CHAPTER 29

MERGERS AND ACQUISITIONS

SLIDES

CHAPTER ORGANIZATION

29.1 The Basic Forms of Acquisitions

Merger or Consolidation

Acquisition of Stock

Acquisition of Assets

A Classification Scheme

A Note about Takeovers

29.2 Synergy

29.1 Key Concepts and Skills

29.2 Chapter Outline

29.3 The Basic Forms of Acquisitions

29.4 Merger versus Consolidation

29.5 Acquisitions

29.6 Varieties of Takeovers

29.7 Synergy

29.8 Synergy

29.9 Sources of Synergy

29.10 Calculating Value

29.11 Two Financial Side Effects of Acquisitions

29.12 A Cost to Stockholders from Reduction in Risk

29.13 The NPV of a Merger

29.14 Cash Acquisition

29.15 Stock Acquisition

29.16 Friendly vs. Hostile Takeovers

29.17 Defensive Tactics

29.18 More (Colorful) Terms

29.19 Have Mergers Added Value?

29.20 Have Mergers Added Value?

29.21 The Tax Forms of Acquisition

29.22 Accounting for Acquisitions

29.23 Going Private and Leveraged Buyouts

29.24 Divestitures

29.25 Quick Quiz

29.3 Sources of Synergy

Revenue Enhancement

Cost Reduction

Tax Gains

Reduced Capital Requirements

29.4 Two Financial Side Effects of Acquisitions

Earnings Growth

Diversification

29.5 A Cost to Stockholders from Reduction in Risk

The Base Case

Both Firms Have Debt

How Can Shareholders Reduce Their Losses from the Coinsurance Effect?

29.6 The NPV of a Merger

Cash

Common Stock

Cash versus Common Stock

29.7 Friendly versus Hostile Takeovers

29.8 Defensive Tactics

Deterring Takeovers before Being in Play

Deterring a Takeover after the Company Is in Play

29.9 Have Mergers Added Value?

Returns to Bidders

Target Companies

The Managers versus the Stockholders

29.10 The Tax Forms of Acquisitions

29.11 Accounting for Acquisitions

29.12 Going Private and Leveraged Buyouts

29.13 Divestitures

Sale

Spin-Off

Carve-Out

Tracking Stocks

ANNOTATED CHAPTER OUTLINE

Slide 29.0 Chapter 29 Title Slide

Slide 29.1 Key Concepts and Skills

Slide 29.2 Chapter Outline

29.1 The Basic Forms of Acquisitions

Slide 29.3 The Basic Forms of Acquisition

Bidder firm – the company making an offer to buy the stock or assets of

another firm

Target firm – the firm that is being sought

Consideration – cash or securities offered in an acquisition or merger

Lecture Tip: Overall, the massive wave of mergers and restructurings of

the 1980s resulted in increased competitiveness, lower costs, and greater

efficiency. A not-uncommon downside to the picture, however, is the job

loss and dislocation associated with the redeployment of corporate assets.

Unfortunately, popular press writers rarely grasp the true causes of such

events. One person who does is Peter Lynch, the successful former

manager of the Fidelity Magellan fund. Consider some of his statements.

“It’s amazing that the basic cause of downsizing is so rarely

acknowledged: these companies have more workers than they really need

– or can afford to pay.

CEOs aren’t callous Scrooges shouting ‘Bah, humbug!’ as they shove

people out the door; they are responding to a competitive situation that

demands that they become more productive.

If we must blame somebody for the layoffs, it ought to be you and me.

All of us are looking for the best deals in clothing, computers and

telephone service – and rewarding the high-quality, low-cost providers

with our business. I haven’t met one person who would agree to pay AT&T

twice the going rate for phone service if AT&T would promise to stop

laying people off. These companies are responding to the constant

pressure from consumers and shareholders.”

A. Merger or Consolidation

Merger – the complete absorption of one company by another (assets and

liabilities). The bidder remains, and the target ceases to exist.

Consolidation – a new firm is created. Joined firms cease their previous

existence.

Advantage – legally simple and relatively cheap

Disadvantage – must be approved by a majority vote of the shareholders of

both firms, usually requiring the cooperation of both sets of management

Slide 29.4 Merger versus Consolidation

Lecture Tip: Appearing relatively infrequently in previous decades, the

use of the hostile takeover bid to acquire control of a target firm exploded

in the 1980s. The term “corporate raider” (used previously to describe

someone who attempted to acquire board seats via a proxy contest)

entered the mainstream, and the stereotypical raider was cemented in the

public consciousness in the guise of the Gordon Gekko character from the

movie “Wall Street.”

Hostile takeover bids are often made via tender offer to current

shareholders, which obviates the need to obtain approval from the target

firm board. The rapid growth of hostile takeovers resulted in the creation

of an array of defensive mechanisms with which to fight them off.

Often, but not always, hostile bids are launched against firms that have

been performing poorly; the combination of a depressed share price and

dissatisfaction with management increases the bidder’s chance of success.

Of course, bids occur for other reasons; the series of attempts by Kirk

Kerkorian against Chrysler came following tremendous firm growth.

Kerkorian, however, wanted management to release some of the $7 billion

in cash reserves the firm had built up.

Lecture Tip: The merger wave of the 1990s is actually the fifth such wave

this century. The first occurred at the turn of the century and involved

approximately 1,500 mergers between 1895 and 1905. The second wave

coincided roughly with the decade of the 1920s and involved

approximately 2,000 transactions.

In the third wave during the late 1960s/early 1970s, annual activity

peaked with over 4,000 mergers in 1973. The late 1980s saw a high of

over 3,000 mergers in 1987. The 1990s was the largest wave, with nearly

8,000 mergers recorded in 1997.

B. Acquisition of Stock

Taking control by buying the voting stock of another firm with cash,

securities or both.

Slide 29.5 Acquisitions

Tender offer – offer by one firm or individual to buy shares in another firm

from any shareholder. Such deals are often contingent on the bidder

obtaining a minimum percentage of the shares; otherwise, no go.

Some factors involved in choosing between a tender offer and a merger:

1. No shareholder vote is required for a tender offer. Shareholders choose

to sell or not.

2. The tender offer bypasses the board and management of the target firm.

3. In unfriendly bids, a tender offer may be a way around unwilling

managers.

4. In a tender offer, if the bidder ends up with less than 80% of the target

firm’s stock, it must pay taxes on a portion of the dividends paid by the

target.

5. Complete absorption requires a merger. A tender offer is often the first

step toward a formal merger.

C. Acquisition of Assets

In an acquisition of assets, one firm buys most or all of another’s assets,

but liabilities are not involved as with a merger. Transferring titles can

make the process costly. The selling firm may remain in business.

D. A Classification Scheme

1. Horizontal acquisition – firms in the same industry

2. Vertical acquisition – firms at different steps of in the production

process

3. Conglomerate acquisition – firms in unrelated industries

Lecture Tip: It is useful to give names to the various types of mergers. For

example, McDonnell-Douglas/Boeing, MCI/British Telecommunications

PLC, and Chrysler/Daimler-Benz are all examples of horizontal mergers.

An example of a vertical merger would be Texaco (excess refining

capacity) and Getty Oil (significant oil reserves). U.S. Steel’s acquisition

of Marathon Oil would be a conglomerate acquisition.

Slide 29.6 Varieties of Takeovers

E. A Note about Takeovers

Lecture Tip: The popularity of proxy contests as a means of gaining

control has waxed and waned over the last five decades. In the 1950s, this

approach was a relatively popular means of removing target firm

management; as noted previously, those who initiated proxy contests were

even referred to in the popular press as “corporate raiders!” Empirical

evidence suggests, however, that proxy contests are time-consuming,

expensive for the dissident shareholder, and unlikely to result in complete

victory.

Tender offers came to the fore in the 1960s and 1970s. Some believe

that the use of the proxy battle waned because of its relatively high cost

and low probability of success. However, the ubiquity of takeover defenses

and regulatory constraints has contributed to the return of the importance

of the proxy battle as a means of gaining control.

Lecture Tip: An interesting example of a long, drawn-out proxy battle

appeared in The Wall Street Journal on October 8, 1996. Physician Steven

Scott founded Coastal Physicians Group, Inc., but was subsequently

ousted by its board of directors. Dr. Scott then filed suit and launched a

proxy fight. In return, the firm’s management counter-sued and blamed

him for the firm’s poor performance. Following several months of

wrangling, two candidates backed by Dr. Scott won board seats. The

struggle for control of Coastal is not unlike many proxy fights, in that they

are often associated with claims and counter-claims, lawsuits, and a great

deal of acrimony and expense.

29.2 Synergy

Slide 29.7 –

Slide 29.8 Synergy

The difference between the value of the combined firms and the sum of

the individual firms is the incremental gain:

V = VAB – (VA + VB).

Synergy – the value of the whole exceeds the sum of the parts

(V > 0)

The value of Firm B to Firm A = VB* = V + VB. VB* will be greater than

VB if the acquisition produces positive incremental cash flows, CF.

CF = EBIT + Depreciation – Taxes – Capital Requirements

CF = Revenue – Costs – Taxes – Capital Requirements

Lecture Tip: You may wish to provide a few examples of synergies that

may be realized from a merger. From an operational standpoint, the

merger may result in better utilization of excess capacity, such as the

Getty acquisition by Texaco. From a financial standpoint, the merger may

provide economies of scale in flotation costs or better access to the

financial markets. If the cash flows are less than perfectly correlated, the

probability of financial distress or bankruptcy may decrease, thereby

reducing the expected costs (assuming reduced variability does not have a

greater effect on the “option value” of equity).

29.3 Sources of Synergy

Slide 29.9 Sources of Synergy

A. Revenue Enhancement

1. Marketing gains – changes in advertising efforts, changes in the

distribution network, changes in the product mix

2. Strategic benefits (beachheads) – acquisitions that allow a firm to enter

a new industry that may become a platform for further expansion

3. Market power – reduction in competition or increase in market share

Lecture Tip: The text notes several reasons for M&A activity. The

following was sent via email to members of a mergers and acquisitions

listserv.

“Do you know a business experiencing a decline in sales, loss

of direction, no longer competitive, ineffective management, …

Or a business that’s being neglected by its corporate parent …

Or a [sic] owner

looking to retire that built a once successful business now

needing reinventing … or a company that needs strong

marketing, finance, and manufacturing disciplines … If you

know such a business … it will be worth your while to reply.”

B. Cost Reduction

1. Economy of scale – per unit costs decline with increasing output

2. Economies of vertical integration – coordinating closely related

activities or technology transfers

3. Complementary resources (economies of scope) – example: banks that

allow insurance or stock brokerage services to be sold on premises

4. Technology transfer

5. Elimination of inefficient management: If management is not doing its

job well, or others may be able to do the job better, acquisitions are one

way to replace management. The threat of takeover may be enough to

make managers act in the best interest of shareholders.

Lecture Tip: One of the fathers of modern takeover theory is Henry

Manne, who published Mergers and the Market for Corporate Control in

1965. In this seminal work, Manne proposes the (now commonly

accepted) notion that poorly run firms are natural takeover targets

because their market values will be depressed, permitting acquirers to

earn larger returns by running the firms successfully. This proposition has

been verified empirically in dozens of academic studies.

You might choose to use Jensen’s definition of the market for corporate

control: “the market in which competing managerial teams compete for

the right to manage corporate resources,” and use statistics provided in

his survey paper, as well as the follow-up by G. Jarrell, J. Brickley, and J.

Netter. (See “The Market for

Corporate Control: The Scientific Evidence,” Journal of Financial

Economics, vol. 11, April 1983, pp. 5 – 50, and “The Market for

Corporate Control: The Evidence Since 1980,” Journal of Economic

Perspectives, vol. 2, Winter 1988, pp. 49 – 68.)

C. Tax Gains

1. Net Operating Losses (NOL) – a firm with losses and not paying taxes

may be attractive to a firm with significant tax liabilities

-Carry-back and carry-forward provisions reduce incentive to merge

-IRS may disallow or restrict the use of NOL

2. Unused or increased debt capacity – adding debt can provide important

tax savings

3. Surplus funds – firms with significant free cash flow can:

-Pay dividends

-Repurchase shares

-Acquire shares or assets of another firm

Lecture Tip: The IRS requires that the merger must have justifiable

business purposes for the NOL carry-over to be allowed. And, if the

acquisition involves a cash payment to the target firm’s shareholders, the

acquisition is considered a taxable reorganization that results in a loss of

NOLs. NOL carry-overs are allowed in a tax-free reorganization that

involves an exchange of the acquiring firm’s common stock for the

acquired firm’s common stock. Additionally, if the target firm operates as

a separate subsidiary within the acquiring firm’s organization, the IRS

will allow the carry-over to shelter the subsidiary’s future earnings, but

not the acquiring firm’s future earnings.

D. Reduced Capital Requirements

1. A firm needing capacity acquires a firm with excess capacity rather than

build new

2. Possible advantages to raising capital given economies of scale in

issuing securities

3. May reduce the investment in working capital

Slide 29.10 Calculating Value

When calculating the gains from synergy, avoid the following mistakes:

1. Do not ignore market values. Use the current market value as a starting

point and ask, “What will change if the merger or acquisition takes place?”

2. Estimate only incremental cash flows. These are the basis of synergy.

3. Use the correct discount rate. Make sure to use a rate appropriate to the

risk of the cash flows.

4. Be aware of transaction costs. These can be substantial and should

include fees paid to investment bankers and lawyers, as well as disclosure

costs.

29.4 Two Financial Side Effects of Acquisitions

Slide 29.11 Two Financial Side Effects of Acquisitions

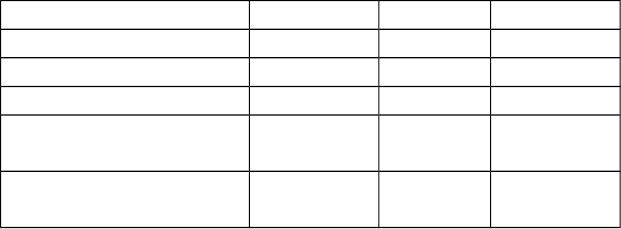

A. Earnings Growth

An acquisition may give the appearance of growth in EPS without actually

changing cash flows. This happens when the bidder’s stock price is higher

than the target’s, so that fewer shares are outstanding after the acquisition

than before.

Example: Pizza Shack wants to merge with Checkers Pizza. The merger

will not create any additional value, so assuming the market is not fooled,

the new firm, Stop ‘n Go Pizza, will be valued at the sum of the separate

market values of the firms.

Stop ‘n Go, is valued at $1,875,000 and has 125,000 shares outstanding

with a price of $15 per share. Pizza Shack stockholders receive 100,000

shares, and Checkers Pizza stockholders receive 25,000 shares of the

combined firm.

Before and after merger financial positions:

Before After

Pizza

Shack

Checkers

Pizza

Stop ‘n Go

Pizza

Total Earnings $150,000 $75,000 $225,000

Number of Shares 100,000 50,000 125,000

Earnings per Share $1.50 $1.50 $1.80

Price per Share $15.00 $7.50 $15.00

Price-to-Earnings

Ratio

10 5 8.33

Total Value $1,500,00

0

$375,00

0

$1,875,00

0

B. Diversification

A firm’s attempt at diversification does not create value because

stockholders could buy the stock of both firms, probably more cheaply.

Firms cannot reduce their systematic risk by merging.

Lecture Tip: In earlier chapters, we pointed out that conflicts of interest

may exist between stockholders and managers in publicly traded firms. As

noted above, diversification-based mergers do not create value for

shareholders (this was illustrated using option pricing theory in an earlier

chapter); however, these mergers may increase sales and reduce the total

variability of firm cash flows.

If managerial compensation and/or prestige is related to firm size, or

if less variable cash flows reduce the likelihood of managerial

replacement, then some mergers may be initiated for the wrong reasons –

they may be in the best interest of managers but not stockholders.

29.5 A Cost to Stockholders from Reduction in Risk