Slide 3.14 Using Financial Statements

Ratios cannot be interpreted in isolation, but are rather to be

considered as comparative metrics – either across time or between

firms.

Lecture Tip: What is “EEBS”? Under the heading “A Wire Story We’d Like

to See,” those people at Fortune magazine have proposed a new

earnings metric: EEBS, or “Earnings Excluding Bad Stuff.” The

tongue-in-cheek article implies that, since Wall Street does not like

things that negatively impact earnings, firms should just report

earnings they would have made “if all this bad stuff hadn’t

happened” during the quarter. At first glance it sounds silly; on

the other hand, it may be the next logical step for those firms that

practice “income smoothing” and “earnings management.”

Lecture Tip: Here’s a tip for teaching about the interpretations of the PE

ratio, either in your discussion of ratios, or in your discussion of

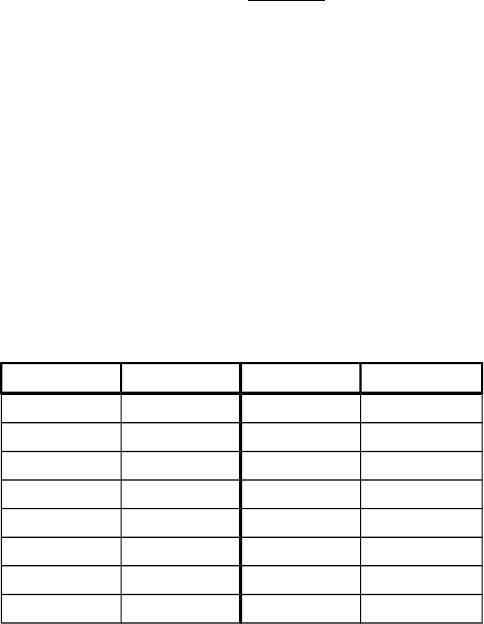

stock market history. Consider the table of year-end PE ratios for

the S&P 500 (courtesy of the S&P web site computed as Index / as

reported EPS):

Year PE Year PE

1988 11.69 1996 19.13

1989 15.45 1997 24.43

1990 15.47 1998 32.60

1991 26.12 1999 30.50

1992 22.82 2000 26.41

1993 21.31 2001 46.50

1994 15.01 2002 31.89

1995 18.14 2003 22.81

The average PE ratio over the 16-year period is 23.77. But what is the

average over a subset through time?

Period Average PE

1988 – 92 18.31

1993 – 97 19.60

1998 – 2003 31.79

Is the increase in market PE a secular trend or a fluke? What does this imply

for traditional measures of “overvaluation” such as the market

PE? And if the benchmark market PE is higher than it used to be,

what does that suggest for the interpretation of company PEs?

Obviously, the high PE in the latest period was a cyclical value, as

subsequent years (particularly given the credit crisis of the late

2000s) have seen a drop to lower levels, even below the other time

period averages reported in the table above. In fact, even with the

market recovery following the credit crisis, the S&P500 PE ratio

as of June 2015 was 19.

Lecture Tip: A Wall Street Journal article suggested that accounting methods

and ratio analysis may require some rethinking in the “new era”

in which we seem to be living. Specifically, an article entitled

“Bulls Use Convoluted Measures to Justify View” from the April

20, 1998, issue notes that “By almost any standard measure of

stock value, Friday’s record closes leave large stocks trading at or

beyond history’s most extreme limits of valuation.” [Note to the

cautious reader: when the WSJ article was written, the DJIA was

at 9167.50; it went as high as 11,500 in early 2000, dropped to

about 7900 after the terrorist attacks on September 11, 2001, was

back to almost 10,400 following the election in early November

2004, and closed around 8,000 at the end of 2008. ]

In any event, the article notes that the bull market of the 1990s

was attributable in large part to nearly divine macroeconomic

conditions – low inflation, low interest rates, and increasing

productivity. Put another way, the traditional valuation

benchmarks – historical price-earnings ratios, market-to-book

ratios, and dividend yields, as well as the underlying accounting

data – require careful consideration.

Lecture Tip: There are the “official” earnings estimates, compiled by First

Call, and then there are the “unofficial” estimates or “whisper

numbers.” Money Daily, in November 1998 called whisper

numbers “unofficial, unsubstantiated and unattributed forecast[s]

derived from rumors, hints and often, innuendo.” Academic

studies suggest that whisper numbers (which are often

disseminated via the Internet) “are a better proxy for market

expectations and are more accurate than consensus numbers.”

(Purdue University professor Susan Watts, quoted in the same

Money Daily article.) Another common term on Wall Street is

“visibility.” This term refers to the ability of management and

analysts to forecast earnings for future quarters. The more

confident they are about their estimates, the more “visibility” that

exists. Of course, visibility was much better when the economy was

good. When the economy began to slow down, visibility vanished.

It ties back to “EEBS.” In a down economy, companies do not

want to predict bad earnings very far into the future, but they are

more than willing to project good earnings for an extended

number of quarters during a good economy.

Lecture Tip: Ask the students to consider how the market-to-book ratio could

be interpreted if you are considering the purchase of a company’s

stock. Some feel a ratio of less than one would be preferred since

the stock is selling below its book value. You can point out that the

market is evaluating the company’s future earnings power, while

the book value reflects the price at which stock had previously

been issued and the earnings that had been retained in the firm.

Valuation techniques concerning a company’s future earnings will

be explored in later chapters (as will capital market efficiency and

security valuation).

3.3 The DuPont Identity

.A A Closer Look at ROE

The DuPont Identity provides analysts with a way to break down ROE and

investigate what areas of the firm need improvement.

Slide 3.15 The DuPont Identity

ROE = (NI / total equity)

multiply by one (assets / assets) and rearrange

ROE = (NI / assets) (assets / total equity) = ROA*EM

multiply by one (sales / sales) and rearrange

ROE = (NI / sales) (sales / assets) (assets / total equity)

ROE = PM*TAT*EM

Slide 3.16 Using the DuPont Identity

These three ratios indicate that a firm’s return on equity depends

on its operating efficiency (profit margin), asset use efficiency

(total asset turnover) and financial leverage (equity multiplier).

Slide 3.17 Calculating the DuPont Identity

Lecture Tip: The development of financial statement analysis is

rooted in a manufacturing tradition, with the large industrial

corporation at its center. Many notions about financial statement

analysis grew out of a view of business in which specialized plant

and equipment are used to turn raw materials into finished goods

that are then sold on credit. This view was modified by the advent

of the large retail corporation, but the emphasis on balance sheet

assets (receivables, inventories, plant and equipment) and the

measures associated with them remain.

Because of this manufacturer/retailer tradition, much of the

conventional wisdom about statement analysis is inappropriate to

many of today’s business situations. This is even more true when

we consider the advent of the “dot.com’s.” Good examples of firms

that do not fit the traditional mold are the professional

organizations formed by doctors, consultants, attorneys, etc., or

other service companies such as television and radio stations and

colleges and universities. The most important assets for these firms

are the people, and they do not show up on the balance sheet.

Their liquidity does not come from current assets but from the

services provided. Financial statements will eventually evolve, but

it is important to understand where we are starting from.

B. Problems with Financial Statement Analysis

Slide 3.18 Potential Problems

-no underlying financial theory

-finding comparable firms

-what to do with conglomerates, multidivisional firms

-differences in accounting practices

-differences in capital structure

-seasonal variations, one-time events

Lecture Tip: While some investors use PE ratios as if they are universally

comparable, differences in generally accepted accounting

practices used to compute EPS make international comparisons

risky. For example, the conventional wisdom for many years was

that the high PE ratios of Japanese stocks was due in part to the

more conservative nature of Japanese accounting practices which

depressed reported earnings and increased PEs.

An interesting discussion of this issue appeared in the November 14, 1988,

Pensions and Investment Age. Gary Schieneman, Vice President –

International Equity Research with Prudential-Bache applied US

accounting standards to 25 Japanese firms in 17 industries and

found little evidence of a systematic downward bias in reported

earnings. But, Paul Aron, Vice-Chairman emeritus of Daiwa

Securities countered by suggesting that, after adjusting for

methodological problems, 75% of the firms in Mr. Schieneman’s

sample did underreport earnings. Regardless of who is correct, the

most telling aspect of the discussion is Mr. Schieneman’s comment

in summing up: “I don’t think earnings mean a whole lot in

Japan.”

Ethics Note: An interesting example of an additional problem

faced by professional analysts is demonstrated by the Trump-

Roffman case. In 1990, Marvin Roffman, an analyst at Janney

Montgomery Scott, Inc. stated in a Wall Street Journal article that,

on the basis of his examination of the financial data, he had

“severe reservations about the future” of the Trump Taj Mahal in

Atlantic City. In response, Donald Trump threatened to sue Janney

Montgomery Scott. Roffman wrote, and then retracted, a

public apology to Trump and was dismissed. He successfully sued and

received a large settlement. Nonetheless, his case illustrates the

dangers one faces as a practicing analyst. (For further details, see

the New York Times, June 6, 1991.)

Lecture Tip: The explosion of the Internet has placed financial information in

the hands of millions of individuals and has increased the speed

with which information is obtained by professionals. Many

companies now webcast their earnings conference calls. This

information used to only be directly available to analysts, who

then passed selected information on to their clients. There is also

more opportunity for false information to be spread quickly. An

excellent example is the case of Emulex and a phony press release.

On Friday, August 25, 2000, someone issued a press release

indicating that the CEO of Emulex was quitting and that quarterly

earnings would be restated from a profit to a loss. The stock price

immediately plunged 62 percent. Mark Jakob has been arrested for

releasing the phony press release. His motive was apparently to

cover substantial losses from a short position in Emulex. The

Internet and other financial news sources disseminated the

information from the press release much faster than would have

been possible in the past. This is an excellent opportunity to

introduce the subject of efficient markets. If information is more

readily available, it should be incorporated into the price more

quickly, thereby increasing market efficiency. There is a trade-off,

however. False information can also be incorporated very quickly,

so investors need to remember the old adage “you can’t believe

everything you read.”

3.4 Financial Models

Slide 3.19 Financial Models

Financial planning is based on the three areas of corporate finance that were

discussed in chapter one: capital budgeting decisions, capital structure

decisions, and working capital management.

.A A Simple Financial Planning Model

Slide 3.20 Financial Planning Ingredients

Sales Forecast – most other considerations depend upon the sales forecast, so

it is said to “drive” the model

Pro Forma Statements – the output summarizing different projections

Asset Requirements – investment needed to support sales growth

Financial Requirements – debt and dividend policies

The “Plug” – designated source(s) of external financing

Economic Assumptions – state of the economy, anticipated changes in interest

rates, inflation, etc.

.B The Percentage of Sales Approach

Slide 3.21 –

Slide 3.22 Percent of Sales Approach

Sales generate retained earnings (unless all income is paid out in dividends).

Retained earnings, plus external funds raised, support an increase

in assets. More assets lead to more sales, and the cycle starts again.

This simplified approach assumes that certain items are fixed and

other vary proportionally with sales. Once forecasted, you must

select a plug account that will be used to make the balance sheet

balance. This number generally reflects External Financing Needed

(EFN).

Lecture Tip: An interesting discussion can be started by asking the

question, “Does a company’s capacity level affect the percentage

of sales approach?”

Lecture Tip: In the first two chapters of the text, we have described “the

financing decision” in one of two ways: either in broad terms,

referring simply to the means by which funding is acquired to

accomplish our investment objectives, or specific terms, i.e.,

capital structure. At this point, the financing decision is

characterized in another way: as one aspect of the day-to-day

operations of the business. You may wish to take this opportunity

to set the stage for the material on working capital management to

be covered in subsequent chapters. Specifically, it can be helpful to

introduce the concept of “spontaneous” financing (financing that arises in the

normal course of business, requires little face-to-face negotiation

with the lender and is less likely to result in bankruptcy

proceedings in case of default). Students should be reminded that

while long-term financing decisions may have greater potential

impacts on firm value, they are made relatively infrequently. Short-

term investment and financing decisions are made continuously

and affect the daily cash flows of the business.

Slide 3.23 Percent of Sales and EFN

An alternative method for calculating EFN is to use a formula

approach, where we subtract expected increases in (spontaneous)

liabilities and equity from the expected increase in assets.

EFN =

3.6 External Financing and Growth

Slide 3.24 External Financing and Growth

All else equal, more growth means more external financing will be

needed.

Lecture Tip: You might point out that the relationship between firm

growth and external financing needs is of utmost importance to firms in

the early stages of their lives. Typically, these are firms that have

developed a new product or technology, are experiencing rapid sales

growth, have continuing capital needs, and must be extremely careful in

forecasting cash flows. Since many of these firms are relatively small

and/or new, their financing problems are often exacerbated by a lack of

access to the capital markets. As such, the “internal growth rate” and

“sustainable growth rate” concepts are of particular importance to

financial decision-makers.

.A EFN and Growth

Lecture Tip: For new firms, internal financing is often virtually zero,

particularly if the product or service being developed has not yet

been marketed to the public. External financing is, therefore, the

only significant source of funds and may come from venture

capitalists, banks, “angels,” or family and friends. Should you

)1(Sales) Projected(ΔSales

Sales

LiabSpon

Sales

Sales

Assets dPM

wish to digress a bit and discuss the concept of “angel investors,” who often

provide capital to start-ups before venture capitalists become

involved, you will find a good hands-on article in the April 1996

issue of Worth magazine. There are also plenty of online resources

that can shed light on this issue.

Assuming no spontaneous sources of funds, EFN equals the increase in total

assets less the addition to retained earnings.

Low growth firms will run a surplus that causes a decline in the debt-to-equity

ratio. As the growth rate increases, the surplus becomes a deficit,

and the firm will need external financing.

.B Financial Policy and Growth

Slide 3.25 The Internal Growth Rate

The Internal Growth Rate (IGR) is the growth rate the firm can maintain with

internal financing only.

IGR = (ROA*b) / [1 – ROA*b]

Slide 3.26 The Sustainable Growth Rate

The Sustainable Growth Rate (SGR) is the maximum growth rate a firm can

achieve without external equity financing, while maintaining a

constant debt-to-equity ratio.

SGR = (ROE*b) / [1 – ROE*b]

Lecture Tip: Some students will wonder why managers would wish to avoid

issuing equity to meet anticipated financing needs. This is a good

opportunity to bring in concepts from previous chapters

(stockholder/bondholder conflicts of interest and agency costs), as

well as to introduce topics to be covered in future chapters

(information asymmetry and signaling, flotation costs, high cost of

equity and corporate governance).

Slide 3.27 Determinants of Growth

Determinants of growth – From the DuPont identity, ROE can be viewed as

the product of profit margin, total asset turnover, and the equity

multiplier. Anything that increases ROE will increase the

sustainable growth rate as well. Therefore, the sustainable growth

rate depends on the following four factors:

Operating efficiency – profit margin

Asset use efficiency – total asset turnover

Financial leverage – equity multiplier

Dividend policy – retention ratio

Lecture Tip: Wanting sales or revenues to grow by X% per year as

a goal of the firm is properly understood as meaning: “All else

equal, we want sales to grow.” Here are some things to consider:

-Cutting margins might make sales grow – but is it good for the firm?

-Using more assets may make sales grow, but is this truly

increasing efficiency?

-Increasing financial leverage might pay for growth – but can

the firm survive?

-Cutting the dividend might pay for growth – but is it what stockholders

want?

.C A Note about Sustainable Growth Rate Calculations

The sustainable growth rate that we commonly see in other texts or

applications is ROE*b – why is it different? The formula that is

used throughout the text is based on an ROE that is computed

using ending balance sheet numbers for equity. The “simpler”

formula is appropriate only when the ROE is computed using

beginning equity balance sheet numbers.

3.7 Some Caveats Regarding Financial Planning Models

Slide 3.28 Some Caveats

The main problem is that the models are really accounting statement

generators rather than determinants of value. As we will see, value is

determined by cash flows, timing and risk; and these financial planning

models do not address any of these issues.

Slide 3.29 –

Slide 3.30 Quick Quiz

Appendix: Useful Financial Ratios

SHORT-TERM SOLVENCY RATIOS

Current ratio = Current assets ÷ Current liabilities

Quick ratio = (Current assets – Inventory) ÷ Current liabilities

Cash ratio = Cash ÷ Current liabilities

FINANCIAL LEVERAGE RATIOS

Total debt ratio = Total debt ÷ Total assets = (Total assets – Total equity) ÷ Total assets

Debt-equity ratio = Total debt ÷ Total equity

Equity multiplier = Total assets ÷ Total equity = 1 + debt-equity ratio

Times interest earned = Earnings before interest and taxes ÷ Interest

Cash coverage = (Earnings before interest and taxes + depreciation + amortization) ÷

Interest

TURNOVER RATIOS

Inventory turnover = Cost of goods sold ÷ Inventory

Days sales in inventory = 365 ÷ Inventory turnover

Receivables turnover = Sales ÷ Receivables

Days’ sales in receivables= 365 ÷ Receivables turnover

Total asset turnover = Sales ÷ Total assets

Days in inventory = Days in period ÷ Inventory turnover

PROFITABILITY MEASURES

Profit margin = Net income ÷ Sales

Return on assets = Net income ÷ Total assets

Return on equity = Net income ÷ Total equity

EBITDA margin = EBITDA ÷ Sales

MARKET VALUE RATIOS

Price-to-earnings ratio = Market price per share ÷ Earnings per share

Market-to-book ratio = Market price per share ÷ Book value per share

Market capitalization = Market price per share x Shares Outstanding

Enterprise Value (EV) = Market capitalization + Market value of interest bearing debt –

cash

EV Multiple = EV ÷ EBITDA