Chapter 13

Financial Statement Analysis

Short Exercises

(5-10 min.) S 13-1

Increase (Decrease)

(Dollars in thousands)

2014

2013

2014

2013

2012

Amount

Percent

Amount

Percent

Revenues

$20,289

$20,045

$18,449

$244

1.2%

$1,596

8.7%

Expenses

10,915

10,338

10,100

Net income

$ 9,374

$ 9,707

$ 8,349

$(333)

(3.4)%

$1,358

16.3%

(5-10 min.) S 13-2

Trend percentages:

2014

2013

2012

2011

Sales ……………….

118%

110%

105%

100%

Net income ………

155%

116%

111%

100%

(10-15 min.) S 13–3

2014

2013

2012

Amount

Percent

Amount

Percent

Amount

Percent

Cash

$ 19,200

3.3%

$ 13,600

2.6%

$ 11,340

2.4%

Receivables, net

34,700

6.0

20,800

4.0

23,900

5.1

Inventory

266,800

46.3

197,600

38.2

148,180

31.2

Prepaid expenses

34,900

6.1

41,600

8.0

33,460

7.0

Property, plant, and

equipment, net

220,400

38.3

244,400

47.2

258,120

54.3

Total assets

$576,000

100.0%

$518,000

100.0%

$475,000

100.0%

Inventory, as a percent of total assets, has grown dramatically. Property,

plant and equipment appears to be wearing out and is not being

replaced due to the growth in inventory which has led to a tight cash

position.

(10 min.) S 13-4

Kraft

Claire

(Amounts in millions)

Amount

Percent

Amount

Percent

Net sales

$18,700

100.0%

$7,869

100.0%

Cost of goods sold

10,573

56.5

4,965

63.1

Selling and administrative

expenses

4,895

26.2

1,521

19.3

Interest expense

53

0.3

23

0.3

Other expense

89

0.5

38

0.5

Income tax expense

730

3.9

250

3.2

Net income

$ 2,360

12.6%

$1,072

13.6%

Kraft earned more net income, but Claire’s net income was a higher

percentage of net sales. Students can argue that Kraft is more profitable

because it earns more net income than Claire. Students could also

argue that Claire is more profitable because it earns a higher percentage

of profit on each dollar of sales than Kraft does.

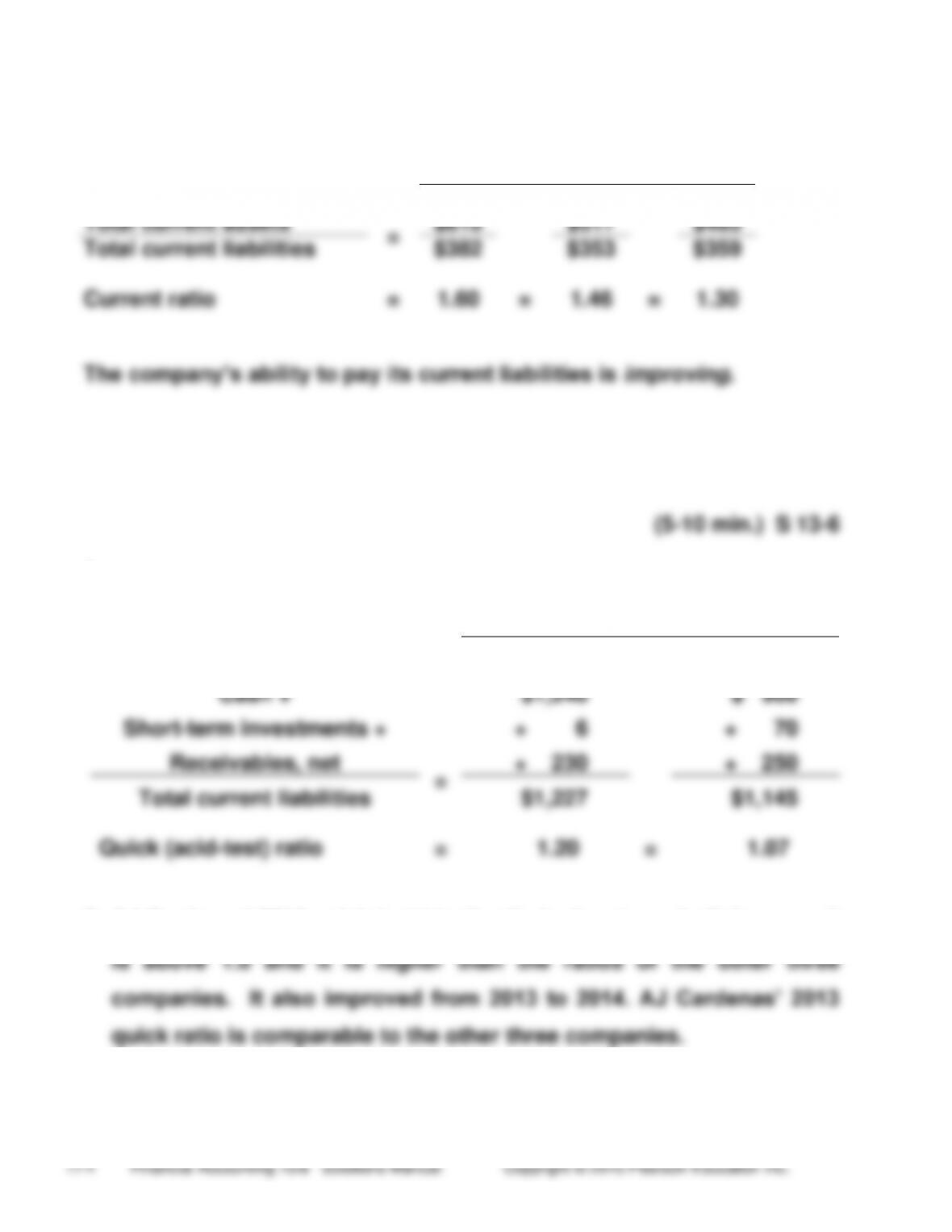

(5-10 min.) S 13-5

2014

2013

2012

Total current assets

=

$610

$517

$465

Total current liabilities

$382

$353

$359

Current ratio

=

1.60

=

1.46

=

1.30

The company’s ability to pay its current liabilities is improving.

(5-10 min.) S 13-6

1.

(Dollar amounts in millions)

2014

2013

Cash +

$1,240

$ 900

Short-term investments +

+ 6

+ 70

Receivables, net

=

+ 230

+ 250

Total current liabilities

$1,227

$1,145

Quick (acid-test) ratio

=

1.20

=

1.07

2. AJ Cardenas’ 2014 quick (acid-test) ratio looks strong both because it

(10-15 min.) S 13–7

(Dollar amounts in millions)

a.

Inventory turnover

=

Cost of goods sold

=

$2,639

Average inventory

($96 + $81) / 2

=

$2,639

=

29.7 times

$89

Days’ inventory

=

365

=

365

=

12 days

outstanding (DIO)

Inventory turnover

29.7

b.

Days’ sales outstanding (DSO):

One day’s

=

$9,840

=

$27.0

sales

365

Average net

Days’ sales

=

receivables

=

$240*

=

9 days

outstanding (DSO)

One day’s

$27.0

sales

____

*($230 + $250) / 2 = $240

c. Days’ payables outstanding:

Accounts payable

=

Cost of goods sold

=

$2,639

=

2.8 times

turnover

Average accounts

payable

($1,000 + $900) / 2

Days’ payables

=

365

=

365

=

130 days

outstanding (DPO)

Accounts payable

turnover

2.8

(continued) S 13-7

d. Cash conversion cycle (in days):

Cash conversion

=

DIO + DSO – DPO

=

12 + 9 – 130

=

– 109

cycle

Inventory turnover and DSO look strong. Turning over inventory about

30 times per year (every 12 days) is fast, and collecting average

receivables in only 9 days is also very fast. However, the company is

taking 130 days to pay off its accounts payable. This is quite slow,

(5-10 min.) S 13-8

(Dollar amounts in millions)

1.

Debt ratio

=

Total liabilities

=

$5,844

=

0.804

Total assets

$7,265

2.

Times-interest-

=

Income from operations

=

$1,230 + $184

=

7.7

earned ratio

Interest expense

$184

3. The debt ratio is high. The ability to pay off debt is weak. The

times-interest-earned ratio is high. The ability to pay interest

(10 min.) S 13-9

(Dollar amounts in millions)

a.

Rate of return on sales

=

Net income

=

$845

=

8.59%

Net sales

$9,840

Asset turnover

=

Net sales

=

$9,840

=

1.42 times

b.

Average

total assets

($7,265 + $6,640) / 2

c.

Rate of return

Rate of return

on sales

x

Asset

turnover

on total assets

=

8.59%

x

1.42

(ROA)

=

12.2%

Leverage ratio

=

Average total assets

=

($7,265 + $6,640) / 2

=

4.74

d.

Average common

stockholders’ equity

($1,421 + $1,515) / 2

e.

Rate of return

Net Preferred

on common

=

income − dividends

=

$845 − $0

=

57.6%*

stockholders’

Average common

$1,468

equity

stockholders’ equity

= ROA x Leverage ratio

= 12.2% x 4.74 = 57.8%*

f.

These rates of return are strong.

*Slight difference due to rounding.

(5-10 min.) S 13–10

(Amounts, except per-share amounts, in millions)

1.

EPS

=

Net income − Preferred dividends

Number of shares of common

=

$620 − $21*

700

stock outstanding

=

$.86

Market price per share

of common stock

Price/earnings

ratio

=

=

$11.83

=

13.76

EPS

$.86

2.

The stock market says that $1 of Redd Cars’ net income is

worth $13.76.

(10 min.) S 13–11

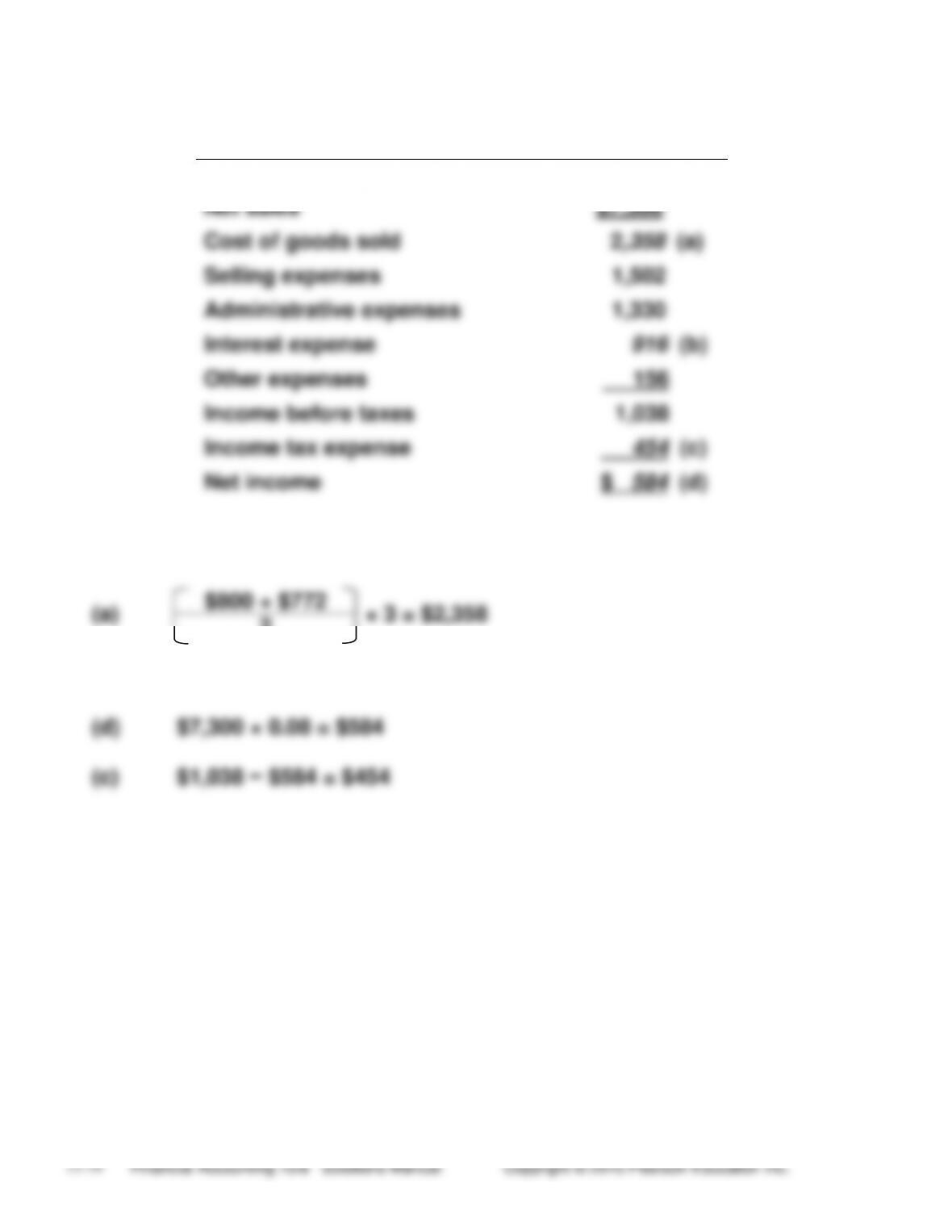

Income Statement

Thousands

Net sales

$7,300

Cost of goods sold

2,358 (a)

Selling expenses

1,502

Administrative expenses

1,330

Interest expense

916 (b)

Other expenses

156

Income before taxes

1,038

Income tax expense

454 (c)

Net income

$ 584 (d)

(a)

$800 + $772

× 3 = $2,358

2

(b)

$7,300 − $2,358 − $1,502 − $1,330 − $156 − $1,038 = $916

(d)

$7,300 × 0.08 = $584

(c)

$1,038 − $584 = $454

(15-20 min.) S 13–12

Balance Sheet

(Dollars in thousands)

Cash

$ 260

Total current liabilities

$2,100

Receivables

706 (a)

Long-term debt

816 (e)

Inventories

1,374

Other long-term

Prepaid expenses

180 (b)

liabilities

920

Total current assets

2,520 (c)

Common stock

200

Plant assets, net

1,955 (d)

Retained earnings

2,814

Other assets

2,375

Total liabilities and

Total assets

$6,850

equity

$6,850 (f)

(f)

=

$6,850 (same as total assets)

(e)

=

$6,850 × 0.56 = $3,836

$3,836 − $2,100 − $920 = $816

Or

$6,850 − $2,814 − $200 − $920 − $2,100 = $816

(c)

=

$2,100 × 1.20 = $2,520

(a)

=

$2,100 × 0.46 = $966; $966 − $260 = $706

(b)

=

$2,520 − $260 − $706 − $1,374 = $180

(d)

=

$6,850 − $2,520 − $2,375 = $1,955

(15-20 min.) S 13–13

TO: Cole Binder Investment Committee

FROM: Student Name

SUBJECT: Investment Recommendation

I recommend that we invest in Tower.org for the following reasons:

1. Tower.org’s. return on equity (ROE) is 5% higher than Graphics

Imaging’s. An investment in Tower.org should therefore produce a

higher return than an investment in Graphics Imaging’s stock.

2. Tower.org’s ROE exceeds its return on assets by a wider margin than

(10 min.) S 13-14

(Dollars in thousands)

EVA®

=

Net

+

Interest

−

Capital

income

expense

charge

=

$761

+

$401

−

$145*

=

$1,017

_____

*Capital

=

Long-term

+

Stockholders’

×

Cost of

charge

debt

equity

capital

=

($620

+

$3,010)

×

.04

=

$145*

The stockholders should be pleased with the EVA® that Schaeffer

Software delivered because it is positive, which meant value was

added.

Exercises

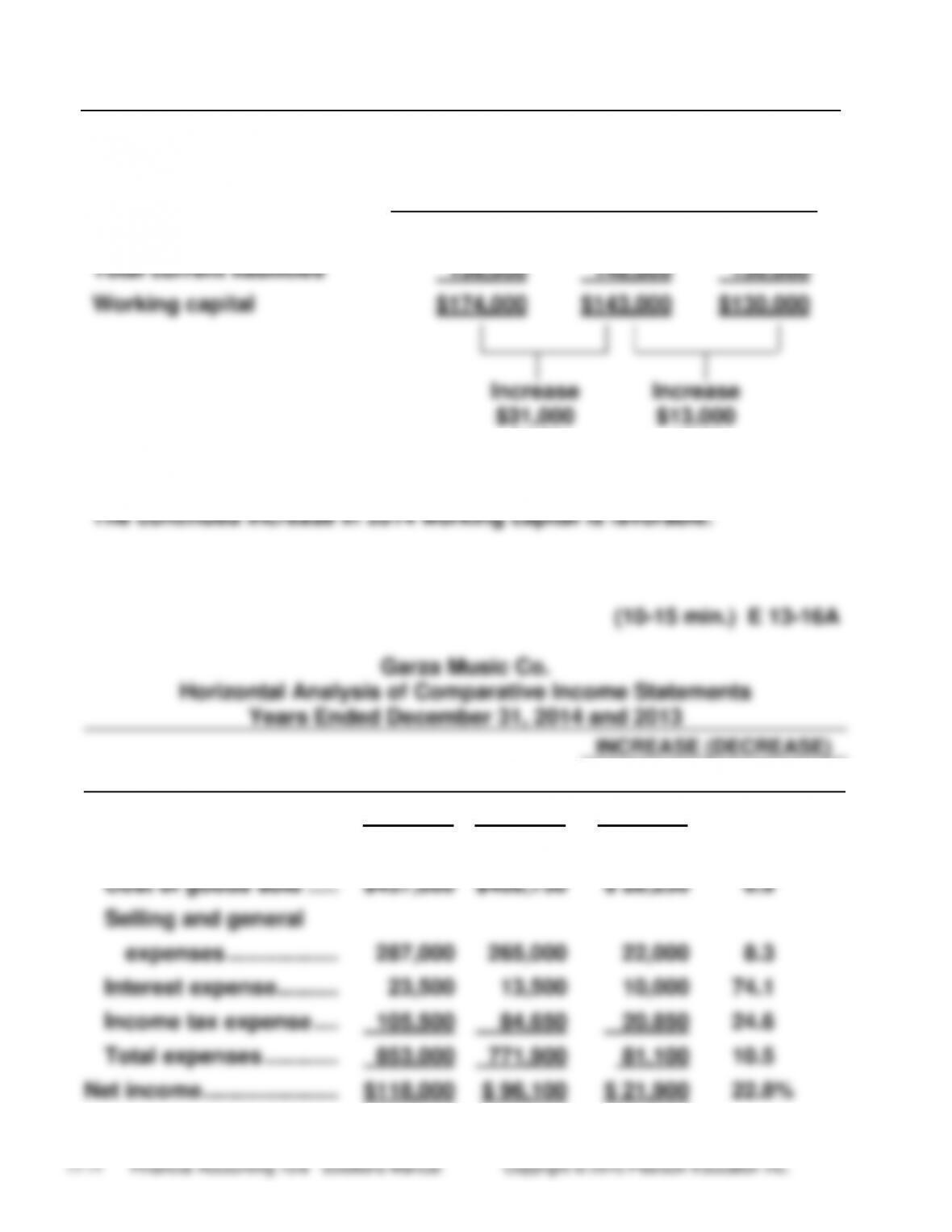

(5-15 min.) E 13-15A

2014

2013

2012

Total current assets

$330,000

$291,000

$260,000

Total current liabilities

156,000

148,000

130,000

Working capital

$174,000

$143,000

$130,000

Increase

Increase

$31,000

$13,000

21.7%

10.0%

The continued increase in 2014 working capital is favorable.

11.9%

23,500

24.6

(5-10 min.) E 13-17A

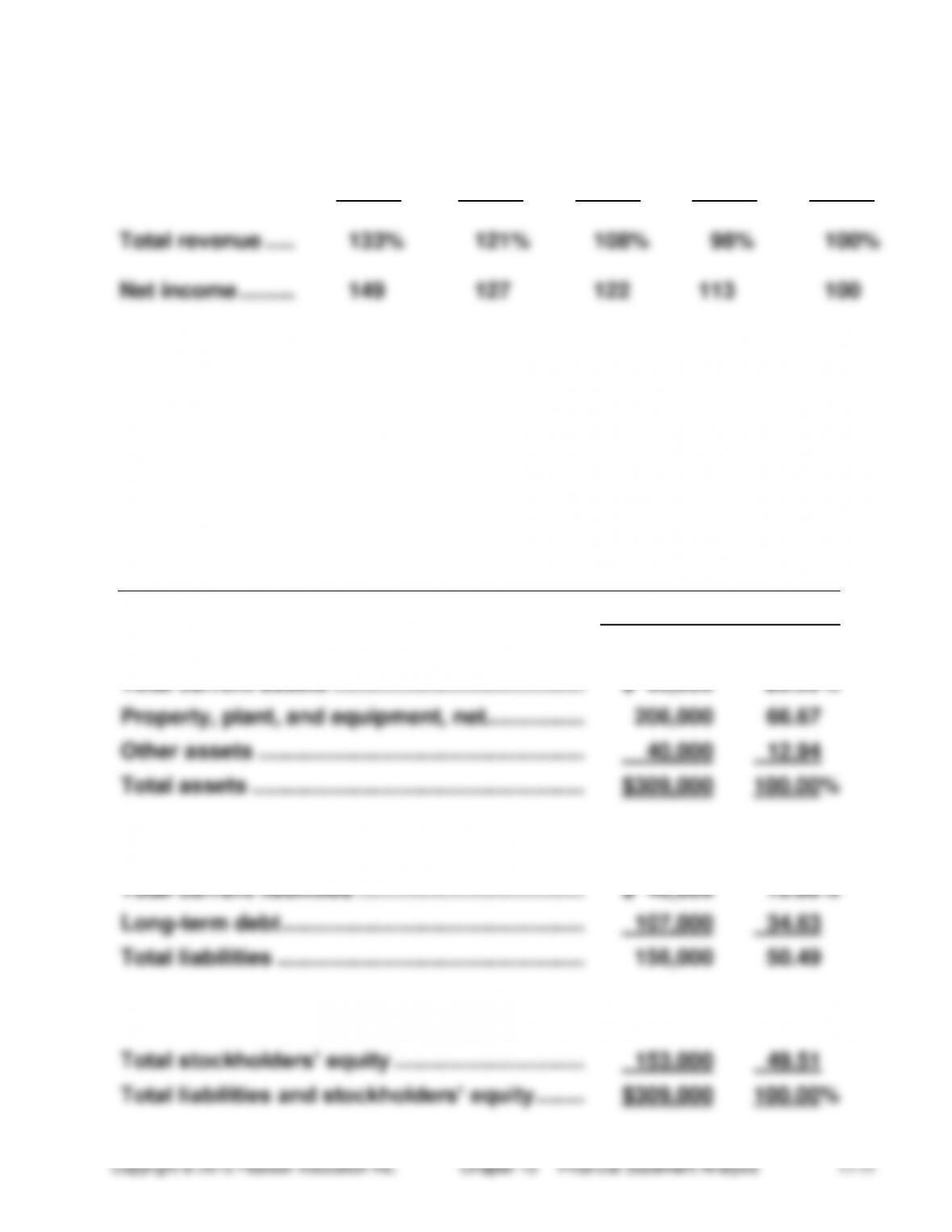

Trend percentages:

Year 4

Year 3

Year 2

Year 1

Year 0

Total revenue …..

133%

121%

108%

98%

100%

Net income ………

149

127

122

113

100

Net income grew by 49% during the period, compared to 33% for total

revenue.

(10-15 min.) E 13-18A

Patterson Golf Company

Vertical Analysis of Balance Sheet

December 31, 2014

AMOUNT

PERCENT

ASSETS

Total current assets …………………………………..

$ 63,000

20.39%

Property, plant, and equipment, net …………….

206,000

66.67

Other assets ……………………………………………..

40,000

12.94

Total assets ………………………………………………

$309,000

100.00%

LIABILITIES

Total current liabilities ……………………………….

$ 49,000

15.86%

Long-term debt ………………………………………….

107,000

34.63

Total liabilities …………………………………………..

156,000

50.49

STOCKHOLDERS’ EQUITY

Total stockholders’ equity ………………………….

153,000

49.51

Total liabilities and stockholders’ equity ……..

$309,000

100.00%

(10-15 min.) E 13-19A

Garza Music Co.

Comparative Common-Size Income Statements

Years Ended December 31, 2014 and 2013

2014

2013

Total revenue ……………………………………………………

100.00%

100.00%

Expenses:

Cost of goods sold ……………………………………….

45.00

47.09

Selling and general expenses ………………………..

29.56

30.53

Interest expense …………………………………………..

2.42

1.56

Income tax expense ………………………………………

10.87

9.75

Total expenses ……………………………………………..

87.85

88.93

Net income ……………………………………………………….

12.15%

11.07%

(10-15 min.) E 13-20A

1. Operations provided very little cash. The company is selling fixed

assets to generate cash.

(10-15 min.) E 13-21A

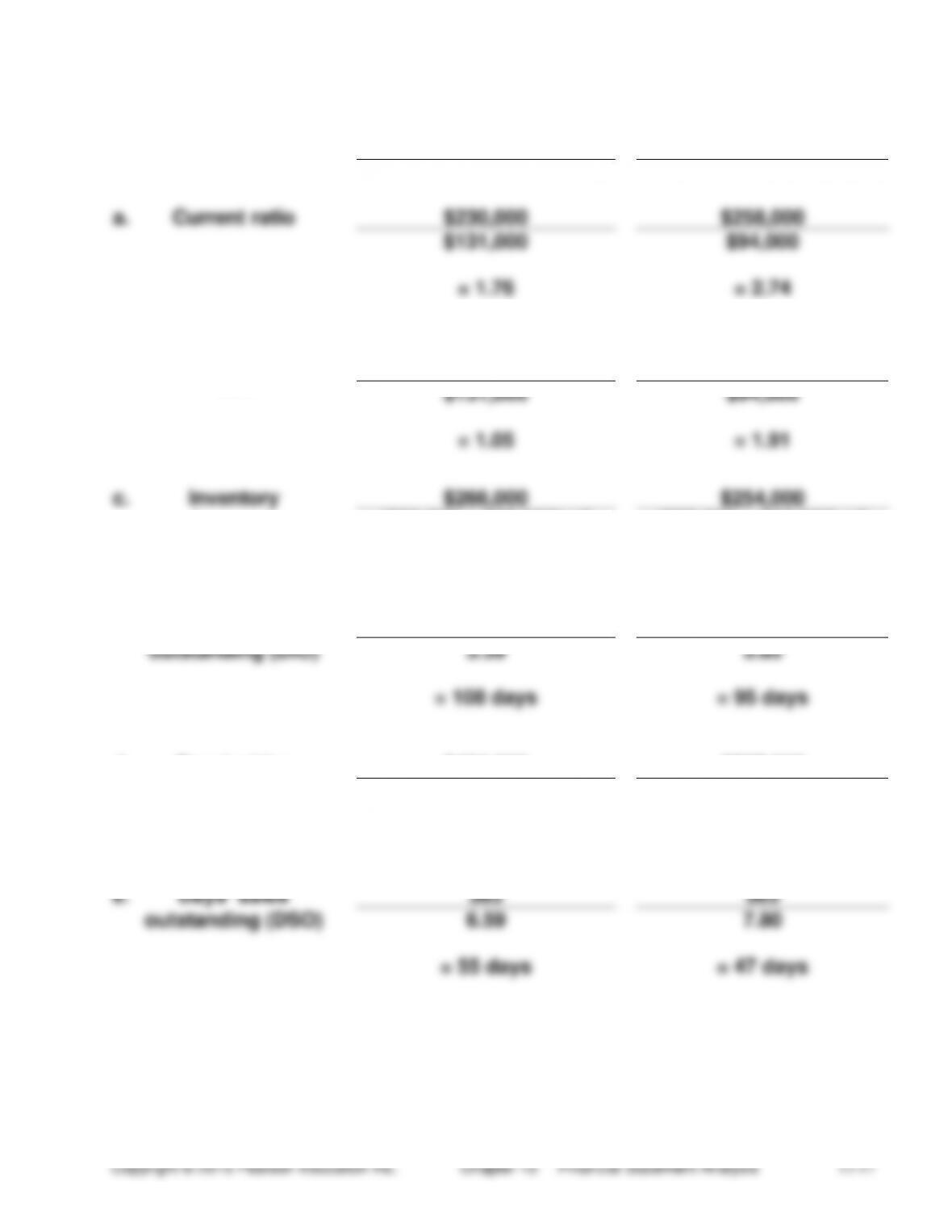

Req. 1

Current Year

Prior Year

a.

Current ratio

$230,000

$258,000

$131,000

$94,000

= 1.76

= 2.74

b.

Quick (acid-test)

ratio

$48,000 + $17,000 +

$72,000

$84,000+ $21,000 +

$75,000

$131,000

$94,000

= 1.05

= 1.91

c.

Inventory

$266,000

$254,000

turnover

($85,000 + $72,000) / 2

($72,000 + $60,000) / 2

= 3.39

= 3.85

Days’ inventory

365

365

outstanding (DIO)

3.39

3.85

= 108 days

= 95 days

d.

Receivables

$484,000

$507,000

turnover

($72,000 + $75,000) / 2

($75,000 + $55,000) / 2

= 6.59

= 7.80

e.

Days’ sales

365

365

outstanding (DSO)

6.59

7.80

= 55 days

= 47 days

(continued) E 13-21A

f.

Payables

$266,000

$254,000

turnover

($75,000 + $65,000) / 2

($65,000 + $50,000) / 2

= 3.80

= 4.42

Days’ payables

365

365

outstanding (DPO)

3.80

4.42

= 96 days

= 83 days

g.

Cash conversion

108 + 55 – 96

95 + 47 – 83

cycle ( DIO + DSO

– DPO)

= 67 days

= 59 days

Req. 2

a. deteriorated

b. deteriorated

Req. 3

(15-20 min.) E 13-22A

a. Working capital (Current assets – Current liabilities)

2014:

$451,000* – $224,000 = $227,000

2013:

$473,000* – $262,000 = $211,000

b. Current ratio (Current assets ÷ Current liabilities)

(10-15 min.) E 13-23A

a. Return on net sales: