Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

14. This is a multi-step problem involving several ratios. It is often easier to look backward to determine

where to start. We need receivables turnover to find days’ sales in receivables. To calculate

receivables turnover, we need credit sales, and to find credit sales, we need total sales. Since we are

given the profit margin and net income, we can use these to calculate total sales as:

Profit margin = Net income / Sales

Credit sales are 80 percent of total sales, so:

Now we can find receivables turnover by:

Receivables turnover = Credit sales / Accounts receivable

15. The solution to this problem requires a number of steps. First, remember that:

Current assets + Net fixed assets = Total assets

So, if we find the current assets and the total assets, we can solve for net fixed assets. Using the

numbers given for the current ratio and the current liabilities, we solve for current assets:

Current ratio = Current assets / Current liabilities

To find the total assets, we must first find the total debt and equity from the information given. So,

we find the net income using the profit margin:

Profit margin = Net income / Sales

We now use the net income figure as an input into ROE to find the total equity:

ROE = Net income / Total equity

Next, we need to find the long-term debt. The long-term debt ratio is:

Now, we can find the total debt of the company:

Total debt = Current liabilities + Long-term debt

Total debt = $1,280 + 1,268.19

Total debt = $2,548.19

And, with the total debt, we can find the total debt & equity, which is equal to total assets:

And finally, we are ready to solve the balance sheet identity as:

16. This problem requires you to work backward through the income statement. First, recognize that

Net income = (1 – tC)EBT. Plugging in the numbers given and solving for EBT, we get:

EBT = $9,620 / (1 – .34)

EBT = $14,575.76

Now, we can add interest to EBT to get EBIT as follows:

To get EBITD (earnings before interest, taxes, and depreciation), the numerator in the cash coverage

ratio, add depreciation to EBIT:

Now, plug the numbers into the cash coverage ratio and calculate:

Cash coverage ratio = EBITD / Interest

17. We can start by multiplying ROE by Total assets / Total assets

ROE =

Net income

Equity =Net income

Equity ×Totalassets

Total assets

Rearranging, we get:

Net income

Sales ×Sales

Total assets ×Total assets

Equity ×EBT

EBT

We can rearrange as:

ROE =

Net income

EBT ×EBT

Sales ×Sales

Total assets ×Total assets

Equity

Finally, multiplying this equation EBIT / EBIT and rearranging yields:

Net income

EBT ×EBT

Sales ×Sales

Total assets ×Total assets

Equity ×EBIT

EBIT

ROE =

Net income

EBT ×EBT

EBIT ×EBIT

Sales ×Sales

Total assets ×Total assets

Equity

(1) (2) (3) (4) (5)

The interpretation of each term is as follows:

(1) This is the company's tax burden. This is the proportion of the company's profits retained after

paying income taxes.

(2) This is the company’s interest burden. It will be 1.00 for a company with no debt or financial

leverage.

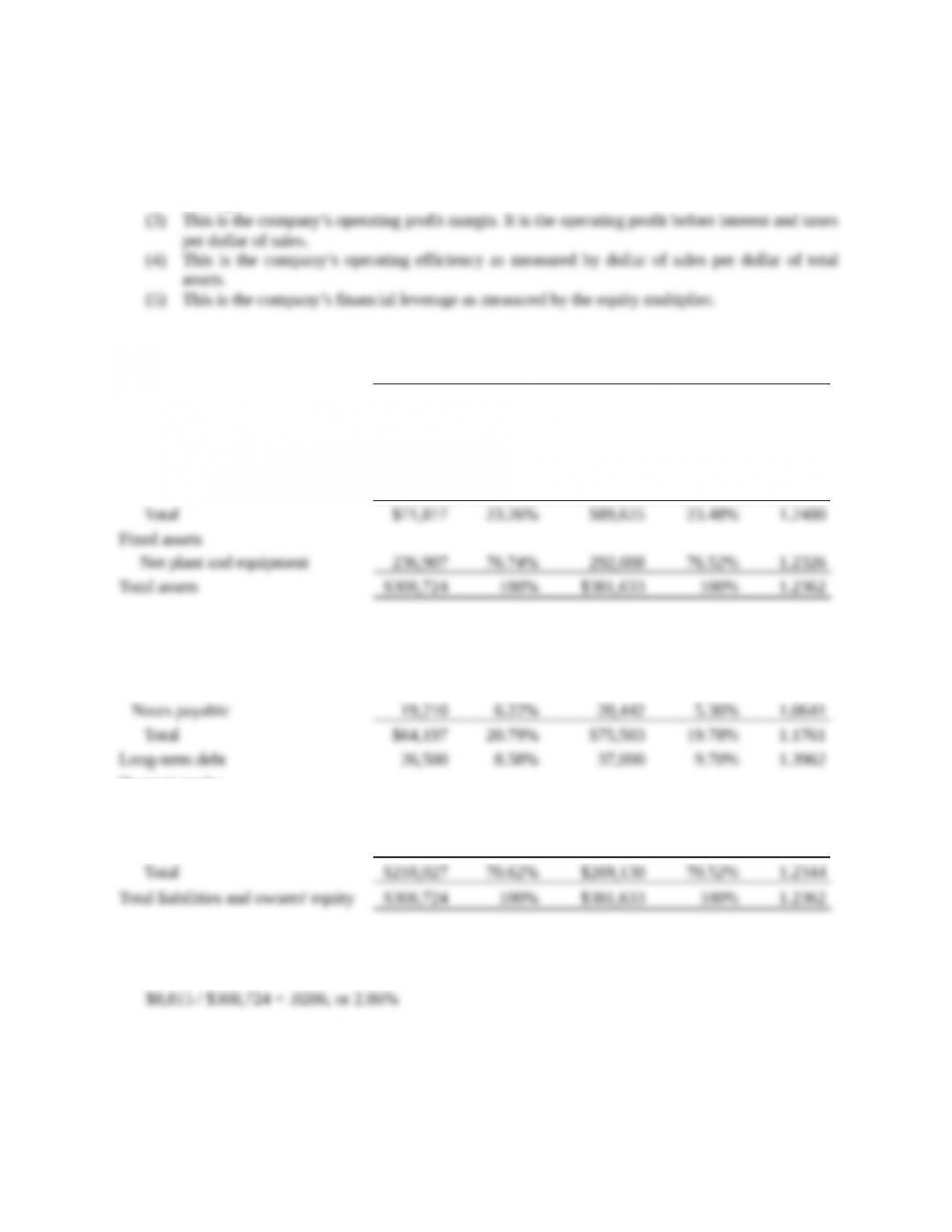

18. 2014

Common

size 2015

Common

size

Common

base year

Assets

Current assets

Cash $8,815 2.86% $11,945 3.13% 1.3551

Accounts receivable 22,498 7.29% 27,524 7.21% 1.2234

Inventory 40,504 13.12% 50,156 13.14% 1.2383

Liabilities and Owners’ Equity

Current liabilities

Accounts payable $44,987 14.57% $55,061 14.43% 1.2239

Owners' equity

Common stock and paid-in

surplus $42,000 13.60% $43,500 11.40% 1.0357

Accumulated retained earnings 176,027 57.02% 225,630 59.12% 1.2818

The common-size balance sheet answers are found by dividing each category by total assets. For

example, the cash percentage for 2014 is:

This means that cash is 2.86 percent of total assets.

The common-base year answers for Question 18 are found by dividing each category value for 2015

by the same category value for 2014. For example, the cash common-base year number is found by:

19. To determine full capacity sales, we divide the current sales by the capacity the company is currently

using, so:

Full capacity sales = $680,000 / .90

20. To find the new level of fixed assets, we need to find the current percentage of fixed assets to full

capacity sales. Doing so, we find:

Fixed assets / Full capacity sales = $640,000 / $755,556

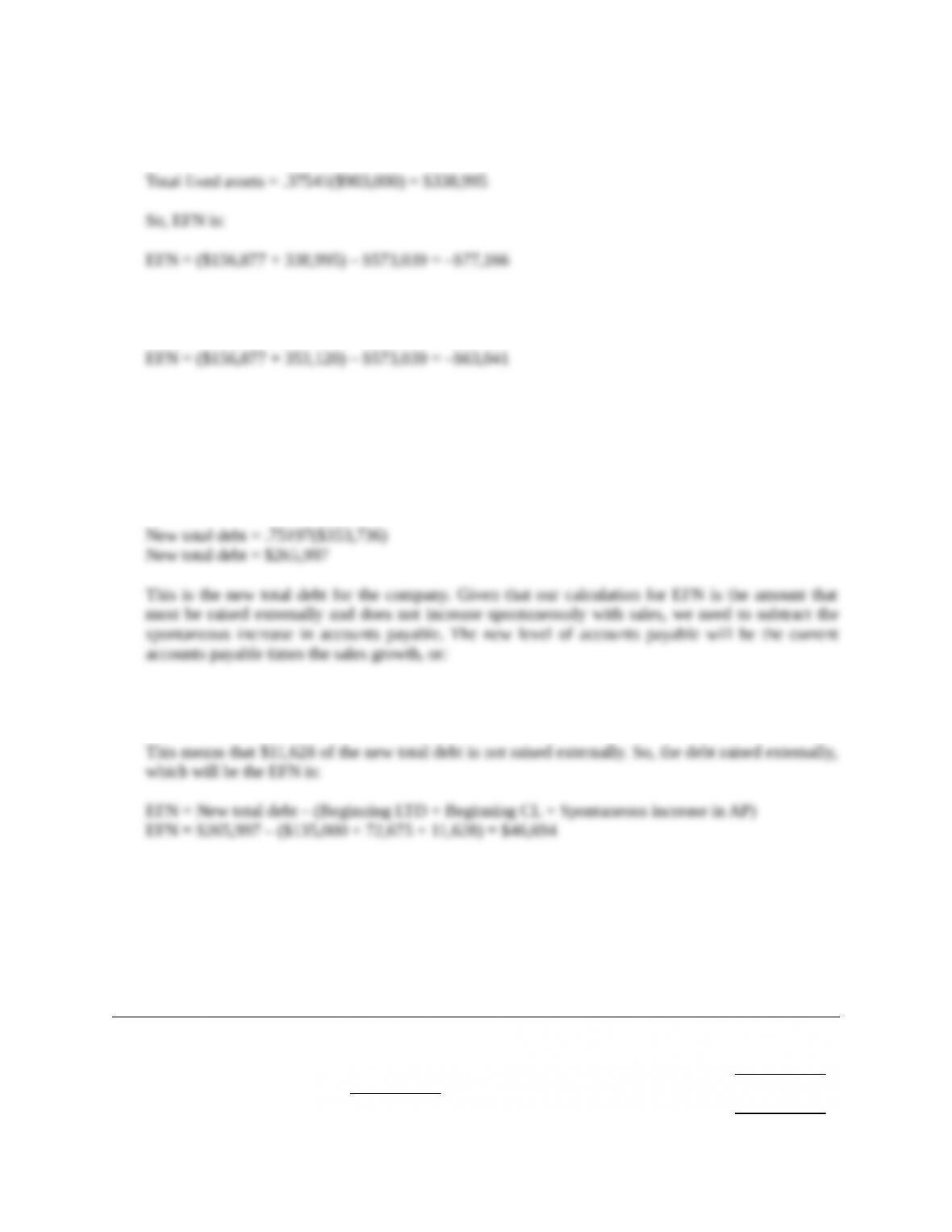

21. Assuming costs vary with sales and a 20 percent increase in sales, the pro forma income statement

will look like this:

MOOSE TOURS INC.

Pro Forma Income Statement

Sales $ 903,000

Costs 702,720

Other expenses 18,480

The payout ratio is constant, so the dividends paid this year is the payout ratio from last year times

net income, or:

Dividends = ($27,331 / $91,104)($110,799)

Dividends = $33,239

And the addition to retained earnings will be:

The pro forma balance sheet will look like this:

MOOSE TOURS INC.

Pro Forma Balance Sheet

Assets Liabilities and Owners’ Equity

Current assets Current liabilities

Cash $ 25,958 Accounts payable $ 69,768

Accounts receivable 41,759 Notes payable 14,535

Inventory 89,160 Total $ 84,303

Total $ 156,877 Long-term debt 135,000

So the EFN is:

EFN = Total assets – Total liabilities and equity

22. First, we need to calculate full capacity sales, which is:

Full capacity sales = $752,500 / .80

Full capacity sales = $940,625

The full capacity ratio at full capacity sales is:

The fixed assets required at full capacity sales is the full capacity ratio times the projected sales

level:

Note that this solution assumes that fixed assets are decreased (sold) so the company has a 100

percent fixed asset utilization. If we assume fixed assets are not sold, the answer becomes:

23. The D/E ratio of the company is:

D/E = ($72,675 + 135,000) / $276,176

D/E = .75197

So the new total debt amount will be:

Spontaneous increase in accounts payable = $58,140(.20)

Spontaneous increase in accounts payable = $11,628

The pro forma balance sheet with the new long-term debt will be:

MOOSE TOURS INC.

Pro Forma Balance Sheet

Assets Liabilities and Owners’ Equity

Current assets Current liabilities

Cash $ 25,958 Accounts payable $ 69,768

Accounts receivable 41,759 Notes payable 14,535

Inventory 89,160 Total $ 84,303

Total $ 156,877 Long-term debt 181,694

The funds raised by the debt issue can be put into an excess cash account to make the balance sheet

balance. The excess debt will be:

Excess debt = $580,621 – 619,733 = $39,111

To make the balance sheet balance, the company will have to increase its assets. We will put this

amount in an account called excess cash, which will give us the following balance sheet:

MOOSE TOURS INC.

Pro Forma Balance Sheet

Assets Liabilities and Owners’ Equity

Current assets Current liabilities

Cash $ 25,958 Accounts payable $ 69,768

Excess cash 39,111

Accounts receivable 41,759 Notes payable 14,535

The excess cash has an opportunity cost that we discussed earlier. Increasing fixed assets would also

not be a good idea since the company already has enough fixed assets. A likely scenario would be the

repurchase of debt and equity in its current capital structure weights. The company’s debt-assets and

equity-assets are:

So, the repurchases of debt and equity will be:

Assuming all of the debt repurchase is from long-term debt, and the equity repurchase is entirely

from the retained earnings, the final pro forma balance sheet will be:

MOOSE TOURS INC.

Pro Forma Balance Sheet

Assets Liabilities and Owners’ Equity

Current assets Current liabilities

Cash $ 25,958 Accounts payable $ 69,768

Accounts receivable 41,759 Notes payable 14,535

Inventory 89,160 Total $ 84,303

Challenge