(continued) P 9-82B

Req. 5

Leverage

ratio

Total assets ($7,265,000)

Total stockholders’ equity ($2,633,000)

=

2.76

Debt ratio

=

Total liabilities ($4,632,000)

=

0.64

Total assets ($7,265,000)

The leverage ratio and debt ratio would increase. The company would

be considered fairly healthy (average risk) from a leverage point of view.

Challenge Exercises and Problem

(10-15 min.) E 9-83

Current ratio

=

Total current assets

=

$324,500 – X

=

2.00

Total current liabilities

$173,800 – X

Let X = amount of current liabilities to pay in order to achieve a current

ratio of 2.00. Murphee Marketing Services should pay off $23,100* of

current liabilities. Then the current ratio will be:

=

=

2.00

(20-30 min.) P 9-84

Req. 1

a. Current ratio

2014

2013

Current

ratio

Current assets

$21,579

= 1.17

$17,551

1.28

Current liabilities

$18,508

$13,721

2014

2013

Debt

ratio

Total

liabilities

$72,921 – $31,317

=.571

$48,671 – $25,346

=.479

Total

assets

$72,921

$48,671

Req. 2

a. Current ratio

Current

ratio

Current assets

$21,579

= 1.07

Current liabilities

$18,508 + $1,590

b. Debt ratio

Current assets

$21,579

= 1.15

Decision Cases

(15-20 min.) Decision Case 1

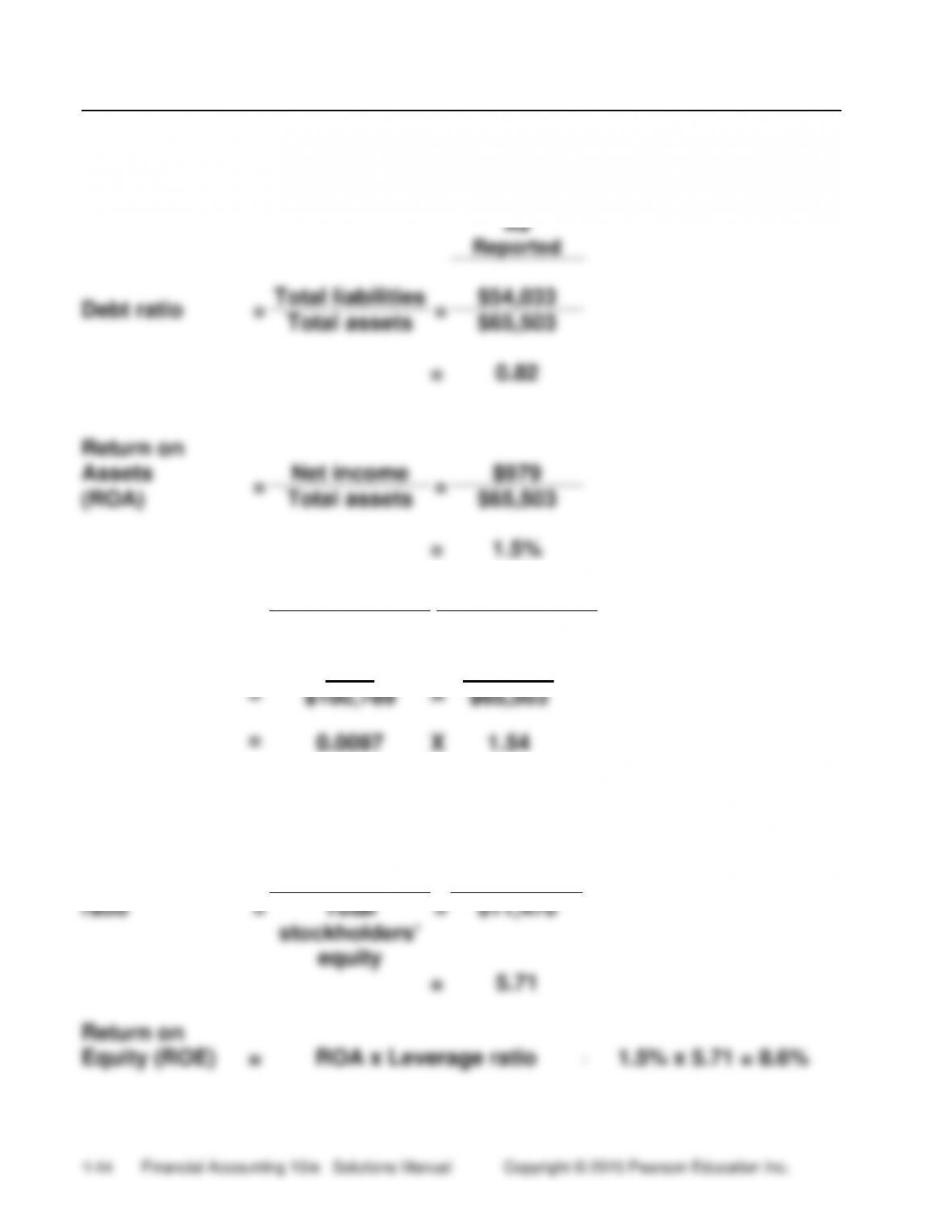

Req. 1

As

Reported

Debt ratio

=

Total liabilities

=

$54,033

Total assets

$65,503

=

0.82

Return on

Assets

=

Net income

=

$979

(ROA)

Total assets

$65,503

=

1.5%

Req.2

=

=

=

=

Net income

Revenue

$979

$100,789

0.0097

1.5%

X

X

X

Revenue

Total assets

$100,789

$65,503

1.54

Leverage

=

Total assets

=

$65,503

ratio

Total

stockholders’

$11,470

equity

=

5.71

Return on

Equity (ROE)

=

=

(continued) Decision Case 1

The ROE is greater than the ROA because the leverage ratio is

extremely high which magnifies the ROA. The debt ratio is also

extremely high and indicates that 82% of the assets were financed

with debt. The high leverage ratio and debt ratio should have made

investors question the soundness of Enron.

Req. 3

After Including the

Special-Purpose Entities

Debt ratio

=

Total liabilities

=

$54,033 + $6,900

Total assets

$65,503 + $500* – $600

= 0.93

*The SPEs originally reported assets of $7,000 million when those assets were

only worth $500 but actually had liabilities of $6,900.

Return on

assets

=

Net income

$979 – $300*

Total assets

$65,503 + $500 – $600

= 1.0%

*The SPEs’ income was nearly wiped out due to the restatement meaning that the

SPE did not earn a net income but had a loss, of which $300 applies to 2000; they

did have assets with a market value of $500.

LLeverage

L ratio

=

Total assets

$65,503 + $500 – $600

Total stock.

equity

($65,503 + $500 – $600) – ($54,033

+ $6,900)

= 14.63

(continued) Decision Case 1

As

After Including the

Reported

Special-Purpose Entities

Operating

Times-interest-

=

Income

=

$1,953

$1,953 + ($300)

earned ratio

Interest

$838

$838 + ($6,900 × .10)

expense

=

2.3 times

= 1.1 times

Req. 4

It appears that Enron excluded the special-purpose-entities (SPEs) from its

financial statements in order to hide their debt from Enron’s investors and

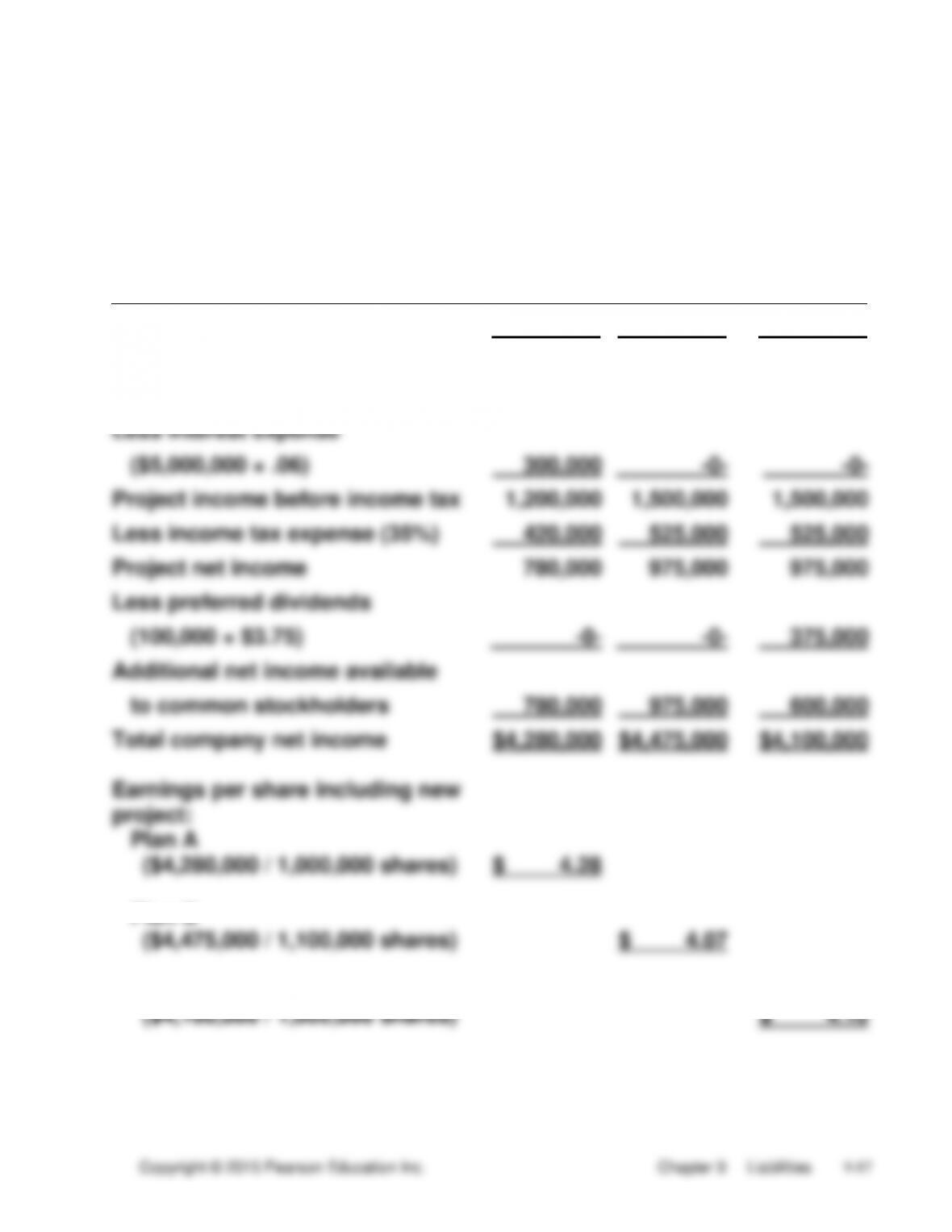

(30-40 min.) Decision Case 2

Req. 1 (Analysis of financing plans)

PLAN A

PLAN B

PLAN C

BORROW

AT 6%

ISSUE

COMMON

STOCK

ISSUE $3.75

NONVOTING

PREFERRED

STOCK

Net income before expansion

$3,500,000

$3,500,000

$3,500,000

Project income before interest

and income tax

$1,500,000

$1,500,000

$1,500,000

Less interest expense

($5,000,000 × .06)

300,000

-0-

-0-

Project income before income tax

1,200,000

1,500,000

1,500,000

Less income tax expense (35%)

420,000

525,000

525,000

Project net income

780,000

975,000

975,000

Less preferred dividends

(100,000 × $3.75)

-0-

-0-

375,000

Additional net income available

to common stockholders

780,000

975,000

600,000

Total company net income

$4,280,000

$4,475,000

$4,100,000

Earnings per share including new

project:

Plan A

($4,280,000 / 1,000,000 shares)

$ 4.28

Plan B

($4,475,000 / 1,100,000 shares)

$ 4.07

Plan C

($4,100,000 / 1,000,000 shares)

$ 4.10

(continued) Decision Case 2

Req. 2 (Recommendation)

The best choice appears to be Plan A — borrowing at 6% — because:

(1) Borrowing allows the family to maintain control of the

business;

Ethical Issue 1

Req. 1

Req. 2 and 3

The potential parties and economic consequences of the decision not to

disclose contingent liabilities are:

1. The bank and its shareholders: With misleading information, they

might extend additional funds to the borrower assuming a better ability

to pay back the funds than actually exists. A contingent liability creates

(continued) Ethical Issue 1

Req. 3 Legal and ethical consequences

Banks have legal requirements in loan agreements that require debtors

FASB and IASB about a new standard for reporting contingencies. It is

likely that, in the future, more losses resulting from lawsuits and other

contingencies are likely to be disclosed in the body and the footnotes of

financial statements.

Ethical Issue 2

1. The ethical issue is whether to structure this lease to avoid its having

4 years, it will be only 66 2/3 percent of the economic life of the asset (6

years). Thus, the lease will fail all of the mechanical tests for the lease

2. The stakeholders are Gocker, the lessee; Morgan, the lessor; and

Last National Bank, Gocker’s present creditor. The potential

consequences to the stakeholders are:

a. economic: If the lease is structured as a capital lease, Gocker

(continued) Ethical Issue 2

b. legal: If we assume that GAAP substitutes for legal requirements, if

3. Student responses will vary on this question. Some will say that, if

the rules allow it, then why not engineer the transaction in such as way

as to benefit Gocker by keeping the asset, and the lease obligation, off

the books. After all, this is perfectly legal, and perfectly in accordance