

2,740

9,698

Less: Unauthorized signature check

$ 417

EFT payment of insurance

407

Service charge

25

(849)

Adjusted book balance, July 31, 2014

$ 8,849

(continued) P 4-52B

Req. 2 (entries based on the reconciliation)

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

July

31

Cash ………………………………………………………….

850

Rent Revenue ……………………………………….

850

EFT deposit for rent revenue.

31

Cash ………………………………………………………….

1,350

Note Receivable ……………………………………

1,350

Note receivable collected by bank.

31

Cash ………………………………………………………….

540

Accounts Payable …………………………………

540

Correction for check #3115 recorded

incorrectly.

31

Accounts Receivable ………………………………….

417

Cash …………………………..………………………..

417

US customer check returned by bank.

31

Insurance Expense …………………………………….

407

Cash …………………………..………………………..

407

EFT for payment of insurance.

31

Miscellaneous Expense………………………………

25

Cash …………………………..………………………..

25

Bank service charge.

(continued) P 4-52B

Req. 3