Archives

978-1259709685 Chapter 1 Lecture Note Part 1

Chapter 1 INTRODUCTION TO CORPORATE FINANCE SLIDES CHAPTER WEB SITES Section Web Address 1.1 www.cfo.com 1.4 www.business-ethics.com 1.6 www.protiviti.com/en-US/Documents/Surveys/2014-SOX- Compliance-Survey-Protiviti.pdf CHAPTER ORGANIZATION 1.1 What Is Corporate Finance? The Balance Sheet Model of the Firm The Financial Manager 1.2 The Corporate […]

978-1259709685 Chapter 1 Lecture Note Part 2

Slide 1.15 The Agency Problem A. Agency Relationships The relationship between stockholders and management is called the agency relationship. This occurs when one party (principal) hires another (agent) to act on their behalf. The possibility of conflicts of interest between […]

978-1259709685 Chapter 1 Solution Manual

CHAPTER 2 – 1 CHAPTER 1 INTRODUCTION TO CORPORATE FINANCE Answers to Concept Questions 1. In the corporate form of ownership, the shareholders are the owners of the firm. The shareholders elect the directors of the corporation, who in turn […]

978-1259709685 Chapter 10 Case

CHAPTER 10 CASE C-1 CHAPTER 10 A JOB AT EAST COAST YACHTS 1. The biggest advantage the mutual funds have is instant diversification. The mutual funds have a 3. The advantage of the actively managed fund is the possibility of […]

978-1259709685 Chapter 10 Lecture Note

Chapter 10 RISK AND RETURN: LESSONS FROM MARKET HISTORY SLIDES CHAPTER WEB SITES Section Web Address 10.1 finance.yahoo.com www.marketwatch.com/markets 10.2 bigcharts.marketwatch.com CHAPTER ORGANIZATION 10.1 Returns Dollar Returns Percentage Returns 10.2 Holding Period Returns 10.1 Key Concepts and Skills 10.2 Chapter […]

978-1259709685 Chapter 10 Solution Manual Part 1

CHAPTER 10 SOME LESSONS FROM CAPITAL MARKET HISTORY Answers to Concepts Review and Critical Thinking Questions 1. They all wish they had! Since they didn’t, it must have been the case that the stellar performance was 2. As in the […]

978-1259709685 Chapter 10 Solution Manual Part 2

CHAPTER 10 – 14. The return of any asset is the increase in price, plus any dividends or cash flows, all divided by the initial price. This preferred stock paid a dividend of $3.50, so the return for the year […]

978-1259709685 Chapter 11 Case

CHAPTER 11 CASE C-1 CHAPTER 11 A JOB AT EAST COAST YACHTS, PART 2 1. There should be little, if any, money allocated to the company stock. The principle of diversification indicates that an individual should hold a diversified portfolio. […]

978-1259709685 Chapter 11 Lecture Note Part 1

Chapter 11 RETURN AND RISK THE CAPITAL ASSET PRICING MODEL (CAPM) SLIDES 11.1 Key Concepts and Skills 11.2 Chapter Outline 11.3 Individual Securities 11.4 Expected Return, Variance, and Covariance 11.5 Expected Return 11.6 Expected Return 11.7 Variance 11.8 Variance 11.9 […]

978-1259709685 Chapter 11 Lecture Note Part 2

Slide 11.15 – Slide 11.16 Portfolios 11.4. The Efficient Set for Two Assets With two assets, you can form portfolios composed of different percentages of each asset. The possible portfolios are referred to as the opportunity set, and the set […]

978-1259709685 Chapter 11 Solution Manual Part 1

CHAPTER 11 RISK AND RETURN: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concepts Review and Critical Thinking Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety […]

978-1259709685 Chapter 11 Solution Manual Part 2

20. For a portfolio that is equally invested in large-company stocks and long-term bonds: 21. We know that the reward-to-risk ratios for all assets must be equal (See Question 19). This can be expressed as: [E(RA) – Rf] / A […]

978-1259709685 Chapter 11 Solution Manual Part 3

CHAPTER 11 – 31. First, we can calculate the standard deviation of the market portfolio using the Capital Market Line (CML). We know that the risk-free asset has a return of 4.3 percent and a standard deviation of zero and […]

978-1259709685 Chapter 12 Case

CHAPTER 12 CASE C-1 CHAPTER 12 THE FAMA-FRENCH MULTI-FACTOR MODEL AND MUTUAL FUND RETURNS NOTE: The example below shows the results for returns between October 2010 and September 2015. The actual answer to the case will change based on current […]

978-1259709685 Chapter 12 Lecture Note

Chapter 12 AN ALTERNATIVE VIEW OF RISK AND RETURN: THE ARBITRAGE PRICING THEORY SLIDES CHAPTER ORGANIZATION 12.1 Introduction 12.2 Systematic Risk and Betas 12.3 Portfolios and Factor Models Portfolios and Diversification 12.4 Betas, Arbitrage, and Expected Returns The Linear Relationship […]

978-1259709685 Chapter 12 Solution Manual Part 1

CHAPTER 12 AN ALTERNATIVE VIEW OF RISK AND RETURN: THE ARBITRAGE PRICING THEORY Answers to Concept Questions 1. Systematic risk is risk that cannot be diversified away through formation of a portfolio. Generally, systematic risk factors are those factors that […]

978-1259709685 Chapter 12 Solution Manual Part 2

CHAPTER 12 B- 8. To determine which investment an investor would prefer, you must compute the variance of portfolios created by many stocks from either market. Because you know that diversification is good, it is reasonable to assume that once […]

978-1259709685 Chapter 12 Solution Manual Part 2

CHAPTER 12 B- 8. To determine which investment an investor would prefer, you must compute the variance of portfolios created by many stocks from either market. Because you know that diversification is good, it is reasonable to assume that once […]

978-1259709685 Chapter 13 Case

CHAPTER 13 CASE C-1 CHAPTER 13 COST OF CAPITAL FOR SWAN MOTORS NOTE: The example below shows the results during November 2012. The actual answer to the case will change based on current market conditions. 1. The book value of […]

978-1259709685 Chapter 13 Lecture Note

Chapter 13 – Risk, Cost of Capital, and Valuation Chapter 13 RISK, COST OF CAPITAL, AND VALUATION SLIDES CHAPTER WEB SITES Section Web Address 13.10 finance.yahoo.com www.reuters.com 13-1 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution […]

978-1259709685 Chapter 13 Solution Manual Part 1

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 3. You are assuming that the new project’s risk is the same as the risk of the firm as a whole, and that […]

978-1259709685 Chapter 13 Solution Manual Part 2

CHAPTER 13 B- 18. The total cost of the equipment including flotation costs was: Using the equation to calculate the total cost including flotation costs, we get: Amount raised(1 – fT) = Amount needed after flotation costs $20,150,000(1 – fT) […]

978-1259709685 Chapter 14 Case

CHAPTER 14 CASE C-1 CHAPTER 14 YOUR 401k ACCOUNT AT EAST COAST YACHTS 1. Before the fact, you would expect that mutual funds managers would be able to outperform the market. This is due, in part, to the Darwinian nature […]

978-1259709685 Chapter 14 Lecture Note

Chapter 14 EFFICIENT CAPITAL MARKETS AND BEHAVIORAL CHALLENGES SLIDES CHAPTER ORGANIZATION 14.1 Key Concepts and Skills 14.2 Chapter Outline 14.3 Can Financing Decisions Create Value? 14.4 Creating Value through Financing 14.5 A Description of Efficient Capital Markets 14.6 Foundations of […]

978-1259709685 Chapter 14 Solution Manual

CHAPTER 14 B- CHAPTER 14 CORPORATE FINANCING DECISIONS AND EFFICIENT CAPITAL MARKETS Answers to Concepts Review and Critical Thinking Questions 1. To create value, firms should accept financing proposals with positive net present values. Firms can create valuable financing opportunities […]

978-1259709685 Chapter 15 Lecture Note Part 1

Chapter 15 LONG-TERM FINANCING: AN INTRODUCTION SLIDES CHAPTER WEB SITES Section Web Address 15.2 www.investinginbonds.com www.nasdbondinfo.com www.sifma.org www.sec.gov CHAPTER ORGANIZATION 15.1 Some Features of Common and Preferred Stocks Common Stock Features Preferred Stock Features 15.2 Corporate Long-Term Debt Is It […]

978-1259709685 Chapter 15 Lecture Note Part 2

Slide 15.7 Bond Classifications Slide 15.8 Required Yields Security – debt classified by collateral and mortgage Collateral – strictly speaking, pledged securities Mortgage securities – secured by mortgage on real property Debenture – an unsecured debt with 10 or more […]

978-1259709685 Chapter 15 Solution Manual

CHAPTER 15 B- CHAPTER 15 LONG-TERM FINANCING: AN INTRODUCTION Answers to Concepts Review and Critical Thinking Questions 1. The indenture is a legal contract and can run into 100 pages or more. Bond features which would be included are: the […]

978-1259709685 Chapter 16 Case

CHAPTER 16 C-1 CHAPTER 16 STEPHENSON REAL ESTATE RECAPITALIZATION 1. If Stephenson wishes to maximize the overall value of the firm, it should use debt to finance the $45 2. Since Stephenson is an all-equity firm with 11 million shares […]

978-1259709685 Chapter 16 Lecture Note

Chapter 16 CAPITAL STRUCTURE: BASIC CONCEPTS SLIDES CHAPTER ORGANIZATION 16.1 The Capital Structure Question and the Pie Theory 16.2 Maximizing Firm Value versus Maximizing Stockholder Interests 16.3 Financial Leverage and Firm Value: An Example Leverage and Returns to Shareholders The […]

978-1259709685 Chapter 16 Solution Manual Part 1

CHAPTER 16 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 1. Assumptions of the Modigliani-Miller theory in a world without taxes: 1) Individuals can borrow at the same interest rate at which the firm borrows. Since […]

978-1259709685 Chapter 16 Solution Manual Part 2

9. a. The rate of return earned will be the dividend yield. The company has debt, so it must make an interest payment. The net income for the company is: The investor will receive dividends in proportion to the percentage […]

978-1259709685 Chapter 16 Solution Manual Part 3

CHAPTER 16 – 23. a. Before the announcement of the stock repurchase plan, the market value of the outstanding debt is $3,100,000. Using the debt–equity ratio, we can find that the value of the outstanding equity must be: The value […]

978-1259709685 Chapter 17 Case

CHAPTER 17 C-1 CHAPTER 17 McKENZIE CORPORATION’S CAPITAL BUDGETING 1. We assume the $5,700,000 is spent immediately so we can ignore time value of money considerations. If we include the time value of money, the numerical solutions will change slightly, […]

978-1259709685 Chapter 17 Lecture Note

Chapter 17 CAPITAL STRUCTURE: LIMITS TO THE USE OF DEBT SLIDES CHAPTER ORGANIZATION 17.1 Costs of Financial Distress Bankruptcy Risk or Bankruptcy Cost? 17.2 Description of Financial Distress Costs Direct Costs of Financial Distress: Legal and Administrative Costs of Liquidation […]

978-1259709685 Chapter 17 Solution Manual

CHAPTER 17 – CHAPTER 17 CAPITAL STRUCTURE: LIMITS TO THE USE OF DEBT Answers to Concepts Review and Critical Thinking Questions 1. Direct costs are potential legal and administrative costs. These are the costs associated with the litigation arising from […]

978-1259709685 Chapter 18 Case

CHAPTER 18 CASE C-1 CHAPTER 18 THE LEVERAGED BUYOUT OF CHEEK PRODUCTS, INC. In this leveraged buyout, the debt level of the company changes through time. Since the debt level changes through time, the APV method is appropriate for evaluating […]

978-1259709685 Chapter 18 Lecture Note

Chapter 18 VALUATION AND CAPITAL BUDGETING FOR THE LEVERED FIRM SLIDES CHAPTER ORGANIZATION 18.1 Adjusted Present Value Approach 18.2 Flow to Equity Approach Step 1: Calculating Levered Cash Flow (LCF) Step 2: Calculating Rs Step 3: Valuation 18.3 Weighted Average […]

978-1259709685 Chapter 18 Solution Manual Part 1

CHAPTER 18 VALUATION AND CAPITAL BUDGETING FOR THE LEVERED FIRM Answers to Concepts Review and Critical Thinking Questions 1. APV is equal to the NPV of the project (i.e. the value of the project for an unlevered firm) plus the […]

978-1259709685 Chapter 18 Solution Manual Part 2

CHAPTER 18 – 11. If the company had to issue debt under the terms it would normally receive, the interest rate on the debt would increase to the company’s normal cost of debt. The NPV of an all-equity project would […]

978-1259709685 Chapter 19 Case

C-1 CASE SOLUTIONS CHAPTER 19 ELECTRONIC TIMING, INC. 1. The value of the company will decline by the amount of the dividend. Ignoring taxes, shareholders 2. The value of the company could increase or decrease. If the company is over-levered, […]

978-1259709685 Chapter 19 Lecture Note Part 1

Chapter 19 DIVIDENDS AND OTHER PAYOUTS SLIDES CHAPTER WEB SITES Section Web Address 19.2 www.earnings.com 19.10 www.investmenthouse.com finance.yahoo.com 19.1 Key Concepts and Skills 19.2 Chapter Outline 19.3 Different Types of Payouts 19.4 Standard Method of Cash Dividend 19.5 Procedure for […]

978-1259709685 Chapter 19 Lecture Note Part 2

Slide 19.16 Personal Taxes and Dividends .A Firms without Sufficient Cash to Pay a Dividend Slide 19.17 Firms without Sufficient Cash In the absence of taxes, issuing stock to pay a dividend would be a zero NPV decision. However, with […]

978-1259709685 Chapter 19 Solution Manual Part 1

CHAPTER 19 DIVIDENDS AND OTHER PAYOUTS Answers to Concepts Review and Critical Thinking Questions 1. Dividend policy deals with the timing of dividend payments, not the amounts ultimately paid. 2. A stock repurchase reduces equity while leaving debt unchanged. The […]

978-1259709685 Chapter 19 Solution Manual Part 2

CHAPTER 19 – 13. a. If the company makes a dividend payment, we can calculate the wealth of a shareholder as: The stock price after the dividend payment will be: PX = $51 – 4.20 PX = $46.80 per share […]

978-1259709685 Chapter 2 Case

C-1 CASE SOLUTIONS CHAPTER 2 CASH FLOWS AT WARF COMPUTERS The operating cash flow for the company is: (NOTE: All numbers are in thousands of dollars) OCF = EBIT + Depreciation – Current taxes OCF = $2,080 + 248 – […]

978-1259709685 Chapter 2 Lecture Note Part 1

Chapter 2 FINANCIAL STATEMENTS AND CASH FLOW SLIDES CHAPTER WEB SITES Section Web Address 2.1 Key Concepts and Skills 2.2 Chapter Outline 2.3 Sources of Information 2.4 The Balance Sheet 2.5 U.S. Composite Corporation Balance Sheet 2.6 Balance Sheet Analysis […]

978-1259709685 Chapter 2 Lecture Note Part 2

Slide 2.17 Non-Cash Items The matching principle also creates the recognition of non-cash items. For example, when we purchase a machine, the cash flow occurs immediately, but we recognize the expense of the machine over time as it is used […]

978-1259709685 Chapter 2 Solution Manual Part 1

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW Answers to Concepts Review and Critical Thinking Questions 1. True. Every asset can be converted to cash at some price. However, when we are referring to a liquid 2. The recognition and […]

978-1259709685 Chapter 2 Solution Manual Part 2

16. The market value of shareholders’ equity cannot be negative. A negative market value in this case would imply that the company would pay you to own the stock. The market value of shareholders’ equity can be stated as: Shareholders’ […]

978-1259709685 Chapter 20 Case

C-1 CASE SOLUTIONS CHAPTER 20 EAST COAST YACHTS GOES PUBLIC 1. The main difference in the costs is the reduced possibility of underpricing in a Dutch auction. As to which is better, we don’t actually know. In theory, the Dutch […]

978-1259709685 Chapter 20 Lecture Note Part 1

Chapter 20 Raising Capital SLIDES CHAPTER ORGANIZATION 20.1 Early-Stage Financing and Venture Capital Venture Capital Stages of Financing Some Venture Capital Realities Venture Capital Investments and Economic Conditions 20.2 The Public Issue 20.1 Key Concepts and Skills 20.2 Chapter Outline […]

978-1259709685 Chapter 20 Lecture Note Part 2

Slide 20.16 IPO Underpricing The underpricing (there is a large increase above the offer price the first day of trading) of IPOs is very common. The record year is still 1999, with an average first day return of almost 70%. […]

978-1259709685 Chapter 20 Solution Manual Part 1

CHAPTER 20 ISSUING SECURITIES TO THE PUBLIC Answers to Concepts Review and Critical Thinking Questions 1. A company’s internally generated cash flow provides a source of equity financing. For a profitable company, outside equity may never be needed. Debt issues […]

978-1259709685 Chapter 20 Solution Manual Part 2

CHAPTER 20 – 11. The current ROE of the company is: The new net income will be the ROE times the new total equity, or: NI1 = (ROE0)(TE1) NI1 = .1849($5,300,000 + 1,500,000) NI1 = $1,257,358 The company’s current earnings […]

978-1259709685 Chapter 21 Case

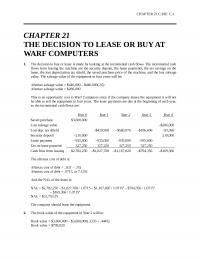

CHAPTER 21 CASE C-1 CHAPTER 21 THE DECISION TO LEASE OR BUY AT WARF COMPUTERS 1. The decision to buy or lease is made by looking at the incremental cash flows. The incremental cash flows from leasing the machine are […]

978-1259709685 Chapter 21 Lecture Note

CHAPTER 21 LEASING SLIDES CHAPTER ORGANIZATION 21.1 Key Concepts and Skills 21.2 Chapter Outline 21.3 Types of Leases 21.4 Buying versus Leasing 21.5 Operating Leases 21.6 Financial Leases 21.7 Sale and Lease-Back 21.8 Leveraged Leases 21.9 Leveraged Leases 21.10 Accounting […]

978-1259709685 Chapter 21 Solution Manual Part 1

CHAPTER 21 LEASING Answers to Concepts Review and Critical Thinking Questions 1. Some key differences are: (1) Lease payments are fully tax-deductible, but only the interest portion 2. The less profitable one because leasing provides, among other things, a mechanism […]

978-1259709685 Chapter 21 Solution Manual Part 2

CHAPTER 21 – 12. The decision to lease results in a debt capacity that is lowered by the present value of the aftertax lease payments. The aftertax lease payment is: 13. a. Since both companies have the same tax rate, […]

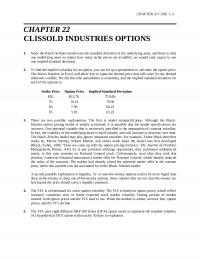

978-1259709685 Chapter 22 Case

CHAPTER 22 CASE C-1 CHAPTER 22 CLISSOLD INDUSTRIES OPTIONS 1. Since the Black–Scholes model uses the standard deviation of the underlying asset, and there is only 2. To find the implied volatility for an option, you can set up a […]

978-1259709685 Chapter 22 Lecture Note Part 1

CHAPTER 22 OPTIONS AND CORPORATE FINANCE SLIDES 22.1 Key Concepts and Skills 22.2 Chapter Outline 22.3 Options 22.4 Options 22.5 Call Options 22.6 Call Option Pricing at Expiry 22.7 Call Option Payoffs 22.8 Call Option Profits 22.9 Put Options 22.10 […]

978-1259709685 Chapter 22 Lecture Note Part 2

Slide 22.35 American Call Lecture Tip: You may want to discuss the importance of arbitrage in the valuation of options. The classic definition of arbitrage is trading in more than one market simultaneously to earn a riskless profit. It is […]

978-1259709685 Chapter 22 Solution Manual Part 1

CHAPTER 22 OPTIONS AND CORPORATE FINANCE Answers to Concept Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put option confers the right, […]

978-1259709685 Chapter 22 Solution Manual Part 2

23. We can use the Black–Scholes model to value the equity of a firm. Using the asset value of $27,200 as the stock price, and the face value of debt of $25,000 as the exercise price, the value of the […]

978-1259709685 Chapter 22 Solution Manual Part 3

CHAPTER 22 – 29. To construct the collar, the investor must purchase the stock, sell a call option with a high strike price, and buy a put option with a low strike price. So, to find the cost of the […]

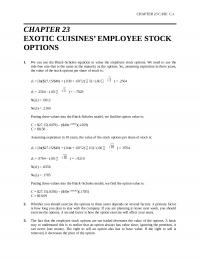

978-1259709685 Chapter 23 Case

CHAPTER 23 CASE C-1 CHAPTER 23 EXOTIC CUISINES’ EMPLOYEE STOCK OPTIONS 1. We can use the Black–Scholes equation to value the employee stock options. We need to use the risk-free rate that is the same as the maturity as the […]

978-1259709685 Chapter 23 Lecture Note

CHAPTER 23 OPTIONS AND CORPORATE FINANCE EXTENSIONS AND APPLICATIONS SLIDES CHAPTER ORGANIZATION 23.1 Executive Stock Options Why Options? Valuing Executive Compensation 23.1 Key Concepts and Skills 23.2 Chapter Outline 23.3 Executive Stock Options 23.4 Valuing Executive Compensation 23.5 Valuing a […]

978-1259709685 Chapter 23 Solution Manual Part 1

CHAPTER 23 OPTIONS AND CORPORATE FINANCE: EXTENSIONS AND APPLICATIONS Answers to Concepts Review and Critical Thinking Questions 1. One of the purposes to giving stock options to CEOs (instead of cash) is to tie the performance of the 4. As […]

978-1259709685 Chapter 23 Solution Manual Part 2

CHAPTER 23 – 8. Using the binomial mode, we will find the value of u and d, which are: u = e/ √ n u = e.70/ √ 12 u = 1.2239 d = 1 / u d = 1 […]

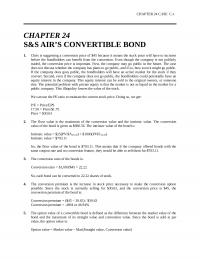

978-1259709685 Chapter 24 Case

CHAPTER 24 CASE C-1 CHAPTER 24 S&S AIR’S CONVERTIBLE BOND 1. Chris is suggesting a conversion price of $45 because it means the stock price will have to increase before the bondholders can benefit from the conversion. Even though the […]

978-1259709685 Chapter 24 Lecture Note

CHAPTER 24 WARRANTS AND CONVERTIBLES SLIDES CHAPTER ORGANIZATION 24.1 Warrants 24.2 The Difference between Warrants and Call Options How the Firm Can Hurt Warrant Holders 24.3 Warrant Pricing and the Black-Scholes Model 24.4 Convertible Bonds 24.5 The Value of Convertible […]

978-1259709685 Chapter 24 Solution Manual

CHAPTER 24 – CHAPTER 24 WARRANTS AND CONVERTIBLES Answers to Concepts Review and Critical Thinking Questions 1. A warrant is issued by the company, and when a warrant is exercised, the number of shares 2. a. If the stock price […]

978-1259709685 Chapter 25 Case

CHAPTER 25 CASE C-1 CHAPTER 25 WILLIAMSON MORTGAGE, INC. 1. Jerry’s mortgage payments form a 25-year annuity with monthly payments, discounted at the long- term interest rate of 5.5 percent. We can solve for the payment amount so that the […]

978-1259709685 Chapter 25 Lecture Note Part 1

CHAPTER 25 DERIVATIVES AND HEDGING RISK SLIDES 22.1 Key Concepts and Skills 22.2 Chapter Outline 22.3 Forward Contracts 22.4 Futures Contracts 22.5 Futures Contracts 22.6 Daily Resettlement: An Example 22.7 Daily Resettlement: An Example 22.8 Daily Resettlement: An Example 22.9 […]

978-1259709685 Chapter 25 Lecture Note Part 2

Slide 25.17 Interest Rate Futures Contracts .A Pricing of Treasury Bonds Slide 25.18 – Slide 25.19 Pricing of Treasury Bonds Recall the general expression for the value of a bond: Bond value = present value of coupons + present value […]

978-1259709685 Chapter 25 Solution Manual Part 1

CHAPTER 25 DERIVATIVES AND HEDGING RISK Answers to Concepts Review and Critical Thinking Questions 1. Since the firm is selling futures, it wants to be able to deliver the lumber; therefore, it is a supplier. Since a decline in lumber […]

978-1259709685 Chapter 25 Solution Manual Part 2

CHAPTER 25 – 7. The duration of a bond is the average time to payment of the bond’s cash flows, weighted by the ratio of the present value of each payment to the price of the bond. Since the bond […]

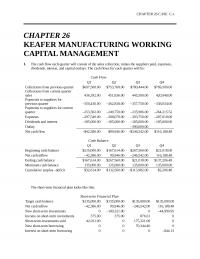

978-1259709685 Chapter 26 Case

CHAPTER 26 CASE C-1 CHAPTER 26 KEAFER MANUFACTURING WORKING CAPITAL MANAGEMENT 1. The cash flow each quarter will consist of the sales collection, minus the suppliers paid, expenses, dividends, interest, and capital outlays. The cash flows for each quarter will […]

978-1259709685 Chapter 26 Lecture Note Part 1

Chapter 26 SHORT-TERM FINANCE AND PLANNING SLIDES CHAPTER WEB SITES Section Web Address Introduction www.afponline.org 26.2 www.businessdebts.com www.opiglobal.com CHAPTER ORGANIZATION 26.1 Key Concepts and Skills 26.2 Chapter Outline 26.3 Balance Sheet Model of the Firm 26.4 Tracing Cash and Net […]

978-1259709685 Chapter 26 Lecture Note Part 2

Slide 26.14 Carrying Costs and Shortage Costs Slide 26.15 Appropriate Flexible Policy Slide 26.16 Appropriate Restrictive Policy Lecture Tip: The just-in-time inventory system is designed to reduce the inventory period. In essence, companies pay their suppliers to carry the inventory […]

978-1259709685 Chapter 26 Solution Manual

CHAPTER 26 – CHAPTER 26 SHORT-TERM FINANCE AND PLANNING Answers to Concepts Review and Critical Thinking Questions 1. These are firms with relatively long inventory periods and/or relatively long receivables periods. 2. These are firms that have a relatively long […]

978-1259709685 Chapter 27 Appendix

Appendix 27A DETERMINING THE TARGET CASH BALANCE SLIDES CHAPTER ORGANIZATION 27A.1 The Basic Idea 27A.2 The BAT Model 27A.3 The Miller-Orr Model: A More General Approach 27A.4 Implications of the BAT and Miller-Orr Models 27A.5 Other Factors Influencing the Target […]

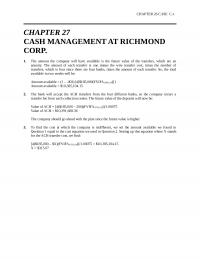

978-1259709685 Chapter 27 Case

CHAPTER 26 CASE C-1 CHAPTER 27 CASH MANAGEMENT AT RICHMOND CORP. 1. The amount the company will have available is the future value of the transfers, which are an annuity. The amount of each transfer is one minus the wire […]

978-1259709685 Chapter 27 Lecture Note

Chapter 27 CASH MANAGEMENT SLIDES CHAPTER WEB SITES Section Web Address 27.2 www.carreker.fiserr.com 27.3 www.gtnews.com 27.4 www.toolkit.cch.com/tools/tools.asp 27.5 www.bloomberg.com CHAPTER ORGANIZATION 27.1 Reasons for Holding Cash The Speculative and Precautionary Motives The Transaction Motive Compensating Balances Costs of Holding Cash […]

978-1259709685 Chapter 27 Solution Manual

CHAPTER 27 APPENDIX – CHAPTER 27 CASH MANAGEMENT Answers to Concepts Review and Critical Thinking Questions 1. Yes. Once a firm has more cash than it needs for operations and planned expenditures, the excess 2. If it has too much […]

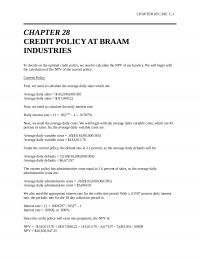

978-1259709685 Chapter 28 Case

CHAPTER 28 CASE C-1 CHAPTER 28 CREDIT POLICY AT BRAAM INDUSTRIES To decide on the optimal credit policy, we need to calculate the NPV of each policy. We will begin with the calculation of the NPV of the current policy. […]

978-1259709685 Chapter 28 Lecture Note Part 1

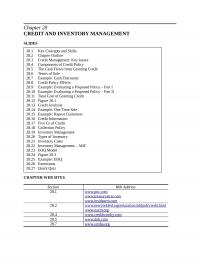

Chapter 28 CREDIT AND INVENTORY MANAGEMENT SLIDES CHAPTER WEB SITES Section Web Address 28.1 www.pnc.com www.treasurystrat.com www.insidearm.com 28.2 www.newyorkfed.org/education/addpub/credit.html www.nacm.org 28.4 www.creditworthy.com 28.5 www.dnb.com 28.7 www.simba.org 28.1 Key Concepts and Skills 28.2 Chapter Outline 28.3 Credit Management: Key Issues 28.4 […]

978-1259709685 Chapter 28 Lecture Note Part 2

Slide 28.14 Example: One Time Sale Repeat Business NPV = -v + (1 – )(P – v)/R Slide 28.15 Example: Repeat Customers A. Credit information: -Financial statements -Credit reports (i.e., Dun and Bradstreet) -Banks -Customer’s payment history Slide 28.16 Credit […]

978-1259709685 Chapter 28 Solution Manual Part 1

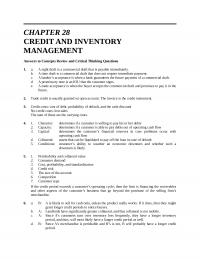

CHAPTER 28 CREDIT AND INVENTORY MANAGEMENT Answers to Concepts Review and Critical Thinking Questions 1. a. A sight draft is a commercial draft that is payable immediately. b. A time draft is a commercial draft that does not require immediate […]

978-1259709685 Chapter 28 Solution Manual Part 2

CHAPTER 28 – 15. The cash flow from the old policy is: The incremental cash flow, which is a perpetuity, is the difference between the old policy cash flows and the new policy cash flows, so: Incremental cash flow = […]

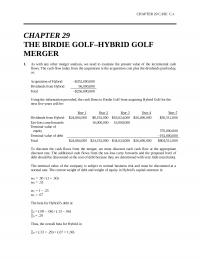

978-1259709685 Chapter 29 Case

CHAPTER 29 CASE C-1 CHAPTER 29 THE BIRDIE GOLF–HYBRID GOLF MERGER 1. As with any other merger analysis, we need to examine the present value of the incremental cash flows. The cash flow today from the acquisition is the acquisition […]

978-1259709685 Chapter 29 Lecture Note Part 1

CHAPTER 29 MERGERS AND ACQUISITIONS SLIDES CHAPTER ORGANIZATION 29.1 The Basic Forms of Acquisitions Merger or Consolidation Acquisition of Stock Acquisition of Assets A Classification Scheme A Note about Takeovers 29.2 Synergy 29.1 Key Concepts and Skills 29.2 Chapter Outline […]

978-1259709685 Chapter 29 Lecture Note Part 2

Slide 29.12 A Cost to Stockholders from Reduction in Risk The coinsurance effect in a merger or acquisition occurs because even if one of the pre-merger firm fails, bondholders will be still be paid by the surviving firm. The coinsurance […]

978-1259709685 Chapter 29 Solution Manual Part 1

CHAPTER 29 MERGERS, ACQUISITIONS, AND DIVESTITURES Answers to Concepts Review and Critical Thinking Questions 1. In the purchase method, assets are recorded at market value, and goodwill is created to account for the excess of the purchase price over this […]

978-1259709685 Chapter 29 Solution Manual Part 2

CHAPTER 29 – 12. a. The synergy will be the present value of the incremental cash flows of the proposed purchase. Since the cash flows are perpetual, the synergy value is: b. The value of Flash-in-the-Pan to Fly-by-Night is the […]

978-1259709685 Chapter 3 Case

CHAPTER 3 CASE C-1 CHAPTER 3 RATIOS AND FINANCIAL PLANNING AT EAST COAST YACHTS 1. The calculations for the ratios listed are: Quick ratio = ($15,823,700 – 6,627,300) / $21,320,300 Quick ratio = .43 times Total asset turnover = $210,900,000 […]

978-1259709685 Chapter 3 Lecture Note Part 1

Chapter 3 FINANCIAL STATEMENTS ANALYSIS AND FINANCIAL MODELS SLIDES CHAPTER WEB SITES Section Web Address 3.2 www.reuters.com/finance/stocks www.sba.gov 3.4 www.planware.org CHAPTER ORGANIZATION 3.1 Key Concepts and Skills 3.2 Chapter Outline 3.3 Financial Statements Analysis 3.4 Ratio Analysis 3.5 Categories of […]

978-1259709685 Chapter 3 Lecture Note Part 2

Slide 3.14 Using Financial Statements Ratios cannot be interpreted in isolation, but are rather to be considered as comparative metrics – either across time or between firms. Lecture Tip: What is “EEBS”? Under the heading “A Wire Story We’d Like […]

978-1259709685 Chapter 3 Solution Manual Part 1

CHAPTER 3 LONG-TERM FINANCIAL PLANNING AND GROWTH Answers to Concepts Review and Critical Thinking Questions 1. Time trend analysis gives a picture of changes in the company’s financial situation over time. Comparing a firm to itself over time allows the […]

978-1259709685 Chapter 3 Solution Manual Part 2

14. This is a multi-step problem involving several ratios. It is often easier to look backward to determine where to start. We need receivables turnover to find days’ sales in receivables. To calculate receivables turnover, we need credit sales, and […]

978-1259709685 Chapter 3 Solution Manual Part 3

CHAPTER 3 – 1 24. The pro forma income statements for all three growth rates will be: MOOSE TOURS INC. Pro Forma Income Statement 15 % Sales Growth 20% Sales Growth 25% Sales Growth Sales $865,375 $903,000 $940,625 Costs 673,440 […]

978-1259709685 Chapter 30 Lecture Note

Chapter 30 FINANCIAL DISTRESS SLIDES CHAPTER ORGANIZATION 30.1 What Is Financial Distress? 30.2 What Happens in Financial Distress? 30.3 Bankruptcy Liquidation and Reorganization Bankruptcy Liquidation Bankruptcy Reorganization 30.4 Private Workout or Bankruptcy: Which Is Best? The Marginal Firm Holdouts Complexity […]

978-1259709685 Chapter 30 Solution Manual

CHAPTER 30 – CHAPTER 30 FINANCIAL DISTRESS Answers to Concepts Review and Critical Thinking Questions 1. Financial distress is often linked to insolvency. Stock-based insolvency occurs when a firm has a 2. Financial distress frequently can serve as a firm’s […]

978-1259709685 Chapter 31 Case

CHAPTER 31 EAST COAST YACHTS GOES INTERNATIONAL 2. If the dollar strengthens, the profit will decline. Conversely, if the dollar weakens, the profit will increase. 3. The company will pay the sales commission out of gross sales, so the after-commission […]

978-1259709685 Chapter 31 Lecture Note Part 1

Chapter 31 INTERNATIONAL CORPORATE FINANCE SLIDES CHAPTER WEB SITES Section Web Address 31.1 www.adr.com 31.1 Key Concepts and Skills 31.2 Chapter Outline 31.3 Terminology 31.4 Terminology 31.5 Foreign Exchange Markets and Exchange Rates 31.6 FOREX Market Participants 31.7 Exchange Rates […]

978-1259709685 Chapter 31 Lecture Note Part 2

Slide 31.18 – Slide 31.20 Interest Rate Parity .A Covered Interest Arbitrage A covered interest arbitrage exists when a riskless profit can be made by borrowing in the U.S. at the risk-free rate, converting the borrowed dollars into a foreign […]

978-1259709685 Chapter 31 Solution Manual

CHAPTER 31 INTERNATIONAL CORPORATE FINANCE Answers to Concepts Review and Critical Thinking Questions 1. a. The dollar is selling at a premium because it is more expensive in the forward market than in b. The franc is expected to depreciate […]

978-1259709685 Chapter 4 Appendix

Appendix 4A Net Present Value: First Principles of Finance SLIDES APPENDIX ORGANIZATION 4A.1 Making Consumption Choices over Time 4A.2 Making Investment Choices 4A.3 Illustrating the Investment Decision ANNOTATED APPENDIX OUTLINE Slide 4A.0 Appendix 4 Title Slide Slide 4A.1 Key Concepts […]

978-1259709685 Chapter 4 Case

CHAPTER 4 CASE C-1 CHAPTER 4 THE MBA DECISION 1. Age is obviously an important factor. The younger an individual is, the more time there is for the (hopefully) increased salary to offset the cost of the decision to return […]

978-1259709685 Chapter 4 Lecture Note Part 1

Chapter 4 DISCOUNTED CASH FLOW VALUATION SLIDES 4.41 Int ere st- Only Loans 4.1 Key Concepts and Skills 4.2 Chapter Outline 4.3 The One-Period Case 4.4 Future Value 4.5 Present Value 4.6 Present Value 4.7 Net Present Value 4.8 Net […]

978-1259709685 Chapter 4 Lecture Note Part 2

Slide 4.17 Calculator Keys Lecture Tip: Texas Instruments offers instructors an “Emulator” software that allows the face of the calculator to be projected onto a computer. This enables instructors to demonstrate key stroke sequences. Slide 4.18 – Slide 4.19 Multiple […]

978-1259709685 Chapter 4 Solution Appendix

CHAPTER 4, APPENDIX NET PRESENT VALUE: FIRST PRINCIPLES OF FINANCE Solutions to Questions and Problems NOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability constraints, when these intermediate steps are […]

978-1259709685 Chapter 4 Solution Manual Part 1

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value decreases. 3. The better deal is the one with equal […]

978-1259709685 Chapter 4 Solution Manual Part 2

19. The time line is: 0 1 … ? – $18,450 $500 $500 $500 $500 $500 $500 $500 $500 $500 Here, we need to find the length of an annuity. We know the interest rate, the PV, and the payments. […]

978-1259709685 Chapter 4 Solution Manual Part 3

42. The time line is: 0 3 PV $135,000 The profit the firm earns is just the PV of the sales price minus the cost to produce the asset. We find the PV of the sales price as the PV […]

978-1259709685 Chapter 4 Solution Manual Part 4

58. To answer this question, we should find the PV of both options, and compare them. Since we are purchasing the car, the lowest PV is the best option. The PV of the leasing option is the PV of the […]

978-1259709685 Chapter 4 Solution Manual Part 5

73. To answer this, we can diagram the perpetuity cash flows, which are: (Note, the subscripts are only to differentiate when the cash flows begin. The cash flows are all the same amount.) ….. C3 C2C2 C1C1C1 Thus, each of […]

978-1259709685 Chapter 4 Solution Manual Part 6

46. PV@ t = 14: $2,150 / .056 = $38,392.86 47. Enter 12 $23,000 $2,242.50 N I/Y PV PMT FV Solve for 2.502% APR = 2.502% 12 = 30.03% Enter 30.03% 12 NOM EFF C/Y Solve for 34.52% 48. […]

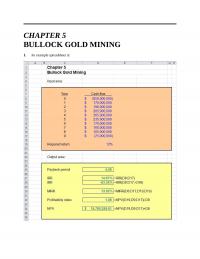

978-1259709685 Chapter 5 Case

CHAPTER 5 BULLOCK GOLD MINING 1. An example spreadsheet is: 2. Since the NPV of the mine is positive, the company should open the mine. We should note, it may be 3. There are many possible variations on the VBA […]

978-1259709685 Chapter 5 Lecture Note Part 1

Chapter 5 NET PRESENT VALUE AND OTHER INVESTMENT RULES SLIDES CHAPTER WEB SITES Section Web Address 5.1 www.missouribusiness.net CHAPTER ORGANIZATION 5.1 Key Concepts and Skills 5.2 Chapter Outline 5.3 Why Use Net Present Value? 5.4 The Net Present Value (NPV) […]

978-1259709685 Chapter 5 Lecture Note Part 2

Slide 5.8 The Discounted Payback Period Lecture Tip: The discounted payback period is the length of time until accumulated discounted cash flows equal or exceed the initial investment. Use of this technique entails all the work of NPV, but its […]

978-1259709685 Chapter 5 Solution Manual Part 1

CHAPTER 5 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Answers to Concepts Review and Critical Thinking Questions 1. Assuming conventional cash flows, a payback period less than the project’s life means that the NPV is positive for a zero discount […]

978-1259709685 Chapter 5 Solution Manual Part 2

13. a. The equation for the NPV of the project is: b. The equation for the IRR of the project is: 0 = –$78,000,000 + $110,000,000 / (1 + IRR) – $13,000,000 / (1 + IRR)2 From Descartes’ rule of […]

978-1259709685 Chapter 5 Solution Manual Part 3

CHAPTER 5 – 25. First, we need to find the future value of the cash flows for the one year in which they are blocked by the government. So, reinvesting each cash inflow for one year, we find: So, the […]

978-1259709685 Chapter 6 Case

CHAPTER 6 CASE #1 C-1 CHAPTER 6, Case #1 BETHESDA MINING To analyze this project, we must calculate the incremental cash flows generated by the project. Since net working capital is built up ahead of sales, the initial cash flow […]

978-1259709685 Chapter 6 Lecture Note Part 1

Chapter 6 MAKING CAPITAL INVESTMENT DECISIONS SLIDES CHAPTER ORGANIZATION 6.1 Incremental Cash Flows: The Key to Capital Budgeting Cash Flows—Not Accounting Income Sunk Costs Opportunity Costs Side Effects Allocated Costs 6.1 Key Concepts and Skills 6.2 Chapter Outline 6.3 Incremental […]

978-1259709685 Chapter 6 Lecture Note Part 2

Slide 6.9 – Slide 6.14 The Baldwin Company .A Which Set of Books? Firms are allowed to keep two sets of books: one for tax purposes and one for stockholder reporting. The tax effects represent a cash flow that is […]

978-1259709685 Chapter 6 Solution Manual Part 1

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will be used in a 2. a. Yes, […]

978-1259709685 Chapter 6 Solution Manual Part 2

17. To calculate the nominal cash flows, we increase each item in the income statement by the inflation rate, except for depreciation. Depreciation is a nominal cash flow, so it does not need to be adjusted for inflation in nominal […]

978-1259709685 Chapter 6 Solution Manual Part 3

25. Replacement decision analysis is the same as the analysis of two competing projects; in this case, keep the current equipment, or purchase the new equipment. We will consider the purchase of the new machine first. Purchase new machine: The […]

978-1259709685 Chapter 6 Solution Manual Part 4

CHAPTER 6 – 33. a. Since the two computers have unequal lives, the correct method to analyze the decision is the EAC. We will begin with the EAC of the new computer. Using the depreciation tax shield approach, the OCF […]

978-1259709685 Chapter 7 Case

CHAPTER 7 C-1 CHAPTER 7 BUNYAN LUMBER, LLC The company is faced with the option of when to harvest the lumber. Whatever harvest cycle the company chooses, it will follow that cycle in perpetuity. Since the forest was planted 20 […]

978-1259709685 Chapter 7 Lecture Note

Chapter 7 RISK ANALYSIS, REAL OPTIONS, AND CAPITAL BUDGETING SLIDES CHAPTER ORGANIZATION 7.1 Sensitivity Analysis, Scenario Analysis, and Break-Even Analysis Sensitivity Analysis and Scenario Analysis Break-Even Analysis 7.2 Monte Carlo Simulation Step 1: Specify the Basic Model 7.1 Key Concepts […]

978-1259709685 Chapter 7 Solution Manual Part 1

CHAPTER 7 RISK ANALYSIS, REAL OPTIONS, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. Forecasting risk is the risk that a poor decision is made because of errors in projected cash flows. 2. With a sensitivity […]

978-1259709685 Chapter 7 Solution Manual Part 2

15. The upper and lower bounds for the variables are: Base Case Best Case Worst Case Unit sales (new) 60,000 66,000 54,000 Price (new) $850 $935 $765 Best-case We will calculate the sales and variable costs first. Since we will […]

978-1259709685 Chapter 7 Solution Manual Part 3

CHAPTER 7 – 23. a. The NPV of the project is the sum of the present value of the cash flows generated by the project. The cash flows from this project are an annuity, so the NPV is: b. The […]

978-1259709685 Chapter 8 Case

CHAPTER 8 C-1 CHAPTER 8 FINANCING EAST COAST YACHT’S EXPANSION PLANS WITH A BOND ISSUE 1. A rule of thumb with bond provisions is to determine who the provisions benefit. If the company benefits, the bond will have a higher […]

978-1259709685 Chapter 8 Lecture Note Part 1

Chapter 8 INTEREST RATES AND BOND VALUATION SLIDES CHAPTER WEB SITES 8.1 Key Concepts and Skills 8.2 Chapter Outline 8.3 Bonds and Bond Valuation 8.4 Bond Valuation 8.5 The Bond-Pricing Equation 8.6 Bond Example 8.7 Bond Example 8.8 Bond Example: […]

978-1259709685 Chapter 8 Lecture Note Part 2

Slide 8.22 Pure Discount Bonds Example Zero coupon bonds are bonds that are offered at deep discounts because there are no periodic coupon payments. Although no cash interest is paid, firms deduct the implicit interest, while holders report it as […]

978-1259709685 Chapter 8 Solution Manual Part 2

24. To find the number of years to maturity for the bond, we need to find the price of the bond. Since we already have the coupon rate, we can use the bond price equation, and solve for the number […]

978-1259709685 Chapter 8 Solution Manual Part 3

CHAPTER 8 – 16. P0 Enter 50 3.15% $1,000 N I/Y PV PMT FV 17. Miller Corporation P0 Enter 26 3.5% $42.50 $1,000 N I/Y PV PMT FV Solve for $1,126.68 P1 Enter 24 3.5% $42.50 $1,000 N I/Y PV […]

978-1259709685 Chapter 9 Case

CHAPTER 9 CASE C-1 CHAPTER 9 STOCK VALUATION AT RAGAN THERMAL SYSTEMS 1. The total dividends paid by the company were $640,000. Since there are 300,000 shares outstanding, the total earnings for the company were: This means the payout ratio […]

978-1259709685 Chapter 9 Lecture Note Part 1

Chapter 9 Stock Valuation SLIDES CHAPTER WEB SITES Section Web Address 9.6 www.bloomberg.com www.nyse.com www.nasdaq.com finance.yahoo.com CHAPTER ORGANIZATION 9.1 The Present Value of Common Stocks Dividends versus Capital Gains 9.1 Key Concepts and Skills 9.2 Chapter Outline 9.3 The PV […]

978-1259709685 Chapter 9 Lecture Note Part 2

Slide 9.16 Where Does R Come From Slide 9.17 Using the DGM to Find R Rearrange P0 = D1 / (R – g) to find R: R = (D1 / P0 ) + g Dividend yield = D1 / P0 […]

978-1259709685 Chapter 9 Solution Manual Part 1

CHAPTER 9 STOCK VALUATION Answers to Concept Questions 1. The value of any investment depends on the present value of its cash flows; i.e., what investors will 3. In general, companies that need the cash will often forgo dividends since […]

978-1259709685 Chapter 9 Solution Manual Part 2

CHAPTER 9 – 23. The required return of a stock consists of two components, the capital gains yield and the dividend yield. In the constant dividend growth model (growing perpetuity equation), the capital gains yield is the same as the […]