CHAPTER 25

DERIVATIVES AND HEDGING RISK

SLIDES

22.1 Key Concepts and Skills

22.2 Chapter Outline

22.3 Forward Contracts

22.4 Futures Contracts

22.5 Futures Contracts

22.6 Daily Resettlement: An Example

22.7 Daily Resettlement: An Example

22.8 Daily Resettlement: An Example

22.9 Daily Resettlement: An Example

22.10 Selected Futures Contracts

22.11 Futures Markets

22.12 Wall Street Journal Futures Price Quotes

22.13 Basic Futures Relationships

22.14 Hedging

22.15 Hedging and Speculating: Example

22.16 Hedging: How many contracts?

22.17 Interest Rate Futures Contracts

22.18 Pricing of Treasury Bonds

22.19 Pricing of Treasury Bonds

22.20 Pricing of Forward Contracts

22.21 Pricing of Forward Contracts: Example

22.22 Pricing of Forward Contracts: Example

22.23 Pricing of Futures Contracts

22.24 Hedging in Interest Rate Futures

22.25 Duration Hedging

22.26 Duration Hedging

22.27 Duration Formula

22.28 Calculating Duration: Example

22.29 Calculating Duration: Example

22.30 Duration

22.31 Swaps Contracts

22.32 The Swap Bank

22.33 An Example of an Interest Rate Swap

22.34 An Example of an Interest Rate Swap

22.35 An Example of an Interest Rate Swap

22.36 An Example of an Interest Rate Swap

22.37 An Example of an Interest Rate Swap

22.38 An Example of an Interest Rate Swap

22.39 An Example of an Interest Rate Swap

25.40 An Example of an Interest Rate Swap

CHAPTER ORGANIZATION

22.1 Derivatives, Hedging, and Risk

22.2 Forward Contracts

22.3 Futures Contracts

22.4 Hedging

22.5 Interest Rate Futures Contracts

Pricing of Treasury Bonds

Pricing of Forward Contracts

Futures Contracts

Hedging in Interest Rate Futures

22.6 Duration Hedging

The Case of Zero Coupon Bonds

The Case of Two Bonds with the Same Maturity but with Different Coupons

Duration

Matching Liabilities with Assets

22.7 Swaps Contracts

Interest Rate Swaps

Currency Swaps

Credit Default Swaps

Exotics

22.8 Actual Use of Derivatives

22.40 An Example of an Interest Rate Swap

22.41 An Example of a Currency Swap

22.42 An Example of a Currency Swap

22.43 An Example of a Currency Swap

22.44 An Example of a Currency Swap

22.45 An Example of a Currency Swap

22.46 An Example of a Currency Swap

22.47 An Example of a Currency Swap

22.48 Credit Default Swaps

22.49 Variations of Basic Swaps

22.50 Risks of Interest Rate and Currency Swaps

22.51 Risks of Interest Rate and Currency Swaps

22.52 Pricing a Swap

22.53 Actual Use of Derivatives

22.54 Quick Quiz

ANNOTATED CHAPTER OUTLINE

Slide 25.0 Chapter 25 Title Slide

Slide 25.1 Key Concepts and Skills

Slide 25.2 Chapter Outline

1. Derivatives, Hedging, and Risk

The value of a derivative asset is “derived” from an underlying primary

asset. Derivatives can be used to change an individual’s or firm’s risk

exposure.

2. Forward Contracts

Slide 25.3 Forward Contracts

Forward contract – agreement between a buyer (long) and a seller (short)

for future delivery of an asset at a price specified today

Forward price – price agreed upon today to be paid at a future date when

delivery occurs

Settlement date – date when delivery occurs and the forward price is paid

(received)

Lecture Tip: In a forward contract, both parties are legally bound to

execute the transaction in the future at the agreed-upon price, but no

money changes hands at the inception of the contract. Here is an example

to help explain this concept to students.

Suppose you want to buy a new Ford Mustang convertible as soon as it

becomes available. You contract with the dealer to pay a specified price

on a specified future date (the delivery date). In essence, a private-market

forward contract has been created. You have a long position (buyer) in the

underlying asset (Mustang) and the Ford dealer has a short position

(seller).

Now suppose that after the contract is signed, demand for the car rises

so that the market value of the car increases above the agreed-upon price.

You have a document that gives you the

right to buy the asset at below market prices, and the dealer is obligated

to sell at that price. The “long” position wins because prices have

increased.

Suppose on the other hand, the economy worsens and the demand for

cars decreases. This drives the market value of the car lower. The dealer,

however, has a contract that forces you to pay the above market price. In

this case, the “short” position wins because prices have decreased.

What keeps either party from defaulting on the contract? This question

is a good lead-in to the discussion of futures, margin and marking-to-

market.

3. Futures Contracts

Slide 25.4 –

Slide 25.5 Futures Contracts

Futures contract – standardized forward contract traded only on an

exchange with gains and losses recognized on a daily basis

Slide 25.6 –

Slide 25.9 Daily Resettlement: An Example

Marking-to-market – process for daily recognizing gains and losses

Slide 25.10 Selected Futures Contracts

Typically, futures contracts are divided into two broad categories

– commodity contracts such as oil, gold, or wheat

– financial contracts such as T-bond or S&P 500

Slide 25.11 Futures Markets

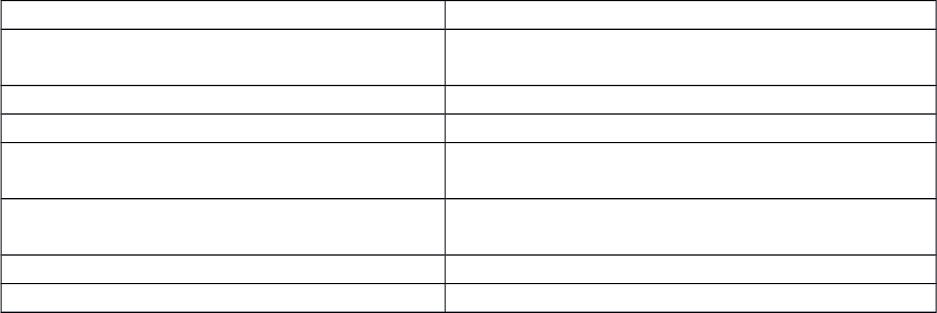

Lecture Tip: So what are the major differences between an OTC forward

contract and an exchange traded futures contract?

Forward Futures

Customized Standard features (delivery date, size of

contract, quality of asset, etc.)

Search cost – use dealers No search cost – contact broker

Low liquidity High liquidity

Higher default risk – limited to large,

creditworthy institutions

Virtually no default risk

No up-front or intermediate cash flows Initial margin requirements, daily marking-to-

market, margin calls

No Clearinghouse Clearinghouse that guarantees performance

Delivery normally occurs Majority of contracts offset, not delivered

Lecture Tip: How do we ensure that both parties fulfill their end of the

contract, particularly if there is a large price movement one way or the

other? The answer provides the main distinguishing characteristic

between straight forward contracts and futures contracts. The only

guarantees with a forward contract are the fear of litigation if one party

defaults and wanting to maintain a good reputation.

Suppose instead of entering into a forward contract with the dealer,

you enter into a futures contract with the Mustang as the underlying asset.

In this instance, both parties would deposit margin (or a good-faith

deposit) with an independent third party. Funds would then be transferred

back and forth between your account and the dealer’s account on a

regular basis as the price of the Mustang fluctuated. When it came time to

buy the car, any gain or loss would already be accounted for, thereby

reducing the likelihood of default.

Slide 25.12 Wall Street Journal Futures Price Quotes

Slide 25.13 Basic Futures Relationships

Settlement price – price at which contracts are marked-to-market and

determined by the settlement committee at each exchange, may or may not

equal the price at the last trade

Open interest – number of outstanding contracts

One problem with forward contracts is enforcing the agreement on the

delivery date. If the cash price on the delivery date is higher than the

agreed price, the seller has the incentive to default, and vice versa. Futures

contracts greatly reduce the risk of default relative to forward contracts by:

1. Having an exchange clearinghouse take one side of every

transaction.

2. Requiring an initial and a maintenance margin.

3. Marking to market on a daily basis.

4. Hedging

Slide 25.14 Hedging

Slide 25.15 Hedging and Speculating: Example

Slide 25.16 Hedging: How many contracts?

Hedging is the process of reducing risk, whether it be the risk of changing

prices, currency fluctuations, or changes in interest rates.

Speculating is the opposite of hedging, which implies it is the process of

increasing risk.

Both hedgers and speculators are necessary for an active, liquid

derivatives market.

While forward and futures contracts can be used for speculative purposes,

the chapter focuses on the use of these derivative securities to reduce risk.

Either side of a forward or futures contract can be used to hedge:

1. A short futures hedge involves selling a futures contract. Short hedges

are used when you will be making delivery of an asset at a future date

(e.g., a farmer anticipating a harvest of wheat) and wish to minimize the

risk of a drop in price.

2. A long futures hedge involves buying a futures contract. Long hedges are

used when you must purchase an asset at a future date (e.g., a bakery with

a demand for wheat) and wish to minimize the risk of a rise in price.

Lecture Tip: It may be beneficial to demonstrate a futures hedge and the

potential payoffs for a soybean farmer who anticipates a harvest of

100,000 bushels in September. Costs to produce the soybeans are incurred

long before the harvest, but the farmer is at risk that the price of soybeans

will fall before harvest time. To reduce this risk, the farmer takes a short

position (because he wants to sell the soybeans) in the futures contract.

This short position offsets the long position that he already has in

soybeans.

Futures contract terms are for 5,000 bushels, and the current futures

price is $4.50 per bushel. The farmer can lock in the delivery price of

soybeans at $4.50 for his harvest by shorting (selling) 20 soybean futures

contracts on June 1st. No cash changes hands today, although margin is

held in the farmer’s account. The 20 contracts represent delivery of

100,000 bushels. The cash flow at delivery is $4.50(100,000) = $450,000

Date Closing Farmer Net

06/01 no money changes hands

06/10 4.60 pay 10,000 (-.1*100,000) -10,000

06/15 4.40 receive 20,000 (.2*100,000) +10,000

06/30 4.20 receive 20,000 +30,000

07/20 4.30 pay 10,000 +20,000

08/05 4.40 pay 10,000 +10,000

08/16 4.20 receive 20,000 +30,000

09/01 4.20

The farmer will deliver the soybeans and receive $4.20 per bushel for

420,000 + 30,000 profit from the futures for a total cash inflow of

450,000.

If a bumper crop occurs and the farmer harvests 120,000 bushels, the

farmer will receive 450,000 for the first 100,000 and then an addition

20,000*4.20 = 84,000 for the extra.

Suppose instead there is a poor harvest and the farmer only has 70,000

bushels. But, because of the short supply, the price is $4.75 per bushel.

The farmer would realize a loss of 25,000 (.25*100,000) on the futures

contracts and would receive 70,000(4.75) = 332,500 for the sale of the

soybeans. His net profit would be $307,500. As this illustrates, the farmer

can only hedge price risk, not quantity risk.

5. Interest Rate Futures Contracts