Chapter 5

Short-Term Investments & Receivables

Short Exercises

(5 min.) S 5-1

1. Trading securities are reported at their current market value (fair

value).

2. A trading security is always a current asset because the investor

intends to sell the trading investment in the very near future — days,

(10 min.) S 5-2

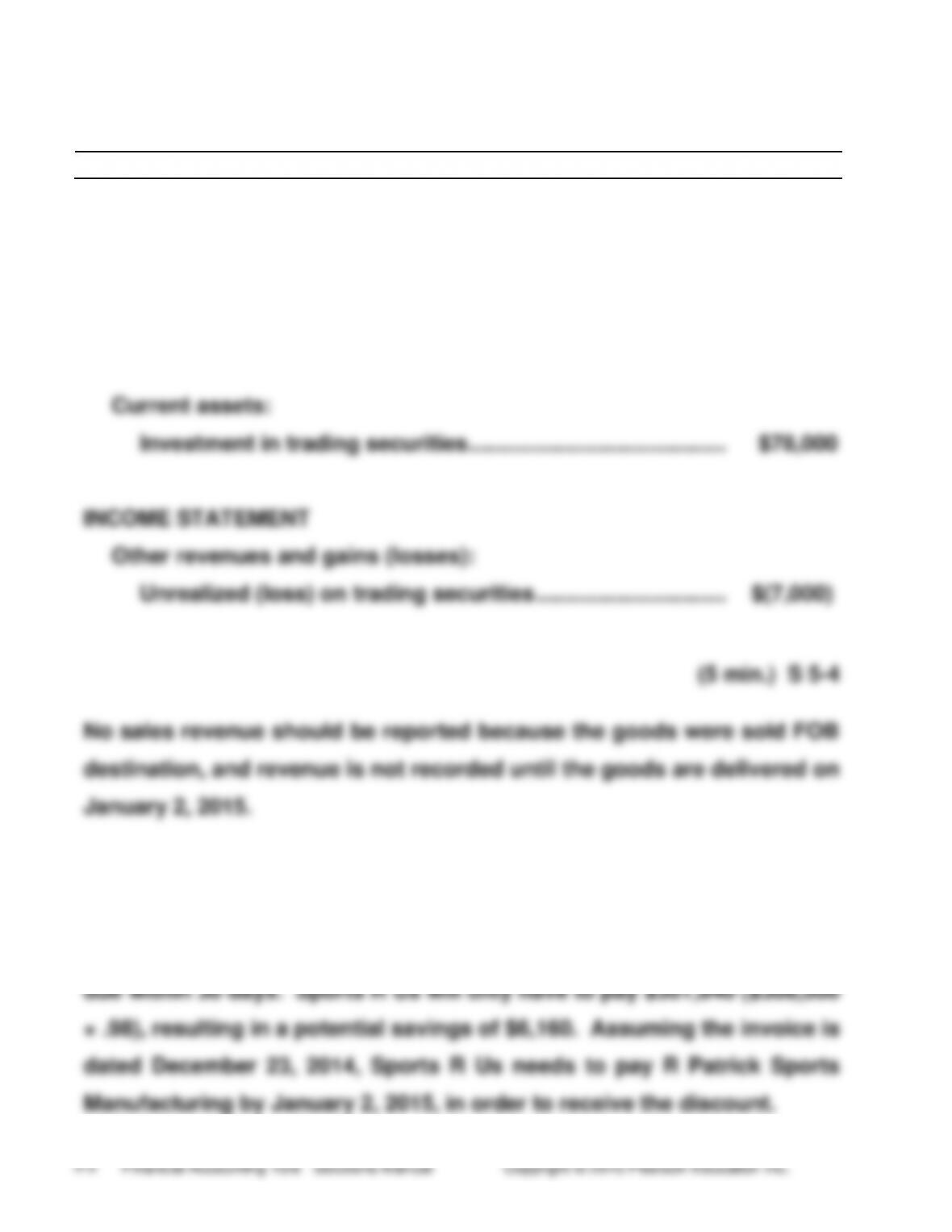

BALANCE SHEET

Current assets:

Investment in trading securities ……………………………….

$172,000

INCOME STATEMENT

Other revenue and gains (losses):

Unrealized gain on trading securities ……………………….

$12,000*

_____

*$172,000 − $160,000 = $12,000

(10 min.) S 5-3

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Unrealized Loss on Trading Securities

($85,000 − $78,000) ……………………………………

7,000

Investment in Trading Securities ………..

7,000

Adjusted investment to market value.

BALANCE SHEET

Current assets:

Investment in trading securities ……………………………………

$78,000

INCOME STATEMENT

Other revenues and gains (losses):

Unrealized (loss) on trading securities ………………………….

$(7,000)

(5 min.) S 5-4

No sales revenue should be reported because the goods were sold FOB

destination, and revenue is not recorded until the goods are delivered on

January 2, 2015.

(5 min.) S 5-5

2/10, n/30 means that Sports R Us will get a 2% discount if they pay the

invoice within 10 days of the invoice date; otherwise, the full amount is

(5 min.) S 5-6

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Sales Returns and Allowances …………………

6,100

Accounts Receivable ………………………..

6,100

(5-10 min.) S 5-7

MEMORANDUM

DATE:

TO: Spencer Crew

FROM: Student Name

RE: Essential element of internal control over collection from

customers

Separation of duties is the essential element in a system to ensure that

cash received by mail from customers is properly handled and

(5 min.) S 5-8

1.

Uncollectible-Account Expense ($483,000 × .02) …

9,660

Allowance for Uncollectible Accounts …………..

9,660

2.

Balance sheet

Accounts receivable …………………………………….

$49,000

Less: Allowance for uncollectible accounts …..

(9,660)

Accounts receivable, net ………………………………

$39,340

(10 min.) S 5-9

1. and 2.

Accounts Receivable

Beg. bal.

303,000

Net credit sales

1,978,000

Collections

2,010,000

Write-offs

29,000

End. bal.

242,000

Allowance for Uncollectible Accounts

Beg. bal.

26,000

Write-offs

29,000

Uncollectible –

account expense

35,000

End. bal.

32,000

3.

BALANCE SHEET

Accounts receivable …………………………………………….

$242,000

Less Allowance for uncollectible accounts ……………

(32,000)

Accounts receivable, net ………………………………………

$210,000

(10 min.) S 5-10

1. True

2. False. Credit terms are usually stated in this form: 2/10 n/30.

4.

5.

Sales revenue

Less: Sales returns and allowances

Less: Sales discounts

= Net sales revenue

Accounts receivable…………………….

$XXX

(X)

(X)

$ XX

$XXX

Less: Allowance for uncollectibles……

(X)

Accounts receivable, net……………….

$ XX

6. False. The direct write-off method overstates assets because it fails

to show the amount of the receivables the company actually expects

to collect.

(10 min.) S 5-11

1. Interest for:

2014

($220,000 × .05 × 7/12) ………………………

$ 6,417

2015

($220,000 × .05) ……………………………….

11,000

2016

($220,000 × .05 × 5/12) ………………………

4,583

3. Payoff at November 30, 2014:

Principal ……………………………………………………

$220,000

Interest ($220,000 × .05 × 6/12) …………………….

5,500

Total ………………………………………………………….

$225,500

(10 min.) S 5-12

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

a.

Aug. 31

Note Receivable — N. Herrera ………………….

5,000

Cash ………………………………………………..

5,000

To loan money.

2015

b.

June 30

Interest Receivable ($5,000 × .06 × 10/12) ….

250

Interest Revenue ………………………………

250

To accrue interest revenue.

2015

c.

Aug. 31

Cash ($5,000 + $300) ……………………………….

5,300

Interest Receivable …………………………..

250

Interest Revenue ($5,000 × .06 × 2/12) ..

50

Note Receivable ……………………………….

5,000

To collect on note receivable.

(10 min.) S 5-13

Req. 1

Cash + Short-term investments

$18,600 + $27,500

Acid-test

ratio

=

+ Net current receivables

=

+ $146,800

Total current liabilities

$203,000

=

.95

The company’s acid-test ratio compares favorably to the industry

average of 0.92.

Req. 2

One day’s sales

=

$1,593,000

=

$4,364

365

Days’ sales in

receivables

Average net

=

accounts receivable

=

($146,800 + $141,800) / 2

One day’s sales

$4,364

=

33 days

Exercises

(10-15 min.) E 5-14A

Req. 1

This is a trading investment because Western Corporation

intends to sell the stock within a short time.

Req. 2

Dec. 15

Investment in Trading Securities

(1,240 × $57) ……………………………………

70,680

Cash ……………………………………………

70,680

Purchased investment.

Dec. 31

Investment in Trading Securities

[(1,240 × $58) − $70,680] …………………..

1,240

Unrealized Gain on Trading

Securities ………………………………….

1,240

Adjusted investment to market value.

Req. 3

BALANCE SHEET (partial)

Current assets:

Investment in trading securities ………………………….

$71,920

INCOME STATEMENT (partial)

Other revenue and gains:

Unrealized gain on trading securities …………………..

$ 1,240

Copyright © 2015 Pearson Education Inc. Chapter 5 Short Term Investments & Receivables

5-9

(continued) E 5-14A

Req. 4

1. This is an available-for-sale security because it is not a trading

security.

2. Dec. 15 Investment in AFSS ……………………………. 70,680

Cash ……………………………………………… 70,680

3. BALANCE SHEET (partial)

Current assets:

Investment in AFSS ……………………………………………. $71,920

(15-20 min.) E 5-15A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

July 2

Accounts Receivable ………………………………

450

Sales Revenue ……………………………………

450

July 10

Accounts Receivable ………………………………

2,500

Sales Revenue ……………………………………

2,500

July 11

Cash ($450 − $9) ……………………………………..

441

Sales Discounts ($450 × 2%) ……………………

9

Accounts Receivable ………………………….

450

July 15

Sales Returns and Allowances ………………..

350

Accounts Receivable ………………………….

350

July 19

Cash ($2,150 − $43) …………………………………

2,107

Sales Discounts ($2,150 × 2%) …………………

43

Accounts Receivable ($2,500 − $350) …..

2,150

Req. 2

Sales revenue ($450 + $2,500) $2,950

(15-20 min) E5-16A

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2014

Dec.

31

Doubtful-Account Expense ($608,000 × .01) …

6,080

Allowance for Doubtful Accounts …………..

6,080

BALANCE SHEET

Current assets:

Accounts receivable, net of allowance

for doubtful accounts of $7,420* ………………………

$88,580**

_____

*$1,340 + $6,080 = $7,420

**$96,000 − $7,420 = $88,580

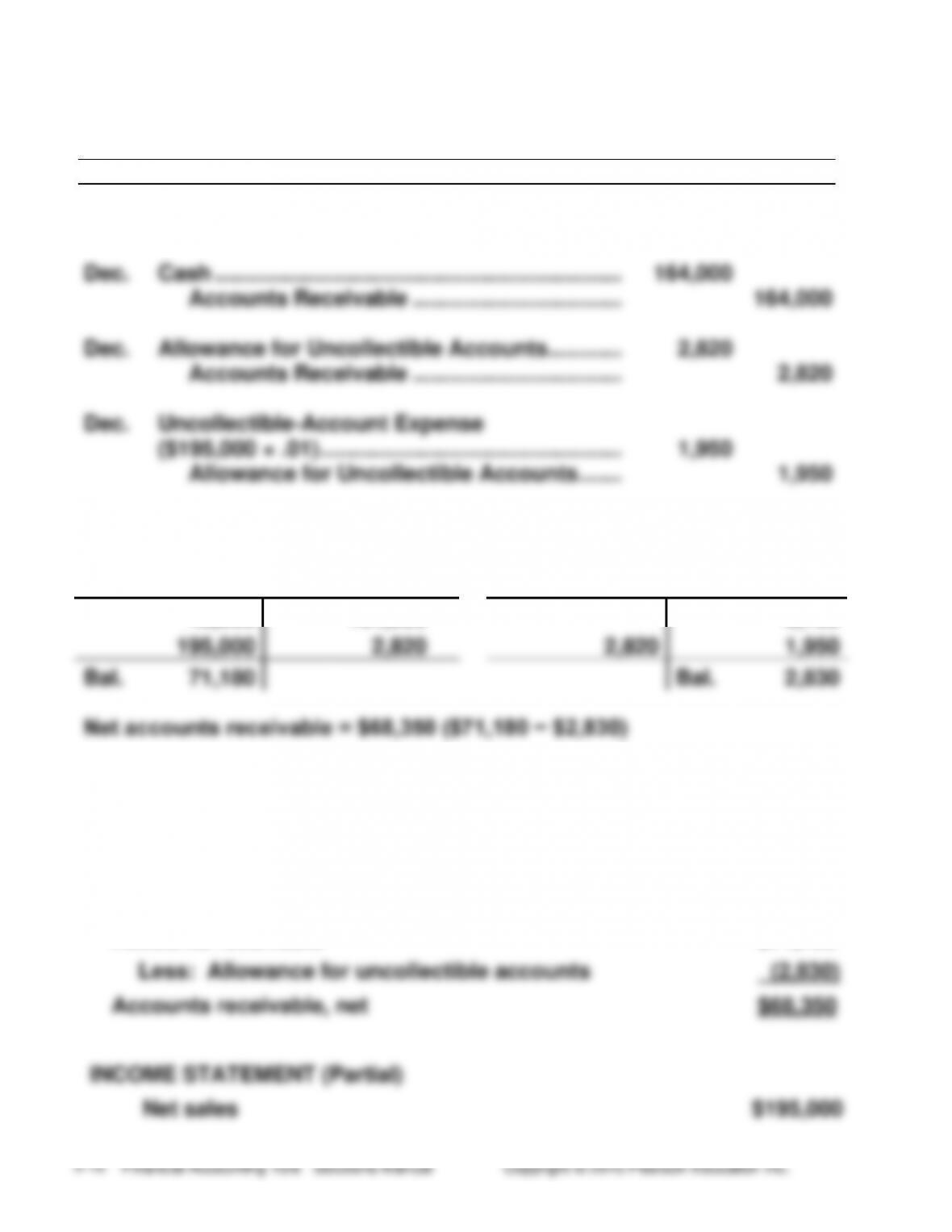

(15 min.) E 5-17A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Dec.

Accounts Receivable …………………………………

195,000

Sales Revenue ………………………………………

195,000

Dec.

Cash …………………………………………………………

164,000

Accounts Receivable …………………………....

164,000

Dec.

Allowance for Uncollectible Accounts…………

2,820

Accounts Receivable …………………………....

2,820

Dec.

Uncollectible-Account Expense

($195,000 × .01) ………………………………………….

1,950

Allowance for Uncollectible Accounts …….

1,950

Req. 2

Accounts Receivable

Allowance for

Uncollectible Accounts

43,000

164,000

3,700

195,000

2,820

2,820

1,950

Bal.

71,180

Bal.

2,830

Net accounts receivable = $68,350 ($71,180 − $2,830)

Windsor Party Planners expects to collect the net receivable amount.

Req. 3

BALANCE SHEET (Partial)

Current assets:

Accounts receivable

Less: Allowance for uncollectible accounts

$71,180

(2,830)

Accounts receivable, net

$68,350

IINCOME STATEMENT (Partial)

Net sales

$195,000

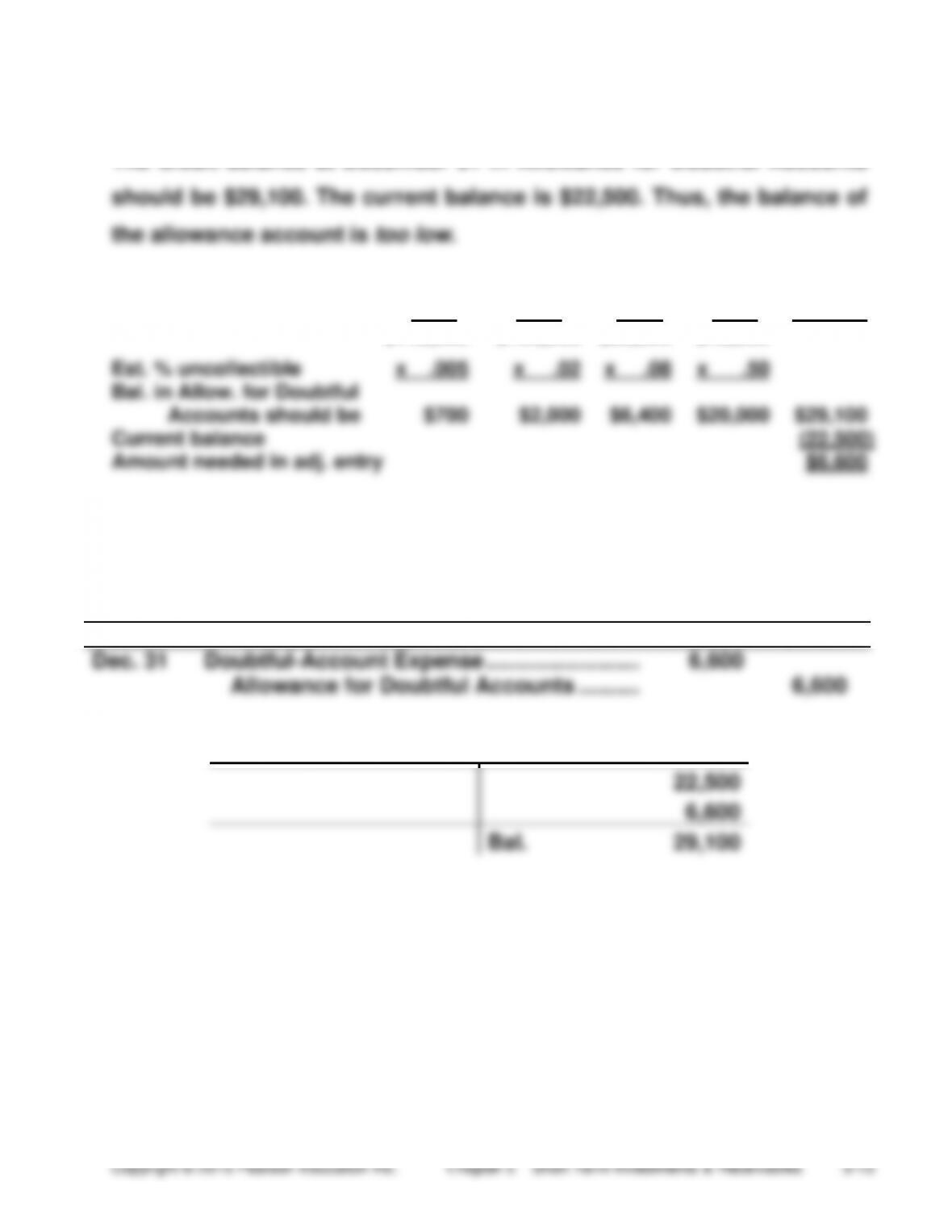

(15-30 min.) E 5-18A

Req. 1

The credit balance at December 31 in Allowance for Doubtful Accounts

1-30 31–60 61–90 Over 90 Total

days days days days balance

$140,000 $100,000 $80,000 $40,000

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Dec. 31

Doubtful-Account Expense …………………….

6,600

Allowance for Doubtful Accounts ……….

6,600

Allowance for Doubtful Accounts

22,500

6,600

Bal.

29,100

(continued) E 5-18A

Req. 3

BALANCE SHEET

Current assets:

Cash ………………………………………………………….

$ XX

Short-term investments ………………………………

XX

Accounts receivable, net of allowance

for doubtful accounts of $29,100 …………….

330,900*

Or

*Another way to report accounts receivable is

Accounts receivable …………………………………..

$360,000

Less: Allowance for doubtful accounts ……….

(29,100)

330,900

(15-20 min.) E 5-19A

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

May

Accounts Receivable ……………………………….

4,050

Service Revenue ………………………………….

4,050

Recorded revenue on account.

May

Bad-Debt Expense ($4,050 × .025) ……………..

101

Allowance for Bad Debts ………………………

101

Recorded expense for the month.

May

Sales Returns and Allowances ………………….

106

Accounts Receivable

106

Recorded sales returns from customers.

May

Allowance for Bad Debts ($33 + $53) …………

86

Accounts Receivable …………………………...

86

Wrote off uncollectible receivables.

(10-15 min.) E 5-20A

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Aug.

1

Note Receivable — Jill Waterman………..

5,000

Cash………………………………………..

5,000

Oct.

6

Note Receivable — King Properties……..

12,000

Service Revenue ………………………..

12,000

16

Note Receivable — Vernon, Inc.………….

2,000

Accounts Receivable – Vernon, Inc..…

2,000

31

Interest Receivable…………………………..

140*

Interest Revenue………………………….

140

_____

*($5,000 × .07 × 91/365) + ($12,000 × .06 × 25/365) + ($2,000 × .05 × 15/365)

$87** + $49** + $4** = $140

** Rounded to nearest dollar.

Harland Services earned interest revenue of $140 this year.

(10-15 min.) E 5-21A

Req. 1

Quick

Cash and Marketable Net current

(a)

(acid-test)

=

Cash equiv. + securities + receivables

ratio

Total current liabilities

=

$11,000 + $27,000 + $61,000

$20,000 + $112,000

=

$99,000

$132,000

=

0.75

A quick (acid-test) ratio of 0.75 is fairly weak.

(b)

One day’s

=

Sales revenue

=

$780,000

=

$2,137

sales

365

365

Days’ sales

Average net

in

=

accounts receivable

=

($61,000 + $75,000) / 2

receivables

One day’s sales

$2,137

=

32 days

Req. 2

Sutterfield could speed up cash flows from receivables by offering

discounts for early payments or increasing penalties for late payments.

(10-15 min.) E 5-22A

Req. 1

Average collection period:

Millions of dollars

One day’s sales

=

$750,000

=

$2,055

365

Days’ sales in receivables

=

($6,810 + $5,310) / 2

=

2.95 days

(average collection period)

$2,055

Req. 2

Jennings Co., Inc’s collection period is short because Jennings Co. sells

(10-15 min.) E 5-23B

Req. 1

This is a trading investment because Spring Corporation

intends to sell the stock within a short time.

Req. 2

Dec. 15

Investment in Trading Securities

(825 × $59) ………………………………………

48,675

Cash ……………………………………………

48,675

Purchased investment.

Dec. 31

Investment in Trading Securities

[(825 × $62) − $48,675] ……………………..

2,475

Unrealized Gain on Trading

Securities ………………………………….

2,475

Adjusted investment to market value.

Req. 3

BALANCE SHEET (Partial)

Current assets:

Investment in trading securities …………………………...

$51,150

INCOME STATEMENT (Partial)

Other revenue and gains:

Unrealized gain on trading securities …………………….

$ 2,475

(continued) E 5-23B

Req. 4

1. This is an available-for-sale security because it is not a trading

security.

2. Dec. 15 Investment in AFSS ……………………………. 48,675

Cash ……………………………………………… 48,675

INCOME STATEMENT (partial)

(nothing)

STATEMENT OF COMPREHENSIVE INCOME:

(15-20 min.) E 5-24B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Nov. 8

Accounts Receivable ……………………………….

650

Sales Revenue …………………………………….

650

Nov. 15

Accounts Receivable ……………………………….

1,800

Sales Revenue …………………………………….

1,800

Nov. 16

Sales Returns and Allowances …………………

500

Accounts Receivable …………………………..

500

Nov. 17

Cash ($650 − $13) …………………………………….

637

Sales Discounts ($650 × 2%) …………………….

Accounts Receivable …………………………..

13

650

Nov. 24

Cash ($1,300 − $26) ………………………………….

1,274

Sales Discounts ($1,300 × 2%) ………………….

26

Accounts Receivable ($1,800 − $500) ……

1,300

Req. 2

Sales revenue ($650 + $1,800) $2,450