25. Replacement decision analysis is the same as the analysis of two competing projects; in this case,

keep the current equipment, or purchase the new equipment. We will consider the purchase of the

new machine first.

Purchase new machine:

The initial cash outlay for the new machine is the cost of the new machine. We can calculate the

operating cash flow created if the company purchases the new machine. The maintenance cost is an

incremental cash flow, so using the pro forma income statement, and adding depreciation to net

income, the operating cash flow created each year by purchasing the new machine will be:

Notice the taxes are negative, implying a tax credit. The new machine also has a salvage value at the

end of five years, so we need to include this in the cash flows analysis. The aftertax salvage value

will be:

Notice the NPV is negative. This does not necessarily mean we should not purchase the new

machine. In this analysis, we are only dealing with costs, so we would expect a negative NPV. The

Keep old machine:

The initial cash outlay for the keeping the old machine is the market value of the old machine,

including any potential tax. The decision to keep the old machine has an opportunity cost, namely,

the company could sell the old machine. Also, if the company sells the old machine at its current

value, it will incur taxes. Both of these cash flows need to be included in the analysis. So, the initial

cash flow of keeping the old machine will be:

Next, we can calculate the operating cash flow created if the company keeps the old machine. We

need to account for the cost of maintenance, as well as the cash flow effects of depreciation. The pro

forma income statement, adding depreciation to net income to calculate the operating cash flow will

be:

The old machine also has a salvage value at the end of five years, so we need to include this in the

cash flows analysis. The aftertax salvage value will be:

The company should buy the new machine since it has a greater NPV.

There is another way to analyze a replacement decision that is often used. It is an incremental cash

flow analysis of the change in cash flows from the existing machine to the new machine, assuming

the new machine is purchased. In this type of analysis, the initial cash outlay would be the cost of the

new machine, and the cash inflow (including any applicable taxes) of selling the old machine. In this

case, the initial cash flow under this method would be:

The cash flows from purchasing the new machine would be the difference in the operating expenses.

We would also need to include the change in depreciation. The old machine has a depreciation of

$320,000 per year, and the new machine has a depreciation of $900,000 per year, so the increased

depreciation will be $580,000 per year. The pro forma income statement and operating cash flow

under this approach will be:

Net income –$45,000

Taxes –360,000

So, this analysis still tells us the company should purchase the new machine. This is really the same

type of analysis we originally did. Consider this: Subtract the NPV of the decision to keep the old

machine from the NPV of the decision to purchase the new machine. You will get:

26. Here we are comparing two mutually exclusive assets, with inflation. Since each will be replaced

when it wears out, we need to calculate the EAC for each. We have real cash flows. Similar to other

capital budgeting projects, when calculating the EAC, we can use real cash flows with the real

interest rate, or nominal cash flows and the nominal interest rate. Using the Fisher equation to find

the real required return, we get:

This is the interest rate we need to use with real cash flows. We are given the real aftertax cash flows

for each asset, so the NPV for the XX40 is:

And the EAC for the RH45 is:

27. The project has a sales price that increases at 3 percent per year, and a variable cost per unit that

increases at 4 percent per year. First, we need to find the sales price and variable cost for each year.

The table below shows the price per unit and the variable cost per unit each year.

Year 1 Year 2 Year 3 Year 4 Year 5

Using the sales price and variable cost, we can now construct the pro forma income statement for

each year. We can use this income statement to calculate the cash flow each year. We must also make

sure to include the net working capital outlay at the beginning of the project, and the recovery of the

net working capital at the end of the project. The pro forma income statement and cash flows for

each year will be:

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Revenues $860,000.00 $885,800.00 $912,374.00 $939,745.22 $967,937.58

Fixed costs 195,000.00 195,000.00 195,000.00 195,000.00 195,000.00

Variable costs 300,000.00 312,000.00 324,480.00 337,459.20 350,957.57

Capital

spending –$975,000

NWC –25,000 25,000

Total cash

flow –$1,000,000 $307,200.00 $316,308.00 $325,610.04 $335,108.77 $369,806.81

With these cash flows, the NPV of the project is:

We could also answer this problem using the depreciation tax shield approach. The revenues and

variable costs are growing annuities, growing at different rates. The fixed costs and depreciation are

ordinary annuities. Using the growing annuity equation, the present value of the revenues is:

And the present value of the variable costs will be:

The fixed costs and depreciation are both ordinary annuities. The present value of each is:

PV of fixed costs = C({1 – [1 / (1 + r)]t } / r )

PV of depreciation = C({1 – [1 / (1 + r)]t } / r )

Now, we can use the depreciation tax shield approach to find the NPV of the project, which is:

Challenge

28. Probably the easiest OCF calculation for this problem is the bottom up approach, so we will

construct an income statement for each year. Beginning with the initial cash flow at time zero, the

project will require an investment in equipment. The project will also require an investment in NWC

of $1,500,000. So, the cash flow required for the project today will be:

Now we can begin the remaining calculations. Sales figures are given for each year, along with the

price per unit. The variable costs per unit are used to calculate total variable costs, and fixed costs

are given at $1,850,000 per year. To calculate depreciation each year, we use the initial equipment

Year 1 2 3 4 5

Ending book value $16,713,450 $11,937,900 $8,527,350 $6,091,800 $4,350,450

Sales $27,945,000 $30,705,000 $33,465,000 $31,740,000 $26,565,000

Variable costs 15,390,000 16,910,000 18,430,000 17,480,000 14,630,000

Net cash flows

Operating cash flow $7,933,543 $9,435,693 $9,763,943 $8,918,943 $7,164,723

After we calculate the OCF for each year, we need to account for any other cash flows. The other

cash flows in this case are NWC cash flows and capital spending, which is the aftertax salvage of the

Notice that the NWC cash flow is negative. Since the sales are increasing, we will have to spend

more money to increase NWC. In Year 3, the NWC cash flow becomes positive when sales are

declining. And, in Year 5, the NWC cash flow is the recovery of all NWC the company still has in

the project.

To calculate the aftertax salvage value, we first need the book value of the equipment. The book

The market value of the used equipment is 20 percent of the purchase price, or $3.9 million, so the

aftertax salvage value will be:

The aftertax salvage value is included in the total cash flows as capital spending. Now we have all of

the cash flows for the project. The NPV of the project is:

IRR = 33.29%

We should accept the project.

29. To find the initial pretax cost savings necessary to buy the new machine, we should use the tax shield

approach to find the OCF. We begin by calculating the depreciation each year using the MACRS

depreciation schedule. The depreciation each year is:

D1 = $710,000(.3333) = $236,643

Using the tax shield approach, the OCF each year is:

OCF1 = (S – C)(1 – .35) + .35($236,643)

OCF2 = (S – C)(1 – .35) + .35($315,595)

Now we need the aftertax salvage value of the equipment. The aftertax salvage value is:

To find the necessary cost reduction, we must realize that we can split the cash flows each year. The

OCF in any given year is the cost reduction (S – C) times one minus the tax rate, which is an annuity

for the project life, and the depreciation tax shield. To calculate the necessary cost reduction, we

would require a zero NPV. The equation for the NPV of the project is:

30. To find the bid price, we need to calculate all other cash flows for the project, and then solve for the

bid price. The aftertax salvage value of the equipment is:

Now we can solve for the necessary OCF that will give the project a zero NPV. The equation for the

NPV of the project is:

The easiest way to calculate the bid price is the tax shield approach, so:

31. a. This problem is basically the same as the previous problem, except that we are given a sales

price. The cash flow at Time 0 for all three parts of this question will be:

We will use the initial cash flow and the salvage value we already found in that problem. Using

the bottom up approach to calculating the OCF, we get:

Assume price per unit = $18 and units/year = 165,000

Year 1 2 3 4 5

Sales $2,970,000 $2,970,000 $2,970,000 $2,970,000 $2,970,000

Variable costs 1,526,250 1,526,250 1,526,250 1,526,250 1,526,250

Fixed costs 450,000 450,000 450,000 450,000 450,000

Change in NWC 130,000

Capital spending 97,500

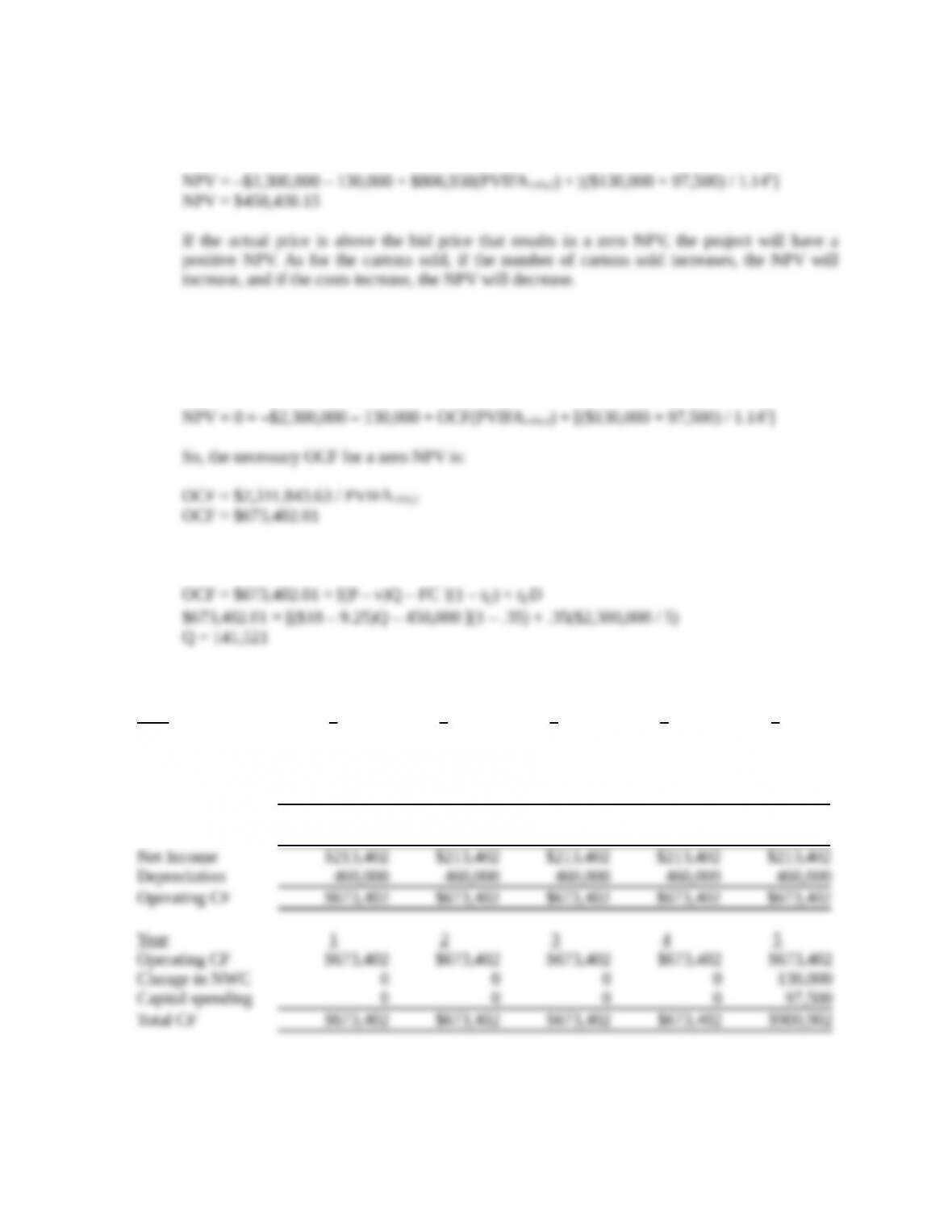

Total CF $806,938 $806,938 $806,938 $806,938 $1,034,438

With these cash flows, the NPV of the project is:

b. To find the minimum number of cartons sold to still breakeven, we need to use the tax shield

approach to calculating OCF, and solve the problem similar to finding a bid price. Using the

initial cash flow and salvage value we already calculated, the equation for a zero NPV of the

project is:

Now we can use the tax shield approach to solve for the minimum quantity as follows:

As a check, we can calculate the NPV of the project with this quantity. The calculations are:

Year 1 2 3 4 5

Sales $2,547,382 $2,547,382 $2,547,382 $2,547,382 $2,547,382

Variable costs 1,309,071 1,309,071 1,309,071 1,309,071 1,309,071

Fixed costs 450,000 450,000 450,000 450,000 450,000

Depreciation 460,000 460,000 460,000 460,000 460,000

EBIT $328,311 $328,311 $328,311 $328,311 $328,311

Taxes (35%) 114,909 114,909 114,909 114,909 114,909

NPV = –$2,300,000 – 130,000 + $673,402 (PVIFA14%,5) + [($130,000 + 97,500) / 1.145] $0

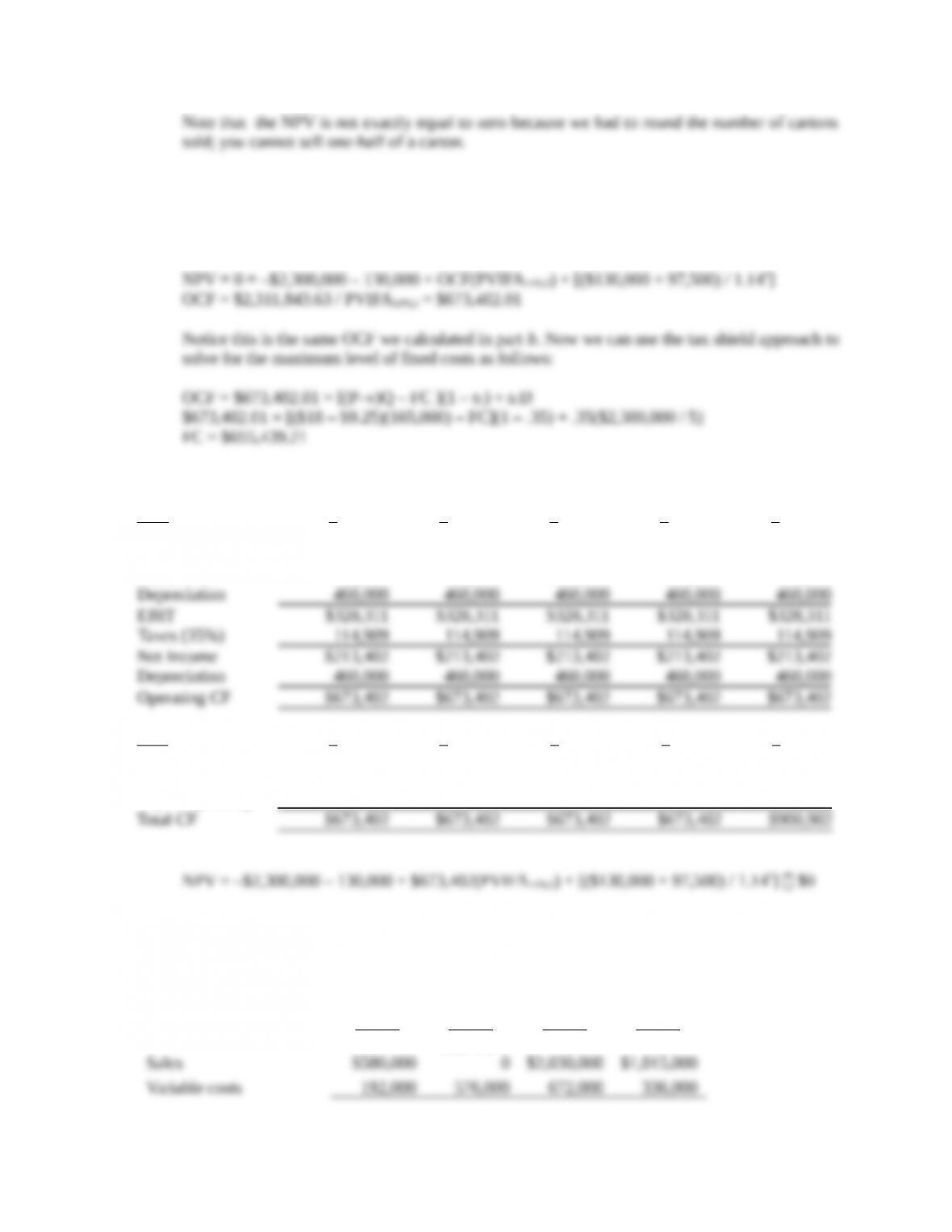

c. To find the highest level of fixed costs and still breakeven, we need to use the tax shield

approach to calculating OCF, and solve the problem similar to finding a bid price. Using the

initial cash flow and salvage value we already calculated, the equation for a zero NPV of the

project is:

As a check, we can calculate the NPV of the project with this quantity. The calculations are:

Year 1 2 3 4 5

Sales $2,970,000 $2,970,000 $2,970,000 $2,970,000 $2,970,000

Variable costs 1,526,250 1,526,250 1,526,250 1,526,250 1,526,250

Fixed costs 655,439 655,439 655,439 655,439 655,439

Year 1 2 3 4 5

Operating CF $673,402 $673,402 $673,402 $673,402 $673,402

Change in NWC 0 0 0 0 130,000

Capital spending 0 0 0 0 97,500

32. We need to find the bid price for a project, but the project has extra cash flows. Since we don’t

already produce the keyboard, the sales of the keyboard outside the contract are relevant cash flows.

Since we know the extra sales number and price, we can calculate the cash flows generated by these

sales. The cash flow generated from the sale of the keyboard outside the contract is:

Year 1 Year 2 Year 3 Year 4

$1,740,00

So, the addition to NPV of these market sales is:

You may have noticed that we did not include the initial cash outlay, depreciation, or fixed costs in

the calculation of cash flows from the market sales. The reason is that it is irrelevant whether or not

we include these here. Remember that we are not only trying to determine the bid price, but we are

also determining whether or not the project is feasible. In other words, we are trying to calculate the

NPV of the project, not just the NPV of the bid price. We will include these cash flows in the bid

price calculation. Whether we include these costs in this initial calculation is irrelevant since you will

come up with the same bid price if you include these costs in this calculation, or if you include them

in the bid price calculation.

Next, we need to calculate the aftertax salvage value, which is:

Instead of solving for a zero NPV as is usual in setting a bid price, the company president requires an

NPV of $100,000, so we will solve for an NPV of that amount. The NPV equation for this project is

(remember to include the NWC cash flow at the beginning of the project, and the NWC recovery at

the end):

Now we can solve for the bid price as follows: