Chapter 11

RETURN AND RISK

THE CAPITAL ASSET PRICING MODEL (CAPM)

SLIDES

11.1 Key Concepts and Skills

11.2 Chapter Outline

11.3 Individual Securities

11.4 Expected Return, Variance, and Covariance

11.5 Expected Return

11.6 Expected Return

11.7 Variance

11.8 Variance

11.9 Standard Deviation

11.10 Covariance

11.11 Correlation

11.12 The Return and Risk for Portfolios

11.13 Portfolios

11.14 Portfolios

11.15 Portfolios

11.16 Portfolios

11.17 The Efficient Set for Two Assets

11.18 The Efficient Set for Two Assets

11.19 Portfolios with Various Correlations

11.20 The Efficient Set for Many Securities

11.21 The Efficient Set for Many Securities

11.22 Announcements, Surprises, and Expected Returns

11.23 Announcements, Surprises, and Expected Returns

11.24 Diversification and Portfolio Risk

11.25 Portfolio Risk and Number of Stocks

11.26 Risk: Systematic and Unsystematic

11.27 Total Risk

11.28 Optimal Portfolio with a Risk-Free Asset

11.29 Riskless Borrowing and Lending

11.30 Riskless Borrowing and Lending

11.31 Market Equilibrium

11.32 Market Equilibrium

11.33 Risk When Holding the Market Portfolio

11.34 Estimating β with Regression

11.35 The Formula for Beta

11.36 Relationship between Risk and Expected Return (CAPM)

11.37 Expected Return on a Security

11.38 Relationship Between Risk & Return

11.39 Relationship Between Risk & Return

11.40 Quick Quiz

CHAPTER ORGANIZATION

11.1 Individual Securities

11.2 Expected Return, Variance, and Covariance

Expected Return and Variance

Covariance and Correlation

11.3 The Return and Risk for Portfolios

The Expected Return on a Portfolio

Variance and Standard Deviation of a Portfolio

11.4 The Efficient Set for Two Assets

11.5 The Efficient Set for Many Securities

Variance and Standard Deviation in a Portfolio of Many Assets

11.6 Diversification

The Anticipated and Unanticipated Components of News

Risk: Systematic and Unsystematic

The Essence of Diversification

11.7 Riskless Borrowing and Lending

The Optimal Portfolio

11.8 Market Equilibrium

Definitions of the Market Equilibrium Portfolio

Definition of Risk When Investors Hold the Market Portfolio

The Formula for Beta

A Test

11.9 Relationship between Risk and Expected Return (CAPM)

Expected Return on Market

Expected Return on Individual Security

ANNOTATED CHAPTER OUTLINE

Slide 11.0 Chapter 11 Title Slide

Slide 11.1 Key Concepts and Skills

Slide 11.2 Chapter Outline

Lecture Tip: You may find it useful to emphasize the economic

foundations of the material in this chapter. Specifically, we assume:

-Investor rationality: Investors are assumed to prefer more money to

less and less risk to more, all else equal. The result of this assumption

is that the ex ante risk-return trade-off will be upward sloping.

-As risk-averse return-seekers, investors will take actions consistent

with the rationality assumptions. They will require higher returns to

invest in riskier assets and are willing to accept lower returns on less

risky assets.

-Similarly, they will seek to reduce risk while attaining the desired

level of return, or increase return without exceeding the maximum

acceptable level of risk.

Given the underlying assumptions above, this may be a good point at

which to discuss the increasingly popular field of behavioral finance. I.e.,

are investors rational?

1. Individual Securities

Characteristics include: expected return, variance, standard deviation,

covariance, and correlation.

Slide 11.3 Individual Securities

2. Expected Return, Variance, and Covariance

Slide 11.4 Expected Return, Variance, and Covariance

A. Expected Return and Variance

Let n denote the total number of states of the economy, Ri the return in

state i, and pi the probability of state i. Then the expected return,

R

−

, is

given by:

R

¿=∑

i=1

n

piRi

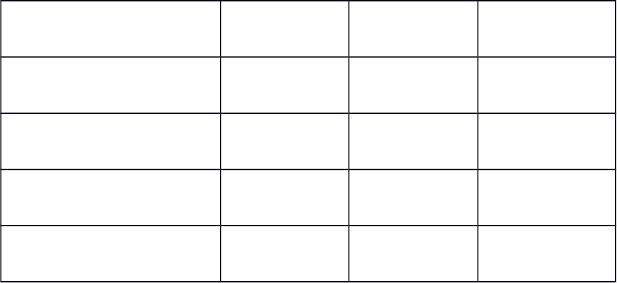

Example:

State of economy Probabilit

y

Return

(%)

Product

+1% change in

GDP

.25 -5 -1.25

+2% change in

GDP

.50 15 7.50

+3% change in

GDP

.25 35 8.75

Sums 1.00 E(R) =

15%

Slide 11.5 –

Slide 11.6 Expected Return

Variance measures the dispersion of points around the mean of a

distribution. In this context, we are attempting to characterize the

variability of possible future security returns around the expected return.

In other words, we are trying to quantify risk and return. Variance

measures the total risk of the possible returns.

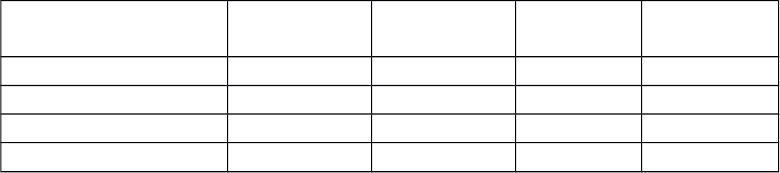

State of Economy Probability Return (%) Squared

Deviation

Product

(Dev*Prob)

+1% change in GDP .25 -5 400 100

+2% change in GDP .50 15 0 0

+3% change in GDP .25 35 400 100

Total 1.00 E(R) = 15 2 = 200

Standard deviation = square root of variance = 14.14%

Calculating the Variance

Var (R)=σ2=∑

i=1

n

pi(Ri−R

¿)2

Slide 11.7 –

Slide 11.8 Variance

Slide 11.9 Standard Deviation

Lecture Tip: Some students experience confusion in understanding the

mathematics of the variance calculation. They may have the feeling that

they should divide the variance of an expected return by (n-1). Point out

that the probabilities account for this division. We divide by n-1 in the

historical variance because we are looking at a sample. If we looked at

the entire population (which is what we are doing with expected values),

then we would divide by n (or multiply by 1/n) to get our historical

variance. This is the same as saying that the “probability” of occurrence

is the same for all observations and is equal to 1/n.

Lecture Tip: Each individual has their own level of risk tolerance. Some

people are just naturally more inclined to take risk, and they will not

require the same level of compensation as others for doing so. Our risk

preferences also change through time. We may be willing to take more risk

when we are young and without a spouse or kids. But, once we start a

family, our risk tolerance may drop.

B. Covariance and Correlation

Covariance is essentially a form of the variance calculation, but it

compares two assets rather than looking at a single security in isolation.

Take the deviation from the expected outcome for each security and

multiply them together. This replaces the squared deviation from the

variance calculation. From this point, the calculations are the same.

Slide 11.10 Covariance

The correlation standardizes the covariance by dividing by the product of

the standard deviations of the two assets. The result is a value between

positive 1 and negative 1.

Slide 11.11 Correlation

3. The Return and Risk for Portfolios

A portfolio is a collection of assets, such as stocks and bonds, held by an

investor.

Portfolios can be described by the percentage investment in each asset,

and these percentages are called portfolio weights.

Example: If two securities in a portfolio have a combined value of

$10,000 with $6000 invested in IBM and $4000 in GM, then the weight in

IBM = 6/10 = .6, and the weight in GM = 4/10 = .4.

Slide 11.12 The Return and Risk for Portfolios

A. The Expected Return on a Portfolio

The expected return on a portfolio is the sum of the product of the

expected returns on the individual securities and their portfolio weights.

Let wj be the portfolio weight for asset j and m be the total number of

assets in the portfolio; then

R

¿

p=∑

j=1

m

wjR

¿

j

This formula also works if you drop the expectations and just compute the

portfolio return in each state of the economy. This is useful for the

calculation of the portfolio variance in the next section.

Slide 11.13 –

Slide 11.14 Portfolios

B. Variance and Standard Deviation of a Portfolio

Portfolio Variance: Unlike expected return, the variance of a portfolio is

NOT the weighted sum of the individual security variances. Combining

securities into portfolios can reduce the total variability of returns.

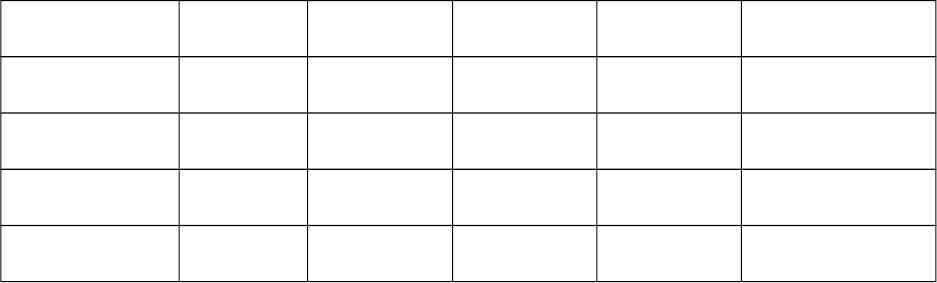

Example: Consider a portfolio with equal amounts invested in three

stocks:

State of

Economy

Probabilit

y

Return on A

(%)

Return on B

(%)

Return on C

(%)

Return on

Portfolio (%)

+1% change in

GDP

.25 -5 0 20 5

+2% change in

GDP

.50 15 10 10 11.7

+3% change in

GDP

.25 35 20 0 18.3

Expected

Return

15 10 10 11.7

Variances and standard deviations:

Var(A) = .25(-5-15)2 + .5(15-15)2 + .25(35-15)2 = 200

Std. Dev.(A) = 14.14

Var(B) = .25(0 – 10)2 + .5(10 – 10)2 + .25(20 – 10)2 = 50

Std. Dev.(B) = 7.07107

Var(C) = .25(20 – 10)2 + .5(10-10)2 + .25(0-10)2 = 50

Std. Dev.(C) = 7.07107

Var(portfolio) = .25(5-11.7)2 + .5(11.7-11.7)2 + .25(18.3-11.7)2 = 22.1125

Std. Dev.(portfolio) = 4.7024

Notice that the portfolio variance is less than any of the individual

variances.

Lecture Tip: In most business programs, a course in elementary statistics

is a prerequisite for the introductory finance course. And, while students

are sometimes fuzzy on the details, they usually remember the general

concept of the correlation coefficient (and hopefully the covariance). They

almost always remember that the correlation coefficient is bounded by –1

and 1. You may find it useful to reintroduce them to the correlation

concept here to deepen their understanding of portfolio variance.

Specifically, for a two-asset portfolio, the portfolio variance is equal

to:

w1

2σ1

2+ w2

2σ2

2+ 2w1w2σ1σ2ρ1,2

or w1

2σ1

2+ w2

2σ2

2+ 2w1w2σ1,2

where 1,2 is the correlation coefficient and 1,2 is the covariance. When

you expand the equation to more assets, you will have a variance term for

each asset and a covariance term for each pair of assets. As you increase

the number of assets, it is easy to see that the correlation (covariance)

between assets is much more important in determining the portfolio

variance than the individual variances.

Reconsider the previous example.

The following covariances can be computed:

cov(A,B) = 100

cov(A,C) = -100

cov(B,C) = -50

Using the covariances and extending the formula above to three assets,

you can compute a portfolio variance and standard deviation:

var = (1/3)2(200) + (1/3)2(50) + (1/3)2(50) + 2(1/3)(1/3)(100) + 2(1/3)

(1/3)(-100) + 2(1/3)(1/3)(-50) = 22.22

standard deviation = 4.71%

This is just as we computed earlier, with a slight difference due to

rounding portfolio returns.