CHAPTER 10

SOME LESSONS FROM CAPITAL

MARKET HISTORY

Answers to Concepts Review and Critical Thinking Questions

1. They all wish they had! Since they didn’t, it must have been the case that the stellar performance was

2. As in the previous question, it’s easy to see after the fact that the investment was terrible, but it

3. No, stocks are riskier. Some investors are highly risk averse, and the extra possible return doesn’t

4. Unlike gambling, the stock market is a positive sum game; everybody can win. Also, speculators

5. T–bill rates were highest in the early eighties. This was during a period of high inflation and is

6. Before the fact, for most assets, the risk premium will be positive; investors demand compensation

over and above the risk-free return to invest their money in the risky asset. After the fact, the

7. Yes, the stock prices are currently the same. Below is a diagram that depicts the stocks’ price

movements. Two years ago, each stock had the same price, P0. Over the first year, General Materials’

stock price increased by 10 percent, or (1.1) P0. Standard Fixtures’ stock price declined by 10

percent, or (.9) P0. Over the second year, General Materials’ stock price decreased by 10 percent,

8. The stock prices are not the same. The return quoted for each stock is the arithmetic return, not the

geometric return. The geometric return tells you the wealth increase from the beginning of the period

to the end of the period, assuming the asset had the same return each year. As such, it is a better

measure of ending wealth. To see this, assuming each stock had a beginning price of $100 per share,

the ending price for each stock would be:

9. To calculate an arithmetic return, you sum the returns and divide by the number of returns. As such,

10. Risk premiums are about the same whether or not we account for inflation. The reason is that risk

premiums are the difference between two returns, so inflation essentially nets out. Returns, risk

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Basic

1. The return of any asset is the increase in price, plus any dividends or cash flows, all divided by the

initial price. The return of this stock is:

2. The dividend yield is the dividend divided by the price at the beginning of the period, so:

And the capital gains yield is the increase in price divided by the initial price, so:

3. Using the equation for total return, we find:

And the dividend yield and capital gains yield are:

Here’s a question for you: Can the dividend yield ever be negative? No, that would mean you were

4. The total dollar return is the change in price plus the coupon payment, so:

The total nominal percentage return of the bond is:

Notice here that we could have used the total dollar return of $87 in the numerator of this equation.

Using the Fisher equation, the real return was:

5. The nominal return is the stated return, which is 11.80 percent. Using the Fisher equation, the real

return was:

6. Using the Fisher equation, the real returns for government and corporate bonds were:

(1 + R) = (1 + r)(1 + h)

7. The average return is the sum of the returns, divided by the number of returns. The average return for each

stock was:

¯

X=

[

∑

i=1

N

xi

]

/N=

[

. 09+.21−.27 +.15+. 23

]

5=. 0820, or 8 .20

¯

Y=

[

∑

i=1

N

yi

]

/N=

[

. 12+. 27−.32+. 14+. 36

]

5=. 1140, or 11. 40

We calculate the variance of each stock as:

σX2=

[

∑

i=1

N

(

xi−¯

x

)

2

]

/

(

N−1

)

σX2=1

5−1

{

(

. 09−. 082

)

2+

(

. 21−. 082

)

2+

(

−. 27−.082

)

2+

(

.15−. 082

)

2+

(

. 23−. 082

)

2

}

=. 04172

σY2=1

5−1

{

(

. 12−. 114

)

2+

(

. 27−. 114

)

2+

(

−. 32−. 114

)

2+

(

.14−. 114

)

2+

(

. 36−.114

)

2

}

=. 06848

The standard deviation is the square root of the variance, so the standard deviation of each stock is:

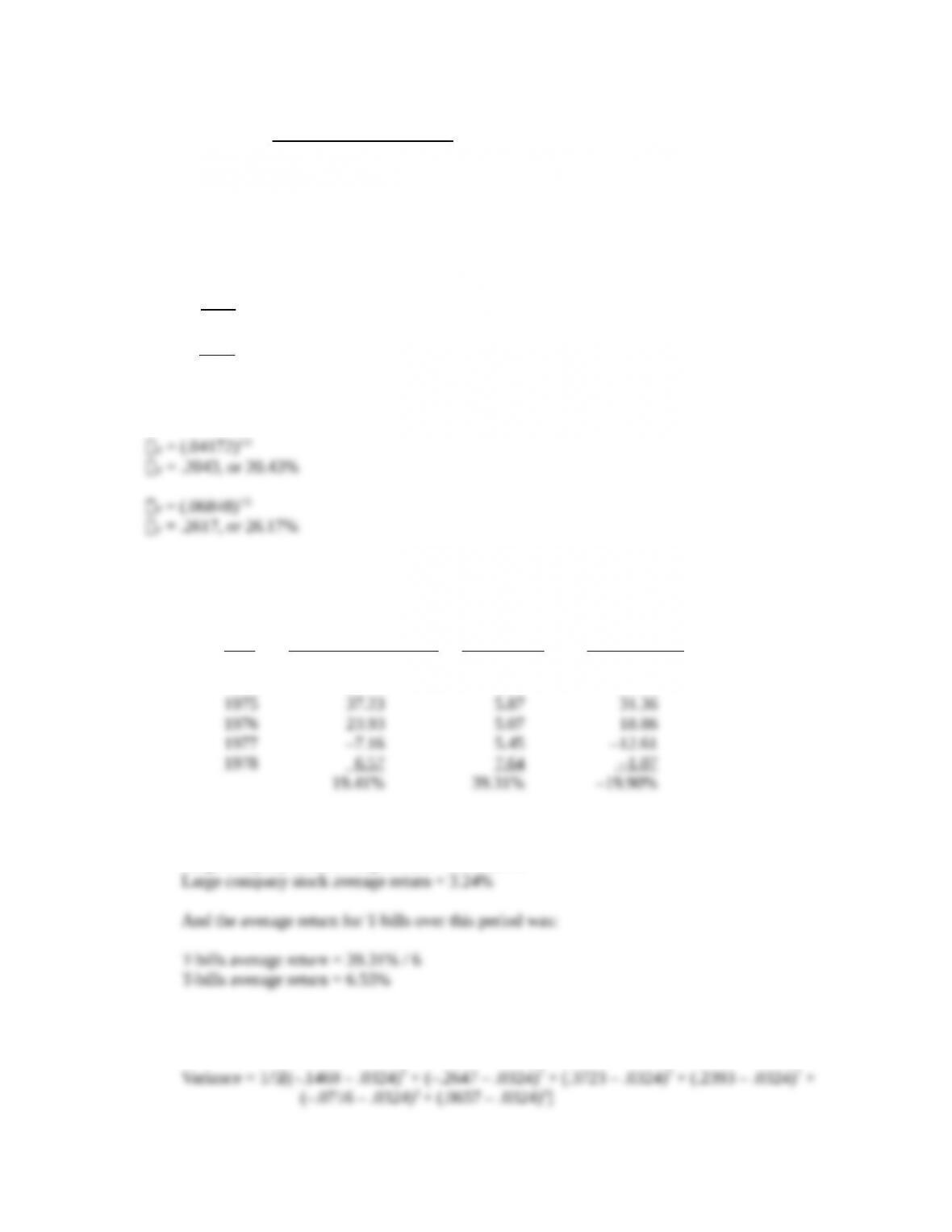

8. We will calculate the sum of the returns for each asset and the observed risk premium first. Doing so,

we get:

Year Large co. stock return T–bill return Risk premium

1973 –14.69% 7.29% 21.98%

1974 –26.47 7.99 –34.46

a. The average return for large company stocks over this period was:

Large company stock average return = 19.41% / 6

b. Using the equation for variance, we find the variance for large company stocks over this period

was:

And the standard deviation for large company stocks over this period was:

Using the equation for variance, we find the variance for T-bills over this period was:

And the standard deviation for T-bills over this period was:

c. The average observed risk premium over this period was:

Average observed risk premium = –19.90% / 6

(.1886 – (–.0332))2 + (–.1261 – (–.0332))2 + (–.0107 – (–.0332))2]

Variance = .062078

And the standard deviation of the observed risk premium was:

9. a. To find the average return, we sum all the returns and divide by the number of returns, so:

b. Using the equation to calculate variance, we find:

Variance = 1/4[(.21 – .122)2 + (.17 – .122)2 + (.26 – .122)2 + (–.07 – .122)2 +

(.04 – .122)2]

10. a. To calculate the average real return, we can use the average return of the asset and the average

inflation rate in the Fisher equation. Doing so, we find:

b. The average risk premium is the average return of the asset, minus the average real risk-free

rate, so, the average risk premium for this asset would be:

RP=R

–

Rf

RP

= .1220 – .0510

RP

= .0710, or 7.10%

11. We can find the average real risk-free rate using the Fisher equation. The average real risk-free rate

was:

And to calculate the average real risk premium, we can subtract the average risk-free rate from the

average real return. So, the average real risk premium was:

rp=r

–

rf

= 7.68% – .86%

rp

= 6.81%

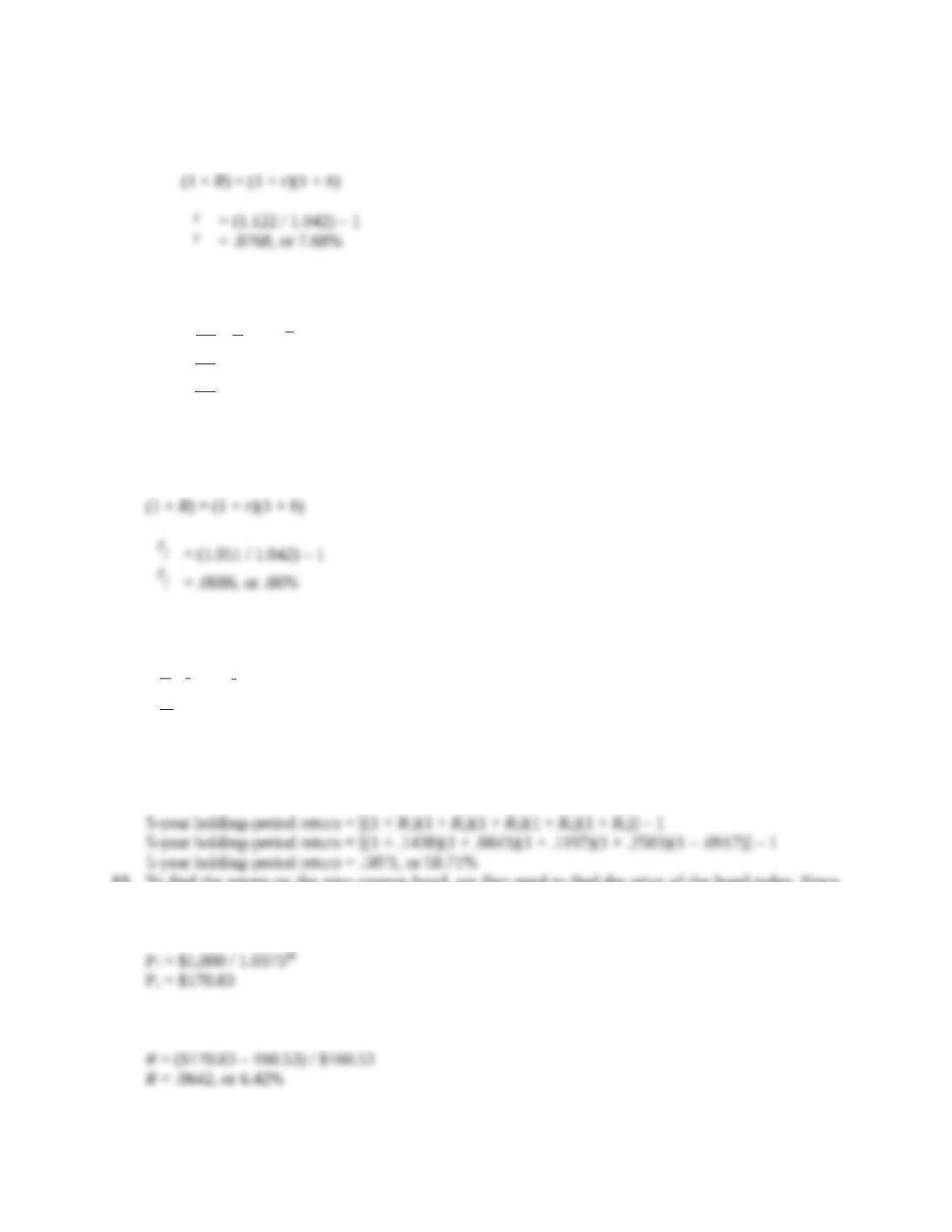

12. Applying the five-year holding-period return formula to calculate the total return of the stock over

the five-year period, we find:

13. To find the return on the zero coupon bond, we first need to find the price of the bond today. Since

one year has elapsed, the bond now has 24 years to maturity. Using semiannual compounding, the

price today is:

There are no intermediate cash flows on a zero coupon bond, so the return is the capital gain, or: