(15-20 min.) E 5-25B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Dec.

31

Doubtful-Account Expense ($795,000 × .02) …

15,900

Allowance for Doubtful Accounts ……………

15,900

BALANCE SHEET

Current assets:

Accounts receivable, net of allowance

for doubtful accounts of $16,630* ……………………..

$65,370**

_____

*$730 + $15,900 = $16,630

**$82,000 − $16,630 = $65,370

(15 min.) E 5-26B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Oct.

Accounts Receivable ………………………………..

323,000

Sales Revenue ……………………………………..

323,000

Oct.

Cash ………………………………………………………..

257,000

Accounts Receivable …………………………...

257,000

Oct.

Allowance for Uncollectible Accounts………..

3,600

Accounts Receivable …………………………...

3,600

Oct.

Uncollectible-Account Expense

($323,000 × .03) …………………………………………

9,690

Allowance for Uncollectible Accounts ……

9,690

Req. 2

Accounts Receivable

Allowance for

Uncollectible Accounts

56,000

257,000

3,000

323,000

3,600

3,600

9,690

Bal.

118,400

9,090

Net accounts receivable = $109,310 ($118,400 − $9,090)

Pendley Party Shop expects to collect the net receivable amount.

Req. 3

BALANCE SHEET (Partial)

Current assets:

Accounts receivable ……………………………………………..

Less: Allowance for uncollectible accounts …………..

$118,400

(9,090)

Accounts receivable, net ……………………………………………….

$109,310

IINCOME STATEMENT (Partial)

Net sales

$323,000

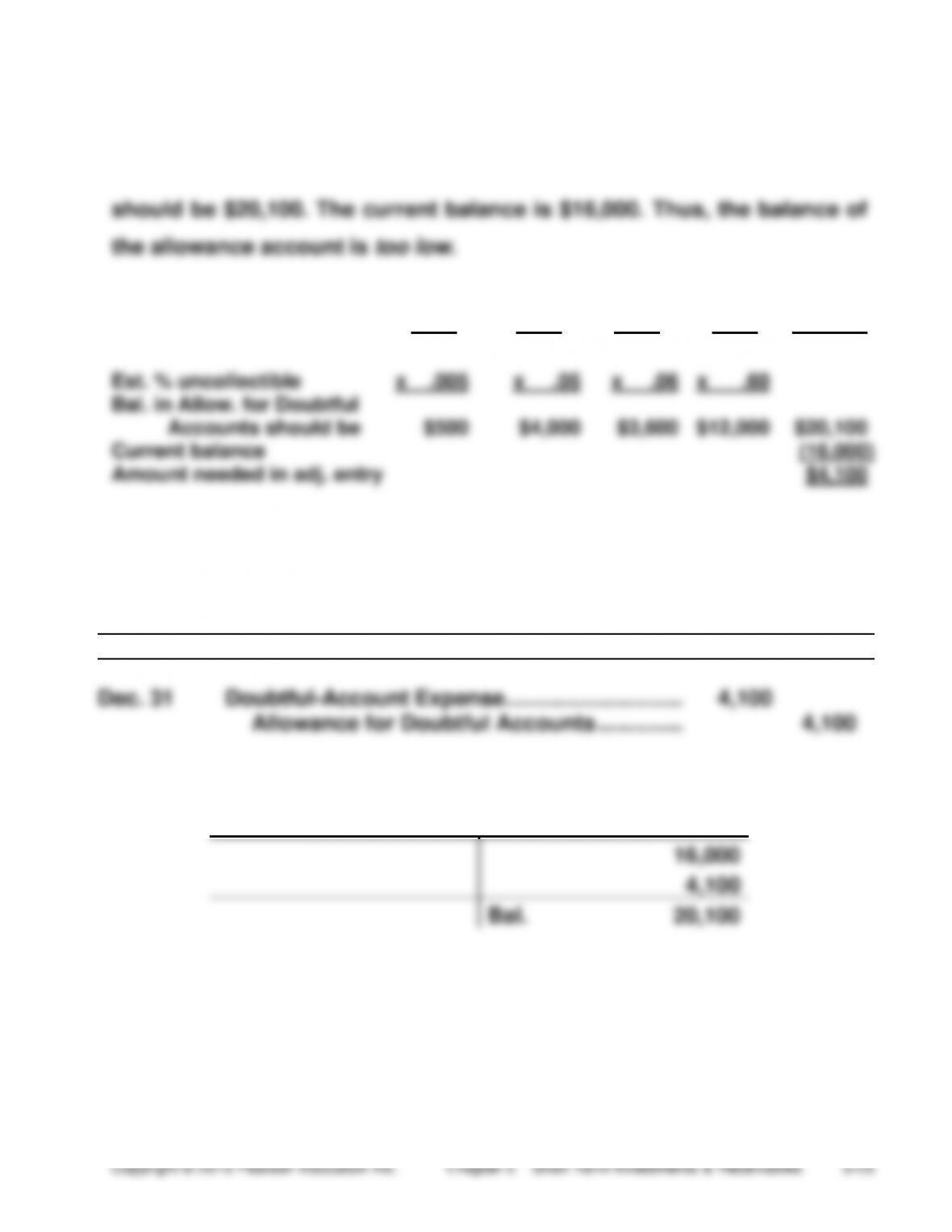

(15-30 min.) E 5-27B

Req. 1

The credit balance at December 31 in Allowance for Doubtful Accounts

1-30 31–60 61–90 Over 90 Total

days days days days balance

$100,000 $80,000 $60,000 $20,000

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Dec. 31

Doubtful-Account Expense ………………………..

4,100

Allowance for Doubtful Accounts …………..

4,100

Allowance for Doubtful Accounts

16,000

4,100

Bal.

20,100

(continued) E 5-27B

Req. 3

BALANCE SHEET

Current assets:

Cash …………………………………………………………..

$ XX

Short-term investments ……………………………….

XX

Accounts receivable, net of allowance

for doubtful accounts of $20,100 ………………

239,900*

Or

Accounts receivable ……………………………………

$260,000

Less: Allowance for doubtful accounts …………

(20,100)

239,900

(15-20 min.) E 5-28B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

May

Accounts Receivable …………………………………

5,300

Service Revenue …………………………………..

5,300

Recorded revenue on account.

May

Bad-Debt Expense ($5,300 × .04) …………………

212

Allowance for Bad Debts ……………………….

212

Recorded expense for the month.

May

Sales Returns and Allowances ……………………

104

Accounts Receivable …………………………….

104

Recorded sales returns from customers.

May

Allowance for Bad Debts ($31 + $219) …………

250

Accounts Receivable …………………………….

250

Wrote off uncollectible receivables.

(10-15 min.) E 5-29B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

May

1

Note Receivable — Rock Cason …………………

19,000

Cash…………………………………………………….

19,000

July

6

Note Receivable — Fairway Golf Course …….

15,000

Service Revenue …………………………………..

15,000

16

Note Receivable — Hull, Inc……………………….

5,000

Accounts Receivable – Hull, Inc. ……………

5,000

31

Interest Receivable ……………………………………

343*

Interest Revenue …………………………………..

343

_____

*($19,000 × .06 × 91/365) + ($15,000 × .05 × 25/365) + ($5,000 × .04 × 15/365) = $343**

$284** + $51** + $8**

** Rounded to nearest dollar.

Oak Tree Realty earned interest revenue of $343 this year.

(10-15 min.) E 5-30B

Req. 1

Cash and Short-term Net current

(a)

Acid-test

=

Cash equiv. + investments + receivables

ratio

Total current liabilities

=

$7,000 + $29,000 + $62,000

$23,000 + $109,000

=

$98,000

$132,000

=

0.74

An acid-test ratio of 0.74 is fairly weak.

(b)

One day’s

=

Sales revenue

=

$812,500

=

$2,226

sales

365

365

Days’ sales

Average net

in

=

accounts receivable

=

($62,000 + $76,000) / 2

receivables

One day’s sales

$2,226

=

31 days

Req. 2

(10-15 min.) E 5-31B

Req. 1

Average collection period:

Millions of dollars

One day’s sales

=

$750,500

=

$2,056

365

Days’ sales in receivables

=

($4,870 + $5,210) / 2

=

2.45 days

(average collection period)

$2,056

Req. 2

City Electronics Co., Inc’s collection period is short because City

Quiz

Q5–32

b

Q5–33

c

Q5–34

d

Q5–35

a

[($170,000 × .02) + ($41,000 × .08) + ($9,000 × .20) −

$3,000 = $5,480]

Q5–36

$211,520

($220,000 − $8,480 = $211,520)

Q5–37

c

($100,000 × .02 = $2,000)

Q5–38

b

($3,000 + $2,000 = $5,000)

Q5–39

$3,000

($5,000 − $2,000 = $3,000)

Q5–40

d

($30,000 × .11 × 5/12 = $1,375)

Q5–41

a

Q5–42

c

($30,000 × .11 × 6/12 = $1,650)

Q5–43

b

Q5–44

Cash ………………………………

Note Receivable …………

Interest Receivable …….

Interest Revenue ………..

31,650

30,000

1,375

275

Q5–45

c

Q5–46

c

[($90,000 + $114,000) / 2] ÷ ($1,095,000 / 365 days) =

34 days]

Q5–47

a

Problems

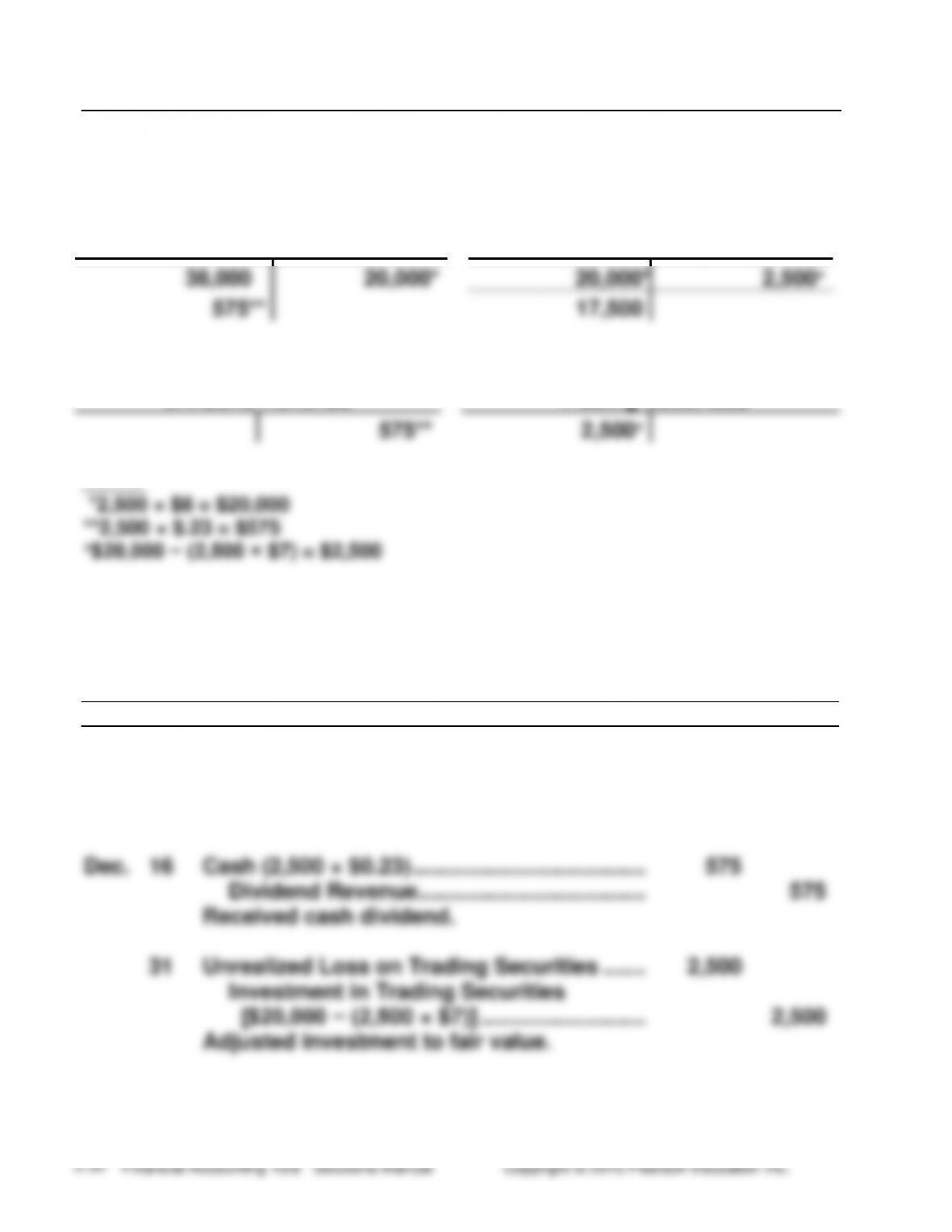

(20-30 min.) P 5-48A

Reqs. 1 and 2

Cash

Investment in Trading Securities

38,000

20,000*

20,000*

2,500+

575**

17,500

Dividend Revenue

Unrealized Loss on

Trading Securities

575**

2,500+

_____

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Nov.

16

Investment in Trading Securities ……………..

20,000

Cash (2,500 × $8) …………………………………

20,000

Purchased investment.

Dec.

16

Cash (2,500 × $0.23) ………………………………..

575

Dividend Revenue ……………………………….

575

Received cash dividend.

31

Unrealized Loss on Trading Securities …….

2,500

Investment in Trading Securities

[$20,000 − (2,500 × $7)] ………………………

2,500

Adjusted investment to fair value.

(continued) P 5-48A

Req. 3

BALANCE SHEET

Req. 4

INCOME STATEMENT

Other revenue and (expense):

Req. 5

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2015

Jan.

14

Cash …………………………………………………….

19,850

Investment in Trading Securities ………..

17,500

Gain on Sale of Trading Securities ……..

2,350

Sold investment at a gain.

(continued) P 5-48A

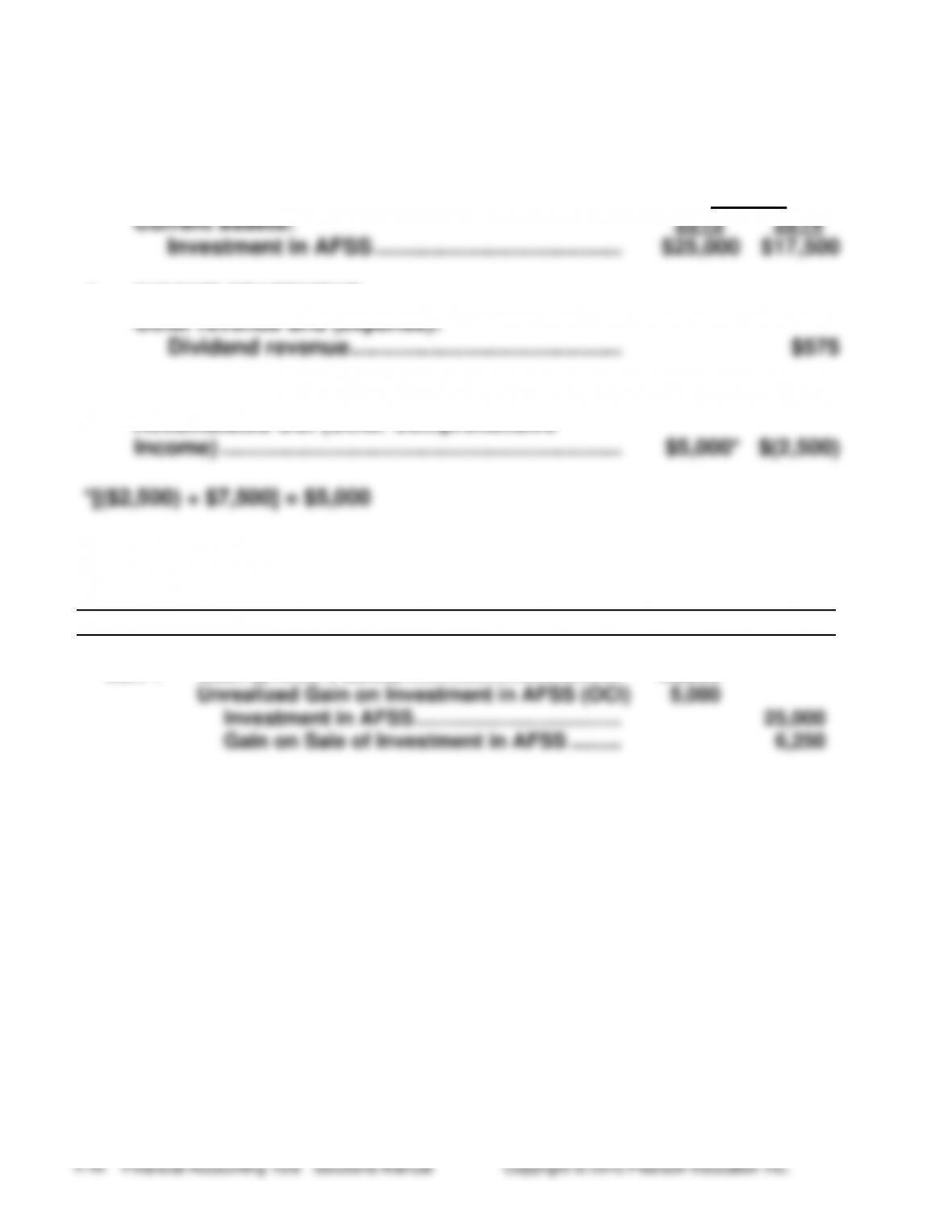

Req. 6

3.

BALANCE SHEET

Dec. 31

Current assets:

2015

2014

Investment in AFSS ………………………………….

$25,000

$17,500

4.

INCOME STATEMENT

Other revenue and (expense):

Dividend revenue ……………………………………..

$575

STOCKHOLDERS’ EQUITY

Accumulated OCI (Other Comprehensive

Income) ………………………………………………………..

$5,000*

$(2,500)

5. Sale of securities:

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2016

Jan. 1

Cash ($10.50 x 2,500) …………………………………

26,250

Unrealized Gain on Investment in AFSS (OCI)

5,000

Investment in AFSS ……………………………….

25,000

Gain on Sale of Investment in AFSS ………

6,250

(10-15 min.) P 5-49A

MEMORANDUM

DATE: _________________

TO: Management of Brierra Products, Inc.

FROM: Student Name

RE: Evaluation of internal control over cash receipts from

customers

By opening the mail, the accountant has direct access to cash. This

creates an internal control weakness because the accountant also posts

credits to customer accounts. She can steal a cash receipt from a

customer and write off the customer account as uncollectible. The theft

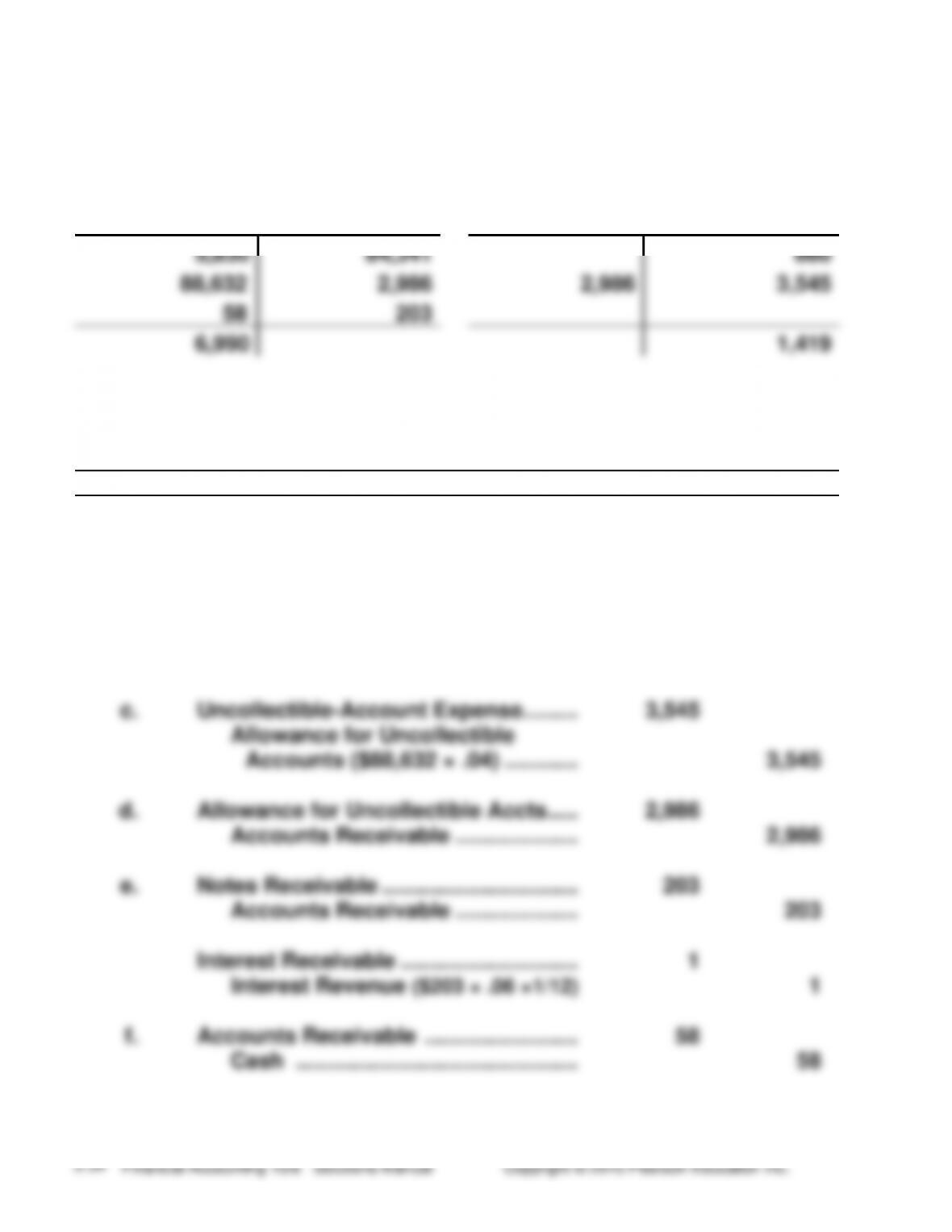

(15-20 min.) P 5-50A

(All amounts in millions)

Reqs. 1 and 3

Accounts Receivable

Allowance for Uncollectible Accts

5,830

84,341

860

88,632

58

2,986

203

2,986

3,545

6,990

1,419

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

a.

Cash ……………………………………………..

9,848

Accounts Receivable ……………………..

88,632

Service Revenue ……………………….

98,480

b.

Cash ……………………………………………..

84,341

Accounts Receivable ………………..

84,341

c.

Uncollectible-Account Expense ………

3,545

Allowance for Uncollectible

Accounts ($88,632 × .04) …………

3,545

d.

Allowance for Uncollectible Accts …..

2,986

Accounts Receivable ………………..

2,986

e.

Notes Receivable …………………………..

203

Accounts Receivable ………………..

203

Interest Receivable ………………………..

1

Interest Revenue ($203 × .06 ×1/12)

1

f.

Accounts Receivable …………………….

58

Cash ……………………………………….

58

(continued) P 5-50A

Req. 4

These balances agree with the actual Quick Mail amounts.

Req. 5

INCOME STATEMENT

Service revenue ………………………..

+ Interest revenue ……………………….

− Uncollectible-account expense …

$98,480

1

(3,545)

Net effect on net income ……………

$94,936

(25-35 min.) P 5-51A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Nov.

30

Allowance for Doubtful Accounts ………………………

3,900

Accounts Receivable — Proctor Carpets ……..

3,100

Accounts Receivable — Antiques on Austin …

800

Dec.

31

Doubtful-Account Expense ………………………………..

9,628

Allowance for Doubtful Accounts ………………..

9,628*

_____

1-30 31–60 61–90 Over 90 Total

days days days days balance

$259,000 $93,000 $39,000 $36,000

Req. 2

Allowance for Doubtful Accounts

Nov. 30 Write-offs

3,900

Sept. 30 Balance

15,100

Dec. 31 Adjusting

9,628

Dec. 31 Balance

20,828

(continued) P 5-51A

Req. 3

Asher Communications

Comparative Balance Sheets (Partial)

December 31, 2015 and December 31, 2014

2015

2014

Accounts receivable……………………………….

$427,000

$408,000

Less: Allowance for doubtful accounts………

(20,828)

(9,700)

Accounts receivable, net………………………..

$406,172

$398,300

(20-25 min.) P 5-52A

Req. 1

Cash ($21,000 − $9,000) ………………………………..

$12,000

Investment in trading securities …………………….

12,000

Accounts receivable …………………………………….

$29,000

Less: Allowance for uncollectible accts …….

(1,700)

27,300

Inventory ……………………………………………………..

28,000

Prepaid expenses …………………………..…………….

6,000

Total current assets ………………………………….

$85,300

Accounts payable …………………………………………

Other current liabilities …………………………………

$30,000

27,000

Total current liabilities ………………………………

$57,000

Req. 2

As reported

Corrected

Current

=

$98,000

=

1.72

$85,300

=

1.50

ratio

$57,000

$57,000

Quick

$21,000 + $14,000

$12,000 + $12,000

(acid-test)

=

+ $29,000

=

1.12

+ $27,300

=

0.90

ratio

$57,000

$57,000

(continued) P 5-52A

Req. 3

Net income, as reported ……………………………..

$46,000

Less: Unrealized loss on trading investments

($14,000 − $12,000) ………………………………..

(2,000)

Less: Correction for conversion to the

allowance method —

Correct uncollectible-account expense,

per aging method ………………………………

$1,700

Uncollectible-account expense as

reported using the direct write-off

method ……………………………………………..

(500)

(1,200)

Net income, as corrected …………………………...

$42,800

(20-30 min.) P 5-53A

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Oct.

31

Note Receivable — Stan’s Foods ……………..

24,000

Sales Revenue…………………………………….

24,000

Dec.

31

Interest Receivable

($24,000 × .06 × 2/12) ……………………………….

240

Interest Revenue …………………………………

240

2015

Jan.

31

Cash ………………………………………………………

24,360

Note Receivable — Stan’s Foods …………

24,000

Interest Receivable ……………………………..

240

Interest Revenue

($24,000 × .06 × 1/12) ……………………..

120

Feb.

18

Note Receivable — Dutton Market …………..

6,800

Accounts Receivable —

Dutton Market …………………………………..

6,800

19

Cash ………………………………………………………

6,600

Financing Expense …………………………………

200

Note Receivable — Dutton Market ……….

6,800

Nov.

11

Note Receivable — Kosher Foods Co. ……..

15,000

Cash …………………………………………………..

15,000

Dec.

31

Interest Receivable …………………………………

98

Interest Revenue

($15,000 × .0475 × 50/365) ……………….

98