CHAPTER 6 –

33. a. Since the two computers have unequal lives, the correct method to analyze the decision is the

EAC. We will begin with the EAC of the new computer. Using the depreciation tax shield

approach, the OCF for the new computer system is:

Notice that the costs are positive, which represents a cash inflow. The costs are positive in this

case since the new computer will generate a cost savings. The only initial cash flow for the new

computer is the cost of $580,000. We next need to calculate the aftertax salvage value, which

is:

And the EAC of the new computer is:

EAC = –$205,885.31 / (PVIFA14%,5) = –$59,971.00

Analyzing the old computer, the only OCF is the depreciation tax shield, so:

OCF = $90,000(.38) = $34,200

The initial cost of the old computer is a little trickier. You might assume that since we already

own the old computer there is no initial cost, but we can sell the old computer, so there is an

opportunity cost. We need to account for this opportunity cost. To do so, we will calculate the

This is the initial cost of the old computer system today because we are forgoing the

opportunity to sell it today. We next need to calculate the aftertax salvage value of the computer

system in two years since we are “buying” it today. The aftertax salvage value in two years is:

And the EAC of the old computer is:

EAC = – $133,944.23 / (PVIFA14%,2) = –$81,342.95

1

CHAPTER 6 –

b. If we are only concerned with whether or not to replace the machine now, and are not worrying

about what will happen in two years, the correct analysis is NPV. To calculate the NPV of the

decision on the computer system now, we need the difference in the total cash flows of the old

computer system and the new computer system. From our previous calculations, we can say the

cash flows for each computer system are:

tNew computer Old computer Difference

0 –$580,000 –$245,200 –$334,800

Since we are only concerned with marginal cash flows, the cash flows of the decision to replace

the old computer system with the new computer system are the differential cash flows. The

NPV of the decision to replace, ignoring what will happen in two years is:

34. To answer this question, we need to compute the NPV of all three alternatives, specifically, continue

to rent the building, Project A, or Project B. We would choose the project with the highest NPV. If all

There are several important cash flows we should not consider in the incremental cash flow analysis.

The remaining fraction of the value of the building and depreciation are not incremental and should

not be included in the analysis of the two alternatives. The $1,250,000 purchase price of the building

is the same for all three options and should be ignored. In effect, what we are doing is finding the

We will begin by calculating the NPV of the decision of continuing to rent the building first.

Continue to rent:

2

CHAPTER 6 –

Since there is no incremental depreciation, the operating cash flow is the net income. So, the NPV of

the decision to continue to rent is:

Product A:

Next, we will calculate the NPV of the decision to modify the building to produce Product A. The

income statement for this modification is the same for the first 14 years, and in Year 15, the company

will have an additional expense to convert the building back to its original form. This will be an

Initial cash outlay:

Building modifications –$115,000

Years 1-14 Year 15

Revenue $235,000 $235,000

Expenditures 85,000 85,000

The OCF each year is net income plus depreciation. So, the NPV for modifying the building to

manufacture Product A is:

Product B:

Now we will calculate the NPV of the decision to modify the building to produce Product B. The

income statement for this modification is the same for the first 14 years, and in Year 15, the company

will have an additional expense to convert the building back to its original form. This will be an

expense in Year 15, so the income statement for that year will be slightly different. The cash flow at

3

CHAPTER 6 –

time zero will be the cost of the equipment, and the cost of the initial building modifications, both of

which are depreciable on a straight-line basis. So, the pro forma cash flows for Product B are:

Initial cash outlay:

Years 1-14 Year 15

Revenue $265,000 $265,000

Expenditures 105,000 105,000

Depreciation 27,000 27,000

The OCF each year is net income plus depreciation. So, the NPV for modifying the building to

manufacture Product B is:

Since Product A has the highest NPV, the company should opt for that product.

We could have also done the analysis as the incremental cash flows between Product A and

NPV of differential cash flows between Product B and continuing to rent:

Since the differential NPV of Product A is positive and is the largest incremental NPV, the company

should choose Project A, which is the same as our original result.

35. The discount rate is expressed in real terms, and the cash flows are expressed in nominal terms. We

can answer this question by converting all of the cash flows to real dollars. We can then use the real

interest rate. The real value of each cash flow is the present value of the Year 1 nominal cash flows,

4

CHAPTER 6 –

discounted back to the present at the inflation rate. So, the real value of the revenue and costs will

be:

Revenues, labor costs, and other costs are all growing perpetuities. Each has a different growth rate,

so we must calculate the present value of each separately. Using the real required return, the present

value of each of these is:

The lease payments are constant in nominal terms, so they are declining in real terms by the inflation

Now we can use the tax shield approach to calculate the net present value. Since there is no

investment in equipment, there is no depreciation; therefore, no depreciation tax shield, so we will

ignore this in our calculation. This means the cash flows each year are equal to net income. There is

also no initial cash outlay, so the NPV is the present value of the future aftertax cash flows. The NPV

of the project is:

In general, we can answer capital budgeting problems in nominal terms as well. However, in this

case, the computation would have been impossible. The reason is that we are dealing with growing

perpetuities. In other problems, when calculating the NPV of nominal cash flows, we could calculate

36. We are given the real revenue and costs, and the real growth rates, so the simplest way to solve this

problem is to calculate the NPV with real values. While we could calculate the NPV using nominal

values, we would need to find the nominal growth rates, and convert all values to nominal terms. The

real labor costs will increase at a real rate of 2 percent per year, and the real energy costs will

increase at a real rate of 3 percent per year, so the real costs each year will be:

Year 1 Year 2 Year 3 Year 4

5

CHAPTER 6 –

Remember that the depreciation tax shield also affects a firm’s aftertax cash flows. The present value

of the depreciation tax shield must be added to the present value of a firm’s revenues and expenses to

Depreciation is a nominal cash flow, so to find the real value of depreciation each year, we discount

the real depreciation amount by the inflation rate. Doing so, we find the real depreciation each year

is:

Year 1 real depreciation = $36,250,000 / 1.05 = $34,523,809.52

Now we can calculate the pro forma income statement each year in real terms. We can then add back

depreciation to net income to find the operating cash flow each year. Doing so, we find the cash flow

of the project each year is:

Year 0 Year 1 Year 2 Year 3 Year 4

Revenues

$67,425,000.0

0

$76,125,000.0

0

$82,650,000.0

0

$73,950,000.0

0

Labor cost 18,200,000.00 19,890,000.00 22,992,840.00 22,073,126.40

Energy cost 798,000.00 880,650.00 1,028,012.10 996,567.02

Capital

spending

–

$145,000,000

6

CHAPTER 6 –

37. Here we have the sales price and production costs in real terms. The simplest method to calculate the

project cash flows is to use the real cash flows. In doing so, we must be sure to adjust the

depreciation, which is in nominal terms. We could analyze the cash flows using nominal values,

Headache only:

We can find the real revenue and production costs by multiplying each by the units sold. We must be

sure to discount the depreciation, which is in nominal terms. We can then find the pro forma net

income, and add back depreciation to find the operating cash flow. Discounting the depreciation each

year by the inflation rate, we find the following cash flows each year:

Year 1 Year 2 Year 3

Sales $24,800,000 $24,800,000 $24,800,000

Production costs 12,160,000 12,160,000 12,160,000

And the NPV of the headache only pill is:

Headache and arthritis:

For the headache and arthritis pill project, the equipment has a salvage value. We will find the

aftertax salvage value of the equipment first, which will be:

Market value $1,000,000

Remember, to calculate the taxes on the equipment salvage value, we take the book value minus the

market value, times the tax rate. Using the same method as the headache only pill, the cash flows

each year for the headache and arthritis pill will be:

Year 1 Year 2 Year 3

Sales $37,975,000 $37,975,000 $37,975,000

7

CHAPTER 6 –

EBT $5,656,764 $5,977,246 $6,288,395

Tax 1,923,300 2,032,264 2,138,054

So, the NPV of the headache and arthritis pill is:

The company should manufacture the headache and arthritis remedy since the project has a higher

NPV.

38. Since the project requires an initial investment in inventory as a percentage of sales, we will

calculate the sales figures for each year first. The incremental sales will include the sales of the new

table, but we also need to include the lost sales of the existing model. This is an erosion cost of the

new table. The lost sales of the existing table are constant for every year, but the sales of the new

table change every year. So, the total incremental sales figure for the five years of the project will be:

Year 1 Year 2 Year 3 Year 4 Year 5

New $11,590,000 $13,725,000 $16,470,000 $14,945,000 $14,030,000

Now we will calculate the initial cash outlay that will occur today. The company has the necessary

production capacity to manufacture the new table without adding equipment today. So, the

equipment will not be purchased today, but rather in two years. The reason is that the existing

capacity is not being used. If the existing capacity were being used, the new equipment would be

required, so it would be a cash flow today. The old equipment would have an opportunity cost if it

could be sold. As there is no discussion that the existing equipment could be sold, we must assume it

cannot be sold. The only initial cash flow is the cost of the inventory. The company will have to

spend money for inventory with the new table, but will be able to reduce inventory of the existing

table. So, the initial cash flow today is:

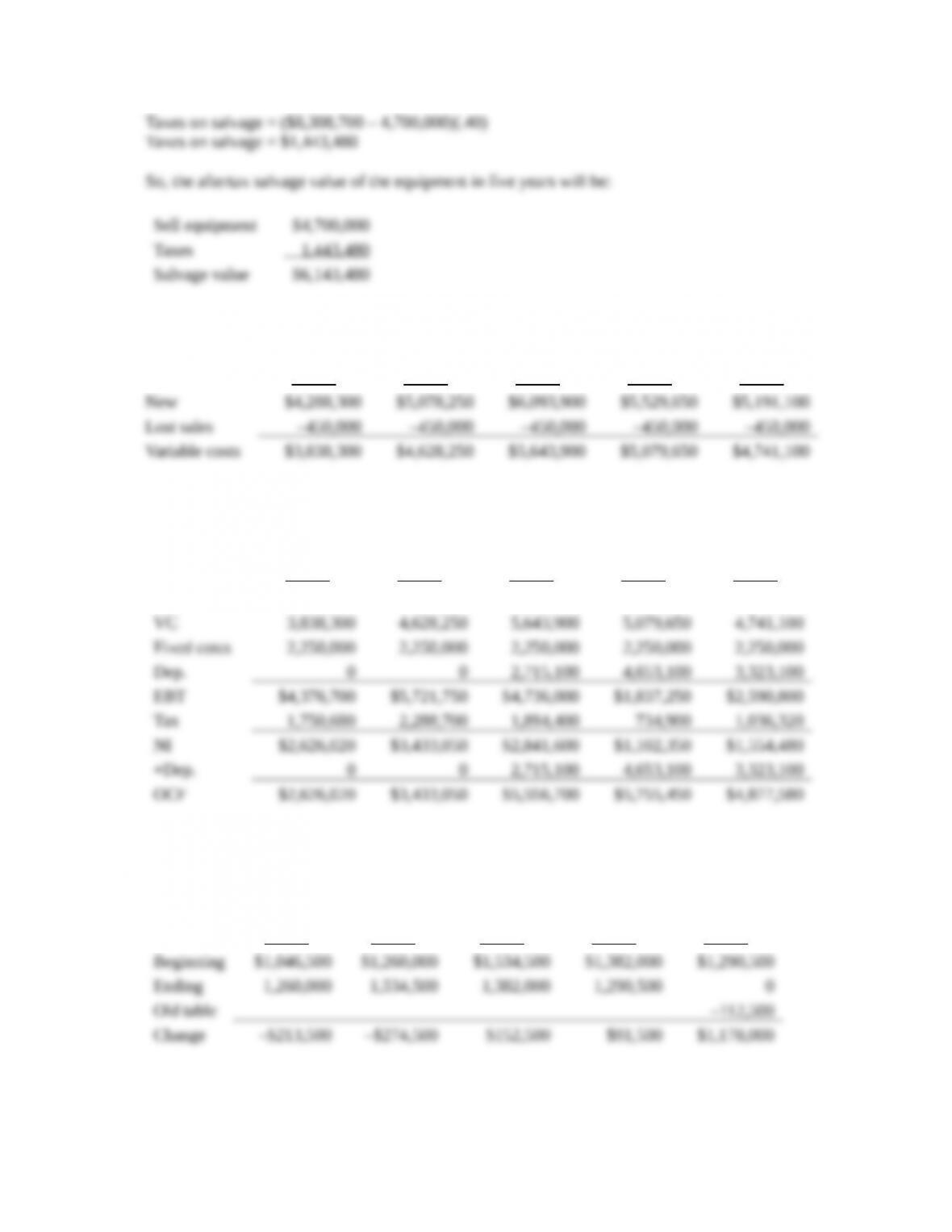

The taxes on the salvage value will be:

8

CHAPTER 6 –

Next, we need to calculate the variable costs each year. The variable costs of the lost sales are

included as a variable cost savings, so the variable costs will be:

Year 1 Year 2 Year 3 Year 4 Year 5

Now we can prepare the rest of the pro forma income statements for each year. The project will have

no incremental depreciation for the first two years as the equipment is not purchased for two years.

Adding back depreciation to net income to calculate the operating cash flow, we get:

Year 1 Year 2 Year 3 Year 4 Year 5

Sales $10,465,000 $12,600,000 $15,345,000 $13,820,000 $12,905,000

Next, we need to account for the changes in inventory each year. The inventory is a percentage of

sales. The way we will calculate the change in inventory is the beginning of period inventory minus

the end of period inventory. The sign of this calculation will tell us whether the inventory change is a

cash inflow, or a cash outflow. The inventory each year, and the inventory change, will be:

Year 1 Year 2 Year 3 Year 4 Year 5

Notice that we recover the remaining inventory at the end of the project. We must also spend

$112,500 for inventory since the 250 units per year in sales of the oak table will begin again. The

9

CHAPTER 6 –

total cash flows for the project will be the sum of the operating cash flow, the capital spending, and

the inventory cash flows, so:

Year 1 Year 2 Year 3 Year 4 Year 5

The NPV of the project, including the inventory cash flow at the beginning of the project, will be:

The company should go ahead with the new table.

b. You can perform an IRR analysis, and would expect to find three IRRs since the cash flows

c. The profitability index is intended as a “bang for the buck” measure; that is, it shows how much

shareholder wealth is created for every dollar of initial investment. This is usually a good

10