CHAPTER 16

CAPITAL STRUCTURE:

BASIC CONCEPTS

Answers to Concepts Review and Critical Thinking Questions

1. Assumptions of the Modigliani-Miller theory in a world without taxes: 1) Individuals can borrow at

the same interest rate at which the firm borrows. Since investors can purchase securities on margin,

an individual’s effective interest rate is probably no higher than that for a firm. Therefore, this

assumption is reasonable when applying MM’s theory to the real world. If a firm were able to

borrow at a rate lower than individuals, the firm’s value would increase through corporate leverage.

2. False. A reduction in leverage will decrease both the risk of the stock and its expected return.

3. False. Modigliani-Miller Proposition II (No Taxes) states that the required return on a firm’s equity

5. Business risk is the equity risk arising from the nature of the firm’s operating activity, and is directly

related to the systematic risk of the firm’s assets. Financial risk is the equity risk that is due entirely

6. No, it doesn’t follow. While it is true that the equity and debt costs are rising, the key thing to

7. Because many relevant factors such as bankruptcy costs, tax asymmetries, and agency costs cannot

easily be identified or quantified, it is practically impossible to determine the precise debt–equity

Solutions to Questions and Problems

NOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Basic

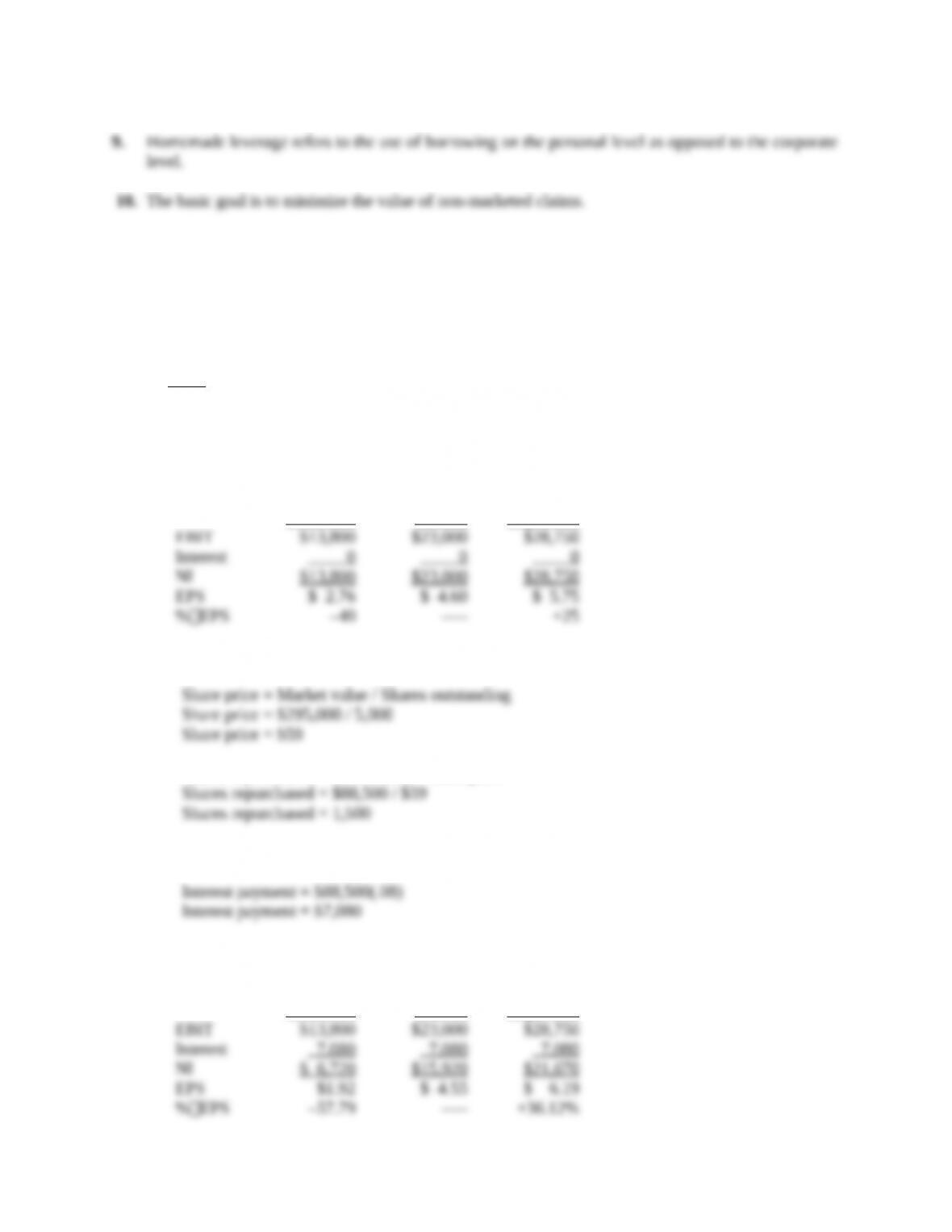

1. a. A table outlining the income statement for the three possible states of the economy is shown

below. The EPS is the net income divided by the 5,000 shares outstanding. The last row shows

the percentage change in EPS the company will experience in a recession or an expansion

economy.

Recession Normal Expansion

b. If the company undergoes the proposed recapitalization, it will repurchase:

Shares repurchased = Debt issued / Share price

The interest payment each year under all three scenarios will be:

The last row shows the percentage change in EPS the company will experience in a recession

or an expansion economy under the proposed recapitalization.

Recession Normal Expansion

2. a. A table outlining the income statement with taxes for the three possible states of the economy is

shown below. The share price is $59, and there are 5,000 shares outstanding. The last row

shows the percentage change in EPS the company will experience in a recession or an

expansion economy.

Recession Normal Expansion

b. A table outlining the income statement with taxes for the three possible states of the economy

and assuming the company undertakes the proposed capitalization is shown below. The interest

payment and shares repurchased are the same as in part b of Problem 1.

Recession Normal Expansion

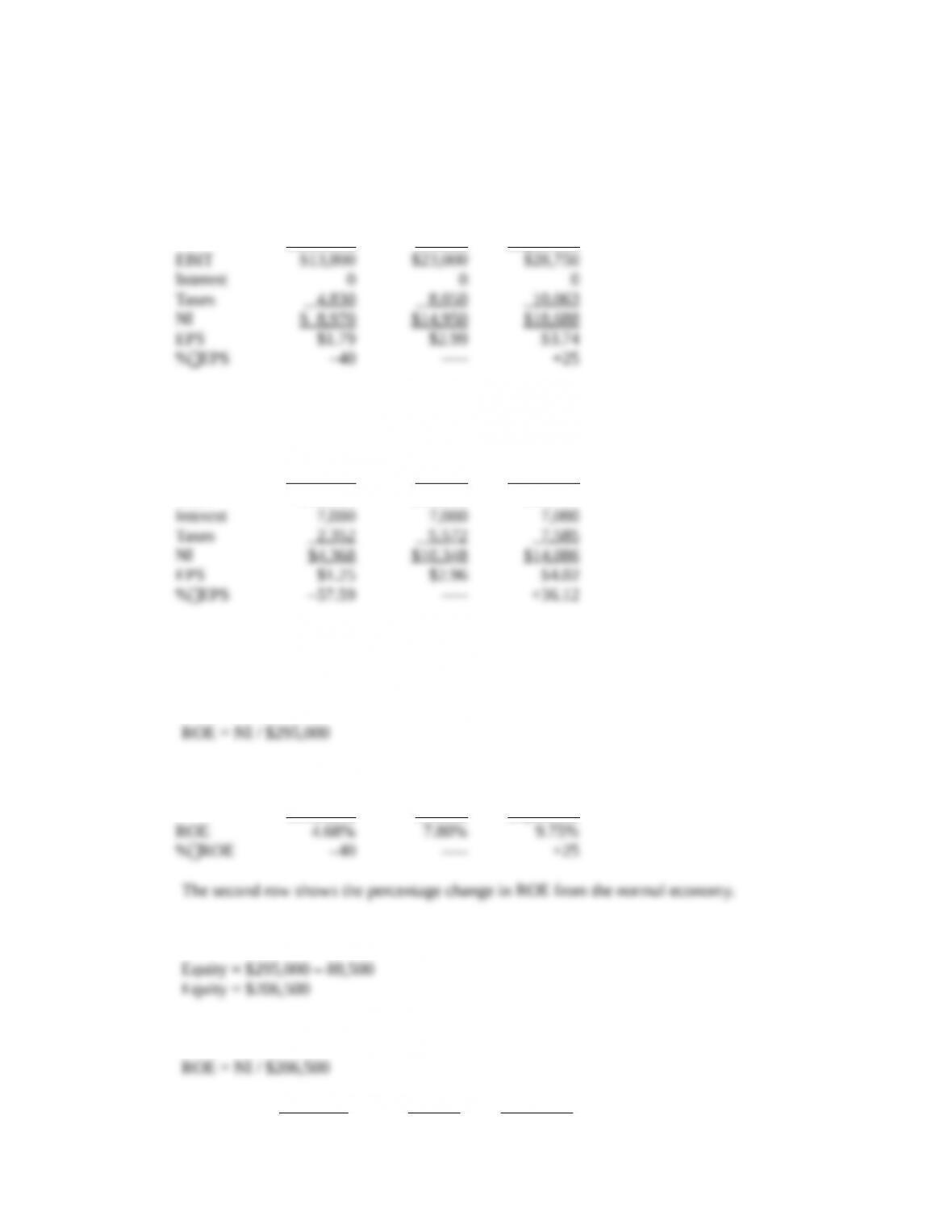

EBIT $13,800 $23,000 $28,750

Notice that the percentage change in EPS is the same both with and without taxes.

3. a. Since the company has a market-to-book ratio of 1.0, the total equity of the firm is equal to the

market value of equity. Using the equation for ROE:

The ROE for each state of the economy under the current capital structure and no taxes is:

Recession Normal Expansion

b. If the company undertakes the proposed recapitalization, the new equity value will be:

So, the ROE for each state of the economy is:

Recession Normal Expansion

c. If there are corporate taxes and the company maintains its current capital structure, the ROE is:

If the company undertakes the proposed recapitalization, and there are corporate taxes, the ROE

for each state of the economy is:

Notice that the percentage change in ROE is the same as the percentage change in EPS. The

percentage change in ROE is also the same with or without taxes.

4. a. Under Plan I, the unlevered company, net income is the same as EBIT with no corporate tax.

The EPS under this capitalization will be:

Under Plan II, the levered company, EBIT will be reduced by the interest payment. The interest

payment is the amount of debt times the interest rate, so:

And the EPS will be:

b. Under Plan I, the net income is $1,750,000 and the EPS is:

Under Plan II, the net income is:

And the EPS is:

c. To find the breakeven EBIT for two different capital structures, we set the equations for EPS

equal to each other and solve for EBIT. The breakeven EBIT is:

5. We can find the price per share by dividing the amount of debt used to repurchase shares by the

number of shares repurchased. Doing so, we find the share price is:

The value of the company under the all-equity plan is:

And the value of the company under the levered plan is:

6. a. The income statement for each capitalization plan is:

I II All-equity

The all-equity plan has the highest EPS; Plan I has the lowest EPS.

b. The breakeven level of EBIT occurs when the capitalization plans result in the same EPS. The

EPS is calculated as:

EPS = (EBIT – RBB) / Shares outstanding

This equation calculates the interest payment (RBB) and subtracts it from the EBIT, which

results in the net income. Dividing by the shares outstanding gives us the EPS. For the all-

And the breakeven EBIT between the all-equity capital structure and Plan II is:

EBIT = $13,056

c. Setting the equations for EPS from Plan I and Plan II equal to each other and solving for EBIT,

we get:

d. The income statement for each capitalization plan with corporate income taxes is:

I II All-equity

EBIT $10,500 $10,500 $10,500

The all-equity plan has the highest EPS; Plan I has the lowest EPS.

We can calculate the EPS as:

This is similar to the equation we used before, except that now we need to account for taxes.

Again, the interest expense term is zero in the all-equity capital structure. So, the breakeven

EBIT between the all-equity plan and Plan I is:

The breakeven EBIT between the all-equity plan and Plan II is:

And the breakeven between Plan I and Plan II is:

The break-even levels of EBIT do not change because the addition of taxes reduces the income

of all three plans by the same percentage; therefore, they do not change relative to one another.

7. To find the value per share of the stock under each capitalization plan, we can calculate the price as

the value of shares repurchased divided by the number of shares repurchased. The dollar value of the

shares repurchased is the increase in the value of the debt used to repurchase shares, or:

The number of shares repurchased is the decrease in shares outstanding, or:

So, under Plan I, the value per share is:

And under Plan II, the number of shares repurchased from the all equity plan by the $19,200 in debt

is:

This shows that when there are no corporate taxes, the stockholder does not care about the capital

8. a. The earnings per share are:

EPS = $39,600 / 6,000 shares

EPS = $6.60

b. To determine the cash flow to the shareholder, we need to determine the EPS of the firm under

the proposed capital structure. The market value of the firm is:

Under the proposed capital structure, the firm will raise new debt in the amount of:

Under the new capital structure, the company will have to make an interest payment on the new

debt. The net income with the interest payment will be:

This means the EPS under the new capital structure will be:

Since all earnings are paid as dividends, the shareholder will receive:

c. To replicate the proposed capital structure, the shareholder should sell 35 percent of their

shares, or 35 shares, and lend the proceeds at 7 percent. The shareholder will have an interest

cash flow of:

The shareholder will receive dividend payments on the remaining 65 shares, so the dividends

received will be:

This is the same cash flow we calculated in part a.

d. The capital structure is irrelevant because shareholders can create their own leverage or unlever